Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

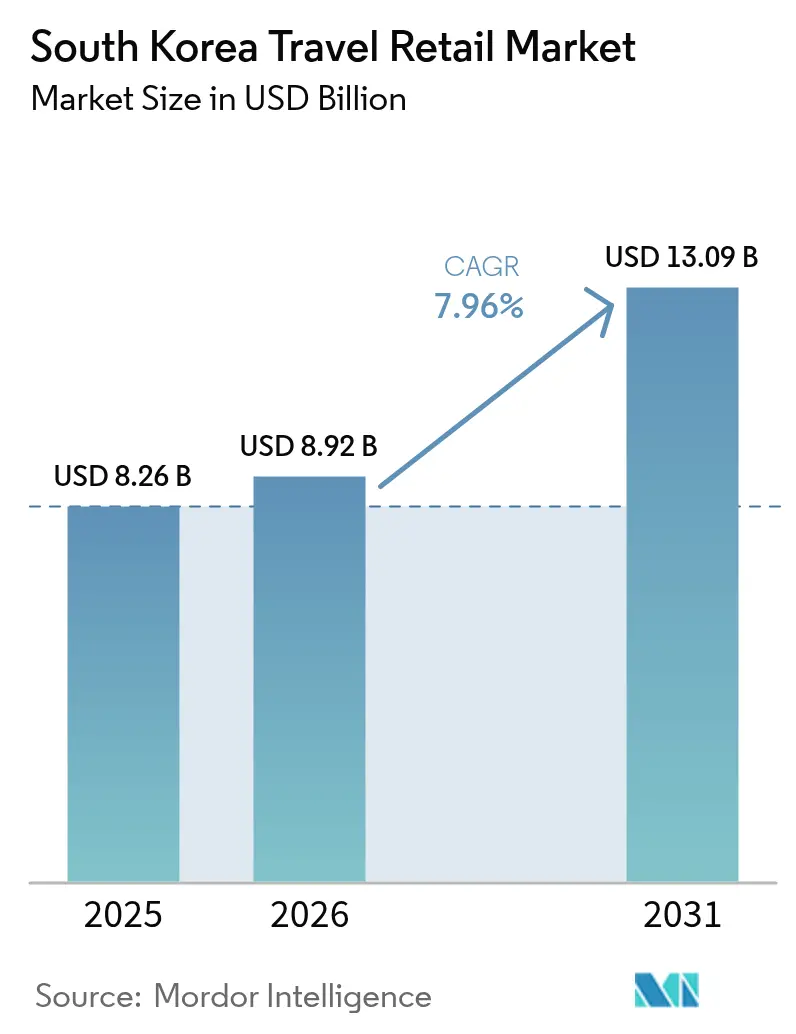

| Base Year Market Size (2025) | USD 8.26 Billion |

| Market Size (2026) | USD 8.92 Billion |

| Market Size (2031) | USD 13.09 Billion |

| Growth Rate (2026 - 2031) | 7.96% CAGR |

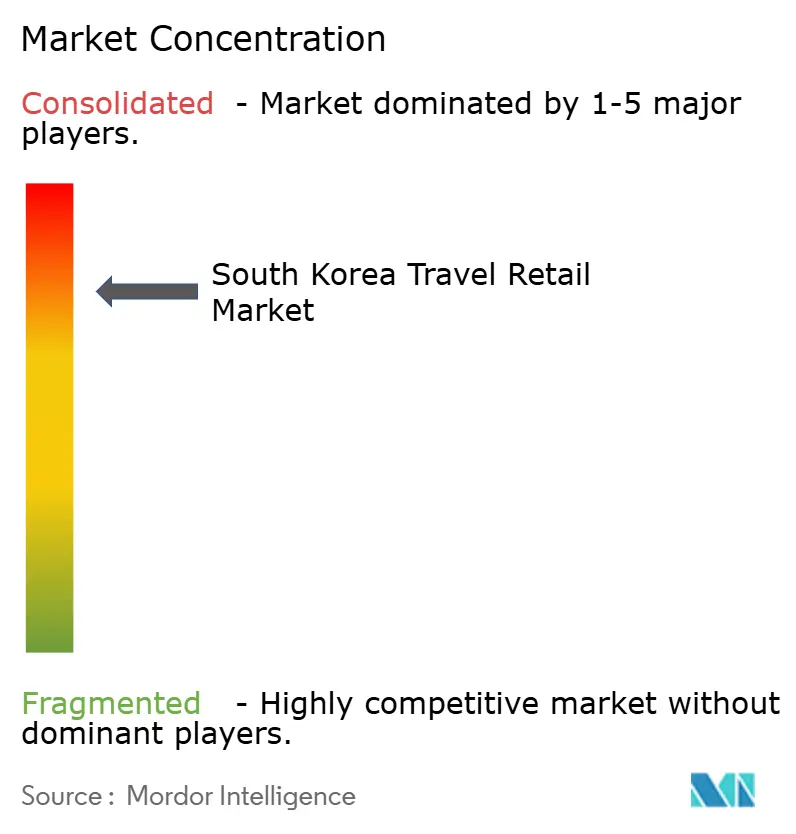

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Travel Retail Market Analysis by Mordor Intelligence

The South Korea travel retail market size is expected to grow from USD 8.26 billion in 2025 to USD 8.92 billion in 2026 and is forecast to reach USD 13.09 billion by 2031 at 7.96% CAGR over 2026-2031. This performance demonstrates a robust rebound from pandemic-era disruption as flight schedules normalize, cruise itineraries resume, and the policy environment turns supportive. Demand is anchored by the return of group tours from mainland China, historically the single largest spending cohort, alongside steady gains from other Asian source markets and the United States. Retailers are also benefiting from the government’s decision to raise duty-free alcohol limits to 2 liters at a higher value ceiling and to expand the perfume allowance to 100 ml, thereby widening the typical tourist basket. Operators have rapidly scaled AI-powered dynamic pricing systems that recalibrate shelf prices multiple times per day, improving conversion and margin management while supporting inventory optimization. New revenue streams are emerging from growing cruise passenger volumes in Busan and Jeju, the proliferation of medical wellness tourism, and the bundling of K-culture merchandise that monetizes the global Hallyu wave. Although airport concessions remain the dominant channel, consumers increasingly seek seamless omnichannel experiences that integrate pre-order mobile platforms, downtown pick-up, and immediate tax-refund services, signaling the next phase of digital transformation in the South Korea travel retail market.

Key Report Takeaways

- By product type, fragrances & cosmetics commanded 39.94% revenue share of the South Korea travel retail market in 2025, while Wine and Spirits is forecast to post the fastest 15.33% CAGR through 2031.

- By distribution channel, airport stores held 82.12% of South Korea travel retail market share in 2025; cruise liners are set to expand at an 17.78% CAGR to 2031 as Busan consolidates its status as a Northeast Asian cruise hub.

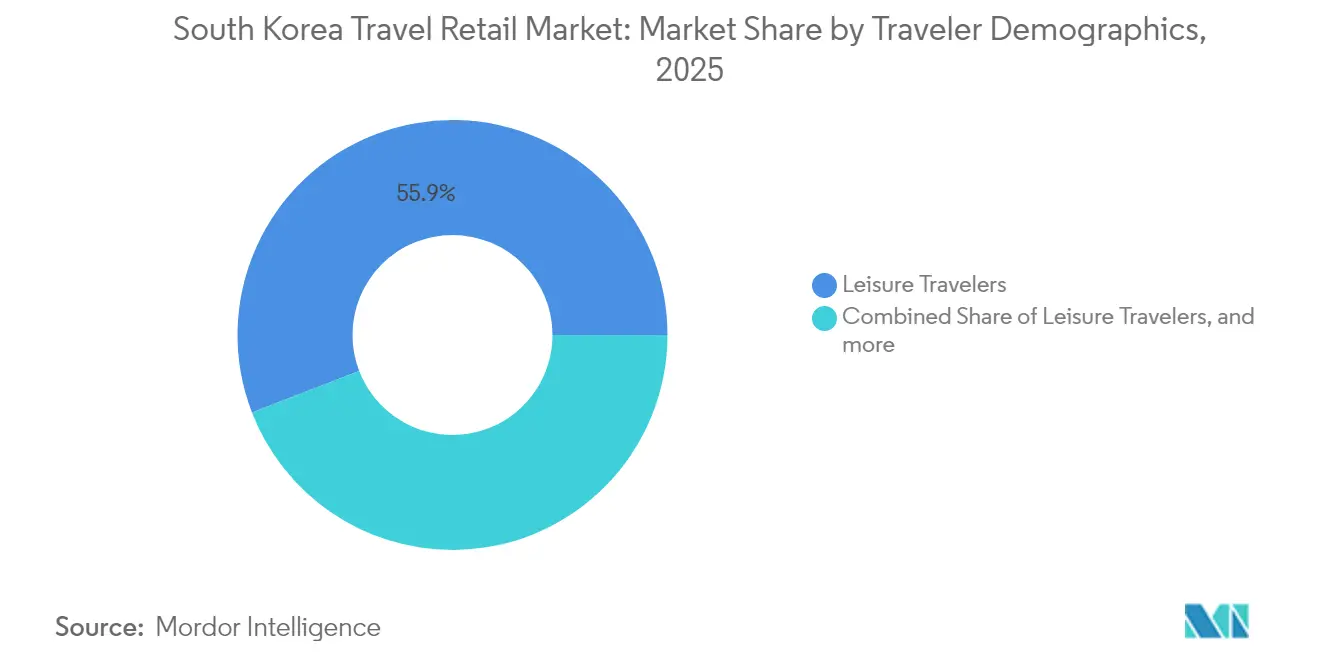

- By traveler demographic, leisure tourists accounted for 55.86% of the South Korea travel retail market size in 2025, whereas medical and wellness tourists are projected to grow at a 13.01% CAGR through 2031 as cosmetic-surgery demand escalates.

- By geography, the Seoul Capital Region retained 68.71% share of the South Korea travel retail market in 2025; Jeju Island is advancing at an 11.05% CAGR on the back of cruise tourism recovery and wellness positioning.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Return of Chinese group tours & easing visa rules | +2.1% | APAC core, spill-over to Seoul Capital Region | Medium term (2-4 years) |

| Increased duty-free alcohol allowance & tobacco quota adjustments | +1.3% | Global, concentrated in Seoul & Jeju | Short term (≤ 2 years) |

| K-culture fandom-driven merchandise bundling | +1.8% | Global, strongest in APAC and North America | Long term (≥ 4 years) |

| AI-powered dynamic pricing & digital twin store fronts | +0.9% | National, early gains in Seoul, Busan, Jeju | Medium term (2-4 years) |

| Rising demand for premium tequila & craft spirits | +0.7% | Global, led by Seoul Capital Region | Medium term (2-4 years) |

| Resumption of cruise itineraries boosting port retail footfall | +1.2% | APAC core, focused on Busan & Jeju | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Return of Chinese Group Tours & Easing Visa Rules

The reinstatement of organized tours from mainland China has restored the largest single demand pillar for the South Korea travel retail market, given that Chinese visitors historically generated 80-90% of duty-free sales volumes[1]Source: Kwon Young-sun, “S.Korea's duty-free industry going downhill,” KED Global, kedglobal.com. Passenger throughput at Korean airports reached 91% of 2019 levels by February 2024, yet spending patterns have tilted toward locally manufactured products, signaling evolving taste preferences. Authorities are weighing visa-free entry for Chinese group travelers, a move expected to elevate arrivals beyond the Korea Tourism Organization’s 18.5 million foreign-visitor target for 2025. Retailers are responding by curating assortments that blend K-beauty, cultural souvenirs, and premium international brands to appeal to value-seeking tourists. Enhanced customs monitoring now differentiates legitimate shoppers from commercial resellers, reshaping in-store service protocols and loyalty programs. Over the medium term, operators that localize merchandising and embed Mandarin-enabled digital engagement tools stand to capture outsize share of the incremental inflow.

Increased Duty-Free Alcohol Allowance & Tobacco Quota Adjustments

The Korea Customs Service’s removal of quantity caps, while retaining a 2-liter and USD 400 ceiling, expands spending headroom and diversifies the typical duty-free basket[2]Source: Kim So-young, “S. Korea seeks to raise duty-free allowance limit for alcohol,” The Korea Herald, koreaherald.com. The policy dovetails with South Korea’s emergence as the world’s fastest-growing whisky market, which posted 46% consumption growth since 2021 despite a 72% liquor tax rate. Duty-free operators have launched bundled promotions featuring miniatures and curated gift sets to maximize volume within regulatory limits, buoying average transaction values. Licensing approvals for domestic distilleries rose by 275 in 2023, indicating supply-side responsiveness to premium-spirits demand. Millennials and Gen Z shoppers, who equate alcohol with experiential luxury, are driving trial of craft tequila and high-end rum. This demographic alignment supports continued double-digit value growth in the wine and spirits segment of the South Korea travel retail market.

K-Culture Fandom-Driven Merchandise Bundling

The global popularity of K-pop, K-dramas, and Korean cinema has transformed tourism motivations and elevated shopping to a primary trip purpose. At Olive Young’s Myeong-dong Global Store, 90% of the 3,000 daily visitors are foreign tourists hunting for authentic Korean cosmetics[3]Source: Lee Hyo-jung, “Experience Hassle-free K-beauty Shopping and Immediate Tax Refunds at Olive Young,” Korea Tourism Organization, visitkorea.or.kr. Duty-free shops now collaborate with entertainment agencies to release limited-edition products, live-stream meet-and-greet events, and offer augmented-reality photo zones. Cultural exports linked to Hallyu expanded 22.4% in 2019 and continue to underpin brand equity around the world. By bundling cosmetics, collectibles, and concert tickets, retailers create higher-margin experiential packages that differentiate them from cross-border e-commerce alternatives. Over the long term, fandom monetization is expected to widen the revenue base and deepen customer stickiness in the South Korea travel retail market.

AI-Powered Dynamic Pricing & Digital Twin Store Fronts

Retailers have embraced artificial intelligence to algorithmically adjust prices based on shopper demographics, flight schedules, and real-time inventory, lifting both conversion and margin. Retail media networks now a USD 2 billion segment are projected to climb to USD 10 billion as operators commercialize first-party data for targeted advertising. Virtual store twins allow travelers to preview assortments online and reserve items before arrival, shortening in-store dwell times while alleviating congestion. The Trip.PASS mobile passport, launched nationwide in 2025, enables instant tax refunds at convenience stores, illustrating public-sector alignment with digital payment adoption. Combined, these technologies compress operational costs, improve stock accuracy, and enrich customer experience, positioning early adopters to outperform within the South Korea travel retail market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory crackdown on daigou resellers | -1.4% | APAC core, concentrated in Seoul downtown locations | Short term (≤ 2 years) |

| Escalating concession fees at Incheon & regional airports | -0.8% | National, primary impact on Seoul Capital Region | Medium term (2-4 years) |

| Slow recovery of Chinese outbound group travel | -2.0% | National, with high dependency in Seoul and Jeju duty-free zones | Short to medium term (1–3 years) |

| Stringent import regulations on luxury goods | -1.1% | National, with elevated impact on high-end duty-free segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Crackdown on Daigou Resellers

Stricter customs enforcement has dampened high-volume purchases by professional buyers who previously moved bulk cosmetics and luxury goods into mainland China. The Fair Trade Commission’s probe into platforms such as AliExpress and Shein underscores the broader clampdown on gray-market channels. Downtown duty-free shops have responded by tightening purchase limits, installing RFID-based transaction monitoring, and requiring additional passport verification. While these steps protect brand integrity and tax revenue, they suppress turnover in low-margin SKUs that once relied on daigou traffic. Over time, retailers must pivot toward higher-value, experience-led propositions to offset lost volume. In the near term, the policy drag reduces the South Korea travel retail market CAGR by an estimated 1.4%.

Escalating Concession Fees at Incheon & Regional Airports

Incheon International Airport Corporation’s decision to terminate pandemic-era rent relief reinstates pre-crisis cost structures just as operators rebuild sales. Lotte Duty Free posted a USD 34.6 million loss in H1 2024, illustrating the cash-flow squeeze caused by fixed-fee escalation amid recovering but still volatile demand[4]Source: Retail in Asia staff, “Korean travel retail struggles continue as ‘big four’ see profits tumble,” retailinasia.com. Regional airports contemplate similar policies, pressuring margins across the network. Operators are renegotiating contracts, optimizing floor layouts, and pruning under-performing SKUs to preserve profitability. Should passenger growth stall, elevated fixed costs could accelerate consolidation and elevate barriers to entry, potentially limiting competitive diversity in the South Korea travel retail market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: K-Beauty Supremacy Meets Premium Spirits Momentum

Fragrances & Cosmetics retained a 39.94% slice of the South Korea travel retail market in 2025 on the strength of Korea’s global reputation for innovative skincare and color cosmetics. Buss loads of tourists line up outside landmark stores in Myeong-dong, while digital pre-order platforms secure repeat purchases among outbound Korean travelers who prefer click-and-collect convenience. The South Korea travel retail market size for fragrances & cosmetics is projected to expand in line with overall throughput, supported by brand collaborations and AI-driven skin diagnostics that personalize upselling. Fashion and accessories, with an 10.84% share, lean on limited-edition drops and capsule collections to stay relevant amid rising cross-border e-commerce competition. Tobacco, once a mainstay, continues to lose share because of tightened vaping rules and younger consumers shifting to alternative nicotine formats.

Conversely, wine and spirits is charging forward at a 15.33% CAGR through 2031 as consumers explore high-end tequila and craft whiskies. The South Korea travel retail market share of wine and spirits is therefore on an upward trajectory despite the country’s steep liquor taxes. Operator merchandising now includes experiential tasting bars, QR-based product storytelling, and NFT-enabled authenticity verification. Food and confectionery maintains a steady 11.12% contribution, driven by gift-giving customs among Asian travelers, while electronics and luxury watches suffer substitution risk from online discounters. Overall, the portfolio effect provides a hedge: beauty preserves volume leadership, spirits delivers incremental margin, and cultural confectionery anchors entry-level purchases.

By Distribution Channel: Airport Stronghold Faces Nautical Upside

Airport stores controlled 82.12% of South Korea travel retail market sales in 2025, underpinned by Incheon’s role as a super-connector gateway linking Northeast Asia to North America and Europe. Store footprints resemble mini-shopping malls, complete with digital walls, livestream studios, and robotic baristas that elevate the passenger experience. The South Korea travel retail market size attributed to airports is poised to grow in tandem with seat capacity additions from Korean Air and Asiana’s planned long-haul expansion. However, cruise liners represent the fastest-rising channel with an 17.78% CAGR, fueled by Busan’s designation as a regional cruise hub and Jeju’s ongoing port-upgrade program.

Railway-station duty-free remains a 1.02% niche, partly because domestic travelers can already access similar products online. Downtown channels, once buoyed by daigou activity, confront structural decline, prompting operators to convert legacy stores into immersive showrooms and last-mile pick-up hubs. The mixed-channel mix ensures redundancy; when pandemic shocks cut aviation throughput, cruise and online pre-order platforms absorbed some of the lost revenue. Looking forward, omnichannel integration, allowing inventory pooling across airport, cruise, and downtown nodes, will be critical to safeguarding growth in the South Korea travel retail market.

By Traveler Demographics: Leisure Anchor with Wellness Tailwinds

Leisure travelers supplied 55.86% of 2025 sales, reinforcing tourism’s centrality to the sector’s economics. They are motivated by K-pop attractions, flagship beauty stores, and the cachet of purchasing duty-free luxury items in Seoul. Business travelers, at 17.74%, have not fully recovered to pre-pandemic spending intensity because corporate budgets remain lean and virtual alternatives persist. Visiting friends and relatives account for 9.06%, but their per-capita spend is lower, often centered on confectionery.

Medical and wellness tourists are the breakout cohort, expanding at a 13.01% CAGR as favorable foreign-exchange rates and Korea’s world-class cosmetic-surgery ecosystem lure patients from China, Vietnam, and the Middle East. The South Korea travel retail market responds with curated post-procedure skincare kits and personalized shopping concierge services that cater to restricted-mobility travelers. Student travelers, comprising 10.12%, are another strategic target owing to their social-media amplification power. Combined, the demographic mosaic implies a balanced demand base that cushions the South Korea travel retail market against volatility in any single segment.

Geography Analysis

Seoul Capital Region commanded 68.71% of the South Korea travel retail market in 2025, thanks to Incheon International Airport’s dominant position, dense downtown retail, and the city’s allure as a K-beauty pilgrimage site. The capital’s infrastructure advantage is reinforced by the February 2025 rollout of e-Arrival cards, which simplify immigration procedures and increase passenger dwell time. Nevertheless, reliance on a single metropolitan area exposes operators to any future air-traffic shock or regulatory shift.

Jeju Island is the fastest-growing geography, expanding at an 11.05% CAGR as cruise lines restore calls and medical wellness retreats proliferate. The island’s special administrative regime offers flexible visa policies and tax incentives that foster retail innovation. Chinese travelers, in particular, appreciate Jeju’s visa-free entry, making the island an accessible shopping destination even during bilateral diplomatic strains.

Busan and the broader southeastern corridor held an 8.12% share, poised for uplift once the USD 10.5 billion Gadeokdo New Airport opens in December 2029. Upgraded cruise terminals also channel incremental footfall into portside duty-free zones. The residual 12.25% share is spread across secondary cities and regional airports, where growth is moderate yet strategically important for domestic tourism dispersal. Geographic diversification, therefore, remains a strategic imperative to fortify the South Korea travel retail market against localized disruptions.

Competitive Landscape

The South Korea travel retail market is highly concentrated, with a small group of major players dominating overall revenues. Lotte Duty Free leads the market, driven by its broad presence across major airports and a well-developed digital membership program that boosts customer engagement. The Shilla Duty Free holds a strong position as well, setting itself apart through exclusive partnerships with premium brands and an expanding international footprint, including operations in Singapore, Hong Kong, and upcoming locations in Phuket and Tokyo. Shinsegae Duty Free, Hyundai Department Store Duty Free, and Hanwha Galleria also play key roles, together accounting for a substantial portion of the market.

Margin pressure persists as concession fees normalize and labor costs edge higher, prompting a focus on operational efficiency and tech-driven personalization. AI-enabled price engines, mobile checkout, and retail media networks are common investment themes across leading operators. International diversification acts as a hedge; for instance, Lotte Duty Free’s Dior pop-up at Da Nang Airport reflects a strategy of exporting Korean retail know-how to fast-growing Southeast Asian markets.

White-space opportunities include cruise retail, medical tourism concierge services, and K-culture merchandise, areas where smaller specialists can carve a niche. Cross-border e-commerce platforms remain disruptive, but ongoing crackdowns on daigou resellers offer traditional players a respite. Strategic alliances between retailers and beauty conglomerates exemplified by Coty’s updated joint business plan with The Shilla Duty Free signal a shift toward vertically integrated product pipelines that secure exclusive demand generators. Overall, technology adoption speed and merchandising agility will determine competitive advantage over the next cycle of the South Korea travel retail market.

South Korea Travel Retail Industry Leaders

Lotte Duty Free

The Shilla Duty Free

Shinsegae Duty Free

Hyundai Department Store Duty Free

Hanwha Galleria Duty Free

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Korea Tourism Organization introduced an e-Arrival card, replacing paper forms and streamlining entry processes to boost visitor experience and retail dwell time.

- February 2025: Lotte Tour Development recorded operating income of KRW 39.21 billion (USD 27.2 million) for 2024, a 50.4% sales increase signaling sector recovery.

- July 2024: The Shilla Duty Free opened a flagship liquor store at Incheon Airport, capitalizing on expanded duty-free alcohol allowances.

- July 2024: Lotte Duty Free launched a Dior concept store at Da Nang Airport as part of its international diversification push.

South Korea Travel Retail Market Report Scope

Travel Retail is commonly used to describe the duty-free retail industry and all retail activities dedicated to travelers and tourists. A complete background analysis of the market, including the estimation of market size and forecast, market shares, industry trends, growth drivers, and vendors, is provided. The study also includes insights into market segmentation by product type and distribution channel. Additionally, the report features qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across key points in the industry’s value chain.

The Market is segmented by product type (beauty and personal care, wines and spirits, tobacco, eatables, fashion accessories and hard luxury, and other types), by distribution channel (airports, airlines, ferries, and other distribution channels).

The report offers market size and forecasts for the South Korea travel retail market in terms of value (USD) for all the above segments.

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionary |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends & Relatives (VFR) |

| Medical & Wellness Tourists |

| Student Travelers |

By Geography

| Seoul Capital Region (Incheon & Downtown) |

| Jeju Island |

| Busan & Southeastern Region |

| Other Regions |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionary | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends & Relatives (VFR) | |

| Medical & Wellness Tourists | |

| Student Travelers | |

| By Geography | Seoul Capital Region (Incheon & Downtown) |

| Jeju Island | |

| Busan & Southeastern Region | |

| Other Regions |

Key Questions Answered in the Report

What is the current value of the South Korea travel retail market?

The market is valued at USD 8.92 billion in 2026 and is projected to reach USD 13.09 billion by 2031.

Which product category holds the largest share in South Korea travel retail?

Fragrances & Cosmetics leads with 39.94% share thanks to Korea’s globally recognized K-beauty brands.

How fast is the wine and spirits segment growing?

Wine and spirits is expanding at a 15.33% CAGR, the fastest among all product groups.

Why is Jeju Island considered a high-growth geography?

Jeju benefits from cruise tourism recovery, visa-free entry for certain nationalities, and a strong medical-wellness proposition, resulting in an 11.05% CAGR.

Page last updated on: