Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.77 Billion |

| Market Size (2026) | USD 20.70 Billion |

| Market Size (2031) | USD 33.78 Billion |

| Growth Rate (2026 - 2031) | 10.30% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Travel Retail Market Analysis by Mordor Intelligence

The China Travel Retail Market size is expected to grow from USD 18.77 billion in 2025 to USD 20.7 billion in 2026 and is forecast to reach USD 33.78 billion by 2031 at a 10.30% CAGR over 2026-2031. Hainan Free Trade Port’s December 2025 shift to island-wide special customs operations reduced import costs and enabled competitive pricing against mainland channels, boosting duty-free operator conversions as the China travel retail market expanded. Civil aviation volumes in 2025 reached 770 million passengers, with international routes rebounding strongly, increasing store traffic and demand across categories. Fragrances and cosmetics accounted for the highest revenue share in 2025, while wine and spirits emerged as the fastest-growing category, a trend expected to continue through 2031. These developments supported margin growth and investments in experiential retail. Cruise retail is projected to grow faster than other formats as partnerships expand shipboard footprints, and homeports increase sailings, creating new opportunities to engage high-intent shoppers in the China travel retail market.

Key Report Takeaways

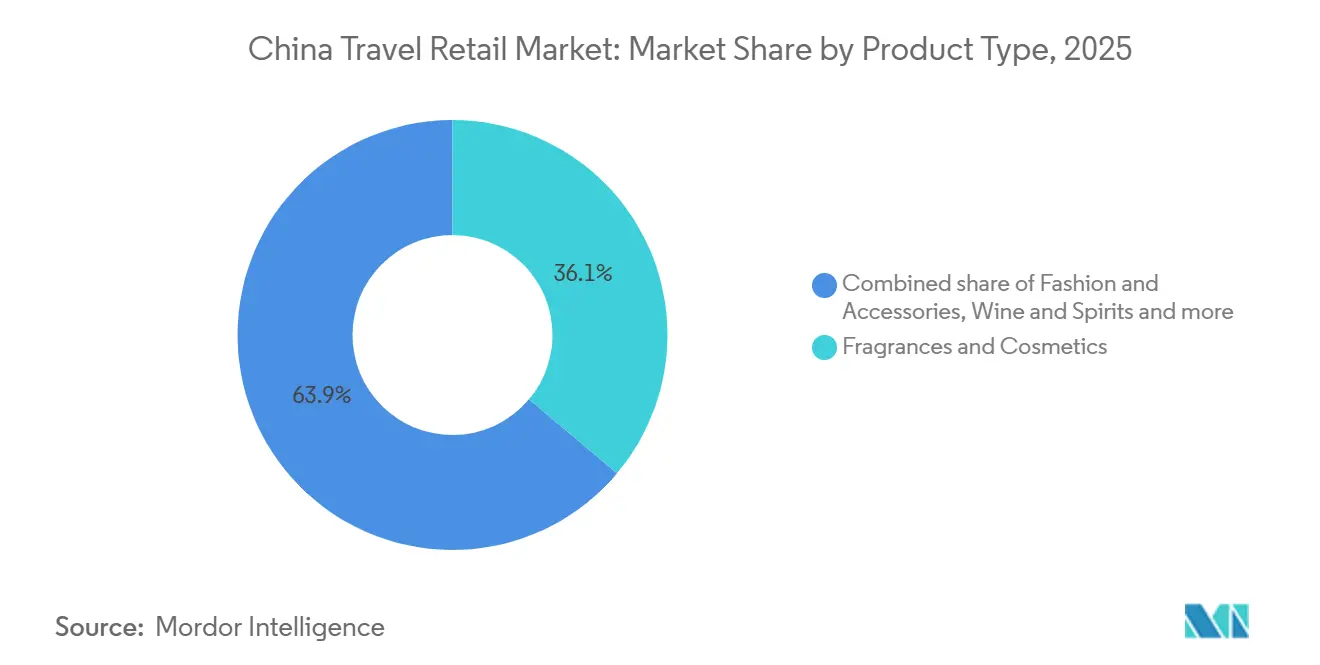

- By product type, fragrances and cosmetics led with 36.12% of the China travel retail market share in 2025. Wine and spirits are forecast to expand at an 11.18% CAGR through 2031.

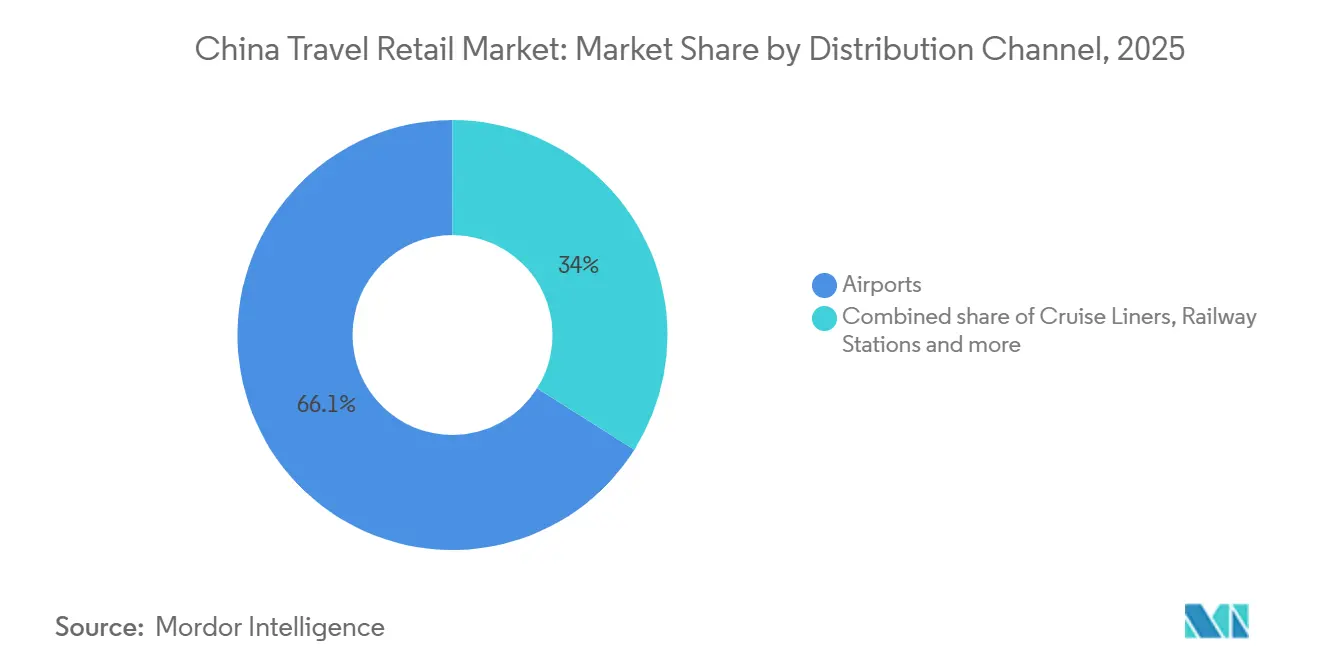

- By distribution channel, airports held 66.05% of the China travel retail market share in 2025. Cruise liners are forecast to expand at a 13.55% CAGR through 2031.

- By traveler demographics, leisure travelers accounted for 47.05% of the China travel retail market share in 2025. Student travelers are forecast to expand at a 12.68% CAGR through 2031.

- By geography, Hainan Province accounted for 29.82% of the China travel retail market share in 2025. Southwest China is forecast to record a 9.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Offshore duty‑free quota expansion and Hainan Free Trade Port policies are accelerating growth | +2.8% | Hainan Province; spillover effects to South-Central and Southwest China | Medium term (2-4 years) |

| Domestic and outbound passenger traffic is rebounding strongly post‑COVID | +2.5% | Global; concentration in North China (Beijing), East China (Shanghai, Hangzhou), South-Central China (Guangzhou, Shenzhen) | Short term (≤ 2 years) |

| Chinese travelers are increasingly trading up to premium beauty and luxury products | +1.9% | First-tier and new first-tier cities (Beijing, Shanghai, Guangzhou, Shenzhen, Chengdu); Hainan Province | Long term (≥ 4 years) |

| Experiential digital‑heritage retail concepts are boosting shopper spending | +1.4% | Tier-1 urban hubs (Shanghai, Beijing); Hainan resorts; select high-speed rail corridors | Medium term (2-4 years) |

| Ultra‑high‑net‑worth private‑jet lounge retailing is gaining momentum | +0.6% | Beijing, Shanghai, Guangzhou, Shenzhen, Hangzhou, Macau, Hong Kong | Long term (≥ 4 years) |

| AI‑driven personalization and virtual shopping concierges are enhancing customer engagement | +1.9% | Tier-1 and Tier-2 urban airports and downtown duty-free stores | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Offshore duty‑free quota expansion and Hainan Free Trade Port policies are accelerating growth

Hainan Free Trade Port implemented island-wide special customs operations in December 2025, expanding zero-tariff eligibility from 1,900 to 6,600 tariff lines, covering 74% of all imports. This initiative accelerated port clearances, reducing import frictions for duty-free operators[1]China Briefing, “Hainan’s 30 Percent Added Value Rule,” China Briefing, china-briefing.com. The model allows "freer access at the first line" for inbound overseas goods and "regulated access at the second line" for transfers between Hainan and the mainland, improving logistics flexibility and supporting value addition on the island. A 30% value-added threshold enables qualifying Hainan-processed goods to enter the mainland duty-free, encouraging localized finishing and assembly while enhancing margins in China's travel retail market. In November 2025, national measures expanded the offshore product catalog to include electronics and lifestyle goods and required duty-free shops to allocate space for domestic brands, diversifying traveler offerings and promoting Chinese brands. The annual offshore quota remains at CNY 100,000 (USD 14,282.5), providing significant capacity for purchases and positioning Hainan as a competitive option for eligible goods in China's travel retail market.

Domestic and outbound passenger traffic is rebounding strongly post‑COVID

China's civil aviation system transported 770 million passengers in 2025, reflecting a 5.5% year-on-year increase. International routes expanded the shopper base for airport and downtown retail. Outbound traffic increased on routes to Central Asia, West Asia, Africa, and Latin America, diversifying customer flows and reducing seasonal fluctuations in duty-free sales. Ningbo Lishe International Airport processed 1.0711 million passengers in 2025, with outbound duty-free sales rising 94.27% year-on-year to CNY 6.94 million (USD 0.99 million), indicating renewed cross-border demand at secondary gateways. Hainan's offshore duty-free sales reached CNY 30.94 billion (USD 4.42 billion) in 2024, serving 5.683 million shoppers. The first week after December 2025's customs regime change generated CNY 736 million (USD 105.1 billion) in Sanya sales, highlighting the policy's immediate impact on the travel retail market. Variations in outbound performance across key destinations were shaped by currency and policy factors, influencing channel preferences and spending patterns as the market scaled.

Premiumisation of Beauty and Luxury Categories Among Chinese Travellers

Fragrances and cosmetics accounted for 36.12% of revenue in China's travel retail market in 2025. Beauty brands used AI skin diagnostics, AR try-on mirrors, and personalized gifting to increase dwell times and transaction values at flagship stores. Estée Lauder reported 3% organic net sales growth in fiscal Q1 2026, driven by travel retail activations with Jo Malone, Le Labo, and Tom Ford during Golden Week in partnership with CDFG in Sanya, indicating improved conversion in North Asia. Wine and spirits are growing at an 11.18% CAGR through 2031, supported by whisky-focused offerings where higher-end labels generate significant margins despite lower volumes. China Duty Free Group’s “Malt & More Whisky by cdf” concept combines tastings, heritage storytelling, and exclusive bottlings to attract consumers to higher segments. Cognac faced challenges after China’s Ministry of Commerce imposed five-year anti-dumping tariffs of 27.7% to 34.9% in July 2025, following a duty-free resupply halt in December 2024. Martell resumed duty-free sales in fiscal Q2 2026, aiding Pernod Ricard’s travel retail recovery, though full-year performance depends on tariff resolution and inventory adjustments.

Experiential digital‑heritage retail concepts are boosting shopper spending

Airports and downtown duty-free locations in China are becoming experience-focused spaces, combining technology and cultural storytelling to boost engagement and conversions. Multi-brand pop-ups in Sanya have recreated travel journeys with product discovery, personalized services, and shareable digital content, increasing average transaction values during events. Interactive and AR-enabled experiences drive beauty activations, while brand collaborations with operators enhance traffic and repeat visits. Pilot programs at high-speed rail stations are testing duty-free formats that integrate local crafts and themed experiences, extending experiential retail beyond airports. Rising railway demand during Spring Festival 2026 highlights the potential for rail-side retail as capacity and services improve[2]Julia Charles Event Management, “Why Immersive Retail Works in Airports,” Julia Charles Event Management, juliacharleseventmanagement.co.uk.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shifting licensing rules and allowance limits are adding uncertainty to the market environment | -1.2% | National; acute impact on new entrants in Tier-2/3 cities | Short term (≤ 2 years) |

| Weak macroeconomic conditions are weighing on discretionary luxury purchases | -1.8% | Nationwide; disproportionate pressure on Northeast China (Liaoning, Heilongjiang) and inland provinces | Medium term (2-4 years) |

| Rising competition from downtown duty‑free and livestream e‑commerce is diverting sales | -0.9% | Tier-1 cities (Beijing, Shanghai, Guangzhou, Shenzhen); Hainan Province | Medium term (2-4 years) |

| Increasing ESG scrutiny is tightening shelf availability for tobacco and alcohol products | -0.4% | Global; compliance-driven reduction in North America and European airport concessions spilling into China JVs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shifting licensing rules and allowance limits are adding uncertainty to the market environment

The creation of 41 new duty-free store opportunities in January 2026, restricted to six approved Chinese entities, increases competition while limiting foreign operators' access, raising execution risks for global brands in China's travel retail market. Guangdong's portfolio adjustments added six inbound locations and discontinued some rail and port sites, highlighting how policy changes can quickly impact store-level economics. Delegating departure store approvals to provincial levels accelerates timelines but fragments quotas, retail criteria, and evaluation metrics, requiring precise navigation by operators and suppliers. New rules allowing downtown reservations with pickup at arrival ports enhance shopper convenience but complicate inventory control and shrink management across multiple fulfillment nodes. The exclusion of liquor and cosmetics from Hainan’s December 2025 tariff waivers sustains tax-related cost pressures on these key categories, limiting margin growth until the tax regime stabilizes[3]The Moodie Davitt Report, “Chinese Authorities Create 41 New Arrivals Duty-Free Store Opportunities,” The Moodie Davitt Report, moodiedavittreport.com.

Weak macroeconomic conditions are weighing on discretionary luxury purchases

Operators in 2025 faced challenges from subdued sentiment and increased online price competition. A retailer reported lower nine-month revenue and profits, though quarterly sales stabilized later in the year. Beauty brands experienced reduced contributions from travel retail compared to pandemic peaks, with weaker conversions in North Asia and consumers prioritizing value. Other brands reported a difficult first half in 2025, citing shifts in reseller dynamics and reduced spending by Chinese tourists, which lowered transaction sizes in key locations. In H1 FY26, a global spirits company reported a 31% decline in China sales due to a tighter high-end market, while noting steady demand for value-focused offerings. These trends emphasize the need for balanced pricing, targeted strategies, and inventory management as China’s travel retail market normalizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fragrance-Led Beauty Dominates, Spirits Drive Fastest Growth

Fragrances and cosmetics held a 36.12% market share in 2025, supported by service-oriented counters and technology-enabled discovery tools that increased dwell time and transaction sizes in airports and downtown locations. Wine and spirits are expected to grow at an 11.18% CAGR through 2031, driven by limited whisky and cognac releases, positioning duty-free as a controlled allocation channel in the China travel retail market. Brand owners introduced tasting-led concepts and heritage storytelling, attracting consumers to higher-value segments and enhancing category education in Hainan flagships. Spirit's performance in late 2025 and early 2026 reflected policy changes and inventory adjustments, with global disclosures showing uneven progress as Chinese channels rebalanced. Food, confectionery, tobacco, fashion, and electronics maintained steady roles, with electronics tailored for younger consumers and fashion operators restructuring store portfolios to align with traffic trends.

Skincare remained dominant in beauty, while makeup and perfume gained traction in 2024 and 2025 due to offline recovery and targeted male and Gen Z recruitment, boosting attachment rates. Spirits sub-categories focused on exclusive offerings and travel-specific editions to differentiate products and maintain pricing structures. Chinese beauty brands expanded into duty-free areas, including independent storefronts in Hainan, thereby diversifying their product lineups. Operators used cross-brand gifting and bundling strategies to increase basket sizes, as seen in multi-brand pop-ups in Sanya, combining services, personalization, and shareable content. Product curation and experience design continue to drive mix shifts and unit value growth, supporting the long-term development of the China travel retail market.

By Distribution Channel: Airports Anchor Volume, Cruise Liners Lead Expansion

Airports held 66.05% of the market share in 2025, serving as primary hubs for passenger volumes and hosting diverse retail brands. Cruise liners are expected to grow at a 13.55% CAGR through 2031, driven by expanded at-sea retail spaces and larger seasonal flows at homeports like Shanghai and Tianjin. Investments in cruise tourism infrastructure and travel retail resorts highlight voyages as key retail venues and consumer engagement platforms. Railside formats are testing duty-free concepts in high-traffic corridors, attracting millions of passengers and enabling themed activations. Downtown duty-free concessions enhance convenience by linking pre-order services with port pickups, ensuring inventory availability and efficient gate management.

Land ports and ferry terminals in South China expanded inbound duty-free designations in January 2026, tapping cross-border commuter flows as new demand sources. Guangdong’s updates aligned with downtown store rollouts in major cities, improving route coverage and shopper access. Cruise terminals adjusted staffing and shopping routes to handle increased passenger volumes, supporting market growth. Airport tenders at key hubs reinforced aviation retail’s central role while fostering competition among operators. This multi-format evolution ensures growth and resilience amid policy changes and traffic fluctuations in the China travel retail market.

By Traveller Demographics: Leisure Anchors Volume, Students Drive Growth

Leisure travelers made up 47.05% of sales in 2025, supported by domestic tourism recovery and event-linked shopping aligned with holidays and city-level promotional calendars. Student travelers are projected to grow at a 12.68% CAGR through 2031, driven by cross-border education and simplified digital payments that enhance confidence among digitally native consumers. Business travelers maintained higher transaction values at Tier-1 airports, though virtual meeting adoption moderated overall growth. Visiting friends and relatives, along with medical and wellness travelers, provided steady traffic tied to family and care-related incentives, adding resilience to category performance. Holiday periods and international visitor flows created additional demand surges, which operators leveraged through targeted activations and curated assortments.

Cruise tour groups showed strong purchasing intent in beauty and accessories, while independent travelers responded to tiered rewards and mobile payment incentives, boosting store throughput in 2025 and early 2026. Operators used event formats and gamified experiences to engage younger shoppers and build loyalty programs across channels. Male participation increased in high-end segments, while female consumers led unit volumes in core beauty categories. Segmentation informed retail design and media strategies, helping brands prioritize services, discovery tools, and exclusive editions. As payment systems standardize and digital pre-ordering becomes routine, operators can refine targeting and fulfillment strategies to support growth in student and leisure traveler segments.

Geography Analysis

Hainan Province held a 29.82% market share in 2025, supported by policy measures, store expansion, and the CNY 100,000 (USD 14,282.5) offshore shopping quota. Special customs operations were implemented island-wide, and zero-tariff product lines expanded to 6,637 items, reducing import costs and expediting clearance. Retail complexes hosted multi-brand activations, boosting sales during campaigns. Large-scale projects aim to enhance beauty and family entertainment offerings through 2026. Offshore duty-free sales reached CNY 30.94 billion (USD 4.42 billion) in 2024, with 5.683 million shoppers, creating a strong base for policy-driven growth. Liquor and cosmetics remained outside the zero-tariff scope, maintaining tax-related constraints until further adjustments[4]Global Times, “Chinese Authorities Announce New Duty-Free Measures,” Global Times, globaltimes.cn.

Southwest China is projected to grow at a 9.26% CAGR through 2031, driven by rail corridor expansion enabling duty-free pilots at high-traffic stations. Downtown duty-free concessions in Western and Northern cities expanded pre-order and pickup options, improving route coverage. East China’s aviation hubs scaled passenger traffic and tax refund infrastructure, while municipal plans supported tax-refund-on-departure stores. South-Central China added six inbound duty-free locations in January 2026 and discontinued others, focusing on cruise and cross-border commuter channels with sustained demand. Regional policy adjustments align retail formats with local traffic dynamics.

North China advanced airport tendering in late 2025, introducing multi-year concessions for refreshed brand portfolios and store investments. Northeast and Northwest regions, supported by visa-free policies and extended transit allowances, serve as gateways for travelers from Russia, Mongolia, and Central Asia. Secondary coastal terminals and island ports enhanced inbound duty-free capacity through coordinated cross-border programs, boosting local retail capture. Policy momentum across regions supports multi-format expansion in the China travel retail market. Investments in customer experience and technology along key corridors align with the core volume base in East and South China, while Hainan’s free trade framework offers structural advantages as the market matures.

Competitive Landscape

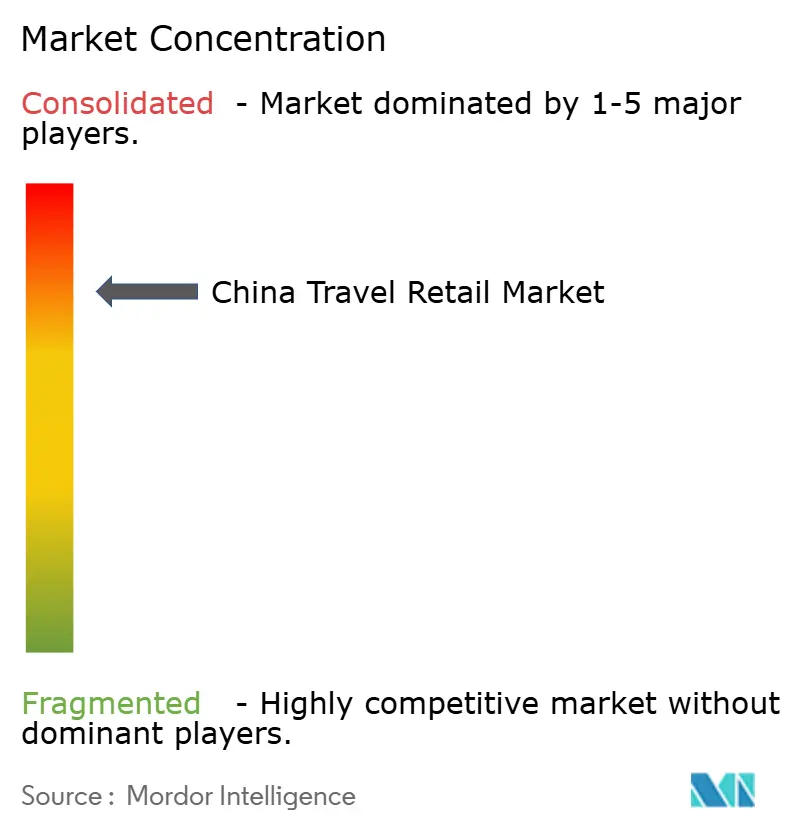

The duty-free sector in China is highly concentrated, with a state-backed operator expected to hold a 78.7% market share in 2024, further strengthening its position in Hainan by 2025. This dominance impacts pricing, concession policies, and supplier agreements. Approved entities control tender eligibility for new arrivals stores, while provincial delegation for departure shops fosters localized competition. Key strategies include omnichannel integration, enhanced customer experiences, and domestic brand inclusion, supported by regulations requiring store space for Chinese products with export-related tax benefits. Technology enhances retail operations through pre-order systems, app reservations, and on-site collection. Brands use activation calendars to promote discovery, trials, and gifting, consolidating shopper engagement across Hainan and Tier-1 airports.

Structural changes in 2026 included the sale of a major international operator’s Greater China retail business to China Tourism Group Duty Free, along with equity subscriptions into newly issued H-shares of the buyer. This transaction consolidates regional capabilities within a single platform supported by policy and network density. International players adjusted operations in Mainland China to recalibrate exposure and restore profitability through 2026 and 2027. Korean retailers focused on cruise channels as Chinese cruise activity increased, optimizing staffing and routes. Beauty brands aligned campaigns with operator-led experience zones to boost dwell time and social engagement.

Spirits companies managed tariffs and channel reactivation to stabilize global travel retail trends in Q2 FY26, despite uneven normalization. Airport authorities launched multi-terminal tenders in late 2025, shaping brand assortments and experiences at departures. South China introduced new inbound locations and discontinued others, prioritizing cruise and commuter corridors. Hainan’s large-scale projects aim to integrate retail and entertainment, ensuring resilience against market shifts. Policy, scale, and execution speed remain critical in determining market share trajectories.

China Travel Retail Industry Leaders

China Tourism Group Duty Free Corp. (CTGDF)

Shenzhen Duty Free Group Co., Ltd.

Sunrise Duty Free Co., Ltd.

Zhuhai Duty Free Group Co., Ltd.

Zhuhai Duty Free Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Authorities in China have approved 41 new duty-free stores at airports, seaports, and land border crossings across 19 provinces. Bidding is limited to six State Council-approved entities, with provincial authorities authorized to approve port departure stores.

- January 2026: DFS and China Tourism Group Duty Free finalized an agreement for the sale of DFS's Greater China retail business. LVMH and the Miller family will allocate a small portion of their proceeds to subscribe to newly issued H-shares of CTG Duty Free.

- December 2025: The Hainan Free Trade Port expanded zero-tariff eligibility from 1,900 to 6,637 tariff lines and implemented island-wide special customs operations, introducing process improvements to enhance logistics timelines.

- August 2025: Shenzhen's first downtown duty-free store opened at UpperHills through a partnership between China Duty Free Group, Shenzhen Duty Free Group, and Shum Yip Group. This development coincided with a rise in city-level duty-free sales in 2025.

China Travel Retail Market Report Scope

China's travel retail industry includes duty-free and travel-related retailing at airports, cruise terminals, railway stations, border zones, and offshore duty-free hubs. It offers products such as beauty, fashion, alcohol, tobacco, and confectionery to domestic and international travelers. The market is segmented by: Product Type: Fragrances & cosmetics, wine & spirits, tobacco, fashion & accessories, food & confectionery, and others. Distribution Channel: Airports, cruise liners, railway stations, and other channels. Traveler Demographics: Business, leisure, visiting friends and relatives (VFR), medical/wellness, and student travelers. Geography: East, South-Central, North, Northeast, Southwest, Northwest China, and Hainan Province. The report reviews the regulatory landscape, technological advancements, supply chain structure, and competitive dynamics. It includes profiles of major duty-free operators and travel retail players, highlighting strategies and market share insights. The study provides market size estimates and growth forecasts in value terms (USD) and concludes with emerging opportunities and the future outlook for China's travel retail industry.

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionery |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewellery, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends and Relatives (VFR) |

| Medical and Wellness Tourists |

| Student Travelers |

By Geography

| East China |

| South-Central China |

| North China |

| Northeast China |

| Southwest China |

| Northwest China |

| Hainan Province |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionery | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewellery, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends and Relatives (VFR) | |

| Medical and Wellness Tourists | |

| Student Travelers | |

| By Geography | East China |

| South-Central China | |

| North China | |

| Northeast China | |

| Southwest China | |

| Northwest China | |

| Hainan Province |

Key Questions Answered in the Report

What is the current size and growth outlook for the China travel retail market?

The China Travel Retail Market is currently valued at USD 18.77 billion in 2025, expected to grow to USD 20.7 billion in 2026, and is forecast to reach USD 33.78 billion by 2031 at a 10.30% CAGR over 2026–2031, reflecting strong growth momentum and expansion potential.

Which product category leads sales within China’s duty-free ecosystem?

Fragrances and cosmetics lead with 36.12% share in 2025, supported by immersive counters and services that elevate conversion at airports and large downtown locations.

Which channels are growing fastest in the China travel retail market?

Cruise liners are projected to be the fastest-growing channel at a 13.55% CAGR through 2031 as operators expand shipboard retail and homeports increase sailings.

How are Hainan policies influencing the China travel retail market?

Hainan launched island-wide special customs operations in December 2025 and expanded zero-tariff lines to 6,637, which reduces import costs and strengthens pricing competitiveness for many eligible products.

Which regions hold the greatest potential for incremental growth?

Southwest China is projected to grow at a 9.26% CAGR through 2031 as rail corridors expand, while Hainan maintains a leading share under free trade policies and large-scale retail projects.

What recent transactions could reshape competitive dynamics?

In January 2026, DFS agreed to sell its Greater China retail business to China Tourism Group Duty Free, with LVMH and the Miller family subscribing to newly issued H-shares of the buyer, which consolidates capabilities in the region.

Page last updated on: