US Location-based Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

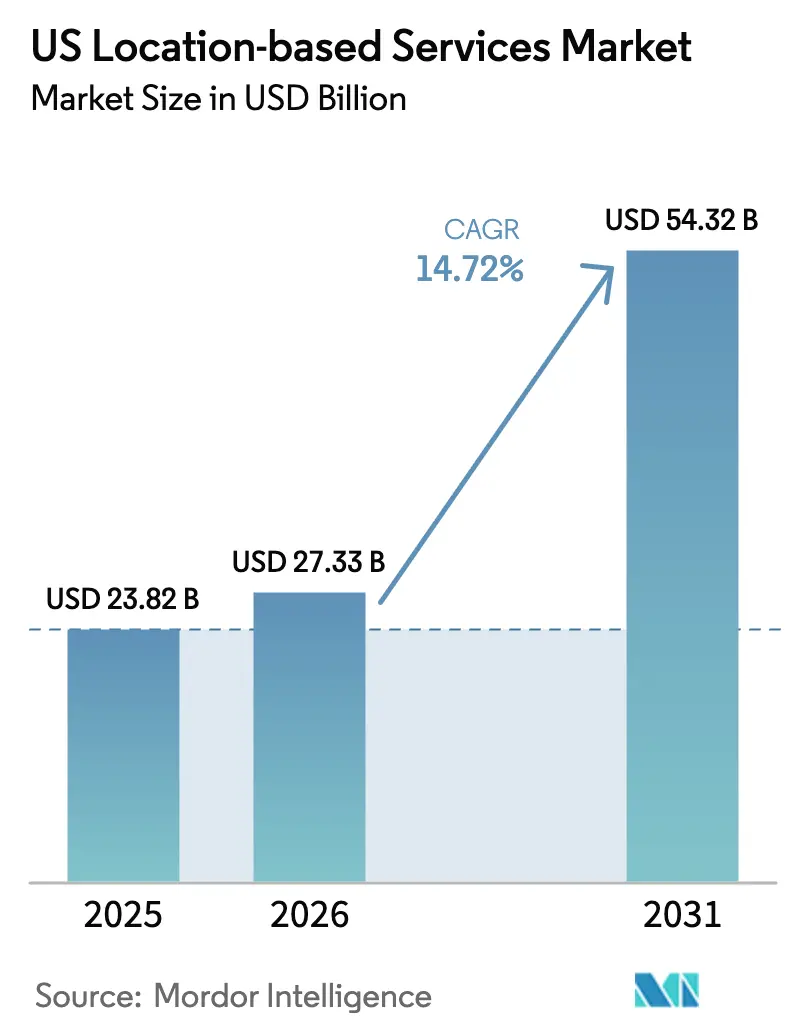

| Base Year Market Size (2025) | USD 23.82 Billion |

| Market Size (2026) | USD 27.33 Billion |

| Market Size (2031) | USD 54.32 Billion |

| Growth Rate (2026 - 2031) | 14.72% CAGR |

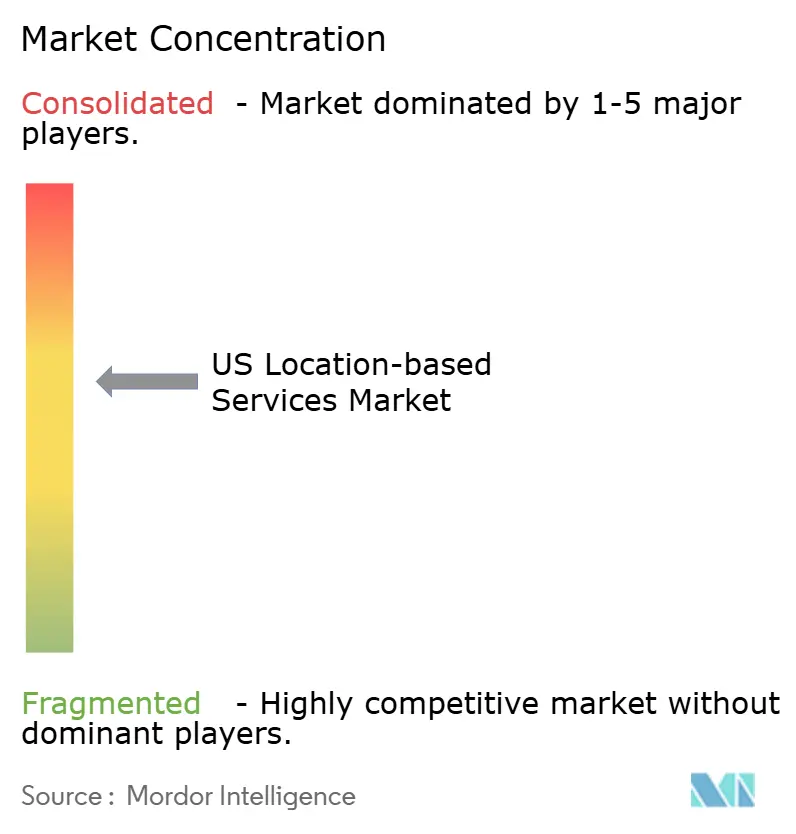

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Location-based Services Market Analysis by Mordor Intelligence

US location-based services market size in 2026 is estimated at USD 27.33 billion, growing from 2025 value of USD 23.82 billion with 2031 projections showing USD 54.32 billion, growing at 14.72% CAGR over 2026-2031. The growth trajectory is fueled by 5G maturation that now covers more than 300 million Americans, a smartphone penetration rate expected to reach 91% of mobile connections by 2028, and widening enterprise demand for real-time operational visibility in logistics, healthcare, and retail settings[1]Ericsson, “5G in the North America Region – Ericsson Mobility Report,” ericsson.com. Federal Transit Administration (FTA) programs that standardize General Transit Feed Specification (GTFS) datasets are widening use cases beyond turn-by-turn navigation into multimodal journey planning and transit analytics. Simultaneously, generative-AI platforms such as CARTO GenAI and Oracle Spatial AI are lowering the skills barrier for spatial analytics by supporting natural-language queries of geospatial data. However, compliance costs linked to California’s Location Privacy Act (AB 1355) and emerging state-level data sovereignty bills are forcing providers to invest in privacy-by-design architectures and flexible consent-management workflows.

Key Report Takeaways

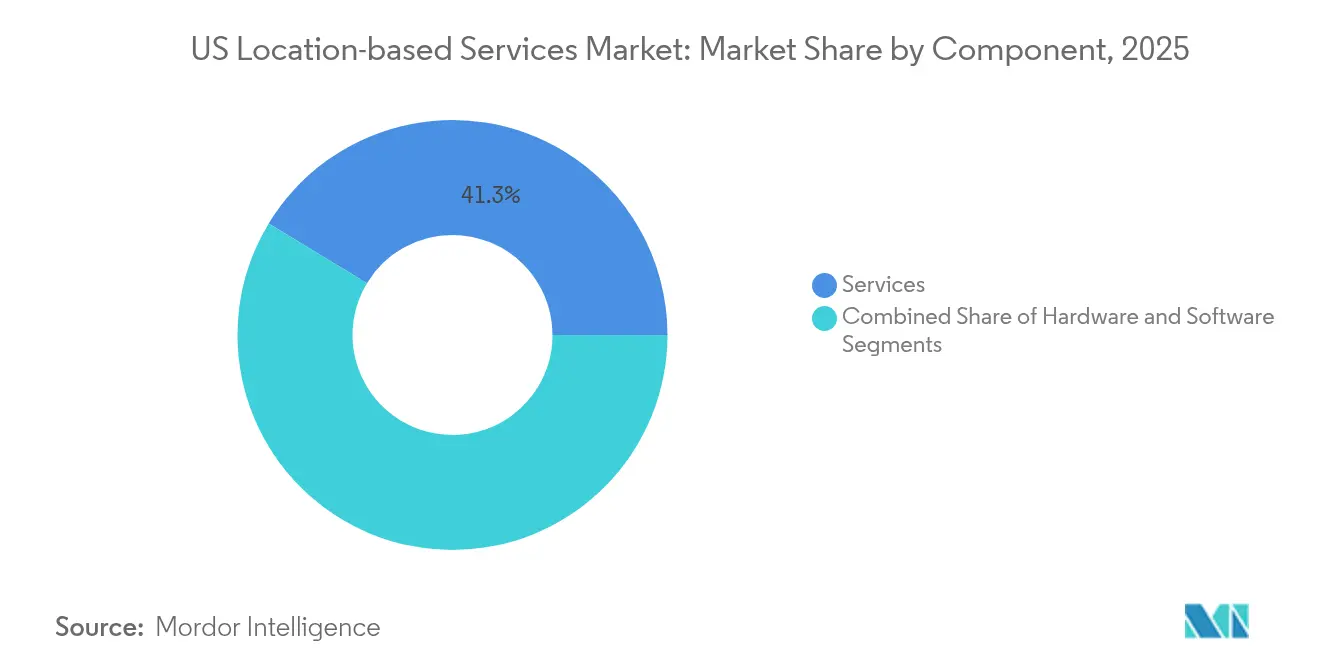

- By component, services led with 41.32% revenue share in 2025 while professional and managed services are projected to advance at a 17.12% CAGR through 2031.

- By location type, outdoor positioning held 55.47% of the US location-based services market share in 2025, whereas indoor positioning is set to expand at a 20.46% CAGR.

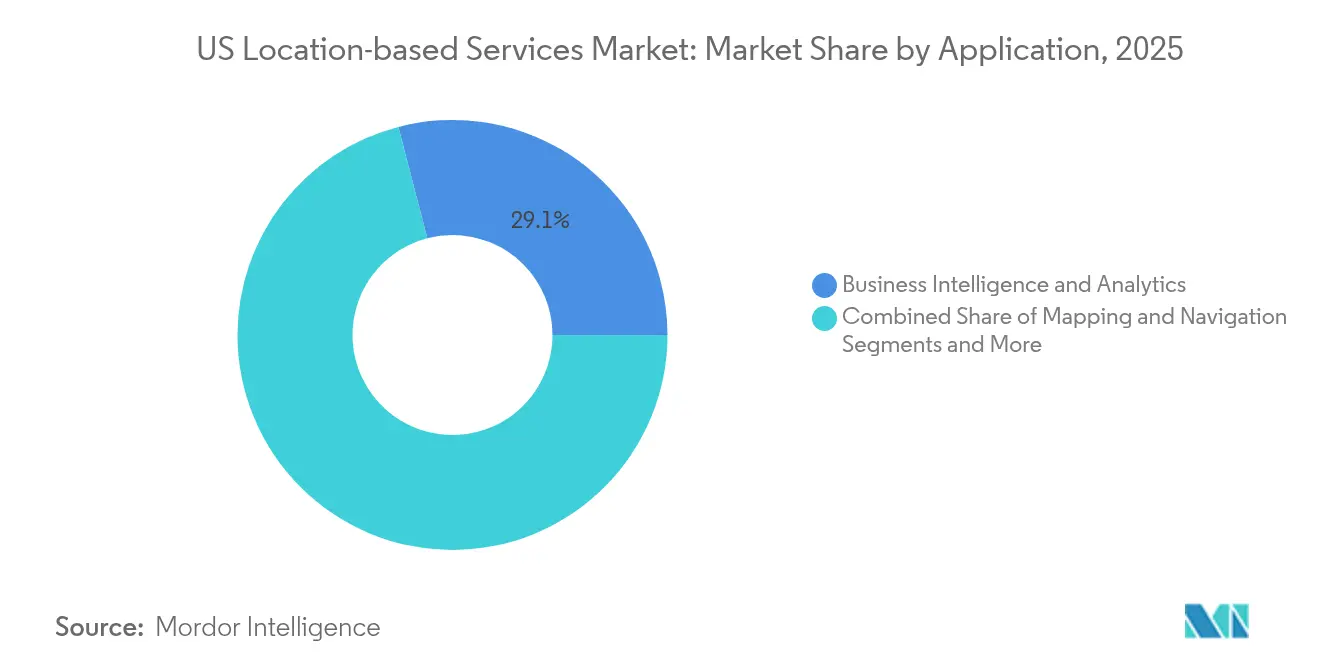

- By application, business intelligence and analytics captured 29.05% share of the US location-based services market size in 2025, while location-based advertising is forecast to grow at a 23.62% CAGR.

- By end-user vertical, transportation and logistics accounted for 23.68% of 2025 revenues, yet healthcare is expected to post the fastest 18.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in United states connect differently with activity unfolding across other parts of the world. In the global location based services market coverage, Mordor Intelligence integrates these into a single analytical framework.

US Location-based Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone penetration and 5G rollout | +2.3% | National, major metropolitan areas | Medium term (2-4 years) |

| Geo-marketing spend surge | +1.8% | National, retail-dense regions | Short term (≤ 2 years) |

| Demand for real-time asset visibility (RTLS) | +1.5% | Healthcare and manufacturing hubs | Medium term (2-4 years) |

| Growth of indoor mapping for retail and venues | +1.2% | Urban centers and high-traffic venues | Medium term (2-4 years) |

| Federal transit LBS datasets unlocking new use cases | +0.9% | Transit-heavy metropolitan areas | Long term (≥ 4 years) |

| Generative-AI-powered spatial analytics | +0.8% | Tech-forward enterprise clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone penetration and 5G rollout

Wide-area 5G now provides low-band coverage to more than 300 million Americans and supports sub-meter positioning when paired with advanced multilateration algorithms. Qualcomm’s X85 5G Modem-RF integrates an on-chip AI engine that enhances time-of-arrival calculations for location accuracy inside large venues. Fixed-wireless access (FWA) rollouts to 9 million premises show 5G’s potential beyond mobility, opening opportunities for geofencing-based home automation and rural asset tracking. Carriers now package “premium positioning” subscriptions; surveys indicate 35% of 5G users will pay extra for enhanced indoor navigation in airports and arenas. These monetization signals underpin long-run revenue confidence for providers in the US location-based services market.

Geo-marketing spend surge

Retailers are pivoting budgets toward proximity-driven campaigns because real-time offers lift in-store conversion rates above demographic-only targeting benchmarks. Cisco Meraki cameras now fuse anonymized WiFi probing with computer vision to segment shoppers by visit frequency and dwell time, feeding that data into dynamic ad platforms. Forty-seven percent of mobile consumers opt in to receive store-triggered coupons when within 100 meters, according to Cisco’s 2025 retail analytics survey. AI-powered demand forecasts allow marketers to pre-buy inventory programmatically when foot-traffic spikes are predicted, converting location data from a descriptive to a predictive asset. The outcome is double-digit budget reallocation to location-targeted formats that accelerates revenue for the US location-based services market.

Demand for real-time asset visibility (RTLS)

Mission Hospital’s CenTrak deployment curbed annual equipment shrinkage by USD 150,000 and generated USD 200,000 in efficiency gains, validating ROI for healthcare RTLS. Sonitor’s SonitorONE supports six locating modalities in one stack and uses 50% fewer beacons than prior-generation systems, reducing installation disruption. Manufacturers leverage EVS mobe3 Live over existing WiFi to track work-in-process goods without extra cabling. These case studies prove that RTLS converts reactive searches into predictive maintenance cycles, a benefit that is pulling new verticals such as food processing into the US location-based services market.

Growth of indoor mapping for retail and venues

Mall of America’s deployment of Inpixon’s interactive maps raised average visitor session time by 13% and supplies anonymized heatmaps for leasing analytics. Hyper AR’s computer-vision toolkit reaches sub-meter accuracy across 200,000 square-feet without external anchors, letting grocers re-sequence pick paths and save USD 2–3 per online order. Apple Indoor Maps’ standardized venue-map schema eases onboarding into enterprise systems such as mobe3 Live, slashing project timelines. The resulting data flow underpins unified commerce dashboards where retailers see both e-commerce and in-store journeys, driving new software subscriptions within the US location-based services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and maintenance cost | –1.2% | National, rural and small markets | Short term (≤ 2 years) |

| Privacy and data-protection compliance burden | –0.8% | CA, MA, IL with national spillover | Medium term (2-4 years) |

| Indoor RF interference in legacy buildings | –0.6% | Dense urban cores | Medium term (2-4 years) |

| State-level data-sovereignty legislation | –0.4% | State-by-state | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High installation and maintenance cost

Predictive WiFi surveys start at USD 395 but full on-site validation climbs to USD 1,450, and end-to-end enterprise deployments average USD 2,000 for every 10,000 square-feet before hardware [2]SecurEdge Networks, “How Much Does a WiFi Site Survey Cost?” securedgenetworks.com. Fiber backhauls adds as much as USD 33,900 for 300-meter digs and takes three to four months to permit and trench. Healthcare installations must pass electromagnetic compatibility tests, raising commissioning budgets and elongate timelines. While Bluetooth low-energy and ultra-wideband can ride existing Ethernet, organizations still face software licensing, security patching, and analytics-platform subscriptions across the life cycle. These cumulative costs stall adoption among mid-tier retailers and community hospitals, tempering near-term growth in the US location-based services market.

Privacy and data-protection compliance burden

California AB 1355 obliges opt-in consent for any collection of “precise geolocation,” a definition that encompasses GPS, IP addresses, and triangulated WiFi identifiers. Enterprises must therefore embed consent orchestration, granular data-retention rules, and subject-access dashboards. Massachusetts and Illinois are drafting parallel frameworks that diverge on allowable processing purposes, creating multi-state governance complexity. Providers now earmark 6–8 % of project budgets for compliance audits, legal reviews, and continuous monitoring. As smaller players lack dedicated privacy teams, they often limit deployments to jurisdictions with clearer rules, clipping addressable revenue within the US location-based services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Deliver Integration Expertise

Services own 41.32% of 2025 revenues and are forecast to record a 17.12% CAGR because enterprises require end-to-end delivery from RF survey through analytics dashboard. Managed services bundles now incorporate location-based data-quality SLAs, proactive sensor-battery replacement, and quarterly analytics tuning. Simultaneously, hardware demand remains steady for IoT tags, beacons, and multi-band antennas that underpin physical capture layers, while software licenses scale in line with sensor counts and data-analytics workloads. CenTrak’s turnkey deployments illustrate why hospitals choose outsourced integration to align RTLS with electronic medical records and nurse-call systems without over-loading internal IT teams . Qualcomm’s Aware enterprise platform further blurs the line between hardware and services by offering device-agnostic APIs that still necessitate solution architects for optimal edge-to-cloud configuration.

In contrast, self-build strategies inside retail and manufacturing operations increasingly combine open-source mapping SDKs with off-the-shelf WiFi analytics, but hidden maintenance overhead often negates up-front savings. As a result, the services segment continues to capture the highest margin profile in the US location-based services market.

By Location Type: Indoor Positioning Breaks Out

Outdoor GPS solutions retained 55.47% revenue share in 2025 thanks to the entrenched role of navigation and last-mile delivery in e-commerce logistics. Yet indoor positioning is projected to grow at a 20.46% CAGR as hospitals, airports, and big-box retailers chase sub-meter accuracy for staff workflows and shopper engagement. Silicon Labs’ BG22 Bluetooth System-on-Chip enables low-power asset tags that report through dense RF environments typical of medical facilities. Apple’s standardized Indoor Maps data model is speeding venue adoption by removing bespoke map-creation steps. This combination of chipset innovation and ecosystem standardization is enlarging the indoor slice of the US location-based services market.

Legacy structures still suffer multipath interference from metallic fixtures, so solution providers deploy AI-assisted calibration routines that auto-tune beacon placement. These advances shrink commissioning windows from weeks to days, helping indoor deployments gain parity with mature outdoor services and setting the stage for future indoor–outdoor handoff use cases that will dominate the US location-based services industry.

By Application: Analytics Tops Navigation

Business intelligence and analytics applications controlled 29.05% of 2025 market value, overtaking navigation for the first time. CARTO’s GenAI makes spatial analysis conversational, letting non-technical staff ask, “Which zip codes saw in-store sales lift after last week’s billboard campaign?” and receive map-based answers in seconds. Oracle Spatial AI adds anomaly detection for events such as crime hot spots and disease clusters, moving analytics from descriptive toward prescriptive practice. Location-based advertising remains the fastest-growing use case at a 23.62% CAGR, driven by programmatic exchanges that sell bid requests with geofencing metadata packaged for real-time bidding.

Consumer mapping and navigation continue to enjoy broad smartphone adoption, yet revenue per user has plateaued as basic turn-by-turn grows commodity. Therefore, software vendors pivot to multimodal routing that fuses transit data unlocked by the FTA, adding subscription-ready premium features such as carbon-tracking dashboards. The analytics focus is expected to widen the US location-based services market size where data-monetization potential outstrips legacy license fees.

By End-user Vertical: Healthcare Takes the Growth Crown

Transportation and logistics remain the biggest spender with 23.68% share, leveraging geofencing for driver compliance and dynamic route recalculation when congestion arises. However, healthcare will log a 18.93% CAGR as RTLS moves from pilot to system-wide deployments that support infection-control workflows and asset-life-cycle optimization. CenTrak’s latest installation yielded a one-year payback, prompting hospital boards to earmark capital budgets for broader coverage. Manufacturing, hospitality, and BFSI sectors follow close behind by tapping location insights to enhance safety audits, guest navigation, and fraud analytics.

In parallel, government agencies modernize transit operations through open data mandates, while IT-telecom players integrate location APIs into IoT platforms to anchor edge-AI applications. This multi-vertical uptake solidifies a diversified demand base that cushions the US location-based services market against sector-specific downturns.

Geography Analysis

Tier-one metropolitan corridors—New York, Los Angeles, San Francisco, and Chicago—account for more than half of enterprise deployments because they combine dense 5G coverage with technology-savvy workforces eager to exploit real-time visibility. The Northeast concentrates academic medical centers that pilot RTLS for patient throughput, while Silicon Valley hosts start-ups building AI-driven geospatial analytics platforms that later scale nationally. West Coast retailers lead indoor-mapping adoption, underpinned by robust venture funding and early consumer acceptance of app-mediated store experiences. The US location-based services market continues to grow fastest in Sunbelt states such as Texas and Florida where manufacturing and logistics hubs prioritize supply-chain precision to offset labor shortages.

California’s AB 1355 privacy regime effectively sets the default for nationwide compliance checklists, compelling vendors in other states to conform even before local laws take effect. In contrast, rural counties face higher per-square-foot installation costs and intermittent 5G coverage, elongating return-on-investment horizons. Carriers are mitigating this divide through fixed-wireless access that extends low-band 5G to 9 million rural homes, thereby unlocking new addressable pockets for the US location-based services market. Federal Transit LBS pilots in Minneapolis and Seattle further anchor opportunities in mid-tier metros by promoting open data ecosystems that private developers can monetize.

Looking forward, state-level data-sovereignty bills in Massachusetts and Illinois could introduce region-locked storage mandates. Vendors planning national rollouts now architect geo-fenced data lakes to adapt without wholesale re-platforming, a design choice that adds upfront cost but preserves scale economics across the broader US location-based services industry.

Mordor Intelligence's coverage of the location based services market extends across other regions including Middle East and Africa, while country-specific intelligence is also available for Canada, Brazil, United Arab Emirates, Nigeria, China, Japan, and India, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The competitive field remains moderately fragmented: platform leaders Google and Apple dominate consumer navigation, yet specialized providers such as CenTrak, Zebra Technologies, and Inpixon command healthcare and indoor-analytics niches. Microsoft extends Azure Maps through alliances with TomTom, HERE, and Esri, offering developers unified APIs that bundle routing, gridded weather, and pedestrian heatmaps. Qualcomm’s chipset roadmap, targeting USD 22 billion in automotive and IoT revenue by FY29, underscores how silicon differentiation influences accuracy and power consumption—key buying criteria for enterprise RTLS.

Strategically, incumbents hedge against privacy risk by embedding on-device processing that reduces raw-location data egress, as evidenced by Apple’s Private Relay and Google’s Federated Analytics. Consolidation also shapes the market: Platform Science’s acquisition of Trimble’s fleet-telematics division merges hardware, ELD compliance software, and data-monetization services into one stack. Meanwhile, HERE Technologies introduced an AI-powered guidance assistant for software-defined vehicles, signaling intensifying RandD competition around in-vehicle location intelligence.

Niche disruptors gain ground through ultra-wideband micro-location and AI-first mapping engines, but scaling remains capital intensive. Overall, the top five vendors control roughly 45–50% of segment revenues, giving the US location-based services market a market-concentration score of 6, denoting a balanced but tightening competitive environment.

US Location-based Services Industry Leaders

IBM Corporation

Cisco Systems Inc.

Google LLC

HPE Aruba Inc

Zebra Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: HERE Technologies unveiled the AI-powered Intelligent Guidance Assistant for software-defined vehicles, marrying large-language-model reasoning with dynamic location data.

- July 2025: Cisco showcased Meraki Smart Cameras and Sensors at Cisco Live US 2025, highlighting real-time location analytics for retail customer-behavior insights.

- June 2025: Esri demonstrated AI enhancements in ArcGIS, including Gaussian-Splats-based 3D object recognition, at GEOINT 2025.

- May 2025: Qualcomm introduced the Snapdragon 7 Gen 4 mobile platform with 65% AI uplift and richer location capabilities for mid-tier smartphones.

US Location-based Services Market Report Scope

Location-based services (LBSs) are computer or mobile apps that deliver information depending on the user's and the device's location. They are often accessed through mobile networks and portable devices like smartphones.

The precision of the location services majorly depends on the software and hardware utilized in the mobile communication system, along with the positioning server. The US location-based services market is segmented by component (hardware, software, and services), by location (indoor and outdoor), by application (mapping and navigation, business intelligence and analytics, location-based advertising, social networking and entertainment, and other applications), by end-user (transportation and logistics, IT and telecom, healthcare, government, BFSI, hospitality, manufacturing, and other end-users).

The market sizes and forecasts are provided in terms of value USD for all the above segments.

| Hardware |

| Software |

| Services |

| Indoor |

| Outdoor |

| Mapping and Navigation |

| Business Intelligence and Analytics |

| Location-based Advertising |

| Social Networking and Entertainment |

| Other Applications |

| Transportation and Logistics |

| IT and Telecom |

| Healthcare |

| Government |

| BFSI |

| Hospitality |

| Manufacturing |

| Other End-users |

| By Component | Hardware |

| Software | |

| Services | |

| By Location Type | Indoor |

| Outdoor | |

| By Application | Mapping and Navigation |

| Business Intelligence and Analytics | |

| Location-based Advertising | |

| Social Networking and Entertainment | |

| Other Applications | |

| By End-user Vertical | Transportation and Logistics |

| IT and Telecom | |

| Healthcare | |

| Government | |

| BFSI | |

| Hospitality | |

| Manufacturing | |

| Other End-users |

Key Questions Answered in the Report

What is the current value of the US location-based services market?

The market is valued at USD 27.33 billion in 2026 and is projected to grow to USD 54.32 billion by 2031.

Which component segment is growing fastest?

Services are expanding at a 17.12% CAGR because enterprises prefer managed deployments that handle integration complexity end-to-end.

Why is indoor positioning gaining momentum over outdoor GPS?

Breakthroughs in Bluetooth low-energy, ultra-wideband, and standardized indoor maps now deliver sub-meter accuracy, enabling new retail and healthcare workflows that outdoor GPS cannot support.

How are privacy regulations affecting the market?

California’s AB 1355 and emerging state bills require explicit opt-in consent and granular data-retention controls, driving up compliance costs and influencing solution design nationwide.

Page last updated on: