Mobile Application Development Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

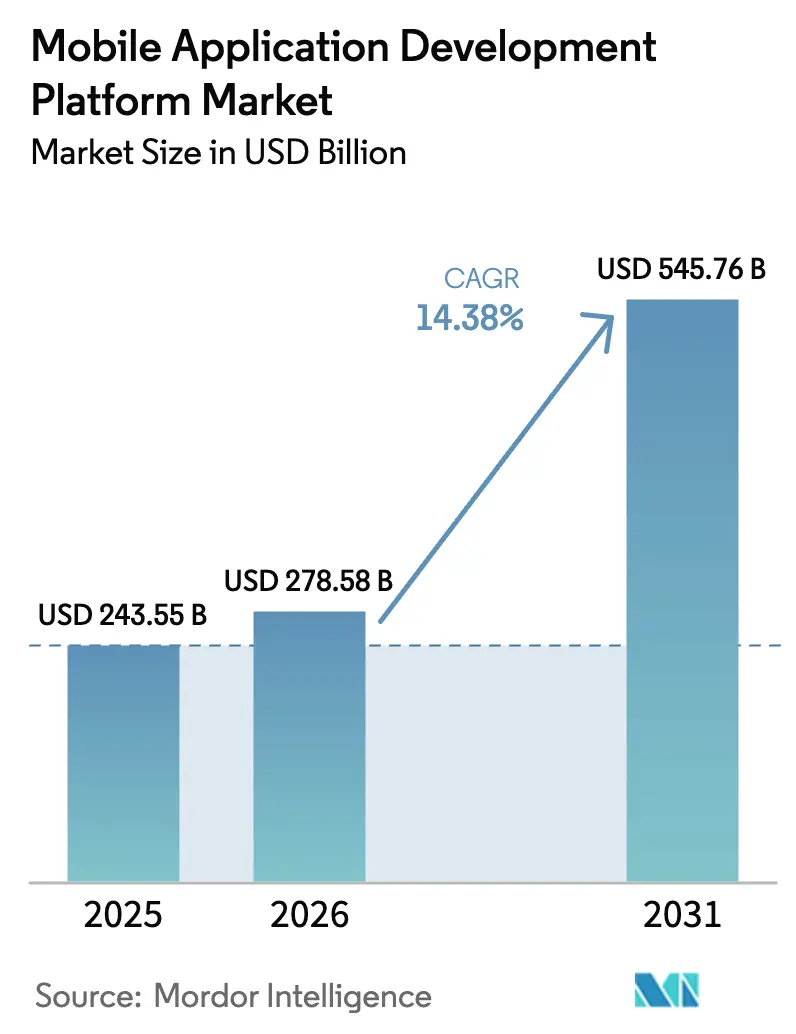

| Market Size (2026) | USD 278.58 Billion |

| Market Size (2031) | USD 545.76 Billion |

| Growth Rate (2026 - 2031) | 14.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Application Development Platform Market Analysis by Mordor Intelligence

The mobile application development platform market size is expected to grow from USD 243.55 billion in 2025 to USD 278.58 billion in 2026 and is forecast to reach USD 545.76 billion by 2031 at 14.38% CAGR over 2026-2031. Widespread 5G availability, the rapid shift to low-code development, and cloud-native microservices are combining to accelerate enterprise investment in modern development environments. Vendors are embedding AI into design, testing, and security workflows, allowing both professional developers and citizen developers to shorten release cycles while improving code quality. Enterprises are prioritizing cross-platform solutions that keep maintenance spending low, meet tight privacy regulations, and integrate seamlessly with real-time analytics and IoT workloads. Competitive intensity is rising as hyperscalers, handset ecosystem owners, and pure-play low-code specialists race to add AI-assisted tooling and verticalized features.

Key Report Takeaways

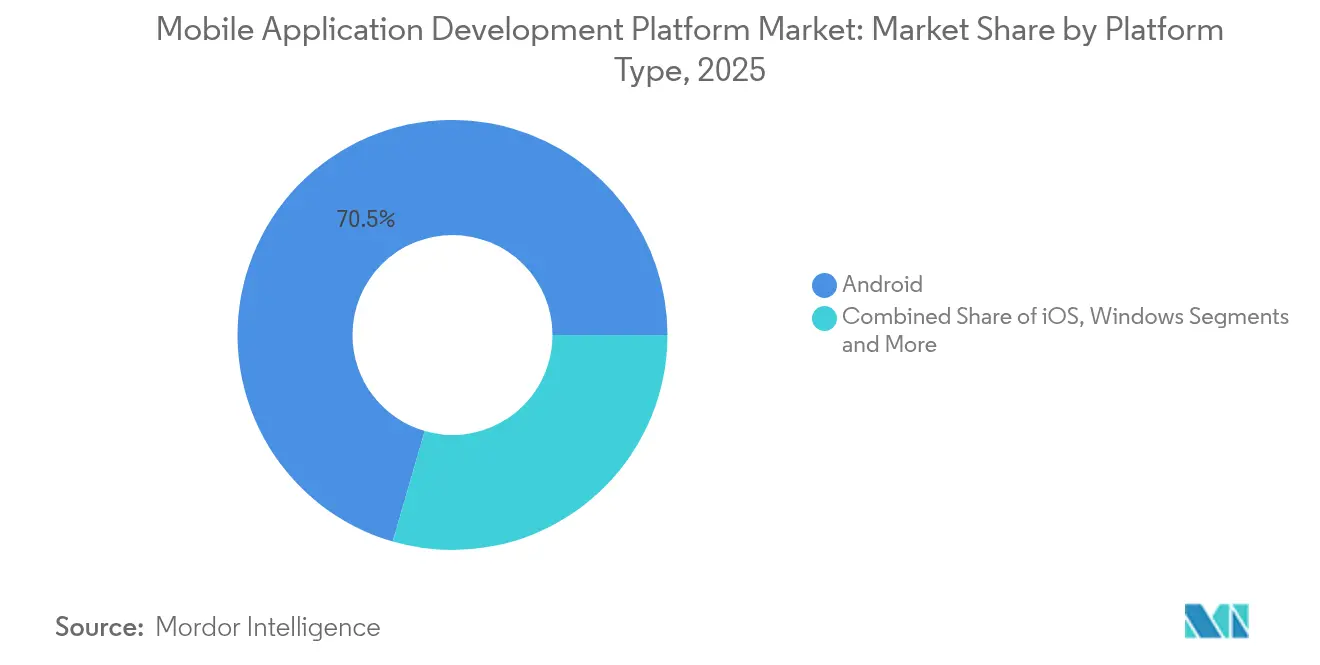

- By platform type, Android retained 70.52% of mobile application development platform market share in 2025, while iOS is projected to post the fastest 14.55% CAGR through 2031.

- By deployment model, cloud deployments commanded 72.36% of the mobile application development platform market size in 2025 and are tracking a 17.05% CAGR to 2031.

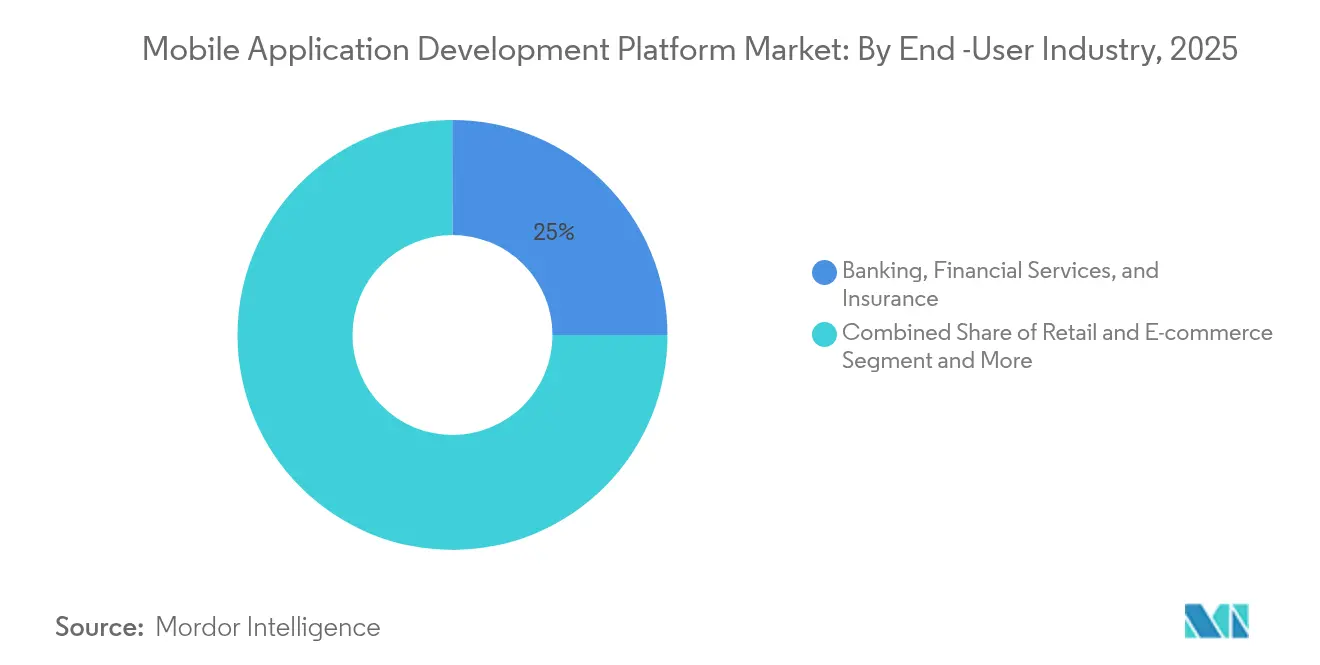

- By end-user industry, BFSI led with 25.02% revenue share in 2025; Media & Entertainment is advancing at an 17.92% CAGR to 2031.

- By organization size, large enterprises accounted for 69.05% of the mobile application development platform market size in 2025, whereas SMEs are growing at an 18.33% CAGR.

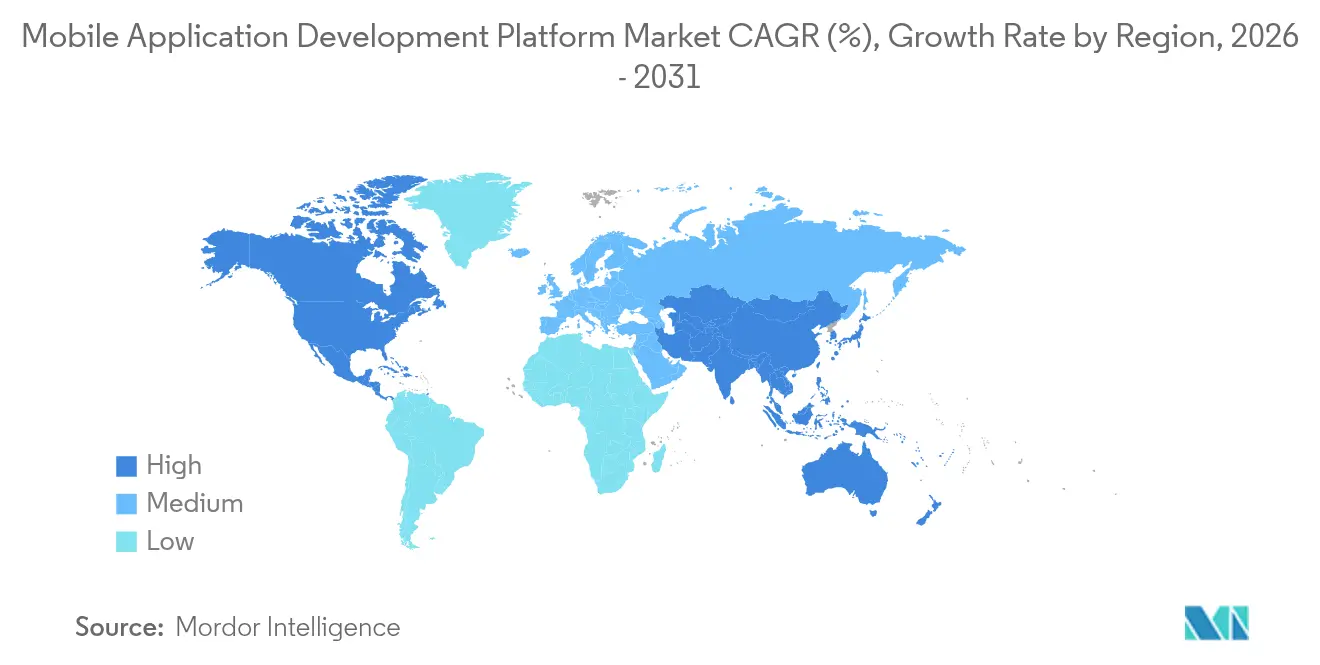

- By geography, North America held 34.12% of the mobile application development platform market share in 2025; Asia-Pacific is expanding at a 17.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Application Development Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging enterprise demand for cross-platform low-code MADPs | +3.2% | Global with North America and EU focus | Medium term (2-4 years) |

| 5G rollouts enabling richer mobile apps | +2.8% | Asia-Pacific core, spill-over to North America and EU | Short term (≤ 2 years) |

| AI-assisted coding tools accelerating release cycles | +2.1% | Global, early uptake in North America | Short term (≤ 2 years) |

| Cloud-native microservices driving mobile front ends | +1.9% | Global, led by North America and EU enterprises | Medium term (2-4 years) |

| Need for real-time analytics and IoT integration | +1.5% | Global, strongest in manufacturing hubs | Medium term (2-4 years) |

| Accessibility mandates for public-sector mobile services | +0.8% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Enterprise Demand for Cross-Platform Low-Code MADPs

Enterprises are replacing siloed, code-heavy toolchains with unified, low-code environments that cut development time by up to 30% while promoting code reuse across Android and iOS projects. Citizen developers now collaborate directly with professional teams, reducing backlog and freeing scarce DevSecOps talent for high-value tasks. Integrated governance controls in modern platforms help enterprises curb technical debt, simplify version upgrades, and lower total cost of ownership.

5G Roll-outs Enabling Richer Mobile Apps

Sub-6 GHz and mmWave 5G coverage lowers latency to single-digit milliseconds, supporting real-time augmented-reality field support, ultra-HD streaming, and instant payments. Development platforms now ship with network-aware SDKs that let applications detect bandwidth conditions and adjust payload delivery dynamically. Early adopters in manufacturing and healthcare are connecting Internet of Medical Things and industrial sensors to mobile dashboards, generating new performance benchmarks for the ecosystem.

AI-Assisted Coding Tools Accelerating Release Cycles

Embedded AI copilots automatically convert natural-language requirements into templated code, flag vulnerabilities, and generate unit tests, helping teams trim sprints by nearly one quarter. Predictive analytics inside the IDE recommend optimal microservice patterns and spot integration conflicts before deployment. Enterprises deploying these features report higher code quality scores and faster compliance checks across regulated workloads.

Cloud-Native Microservices Driving Mobile Front-Ends

Container platforms and service meshes let developers decompose monoliths into modular services that scale independently. Continuous integration pipelines automate patching and rollbacks, keeping mobile front-ends resilient during peak traffic bursts. API-first design aligns mobile releases with backend upgrades, ensuring feature parity across web and native channels while preserving data sovereignty through region-specific clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and privacy compliance burden | −1.8% | Global, strictest in EU and California | Short term (≤ 2 years) |

| Platform fragmentation inflating maintenance cost | −1.4% | Global, acute in enterprise settings | Medium term (2-4 years) |

| Global shortage of DevSecOps talent | −1.1% | Global, most severe in North America and EU | Long term (≥ 4 years) |

| Carbon-emission scrutiny targeting heavyweight apps | −0.6% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Compliance Burden

GDPR, CCPA, and a wave of regional rules require granular consent, data-flow mapping, and breach-response tooling. Non-compliance fines reached EUR 1.6 billion across industries in 2024, driving organisations to demand platforms with built-in encryption key management, automated audit logs, and privacy-by-design templates. Smaller teams that lack dedicated compliance officers are shifting toward turnkey solutions that handle country-specific data residency and age-verification checks.

Platform Fragmentation Inflating Maintenance Cost

Foldable displays, wearables, vehicle infotainment systems, and smart-TV operating systems add substantial QA cycles as each form factor needs individual optimisation. Maintenance spending now averages 18% of first-year development outlay for large enterprises. To contain costs, organisations standardise on cross-platform engines and shared UI kits, yet must still reserve budget for new device test farms and backward-compatibility patches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Android Dominance Faces iOS Enterprise Push

Android held 70.52% of mobile application development platform market share in 2025. The broad hardware ecosystem and customisability drive high adoption in retail logistics, field-service automation, and emerging-market consumer apps. iOS leads growth at a 14.55% CAGR as Apple’s enterprise software initiatives and secure-enclave hardware vie for back-office and regulated workloads. Cross-platform frameworks such as Flutter and React Native help enterprises balance performance with budget limits, extending single codebases into both Android and iOS storefronts. This convergence reduces redundant staffing, shortens QA timelines, and mitigates fragmentation risk.

Demand for progressive web applications also continues to rise. These install-light experiences deliver near-native performance while lowering user acquisition friction. Enterprises in media streaming and quick-commerce tweak PWAs to reach customers who prefer browser-based engagement, especially in bandwidth-constrained geographies. As device OEMs experiment with foldable and wearable screens, vendor roadmaps emphasise adaptive layout engines and responsive design guidelines to sustain consistent UX across screen classes.

By Deployment Model: Cloud-Native Architecture Accelerates

Cloud options captured 72.36% of the mobile application development platform market size in 2025 and are pacing a 17.05% CAGR. Enterprises favour the pay-as-you-scale model, global availability zones, and built-in DevSecOps pipelines that leading hyperscalers provide. Low-code vendors now bundle serverless backends, managed Kubernetes, and policy-as-code modules, allowing teams to dial up resources automatically when new releases spike demand. On-premise instances remain common in defence, public safety, and parts of the financial sector, yet hybrid deployment patterns are gaining ground where data residency laws require domestic storage.

Edge computing complements cloud bursts by placing inference and analytics closer to devices. Retailers deploy lightweight edge clusters in stores to run inventory vision models while syncing aggregates with the core platform overnight. Container toolchains bridge edge and cloud, offering a consistent build-run-observe workflow. This approach improves response time, lowers bandwidth cost, and enhances uptime when connectivity is intermittent.

By End User Industry: BFSI Leadership Challenged by Media Growth

Banking, Financial Services, and Insurance commanded 25.02% of the mobile application development platform market size in 2025. Mobile banking apps, e-wallets, and AI-driven advisory bots require secure coding and stringent audit trails, prompting institutions to pick platforms certified for PCI-DSS and SOC 2 Type II. Media & Entertainment, posting an 17.92% CAGR, benefits from streaming services that bundle interactive polls, real-time chat, and personalised recommendation engines. This sector often deploys micro-frontends to segment features for A/B testing and dynamic updates.

Healthcare adoption steadily rises as telehealth visits exceed in-person primary consultations in several markets. HIPAA-aligned development toolkits and FHIR-compliant APIs help providers roll out symptom checkers and remote monitoring apps without lengthy custom coding. Retail stands out for omnichannel programs that integrate loyalty wallets and in-store scanning, while the public sector channels digitisation grants into citizen-service apps that must hit WCAG accessibility thresholds.

By Organisation Size: SME Acceleration Challenges Enterprise Dominance

Enterprises larger than 1,000 employees represented 69.05% of mobile application development platform market share in 2025. They maintain multi-product portfolios requiring rigorous governance, internationalisation, and complex user management. However, SMEs are growing faster at 18.33% CAGR. Subscription pricing tiers, drag-and-drop interfaces, and community plug-ins lower the entry barrier. Many SMEs launch minimum-viable products in weeks, gather feedback, and iterate rapidly without hiring full-time software engineers.

Citizen developer programs flourish in smaller firms where business owners and domain experts build task-specific apps for inventory counts, local marketing, or customer feedback. Platform vendors respond with visual data modelling, one-click deployment, and contextual learning resources. As SMEs scale, they upgrade to enterprise editions featuring advanced RBAC and API gateways, preserving earlier investments while adding compliance and monitoring layers pivotal for larger workloads.

Geography Analysis

North America retains the revenue crown with a 34.12% share. The region benefits from 71% 5G subscriber penetration, supporting real-time analytics for healthcare wearables and industrial inspection drones. Government procurement rules mandate WCAG 2.1 Level AA compliance for all new mobile public services by 2027, pushing agencies toward solutions with automatic contrast testing and screen-reader simulations. Talent shortages in mobile security and integration disciplines are intensifying wage pressure, prompting enterprises to invest in AI-assisted code review.

Asia-Pacific is the fastest riser at 17.47% CAGR. China and India dominate absolute volume, while Southeast Asia records some of the world’s highest mobile commerce growth rates. Government digital-ID programs spur secure sign-in frameworks within development platforms. Telecom carriers extend 5G SA coverage to tier-2 cities, reducing network bottlenecks for data-rich applications. Japanese and Korean corporates pioneer 6G proof-of-concepts that demand ultra-low-latency edge stacks, setting future requirements for platform vendors.

Europe advances steadily on the back of GDPR and ePrivacy enforcement. Financial penalties for non-compliant apps encourage adoption of platforms with automated personal-data scanners and breach-notification workflows. Germany, France, and the Netherlands invest in sovereign-cloud capacity, giving enterprises the option to confine sensitive payloads within EU borders. Hybrid-cloud configurations enjoy newfound interest as public sector entities reconcile digital-first mandates with on-premise cryptographic HSMs.

Competitive Landscape

The mobile application development platform market features a mix of hyperscalers, ecosystem gatekeepers, and low-code specialists. Google, Apple, and Microsoft package SDKs, CI/CD pipelines, and marketplace distribution into their broader cloud portfolios, leveraging global infrastructure and native OS hooks. OutSystems, Mendix, and Appian concentrate on enterprise low-code suites that integrate process automation, governance dashboards, and AI-generated test cases. Salesforce deepens its data management edge through the USD 8 billion Informatica acquisition, positioning the combined offering as a single source of truth for mobile data orchestration[2]Salesforce, “Salesforce Completes Acquisition of Informatica,” salesforce.com.

IBM enlarges its consulting footprint by acquiring Applications Software Technology to speed Oracle Cloud and low-code rollouts inside the public sector[3]IBM Newsroom, “IBM to Acquire AST to Enhance Oracle Cloud Consulting,” ibm.com. Microsoft’s retirement of Visual Studio App Center has opened space for providers that handle code signing, artifact storage, and phased rollout across both public marketplaces and private enterprise catalogs. Apple’s continued expansion of enterprise APIs and security certifications targets regulated verticals where device integrity and biometric secure enclaves are pivotal. Google’s Flutter framework elevates its cross-platform appeal by integrating Material 3 design widgets and AI code completion features powered by Gemini models.

Pure-play vendors differentiate through vertical depth. Some focus on HIPAA-ready patient portal templates, while others pre-package PSD2 authentication flows for European fintechs. A growing cohort exploits AI to auto-convert legacy Java or .NET codebases into modern Kotlin and Swift modules, easing migration pain for firms saddled with aging apps. Products that modularise core services through recognisable micro-frontend blocks win traction because they let teams evolve features without disrupting the entire codebase.

Mobile Application Development Platform Industry Leaders

Google LLC

Apple Inc.

Microsoft Corporation

IBM Corporation

Salesforce.com Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce closed its USD 8 billion acquisition of Informatica, adding master-data management and low-latency data integration that improve mobile application consistency across multi-cloud estates.

- March 2025: Microsoft retired Visual Studio App Center, steering customers toward partner ecosystems for app artifact management and release workflows.

- January 2025: IBM acquired Applications Software Technology to strengthen Oracle Cloud service delivery and broaden mobile development capabilities for government clients.

- March 2024: Microsoft launched a browser-based mobile game store aligned with EU Digital Markets Act provisions, bypassing incumbent app-store fees.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the mobile application development platform (MADP) market as all licensed software and cloud services that enable professional or citizen developers to design, build, test, deploy, and manage native, hybrid, progressive web, and multiexperience mobile apps across smartphones, tablets, and emerging edge endpoints.

Scope exclusion: Revenues from finished consumer apps, advertising networks, and device hardware are left outside the model.

Segmentation Overview

- By Platform Type

- Android

- iOS

- Windows

- Cross-platform Frameworks (Flutter, React-Native, etc.)

- By Deployment Model

- Cloud

- On-premise

- By End-use Industry

- BFSI

- Retail and E-commerce

- Healthcare

- IT and Telecom

- Media and Entertainment

- Education

- Government

- Others

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed product managers at MADP vendors, cloud hyperscaler partner leads, CIOs in BFSI and retail, and community leaders of Flutter and React Native user groups across North America, Europe, and Asia-Pacific. The calls clarified typical contract values, adoption milestones, and regional pricing adjustments used to fine-tune desk-research assumptions.

Desk Research

We began by mapping publicly available datasets from bodies such as GSMA Intelligence, OECD telecom indicators, the U.S. Bureau of Labor Statistics (developer head count), and regional trade groups like Digital Europe. Annual reports and 10-Ks of leading platform vendors added price and customer mix clues, which were enriched with Questel patent trends on low-code toolchains. Subscription feeds from Dow Jones Factiva and D&B Hoovers helped us follow funding rounds and platform rollouts. This list is illustrative; many additional open and paid sources were reviewed to cross-check numbers and definitions.

Market-Sizing & Forecasting

A top-down construct starts with global developer spending pools and enterprise software budgets, adjusted for mobile penetration and shadow IT adoption. Select bottom-up roll-ups, sampled average selling price multiplied by active platform seats and channel checks, help reconcile totals. Key variables include smartphone installed base growth, cloud migration ratios, low-code seat penetration, average platform subscription price, 5G coverage expansion, and regional wage differentials. Multivariate regression links these drivers to historical revenue; scenario analysis captures currency swings and policy shocks. Gaps in granular country data are bridged with weighted proxies derived from adjacent SaaS benchmarks before final balancing.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly scans, senior analyst variance checks against external markers, and a final sign-off round. We refresh models every twelve months and reopen them mid-cycle when take-private deals, mega acquisitions, or regulatory shifts materially alter the outlook.

Why Mordor's Mobile Application Development Platform Baseline Commands Confidence

Published figures often diverge because firms select different revenue buckets, refresh cadences, and currency bases.

Our disciplined scoping and dual-path modeling ensure the baseline remains both transparent and repeatable for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 243.55 B (2025) | Mordor Intelligence | - |

| USD 22.4 B (2024) | Global Consultancy A | Counts license fees only; omits cloud services and professional support |

| USD 14.8 B (2024) | Trade Journal B | Focuses on low-code subsegment; relies on vendor bookings with limited validation |

| USD 7.15 B (2019) | Industry Association C | Outdated baseline, pre-cloud shift assumptions, narrow SMB scope |

The comparison shows that narrower definitions, older baselines, or single-source estimates lead to markedly lower numbers. By capturing cloud subscriptions, low-code add-ons, and services while rigorously triangulating inputs, Mordor delivers a balanced, future-ready baseline clients can trust.

Key Questions Answered in the Report

What is the current size of the mobile application development platform market?

The mobile application development platform market stands at USD 278.58 billion in 2026.

How fast is the mobile application development platform market expected to grow?

The market is forecast to expand at a 14.38% CAGR over 2026-2031, reaching USD 545.76 billion by 2031.

Which deployment model is expanding the quickest?

Cloud deployment, already holding 72.36% share, is growing at a 17.05% CAGR due to scalable, infrastructure-light benefits.

Which region shows the strongest growth momentum?

Asia-Pacific is projected to grow at 17.47% CAGR through 2031, driven by mobile-first consumer behavior and government digitization.

What impact does 5G have on this market?

5G lowers latency and supports data-intensive use cases, increasing demand for development platforms that optimize application performance for next-generation networks.

Page last updated on: