Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Mobile Core Network Market is Segmented by IMS Core (Session Border Controllers, Voice Application Servers, and More), 4G/5G Packet Core Controller (Mobility Management Entity, Serving Gateway-Control, and More), 4G/5G Subscriber Data Management (Home Subscriber Server, Unified Data Management), Deployment Model (Virtualised VNFs, Cloud-Native CNFs), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

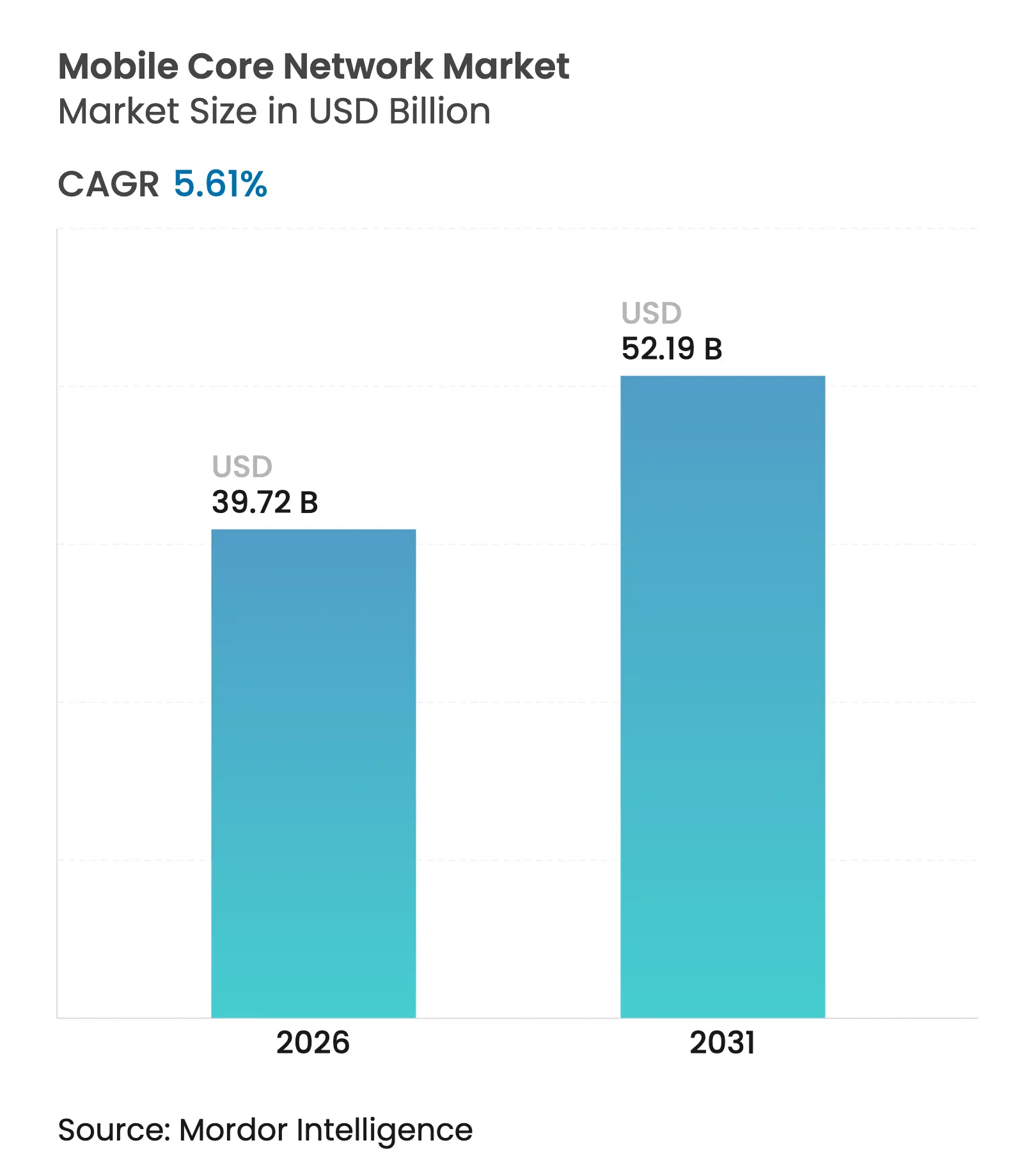

| Market Size (2026) | USD 39.72 Billion |

| Market Size (2031) | USD 52.19 Billion |

| Growth Rate (2026 - 2031) | 5.61 % CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The mobile core network market size was valued at USD 37.61 billion in 2025 and estimated to grow from USD 39.72 billion in 2026 to reach USD 52.19 billion by 2031, at a CAGR of 5.61% during the forecast period (2026-2031). This measured yet steady trajectory follows the end of the explosive 5G build-out phase and reflects operators’ pivot toward cloud-native migrations, AI-assisted automation, and cost-optimized capacity scaling. A 32% revenue surge in Q1 2025, spurred largely by China’s 122% jump in core network spending, underscored the residual momentum of 5G Stand-Alone investments, RCR Wireless News. Leading vendors emphasize integrated AI functions, network slicing support, and API-exposed services as chief differentiators, while hyperscalers extend competitive pressure through core-as-a-service offerings. Spectrum auctions in India, Canada, and the US compel infrastructure upgrades, and rising IoT device counts create fresh demand for scalable subscriber data management. At the same time, high deployment costs, legacy technology coexistence, and security skill shortages temper near-term growth.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Mobile data consumption surge

Mobile data consumption surge

| +1.2% | Global, with Asia-Pacific leading growth | Medium term (2-4 years) |

( ~ ) % Impact on CAGR

Forecast

:

+1.2%

|

Geographic Relevance

:Global, with Asia-Pacific leading

growth |

Impact Timeline

:

Medium term (2-4 years)

|

5G Stand-Alone core roll-outs

5G Stand-Alone core roll-outs

| +1.8% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) | |||

Cloud-native and network

virtualisation

Cloud-native and network

virtualisation

| +0.9% | Global, concentrated in developed markets | Medium term (2-4 years) | |||

Massive-IoT traffic expansion

Massive-IoT traffic expansion

| +0.7% | Global, with industrial clusters in Asia-Pacific and Europe | Long term (≥ 4 years) | |||

Government spectrum auctions

Government spectrum auctions

| +0.6% | India, US, Canada | Short term (≤ 2 years) | |||

AI-driven autonomous core

operations

AI-driven autonomous core

operations

| +0.4% | Global, spill-over from North America to EMEA | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Mobile Data Consumption

Ericsson projects global traffic to reach 237 exabytes per month by 2026, a 46% annual increase LightReading. Operators, therefore, adopt elastic scaling rather than fixed over-provisioning. Generative-AI-enhanced video creation drives uplink spikes that challenge traditional EPC designs, Nokia.[1]Nokia Networks Staff, “AI-Driven Traffic Patterns Challenge Core Designs,” Nokia, nokia.com The resulting asymmetrical flows hasten investment in session management, user plane anchoring, and real-time policy engines capable of millisecond adjustments.

5G Stand-Alone Core Roll-outs

Sixty-one live SA networks worldwide—inclusive of AT&T and Verizon’s planned nationwide launches—illustrate a decisive pivot to slice-ready architectures Fierce Network.[2] Diana Goovaerts, “5G SA Deployments Accelerate,” Fierce Network, fiercenetwork.com SA cores unlock Voice-over-NR, URLLC, and monetisable APIs, but only 39 operators have actually lit SA service, exposing migration complexity LightReading. High-value enterprise and IoT contracts nevertheless render SA capabilities non-negotiable, ensuring sustained equipment and software demand.

Cloud-Native and Network Virtualisation

Operators report 40% resource efficiency gains and 30% OPEX cuts after migrating to Kubernetes-based CNFs LightReading. Vendors now embed ML loops directly into network functions for predictive maintenance and self-healing TotalTelecom.[3]Mary Lennighan, “Total Telecom: AI-Native Core Launch,” Total Telecom, totaltele.com These capabilities promote a shift from hardware-centric upgrades to software-driven feature releases and subscription-priced network services that broaden revenue pools without proportional CAPEX.

Growth in Massive-IoT Traffic

Industrial automation, smart cities, and connected vehicles will lift cellular IoT links to 7.5 billion by 2033 MobileWorldLive. Integrating NB-IoT and LTE-M into the 5G core allows ultra-low-power devices to function for 10 years on a single battery GSMA. Scalability hinges on modern subscriber data layers supporting trillions of policy decisions daily and facilitating granular billing suitable for sensor-level economics.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High implementation and

integration costs

High implementation and

integration costs

| -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

( ~ ) % Impact on CAGR

Forecast

:

-0.8%

|

Geographic Relevance

:

Global, acute in emerging

markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Legacy interoperability

complexity

Legacy interoperability

complexity

| -0.6% | Global, concentrated in mature markets | Medium term (2-4 years) | |||

Cyber-security skill shortage

Cyber-security skill shortage

| -0.4% | North America and EU | Long term (≥ 4 years) | |||

Un-harmonised lawful-intercept

regulations

Un-harmonised lawful-intercept

regulations

| -0.3% | Global, with regulatory fragmentation | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Implementation and Integration Costs

5G infrastructure spending is set to exceed USD 1.3 trillion by 2030, while individual base stations cost USD 100,000–200,000 and core upgrades add USD 20,000–50,000 per site PatentPC. These obligations prompt vendor partnerships, network-sharing alliances, and mergers—such as Nokia’s USD 2.3 billion Infinera acquisition—to spread financial risk Fierce Network. Smaller operators may resort to core-as-a-service models hosted by hyperscalers to contain CAPEX spikes.

Legacy Interoperability Complexity

Multi-generation coexistence means operators must preserve 2G/3G signaling, 4G interworking, and 5G service-based interfaces simultaneously GSMA. Three UK’s replacement of Nokia and Microsoft gear with Ericsson’s unified platform shows the drive to simplify vendor stacks LightReading. Harmonizing lawful intercept, billing, and customer-care processes across divergent network technologies extends timelines and raises integration bills.

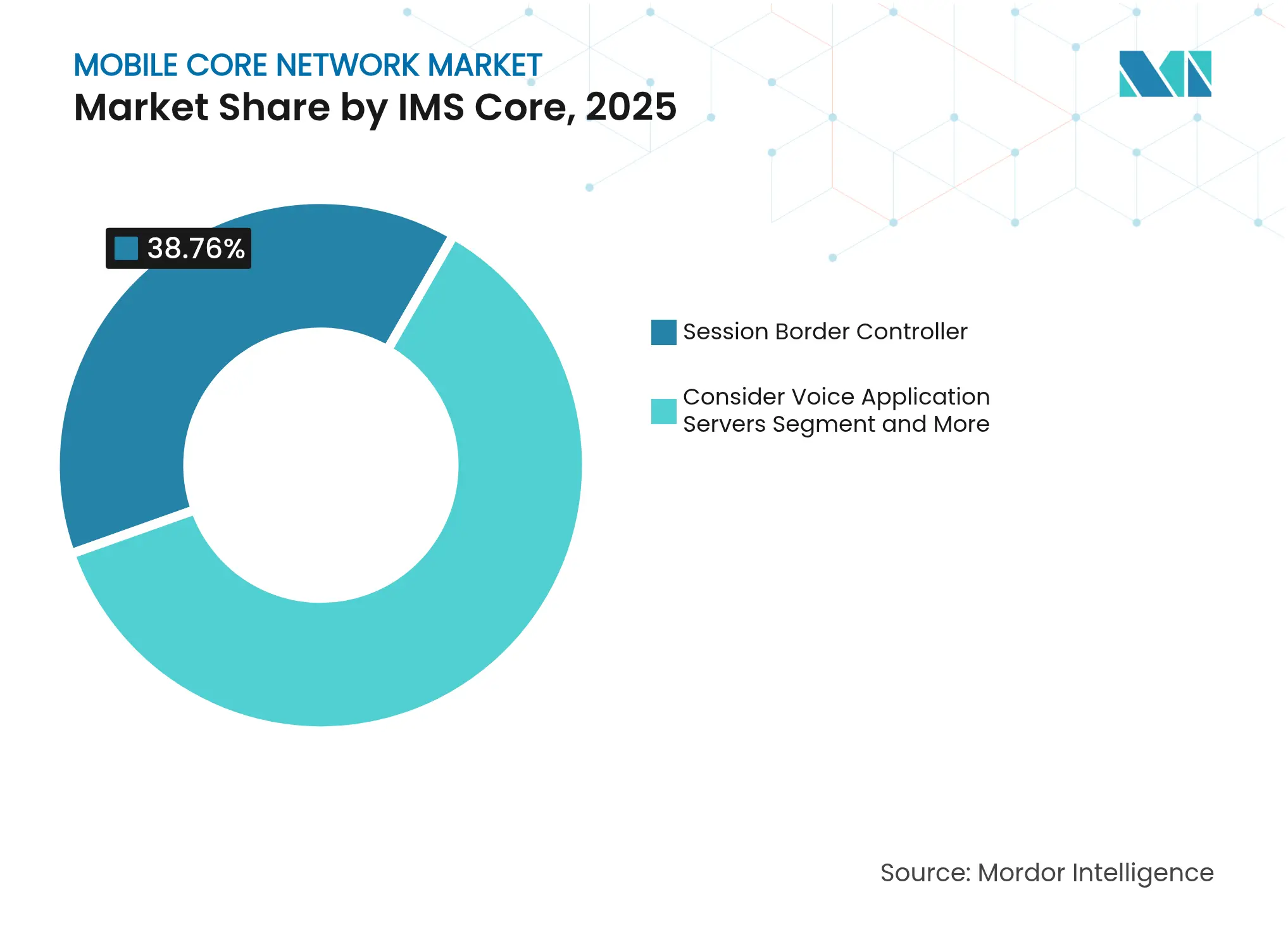

By IMS Core: SBC Leadership in Voice Evolution

The segment generated the largest revenue slice as Session Border Controllers claimed 38.76% of the mobile core network market share in 2025. SBCs underpin secure IP voice and mediate signaling as operators retire circuit switching. Cloud-native SBC sub-systems will grow at 9.05% CAGR by 2031, propelled by voice-over-5G and enterprise UCaaS overlays. These dynamics elevate the mobile core network market size for SBC providers that marry encryption, analytics, and slice-aware session control. Operators in markets planning 2G/3G sunsets accelerate IMS investments to maintain ubiquitous voice roaming, supporting demand visibility through 2031.

A second wave of modernization targets Voice Application Servers and CSCF nodes. Although smaller in absolute revenue, these functions enable differentiated calling features, integration with collaboration platforms, and service exposure via APIs. The mobile core network market, therefore, opens incremental value pools for software-only vendors that can deliver feature velocity and automation.

Note: Segment shares of all individual segments available upon report purchase

By 4G/5G Packet Core Controller: SMF Momentum

The Mobility Management Entity retained the largest installed base, accounting for 30.15% of the mobile core network market size in 2025. Yet its growth plateaus as operators converge on 5G Stand-Alone designs. The Session Management Function, by contrast, surges at 10.45% CAGR, emerging as the logical service anchor for PDU sessions and edge breakout. As SMF deployments rise, adjacent User Plane Function spending follows, creating a multiplier effect inside the broader mobile core network market.

Operators negotiate the coexistence of legacy SGW-C/PGW-C controllers with emerging AMF and SMF stacks. Smooth migration paths, API gateways, and common policy engines are key buying criteria. Vendors able to bundle control-plane, user-plane, and analytics layers within cloud-native constructs gain share as telcos seek integrated, slice-ready platforms.

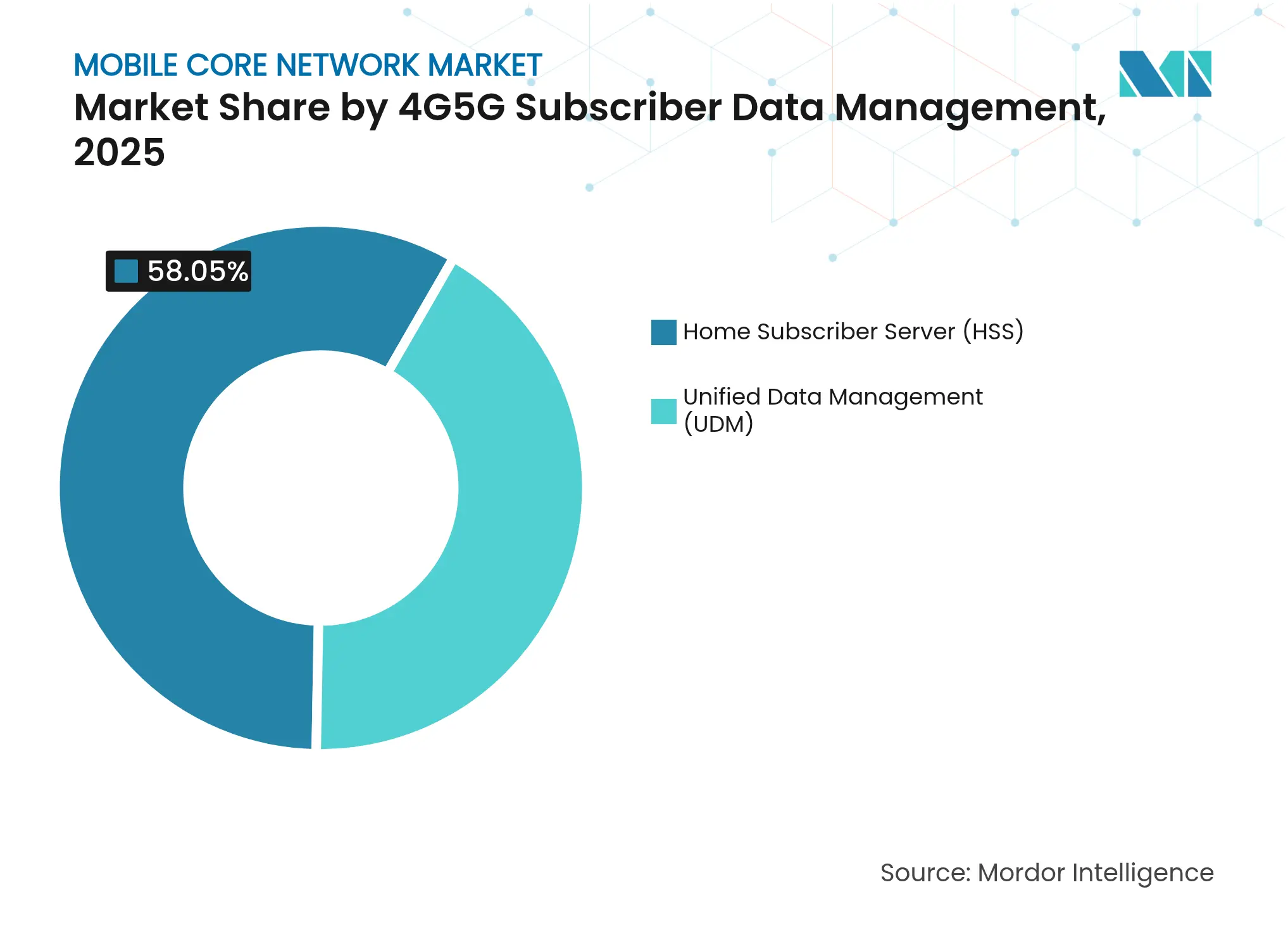

By 4G/5G Subscriber Data Management: UDM Upswing

Home Subscriber Server dominated in 2025 with a 58.05% share of the mobile core network market size. However, operators recognize the limitations of siloed HSS and increasingly adopt Unified Data Management. UDM’s 12.17% forecast CAGR reflects its ability to present a single subscriber view irrespective of radio technology, enabling micro-segmented policies and slice-specific entitlements. As UDM adoption widens, the mobile core network market sees a pivot from static provisioning toward real-time, context-aware orchestration.

Migration involves schema conversions, latency-sensitive database clustering, and northbound exposure of data via APIs to adjacent IT systems. Vendors offering low-disruption overlays win early projects. Cyber-resilience features are also decisive, given the criticality of subscriber data repositories for identity and billing.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Model: CNF Adoption Curve

Virtualized Network Functions commanded 59.05% of revenue in 2025, reflecting a decade of NFV roll-outs. Converged orchestration and shared x86 hardware drove the first cost-down wave, but operators seek deeper automation and cloud agility. Cloud-Native Functions expand at 7.98% CAGR as telcos containerise control and user planes for microservice scaling. The shift enlarges the mobile core network market as software support, Dev-Sec-Ops tooling, and managed services accompany CNF adoption.

Nevertheless, VNF-to-CNF migration is more than a technical rewrite. Telcos retrain operations teams, rediscover CI/CD pipelines, and redefine vendor contracts for consumption-based pricing. Those unable to operationalize new workflows risk extending the life of VNFs, tempering short-term displacement revenue.

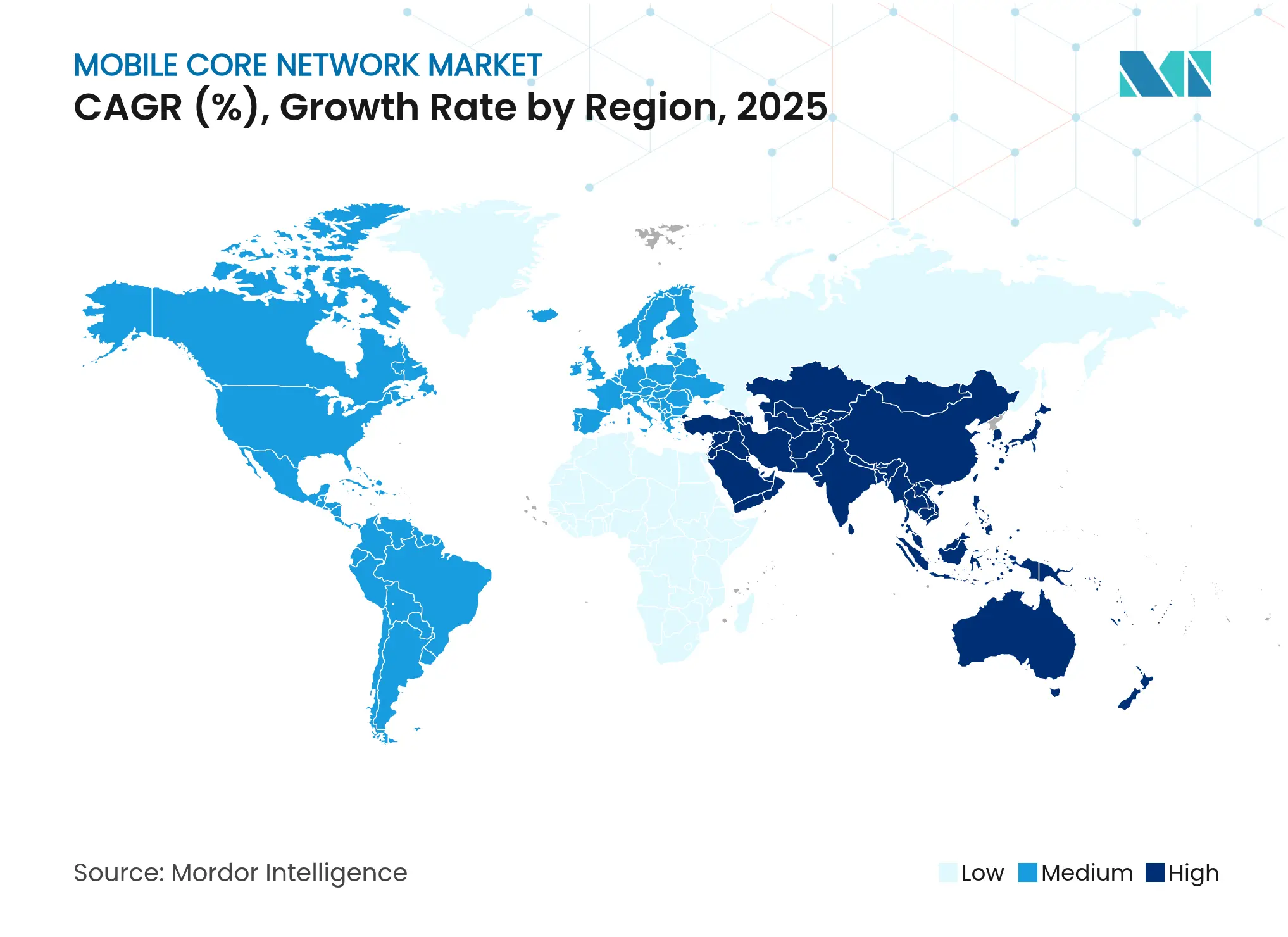

Asia-Pacific contributed 39.48% of 2025 revenue, making it the largest regional slice of the mobile core network market, LightReading. China alone invested USD 3 billion in 5G-Advanced cores in 2025 and activated 5.8 million 5G-A users across 300 cities. India’s 687 MHz spectrum reform worth USD 23.16 billion presses operators to accelerate core upgrades. Regional GDP uplift from mobile technologies reached USD 880 billion in 2023, reinforcing political commitment to telecom expansion GSMA. Combined, these factors anchor a robust addressable base for vendors throughout the forecast.

The Middle East represents the fastest-growing theatre at a 13.86% CAGR to 2031. Oil-funded infrastructure programs and sovereign digital agendas collectively escalate spending on cloud-native cores, security overlays, and AI-driven automation.

North America and Europe show mature saturation, yet modernization cycles sustain investment in the mobile core network market. Ericsson’s 54% North American revenue jump in Q4 2024 signals renewed operator spending triggered by spectrum auctions Ericsson. European telcos prioritise Open RAN and energy-efficiency, pairing them with AI-infused core upgrades for private 5G enterprise propositions. Monetisation shifts from new radio footprints to premium API access, edge compute, and intent-based network functions.

Market Concentration

Market concentration is high. Huawei, ZTE, Ericsson, and Nokia captured roughly 70% of 2024 revenue in the mobile core network market TelecomLead. Huawei’s 22% revenue rise to USD 118 billion in 2024 contrasted with Ericsson’s 5% dip and Nokia’s 21% Q4 2023 fall LightReading. Geopolitical restrictions reshape addressable territories: Huawei dominates in APAC and Middle East, while Ericsson fortifies ties in Europe and North America. Operator preference for fewer suppliers drives replacement deals such as Three UK’s migration to Ericsson’s unified core LightReading.

Technology leadership hinges on AI integration and cloud-native feature sets. Huawei premiered an AI-native core at MWC 2025, TotalTelecom released an autonomous network white paper, and Ericsson partnered with Google Cloud for core-as-a-service. Hyperscalers push deeper: Microsoft’s Azure Operator 5G Core and AWS Outposts threaten traditional vendor margins by bundling cloud credits with telco platforms. In response, legacy vendors broaden software portfolios, acquire optical players to control transport layers, and promote DevOps-centric engagement models.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A Mobile Core Network is defined as the central component of a mobile communication system responsible for providing services and data processing. It is the heart of telecommunications, responsible for routing voice, data, and multimedia traffic across vast networks.

The mobile core network market is segmented by ims core (session border controllers, voice application servers, call session control function), by 4G/5G packet core controller ((MME, SGW-C, PGW-C, AMF, SM), by 4G/5G subscriber data management (home subscriber server, unified data management), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.