Mobile Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

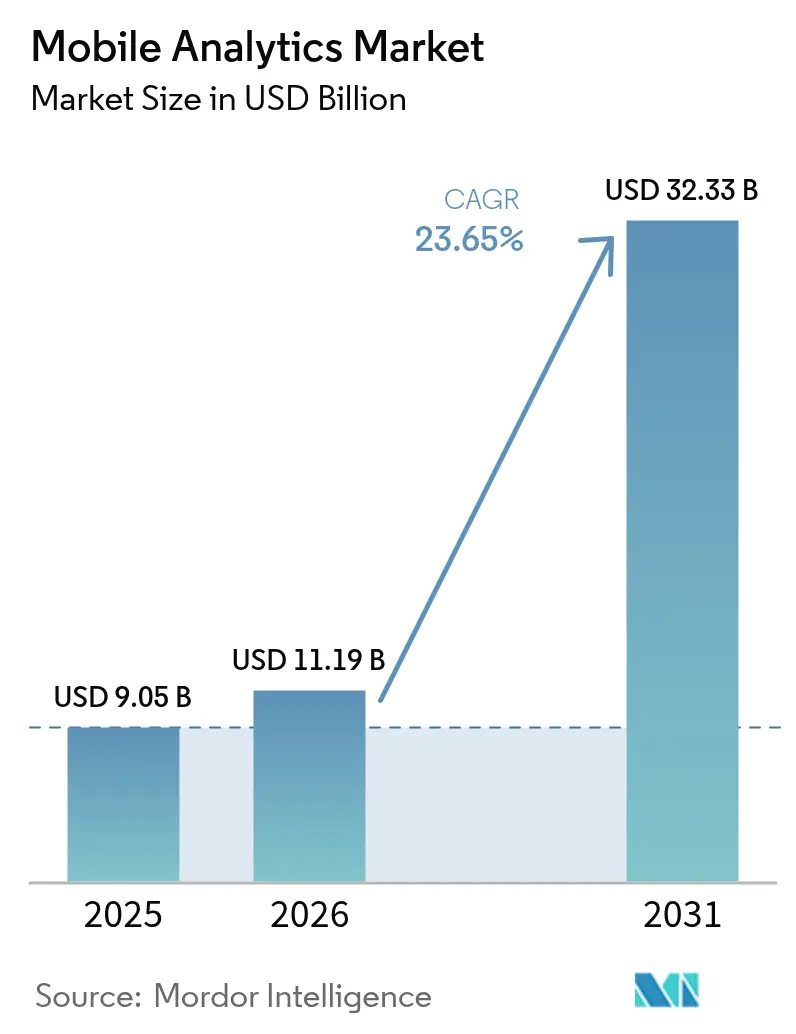

| Market Size (2026) | USD 11.19 Billion |

| Market Size (2031) | USD 32.33 Billion |

| Growth Rate (2026 - 2031) | 23.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Analytics Market Analysis by Mordor Intelligence

The mobile analytics market size was valued at USD 9.05 billion in 2025 and estimated to grow from USD 11.19 billion in 2026 to reach USD 32.33 billion by 2031, at a CAGR of 23.65% during the forecast period (2026-2031). Momentum is driven by the ubiquity of smartphones, cloud-native adoption, and the surge in mobile commerce transactions, which reached USD 3.56 trillion in 2024. Organizations are shifting spend toward behavioral measurement platforms because web-centric tools fail to capture gesture-level signals that drive mobile conversion. Widespread 5G coverage, rising mobile ad budgets, and the growing adoption of edge computing for on-device analytics further expand opportunities across the mobile analytics market. Competitive intensity is increasing as privacy regulation prompts vendors to develop cohort-based, first-party data techniques that balance insight generation with compliance.

Key Report Takeaways

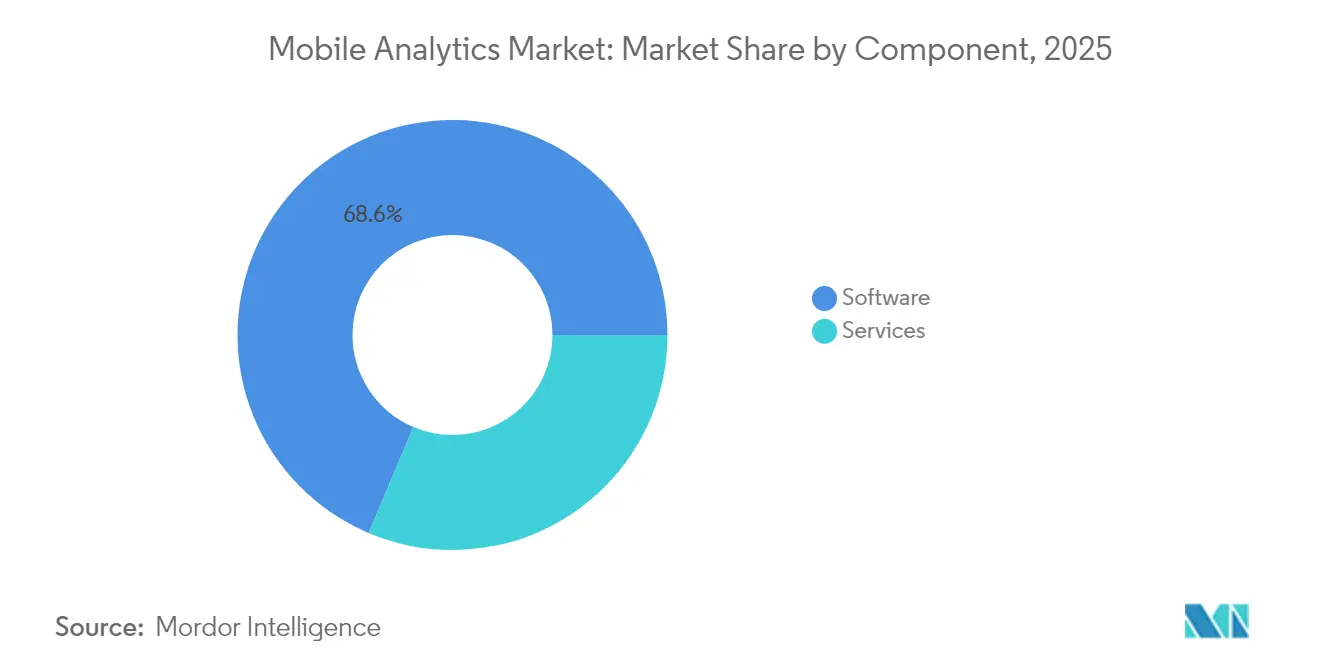

- By component, software solutions led with a 68.62% share of the mobile analytics market in 2025, while services are projected to advance at a 25.4% CAGR through 2031.

- By analytics type, application analytics held a 34.98% share of the mobile analytics market size in 2025, and in-app behavioral analytics is projected to expand at a 24.1% CAGR through 2031.

- By deployment, cloud delivery accounted for 75.88% of the mobile analytics market size in 2025; the segment is projected to rise at a 25.6% CAGR through 2031.

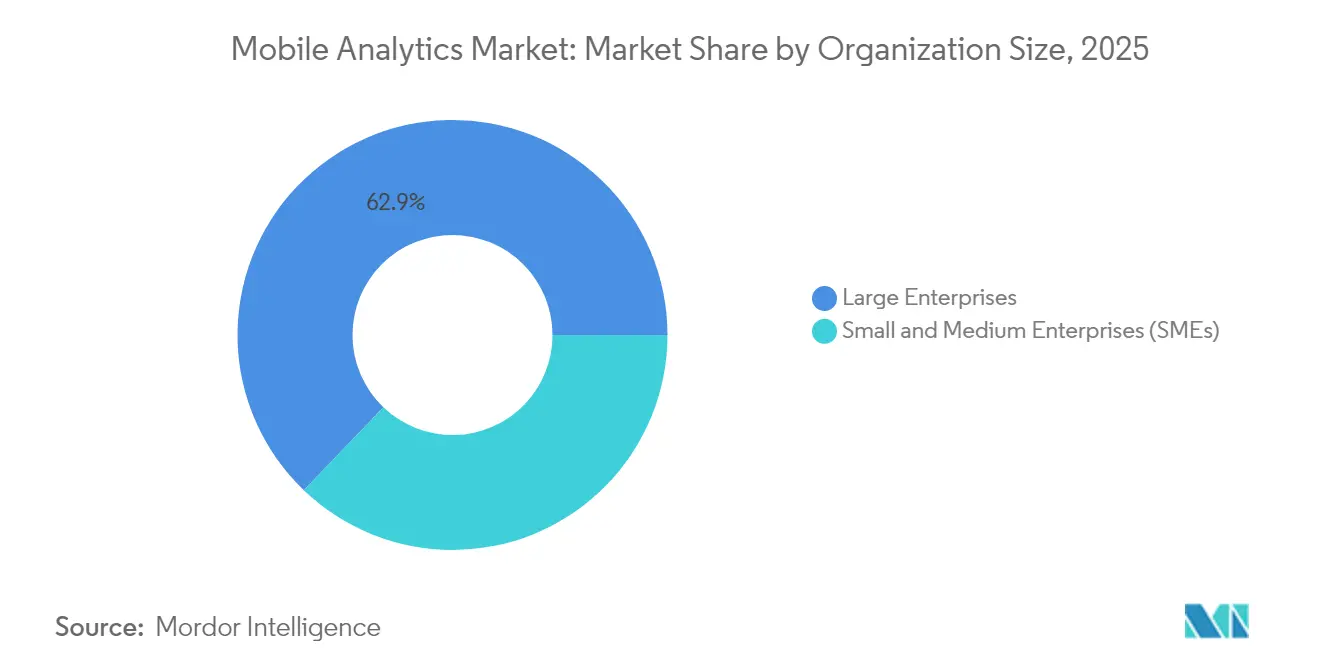

- By organization size, large enterprises generated 62.85% of revenue in 2025, whereas SMEs recorded the highest CAGR at 25.5% through 2031.

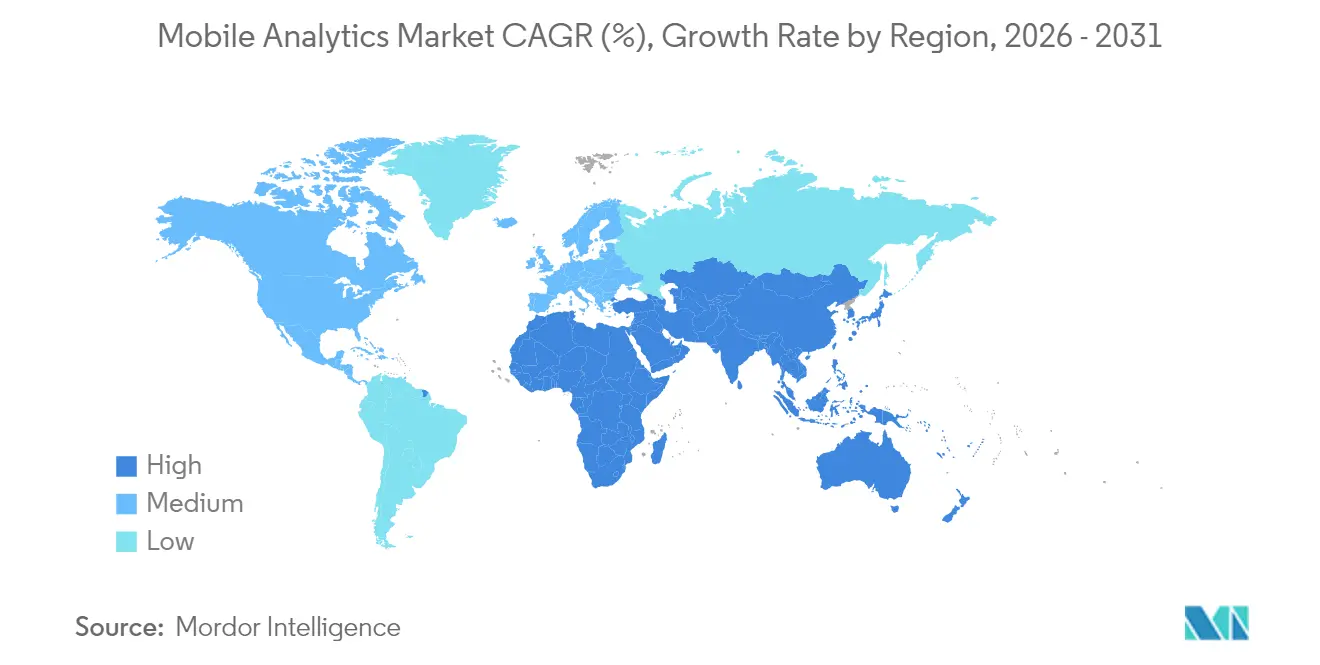

- By geography, North America captured a 38.25% revenue share in 2025; the Asia-Pacific region is the fastest-growing, with a 24.05% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone proliferation generates exabytes of behavioral data | +4.2% | Global; strongest in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Explosive growth of mobile-commerce transactions | +5.1% | Global; concentrated in North America, Europe, Asia-Pacific | Short term (≤2 years) |

| Rapid enterprise shift to cloud-native analytics platforms | +3.8% | Led by North America, Europe; Asia-Pacific following | Medium term (2-4 years) |

| Rising mobile advertising budgets driving demand for in-app insights | +4.6% | Global; emphasis on mature ad markets | Short term (≤2 years) |

| AI-powered predictive analytics enabling hyper-personalization | +3.9% | Early uptake in North America, Europe; global expansion | Long term (≥4 years) |

| On-device, privacy-preserving analytics frameworks | +2.8% | Global, driven by compliance requirements | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Smartphone proliferation generates exabytes of behavioral data.

Global smartphone users reached 6.8 billion in 2024, each device emitting roughly 2.5 GB of behavioral signals per month. Continuous streams of taps, scrolls, and location pings give enterprises fine-grained views of customer journeys, and 5G bandwidth makes real-time inference feasible. Retail apps now mine micro-gestures such as scroll velocity to predict purchase intent with up to 89% accuracy. [1]IEEE Xplore, “Mobile Behavioral Analytics in Retail Applications,” ieeexplore.ieee.org Processing at device edge is gaining ground to reduce latency and safeguard privacy, prompting vendors to ship lightweight SDKs capable of local computation. These SDKs shrink data transfer volumes and meet tightening privacy mandates while keeping performance intact, cementing edge analytics as a key value driver for the mobile analytics market.

Explosive growth of mobile-commerce transactions

Mobile commerce generated 58.9% of global e-commerce value in 2024, placing heavy emphasis on real-time journey tracking within apps. China alone processed USD 49.2 trillion in mobile payments in 2024, fueling demand for fraud detection and multi-touch attribution. [2]People’s Bank of China, “Payment System Report 2024,” pbc.gov.cn Social commerce and live-stream shopping create complex, rapid funnels that standard web tools cannot map. Vendors respond with specialized modules that stitch together purchase pathways across chat, video, and in-app stores within seconds, reinforcing the strategic relevance of the mobile analytics market to omnichannel growth agendas.

Rapid enterprise shift to cloud-native analytics platforms

Cloud deployments now host 76.43% of mobile analytics workloads, up from 61% in 2022, because elastic compute is essential for events. [3]Cloud Security Alliance, “Cloud Security Report 2024,” cloudsecurityalliance.org Amazon Web Services logged a 340% annual rise in mobile analytics ingestion during 2024. Cloud scale supports cross-platform identity stitching, churn prediction, and A/B testing that would strain on-premise clusters. Latency-sensitive apps are adopting regional edge nodes, and sovereignty concerns are pushing hybrid strategies whereby sensitive identifiers stay on-premise while behavioral data lands in the cloud for modeling. The pattern accelerates cloud-centric innovation across the mobile analytics market.

Rising mobile advertising budgets are driving demand for in-app insights.

Advertisers invested USD 362 billion in mobile campaigns in 2024, 69.4% of total digital spend. In-app placements register 88% better engagement than mobile web, pushing brands to request deeper attribution. Gaming studios, for instance, use analytics to time rewarded-video spots, lifting completion by 34%. Apple’s App Tracking Transparency cut deterministic identifiers, so vendors pivot to probabilistic matching and contextual triggers. First-party data strategies and predictive models now underpin budget allocation, sustaining double-digit expansion of the mobile analytics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent data-privacy regulations such as GDPR and CCPA | -2.3% | Europe, North America; spreading worldwide | Medium term (2-4 years) |

| High risk of mobile data security breaches | -1.8% | Global; greater in regions with weak cybersecurity | Short term (≤2 years) |

| Apple’s App Tracking Transparency limits attribution data | -2.1% | Global iOS ecosystem | Short term (≤2 years) |

| SDK fragmentation causing app-performance overhead | -1.4% | Global; acute for low-spec devices in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent data-privacy regulations such as GDPR and CCPA

Enterprises allocate about USD 1.3 million per year to keep mobile analytics stacks GDPR-ready. California’s CCPA extends similar duties to large U.S. markets, while Brazil and India draft parallel laws. Vendors embed differential privacy and federated learning so models run on decentralized data, minimizing raw collection. Google’s Privacy Sandbox for Android exemplifies this pivot, replacing cross-app identifiers with aggregated signals. Compliance lifts barriers to entry and trims the attainable growth curve for the mobile analytics market, even as it differentiates platforms that master privacy-by-design engineering.

Apple’s App Tracking Transparency limits attribution data.

Opt-in rates hover near 25%, sharply reducing deterministic user graphs. E-commerce apps lose visibility into social-discovery-to-purchase funnels, eroding ad ROI calculation accuracy by up to 30%. Vendors scramble to craft probabilistic models and SKAdNetwork integrations, yet benchmarking shows 15-30% lower precision than legacy IDFA-based tracking. First-party data activation gains salience, but smaller publishers struggle to reach the requisite scale, curbing potential spend and slowing near-term revenue for the mobile analytics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Speed Amid Software Leadership

Software products contributed 68.62% of 2025 revenue, underscoring their role as the default entry point for most buyers in the mobile analytics market. Many enterprises favor visual, self-service dashboards that plug into existing data lakes and marketing clouds without extensive coding. Yet rising regulatory complexity and SDK integration pain points elevate consulting and managed services, propelling the segment at 25.4% CAGR to 2031. Implementation partners help migrate legacy tracking setups, deploy privacy-preserving models, and tune real-time personalization engines, workstreams that internal teams often lack bandwidth for. For heavily regulated sectors such as banking, external experts design GDPR-compliant funnels that retain predictive strength while lowering data collection footprints.

Managed services address skill shortages for SMEs by bundling maintenance, data engineering, and experimentation support under subscription. As a result, services revenue captures an expanding slice of the mobile analytics market, even though core software still anchors budget line items. Vendors differentiate via industry playbooks-for instance, healthcare templates that expedite HIPAA alignment. The trend suggests a future where outcome-based service contracts accompany platform licenses, reinforcing mixed-revenue models across the mobile analytics market.

By Analytics Type: Behavioral Insights Drive Next-Level Growth

Application-analytics held a 34.98% share in 2025, thanks to its focus on acquisition, retention, and conversion metrics familiar to digital teams. Campaign analytics and service analytics follow, supporting ad attribution and customer support optimization. However, in-app behavioral analytics is scaling fastest at 24.1% CAGR as enterprises recognize that surface metrics miss crucial intent cues. Streaming services detect abandonment within 30 seconds of playback and push alternate content to improve engagement by 23%. Gaming studios read finger-pressure patterns to tune difficulty curves in real time, anchoring monetization.

Machine learning models have matured to interpret micro-gestures, context switching, and session cadence with high reliability. Consequently, behavioral analytics graduates move from mere diagnostics to predictive orchestration, positioning it as a cornerstone of value creation in the mobile analytics market. As adoption widens, the boundary blurs between behavioral analytics and AI-driven personalization, prompting vendors to bake inference engines directly into SDKs for latency-free decisioning.

By Deployment Mode: Cloud Supremacy Extends

Cloud hosts 75.88% of 2025 deployments and grows at 25.6% CAGR, underscoring elasticity as a strategic must-have. The mobile analytics market size for cloud delivery is forecast to widen its lead because hyperscalers offer serverless pipelines that ingest billions of events at marginal cost. AWS customers process over 100 billion daily events, demonstrating scale economies beyond on-premise capacity. Meanwhile, European banks pursue hybrid patterns that keep personally identifiable information on in-house clusters while sending behavioral vectors to the cloud for modeling.

On-premise remains relevant for defense and public-sector workloads that face strict sovereignty mandates, yet its share slips annually. Cloud vendors counter sovereignty objections by rolling out region-locked instances and encryption-in-use features. As these controls mature, residual resistance is expected to taper, cementing cloud as the primary battleground for innovation across the mobile analytics market.

By Organization Size: SMEs Democratize Advanced Analytics

Large enterprises supplied 62.85% of revenue in 2025, leveraging scale to embed analytics across hundreds of mobile assets. Customized attribution models and cross-device identity graphs are routine inside big-tech and tier-one retail. But SMEs post the sharpest climb at 25.5% CAGR as low-code interfaces and per-seat pricing lower entry barriers. Indie merchants on Shopify, for example, deploy analytics to fine-tune checkout flows and lift basket conversion without coding expertise.

Cloud-native vendors pre-package templates for onboarding, engagement, and monetization, shrinking time-to-value to days rather than months. As SMEs adopt, the mobile analytics market benefits from volume expansion and diversified use cases ranging from hyper-local food delivery to tele-veterinary services. This democratization also pressures vendors to simplify dashboards and abstract data science, reinforcing a user-centric design ethos.

By End-User Vertical: Healthcare Races Ahead

Retail and e-commerce controlled a 22.55% share in 2025, mirroring their dependence on funnel optimization. BFSI ranks second, deploying behavioral signals to flag fraud and tailor credit products. Government agencies embrace analytics for citizen-service KPIs, while telecom operators optimize app self-care tools. Healthcare and life sciences, though smaller today, surge at a 23.7% CAGR as telemedicine, remote monitoring, and digital therapeutics expand. Behavioral analytics improves medication adherence by 40% in pilot programs.

Regulatory backing for digital health-such as relaxed reimbursement rules for virtual visits, intensifies demand. Vendors are tailoring HIPAA-compliant SDKs that store protected health information locally while exporting anonymized signals for cohort trends. Expect health-specific feature sets like symptom-progression dashboards to proliferate, bolstering vertical diversification inside the mobile analytics market.

Geography Analysis

North America produced 38.25% of 2025 revenue owing to entrenched digital ad ecosystems, high mobile spend per capita, and robust venture funding. U.S. lawmakers shaped the regulatory agenda through CCPA, which spurred nationwide adoption of privacy-by-design data architectures. Canada shows momentum in fintech analytics, while Mexico’s expanding e-commerce base creates new white space for vendors that localize Spanish-language dashboards. The region’s deep technical workforce accelerates experimentation with edge AI, reinforcing its leadership in the mobile analytics market.

Asia-Pacific registers the fastest expansion at 24.05% CAGR through 2031. Penetration surpasses 85% in China, India, and Southeast Asia, and government schemes such as Digital India promote mobile-first citizen services. China’s social-commerce giants capture streams of voice, video, and chat that require petabyte-scale analytics, while India’s UPI framework fuels payment data growth. Japan and South Korea leverage 5G to power low-latency gaming insights, and Australia emphasizes CX optimization for banking and travel apps. Fragmented data-protection rules create integration hurdles, yet cross-border providers that secure localized hosting win share, highlighting Asia-Pacific as the prime acceleration engine in the mobile analytics market.

Europe grows steadily under tight GDPR oversight, favoring vendors with advanced consent orchestration. Germany pioneers industrial IoT analytics embedded in connected-car apps, the U.K. capitalizes on open banking trends, and France innovates in media streaming intelligence. Russia enforces compulsory data localization, isolating its ecosystem and opening room for domestic players. Despite a slower regional CAGR, Europe’s policy influence steers global roadmaps, making compliance features developed for EU clients standard elsewhere within the mobile analytics market.

Competitive Landscape

Market fragmentation is moderate: the top five vendors hold roughly 45% revenue, leaving ample space for vertical specialists. Platform owners such as Google, Apple, and Microsoft wield distribution advantage thanks to native OS hooks, while independents like Mixpanel, Amplitude, and AppsFlyer differentiate through deep-dive product analytics and attribution science. Apple’s App Tracking Transparency reshaped playbooks by stripping out IDFA, propelling demand for predictive, privacy-centric measurement. Google allocates USD 2 billion to its Privacy Sandbox to future-proof ad targeting.

Two strategy archetypes dominate the mobile analytics market. Ecosystem integrators bundle analytics with cloud or advertising suites, monetizing data synergies. Best-of-breed specialists focus on niche use cases—gaming retention loops, fintech fraud, or health compliance—commanding price premiums for domain depth. Edge-computing analytics and federated learning represent frontier battlegrounds where start-ups can leapfrog incumbents. Overall rivalry intensifies as vendors race to knit privacy, AI, and real-time orchestration into cohesive products that win enterprise wallets.

Recent consolidation underscores the competitive tempo. Sensor Tower’s USD 1.2 billion buyout of Data.ai’s analytics group forged the largest independent intelligence stack, merging store-ranking with in-app usage metrics. Microsoft Azure’s serverless Mobile Analytics Accelerator touts 60% cost reductions, pressuring rivals on TCO. Amplitude’s acquisition of Experiment integrates feature flags with behavioral data, illustrating the shift toward one-stop experimentation hubs. These maneuvers signal an arms race toward full-cycle insight platforms in the mobile analytics market.

Mobile Analytics Industry Leaders

Adobe Inc.

Alphabet Inc. (Google LLC)

Amplitude, Inc.

AppsFlyer Ltd.

Branch Metrics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Adobe rolled out Adobe Analytics Edge, a privacy-first platform that runs entirely on the device. By investing USD 200 million in edge-computing infrastructure, Adobe lets companies tap real-time mobile insights without moving personal data off the phone.

- September 2025: Salesforce wrapped up its USD 850 million purchase of MoEngage. Folding the mobile-engagement specialist into Customer 360 means Salesforce customers can now pair journey mapping and marketing automation with deep, app-level analytics—all in one place.

- June 2025: Microsoft Azure debuted an AI-Powered Mobile Analytics Suite. Using GPT-4 for automated anomaly detection and predictive modeling, the service helps teams anticipate what users will do next instead of just reading yesterday’s charts.

- January 2025: Apple expanded App Analytics with privacy-preserving cohort analysis. Developers can study user segments without personal identifiers, easing attribution headaches while keeping Apple’s strict privacy promises intact.

Global Mobile Analytics Market Report Scope

Mobile analytics refers to the sector of the technology industry focused on the collection, measurement, and analysis of data related to mobile applications and mobile websites. It involves tools and technologies used by businesses to track and understand the behavior of mobile users, as well as to optimize the performance and user experience of mobile apps. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The Mobile Analytics market is segmented by type (Application Analytics, Campaign Analytics, Service Analytics), end-user vertical (Retail, BFSI, Government, IT and Telecom, Media and Entertainment), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Software |

| Services |

| Application-Analytics |

| Campaign-Analytics |

| Service-Analytics |

| In-App Behavioral Analytics |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Retail and E-commerce |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Sector |

| Information Technology and Telecommunications |

| Media and Entertainment |

| Travel and Hospitality |

| Healthcare and Life-Sciences |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| By Analytics Type | Application-Analytics | ||

| Campaign-Analytics | |||

| Service-Analytics | |||

| In-App Behavioral Analytics | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Vertical | Retail and E-commerce | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Government and Public Sector | |||

| Information Technology and Telecommunications | |||

| Media and Entertainment | |||

| Travel and Hospitality | |||

| Healthcare and Life-Sciences | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the mobile analytics market?

The mobile analytics market size is USD 11.19 billion in 2026.

How fast is revenue expected to grow over the next five years?

Revenue is projected to climb to USD 32.33 billion by 2031 at a 23.65% CAGR.

Which deployment mode is gaining the most traction?

Cloud deployment dominates with 75.88% share in 2025 and is growing at 25.6% CAGR.

Why are in-app behavioral metrics becoming so important?

They capture gesture-level signals that predict intent more accurately than basic funnel metrics, driving higher personalization and retention.

Which region will add the most incremental revenue?

Asia-Pacific, expanding at a 24.05% CAGR, will contribute the largest incremental gains.

How are privacy regulations affecting vendor roadmaps?

GDPR, CCPA, and ATT compel vendors to adopt differential privacy, federated learning, and first-party data approaches, reshaping product features and go-to-market strategies.

Page last updated on: