Mobile Business Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.35 Billion |

| Market Size (2031) | USD 66.28 Billion |

| Growth Rate (2026 - 2031) | 22.18% CAGR |

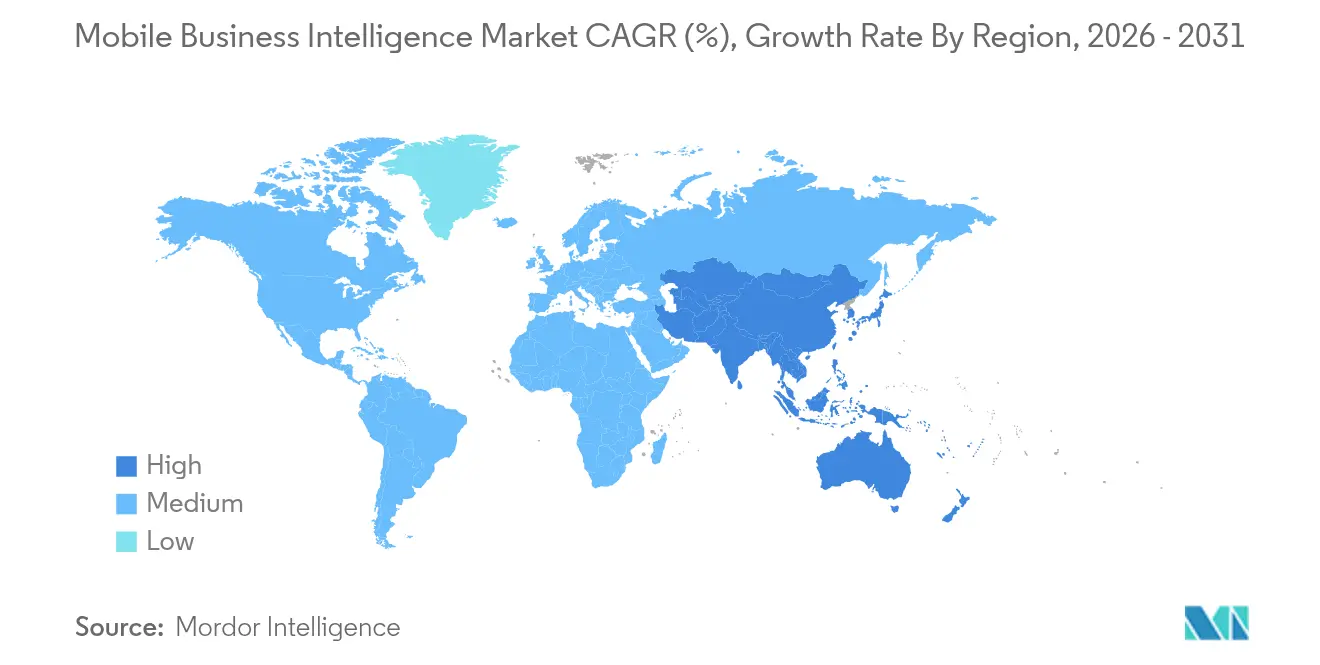

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Business Intelligence Market Analysis by Mordor Intelligence

Mobile business intelligence market size in 2026 is estimated at USD 24.35 billion, growing from 2025 value of USD 19.93 billion with 2031 projections showing USD 66.28 billion, growing at 22.18% CAGR over 2026-2031. This growth reflects the urgency to democratize data access beyond fixed desktops so that distributed employees can act on insights in real time. Strong tailwinds include 5G maturation that lowers latency, the spread of edge computing that keeps processing close to data sources, and the injection of generative AI that simplifies query creation for non-technical users[1]GSMA, “The Mobile Economy 2025,” gsma.com. Software solutions continue to outsell services, yet demand for implementation and managed offerings expands quickly as firms wrestle with complex cloud, AI, and security requirements. North America retains leadership because of mature mobility frameworks, but Asia-Pacific offers the highest upside as local enterprises accelerate digital transformation under mobile-first mandates.

Key Report Takeaways

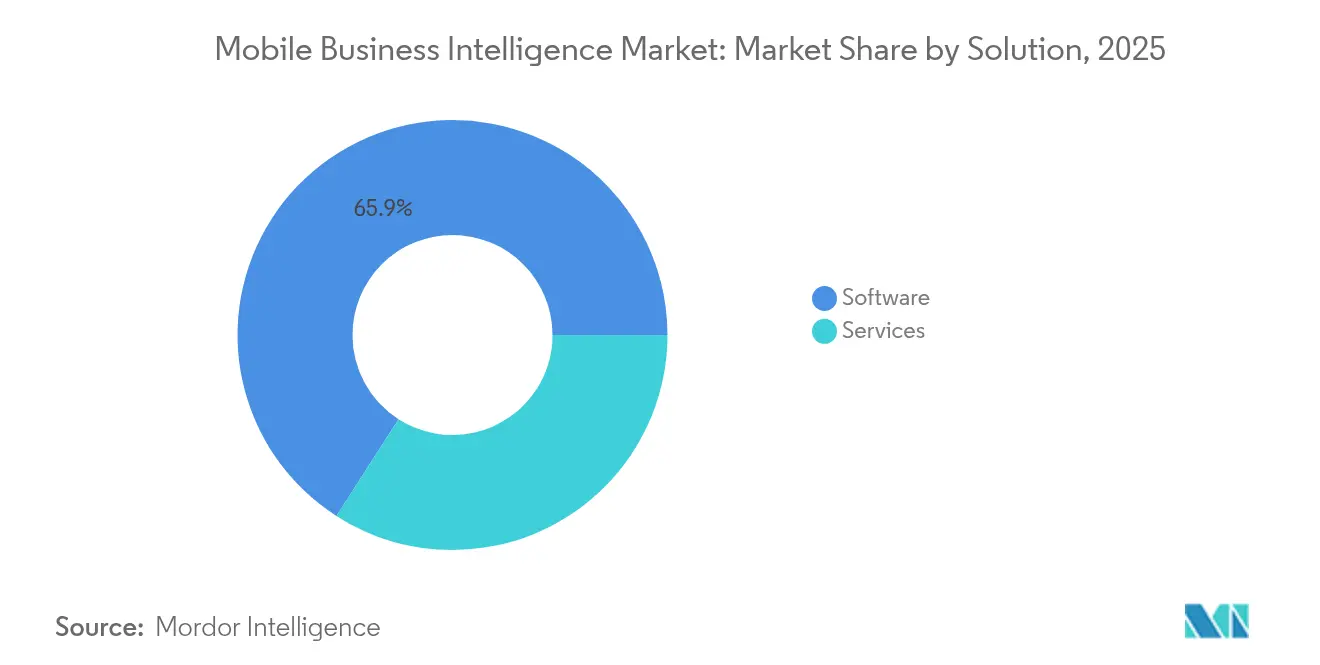

- By solution, software dominated with 65.92% revenue share in 2025, while services are forecast to grow at a 23.70% CAGR through 2031.

- By organization size, large enterprises held 74.35% of the mobile business intelligence market share in 2025; small and medium enterprises are projected to expand at a 23.35% CAGR through 2031.

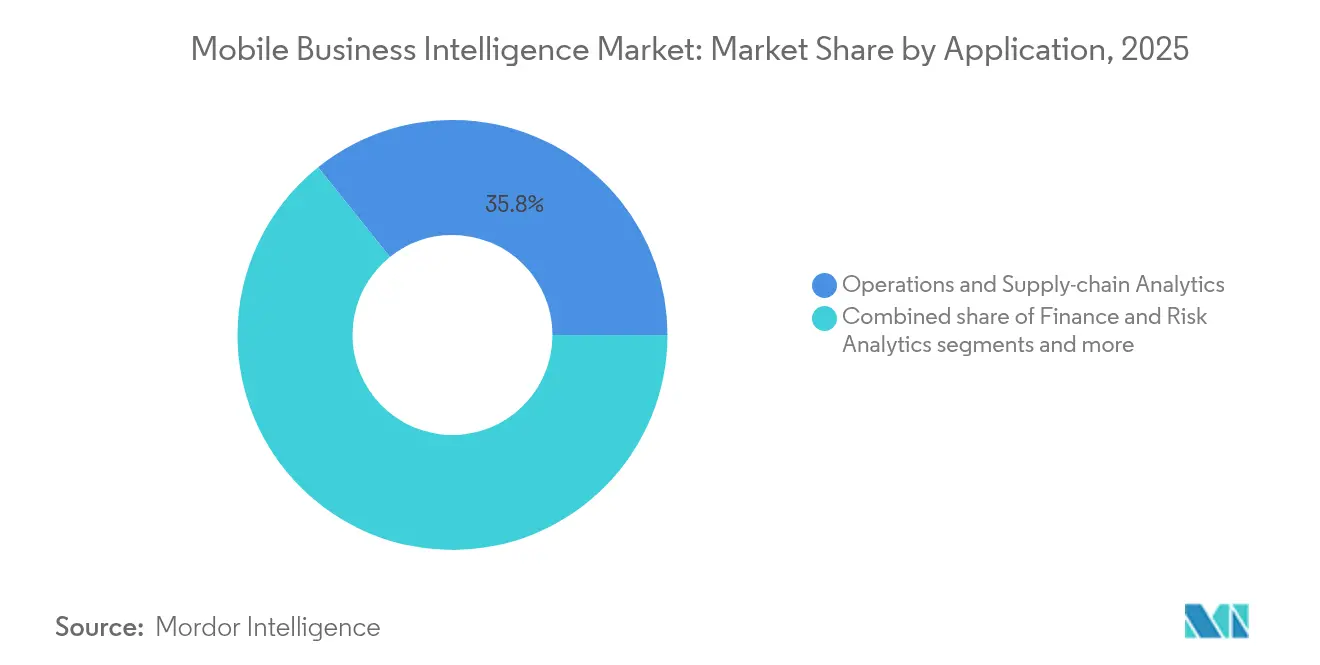

- By application, operations and supply-chain analytics captured 35.75% of the mobile business intelligence market size in 2025, whereas customer experience analytics is set to post the fastest 23.05% CAGR to 2031.

- By end-user vertical, IT and telecommunications led with 25.10% revenue share in 2025; BFSI is expected to be the fastest-growing vertical at 22.65% CAGR through 2031.

- By geography, North America commanded 36.25% of the mobile business intelligence market in 2025, while Asia-Pacific is anticipated to register the highest 22.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Mobile Business Intelligence Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first mobile BI adoption among large enterprises | +4.2% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| Surge in 5G/edge deployments enabling real-time analytics | +3.8% | Asia-Pacific core, spill-over to North America | Short term (≤2 years) |

| BYOD expansion and MDM integration in SMEs | +3.1% | Global, particularly strong in Asia-Pacific and MEA | Medium term (2-4 years) |

| Embedded analytics within SaaS apps and mobile workflows | +2.9% | North America and EU, expanding to Asia-Pacific | Long term (≥4 years) |

| Generative-AI-powered natural-language query interfaces | +2.7% | Global, concentrated in developed markets | Short term (≤2 years) |

| Telco-led “network analytics-as-a-service” offerings | +2.1% | Asia-Pacific and MEA, emerging in Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cloud-first Mobile BI Adoption Among Large Enterprises

Large corporations are swapping on-premises stacks for cloud-native mobile BI so global staff can reach dashboards without VPN friction. More than 52,000 companies actively use Microsoft Power BI, embedding analytics into Microsoft 365 work streams. The shift lowers total cost of ownership because server upkeep disappears and elastic resources scale during peak usage. SAP Analytics Cloud similarly links live transactional data with mobile visualizations while preserving strict identity controls[2]SAP, “SAP Analytics Cloud Product Documentation,” sap.com. As this model proliferates, mobile business intelligence market penetration deepens across regulated sectors that once resisted cloud migration.

Surge in 5G/Edge Deployments Enabling Real-time Analytics

Standalone 5G networks now run in seven Asia-Pacific countries, undergirding a USD 880 billion regional mobile economy that prizes responsive analytics. Edge computing moves processing to local gateways so mobile dashboards refresh in milliseconds, a necessity for factory predictive-maintenance alerts and retail shelf-stocking decisions. Financial-trading desks in Tokyo already exploit sub-millisecond feeds to price derivatives on handheld devices. These examples illustrate how 5G plus edge collectively raise usage intensity inside the mobile business intelligence market.

BYOD Expansion and MDM Integration in SMEs

Seventy percent of SMEs express awareness of analytics tools, and many now reach them first on employee-owned phones because SaaS delivery removes capital obstacles. Case studies from Croatian SMEs confirm that productivity rises when staff consult mobile dashboards, though budget limits and skill gaps still stall some pilots. Modern mobile-device-management suites containerize business apps and allow remote wipes, addressing most privacy concerns. Microsoft Intune’s screenshot-blocking for iOS illustrates continuous hardening that reassures finance teams about sensitive KPI exposure.

Embedded Analytics Within SaaS Apps and Mobile Workflows

SaaS vendors now bake analytics straight into mobile interfaces, eliminating context switching between CRM and BI tools. Salesforce’s planned USD 8 billion purchase of Informatica highlights demand for built-in data management that outputs predictive insights to field sellers on phones. Tableau Next pushes “agentic” analytics, where AI agents surface anomalies directly inside mobile views instead of waiting for users to open static dashboards. Industry-specific SaaS platforms replicate the pattern, giving health-care clinicians bedside decision support without extra training.

Restraints Impact Analysis of Mobile Business Intelligence Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent security and privacy concerns on personal devices | −2.8% | Global, particularly acute in regulated industries | Medium term (2-4 years) |

| Limited mobile dashboard usability for complex analysis | −2.1% | Global, affecting enterprise adoption rates | Short term (≤2 years) |

| Data-governance fragmentation across multi-cloud estates | −1.9% | North America and EU, expanding globally | Long term (≥4 years) |

| App-store policy changes throttling SDK data capture | −1.4% | Global, with iOS/Android policy dependencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Security and Privacy Concerns on Personal Devices

Sixty percent of enterprises cite mobile security as the main barrier to broader BI rollout despite clear sales-performance gains. BYOD policies mingle consumer and corporate apps, raising leakage risks that new Apple privacy manifests only partly mitigate. Banks and hospitals often restrict mobile BI to company-issued phones, slowing penetration in high-value verticals even as encryption and biometric log-ins improve.

Limited Mobile Dashboard Usability for Complex Analysis

Small screens hinder side-by-side visual comparisons and multi-step filtering, reducing analyst productivity versus desktop setups. Academic experiments show cognitive load rises when users must remember prior views instead of pinning them onscreen, hampering situation awareness during complex tasks. Vendors respond by prioritizing fewer but sharper indicators on mobiles, yet power users still revert to laptops for deep dives, capping certain revenue streams in the mobile business intelligence market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Mobile Business Intelligence Market Segment Analysis

By Solution:

Services Accelerate Through AI IntegrationSoftware remains the revenue cornerstone, supplying visualization tools, query engines and governance layers that earned a 65.92% share in 2025. These offerings anchor most enterprise analytics stacks and integrate with identity suites, data warehouses and low-code platforms. Still, surging demand for implementation, customization and managed operations means service providers are booking faster contracts than license vendors. Many clients now outsource fine-tuning of large language models, edge-deployment scripts and zero-trust controls because internal teams lack bandwidth. The mobile business intelligence market size for services is projected to expand at high double-digit CAGR through 2031 as organizations shift from pure software spend toward outcome-based engagements.

Consulting firms bundle data engineering, user-training and day-two optimization so clients can unlock value soon after go-live. Managed-services partners sign multiyear agreements to keep mobile apps patched, monitor usage and refine semantic layers, freeing business units to focus on insight consumption instead of platform care. MicroStrategy’s listing on Google Cloud Marketplace illustrates the trend: automated provisioning trims deployment timelines, while certified partners step in for ongoing governance. These patterns reinforce a service-rich growth arc likely to continue even as self-service tooling improves.

By Organization Size:

SME Adoption Driven by Cloud EconomicsLarge enterprises controlled 74.35% revenue in 2025 because they possess global operations, ample IT staff, and compliance obligations that favor robust mobile BI suites. They embed analytic graphs into ERP and CRM workflows so thousands of employees can track KPIs in the field. Multi-tenant governance, single sign-on, and fine-grained role controls satisfy auditors in finance, healthcare, and public-sector domains. Despite this dominance, the small-business segment now logs the briskest expansion as turnkey SaaS lowers entry barriers.

SMEs appreciate pay-as-you-go subscriptions, automated scaling, and wizard-based report builders that appear within familiar productivity suites. The mobile business intelligence market size for SMEs is forecast to climb steeply as founders seek instant visibility into cash flow, inventory, and customer sentiment without spinning up expensive on-prem databases. Croatian survey data shows that adoption success correlates with top-management sponsorship and clear performance targets. As app stores flood with pre-built connectors to Shopify, QuickBooks, and Stripe, smaller firms can join data-driven cultures without hiring data scientists, underscoring why this cohort will keep outpacing the overall mobile business intelligence industry.

By Application:

Customer Experience Analytics Leads GrowthOperations and supply-chain analytics held 35.75% of 2025 revenue thanks to IoT-linked factories, fleet telematics, and warehouse systems that broadcast metrics to supervisors on tablets. These use cases thrive when edge nodes preprocess sensor streams so only anomalies travel to a cloud dashboard, saving bandwidth and enabling real-time intervention. The mobile business intelligence market continues to prize uptime gains and cost avoidance yielded by predictive maintenance pathways.

Customer-experience analytics meanwhile records the highest 23.05% CAGR because every interaction point—store beacons, chatbots, loyalty apps—spits out data that marketing teams can adjust on the fly. Field sellers view propensity scores before meetings, while service agents see churn risk gauges as soon as a call arrives. In hospitality, geo-fenced promotions trigger only when a guest’s mobile app beacons inside the lobby. These responsive moments shrink decision cycles from hours to seconds and directly impact revenue, explaining why boards approve incremental analytics budgets even during cost-control periods. Where data stays sparse, AI fills gaps with look-alike modeling, sustaining the growth curve.

By End-user Vertical:

BFSI Accelerates Through Regulatory ComplianceIT and telecommunications enterprises led with a 25.10% share in 2025 by virtue of deep in-house engineering talent and constant network-performance monitoring needs. Staff rely on phone dashboards to diagnose traffic spikes, allocate spectrum, and alert customers during outages. Telecoms also monetize anonymized location data, adding external revenue lines that flow back into analytics enhancements.

BFSI shows the sharpest 22.65% CAGR as banks deploy mobile BI for fraud detection, instant credit scoring, and branch foot-traffic analysis. Regulators now require near real-time suspicious-activity reports, making handheld dashboards essential for compliance officers. Insurers blend weather feeds with claim histories to pre-stage adjusters before storms hit. Fin-tech challengers push incumbents faster by offering clients portfolio heat maps inside consumer apps, setting new service benchmarks. Each advance reinforces mobile BI’s status as a regulatory and competitive necessity, driving sustained investment.

Geography Analysis

North America Mobile Business Intelligence Market

North America kept 36.25% of global revenue in 2025, anchored by ubiquitous LTE-Advanced coverage, swift 5G roll-outs, and enterprise familiarity with mobile security frameworks. Silicon Valley vendors pilot novel features—voice query, camera-based data capture—domestically before global releases, giving the region early productivity gains. Tight integrations with Microsoft Entra ID and Okta simplify identity propagation from desktop to phone, boosting active-user counts. High labor costs also motivate firms to chase analytics-driven efficiency, ensuring continued budget allocation for upgrades in the mobile business intelligence market.

APAC Mobile Business Intelligence Market

Asia-Pacific stands out with a projected 22.85% CAGR through 2031 as governments subsidize 5G spectrum and mandate data-localization that favors cloud regions inside national borders. China’s e-commerce giants stream petabyte-scale telemetry into real-time dashboards that optimize flash sales in minutes. India’s Unified Payments Interface pushes billions of daily transactions into analytics clouds, letting banks refine fraud models on smartphones carried by rural agents. Many ASEAN manufacturers skip legacy MES systems and adopt mobile dashboards first, illustrating a leapfrog effect that expands the mobile business intelligence market size faster than any other region.

EMEA and LATAM Mobile Business Intelligence Market

Europe posts steady expansion under the weight of GDPR, sustainability targets, and Industry 5.0 strategies. Utilities use mobile BI to monitor renewable generation, while carmakers rely on handheld analytics to coordinate just-in-sequence deliveries. Strict privacy rules encourage pseudonymization and on-device encryption, raising development complexity but also differentiating vendors that pass compliance audits. Meanwhile, Latin America and the Middle East and Africa open fresh territory. Brazil’s PIX instant-payment network feeds behavioral data to fintechs hungry for mobile insights. Gulf telcos bundle analytics dashboards with enterprise data plans, selling one-stop mobility plus intelligence to oil-field operators, hospitals, and smart-city managers.

Regulatory Landscape

Mobile business intelligence is shaped by privacy, data-residency, and AI governance rules that affect how dashboards, embedded analytics, and GenAI-driven query interfaces are used on smartphones and tablets. In the European Union, GDPR requirements continue to drive encryption, access control, and pseudonymization practices for mobile analytics, while the European Data Protection Board (EDPB) strengthened practical compliance in July 2026 by issuing Guidelines 02/2026 on anonymisation, a consideration for BI platforms that aggregate and share insights across teams.

AI-specific compliance is tightening alongside privacy. Under the EU AI Act (Regulation 2024/1689), transparency obligations and enforcement powers for general-purpose AI providers start on 2 August 2026, affecting mobile BI features that incorporate generative AI, conversational interfaces, and automated narrative insights. China published GB/T 47469-2026 in April 2026 (effective 1 November 2026) as a management guide for personal information processing in mobile internet apps, which increases implementation demands for in-scope mobile BI deployments operating in China, particularly around data handling on mobile endpoints and within app ecosystems.

Value Chain Analysis

The mobile business intelligence value chain starts with data generation and access (enterprise apps, IoT telemetry, and transactional systems), then moves into integration and modeling layers (connectors, semantic layers, and governance), and finally into analytics engines and mobile delivery (dashboards, embedded analytics, and conversational BI). Hyperscaler cloud platforms and identity/security stacks typically sit underneath these deployments, while mobile OS and app-distribution policies influence which analytics SDKs can collect and how apps handle permissions, offline caching, and device-level security.

For many vendors, go-to-market and delivery are partner-led, with system integrators, cloud marketplaces, and distributors driving implementation and local support. Qlik highlighted in 2025 that indirect routes account for over 80% of its revenue, underscoring the role of channel ecosystems in scaling mobile analytics adoption. Regional distribution partnerships such as Qlik and Redington (announced January 2025) support localization across the Middle East and Africa, while collaborations including Mobileum and Telkomsel (announced September 2025) show how connectivity providers and analytics specialists combine to deliver enterprise-grade, real-time insight services in mobile-centric markets.

Competitive Landscape

The market shows moderate concentration because a quartet of platform giants—Microsoft, SAP, IBM, and Salesforce—own broad product suites, large partner ecosystems, and entrenched enterprise contracts. Their roadmaps focus on embedding generative AI throughout the stack, automating data preparation, visualization, and even narrative explanation inside mobile apps. IBM alone earmarked USD 150 billion in cumulative AI investments, including watsonx X and domain-specific model hubs, underscoring the escalating budget bar for top-tier innovators. These incumbents cross-sell BI modules into ERP, CRM, and office software, creating lock-in that dampens share erosion.

Nimble challengers such as ThoughtSpot, Sisense, and Domo compete by simplifying UX and targeting greenfield mid-market accounts. They tout sub-five-minute deployment and consumption-based pricing, resonating with digital natives who scorn perpetual licenses. Several specialize: ThoughtSpot builds search-first experiences; Sisense wraps analytics into vertical SaaS; Domo stresses embedded connectors for citizen developers. Edge-focused players emerge too, pitching container-portable runtimes that analyse machine data at the factory line before syncing summaries to the cloud. Such specialization diversifies the mobile business intelligence market without yet unseating the leaders.

Strategic partnerships intensify rivalry. Snowflake leverages Microsoft Azure OpenAI Service so customers can tap large language models inside Teams chats, pulling live metrics without leaving collaboration threads. MicroStrategy’s Marketplace listing fast-tracks procurement for Google Cloud tenants and unlocks revenue-share incentives for service partners. Telcos form analytics alliances to bundle bandwidth, compute, and dashboards in one invoice. Collectively, these maneuvers sharpen competitive edges and accelerate product cycles, ensuring end users receive frequent innovations that keep demand high.

Mobile Business Intelligence Industry Leaders

IBM Corporation

Microsoft Corporation

SAP SE

SAS Institute

MicroStrategy Incorporated

- *Disclaimer: Major Players sorted in no particular order

Mobile Business Intelligence Market Companies Covered in this Report

- Microsoft Corporation

- SAP SE

- IBM Corporation

- Salesforce Inc. (Tableau)

- Oracle Corporation

- QlikTech International AB

- SAS Institute

- MicroStrategy Inc.

- TIBCO Software

- Sisense Inc.

- ThoughtSpot Inc.

- Google LLC (Looker)

- Domo Inc.

- Yellowfin International

- Phocas Software

- Zoho Corporation

- Board International

- Dundas Data Visualization

- TARGIT A/S

- e-Zest Solutions Ltd.

- Information Builders Inc.

Market Opportunities and Future Outlook

A key opportunity is shifting mobile BI from static dashboards to agentic, AI-augmented interaction models that reduce reliance on specialist analysts and speed frontline decisions. In 2026, vendor roadmaps and launches reflect this direction, including Tableau (Salesforce) unveiling an agentic analytics platform with headless analytics and voice query integration for mobile (May 2026), and Qlik expanding Qlik Cloud Analytics with agentic AI capabilities (June 2026). This creates whitespace for services around governance, model oversight, and secure deployment patterns that help keep mobile experiences responsive while addressing tightening privacy and AI transparency requirements.

Another opportunity is operationalizing mobile BI as a real-time layer across distributed environments where data locality and latency matter, including IoT-heavy operations, field service, and telecom-led enterprise offerings. Partnerships that combine network data, edge processing, and analytics platforms (for example, Mobileum and Telkomsel in Indonesia, announced September 2025) point to demand for packaged outcomes rather than standalone reporting tools. As data fabrics and cross-platform integration patterns (for example, SAP reference architectures aligning data across platforms) become more common, vendors and integrators can differentiate through faster connector deployment, embedded analytics within business workflows, and mobile-first security controls that support BYOD while maintaining auditability.

Recent Industry Developments in Mobile Business Intelligence Market

- June 2026: Bloomberg selected Apptopia to provide mobile app consumer activity data on the Bloomberg Terminal. The selection elevates mobile-app telemetry as a mainstream input for enterprise and financial analytics workflows, increasing demand for tools that turn mobile-first datasets into decision-ready dashboards.

- May 2026: Tealium unveiled AI at the Edge capabilities alongside mobile SDK enhancements to support on-device data transformations and edge inference. The company pushes more analytics processing closer to mobile endpoints, aligning with low-latency mobile BI use cases while reducing the need to transmit sensitive raw data to centralized clouds.

- October 2024: Microsoft announced a EUR 4.3 billion investment in cloud and AI data center capacity in Italy. The expanded regional capacity supports data-residency requirements and higher-performance analytics workloads, strengthening the infrastructure base for cloud-first mobile BI deployments across Europe.

Mobile Business Intelligence Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the mobile business intelligence market is the revenue earned from software and related services that let business users access, analyze, and act on dashboards and reports through smartphones and tablets, either via cloud or on-premise setups.

Scope exclusions: Hardware devices, desktop-only BI tools, and generic reporting modules that do not offer a true mobile interface are not counted.

Segments Covered in This Report

- By Solution

- Software

- Mobile BI Platforms

- Data Visualization Tools

- Dashboard and Reporting Apps

- Services

- Professional Services

- Managed Services

- Software

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Application

- Sales and Marketing Analytics

- Finance and Risk Analytics

- Operations and Supply-chain Analytics

- HR and Workforce Analytics

- Customer Experience Analytics

- By End-user Vertical

- BFSI

- IT and Telecommunications

- Healthcare and Life Sciences

- Retail and E-commerce

- Government and Public Sector

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand context for mobile analytics usage and enterprise software spending, then narrowing it to mobile BI specific revenue streams. We referenced public sources such as the US Census Bureau for digital economy signals, the US Bureau of Labor Statistics for wage and employment trends tied to analytics roles, and the International Telecommunication Union for smartphone and mobile broadband penetration patterns.

To keep the sizing grounded, we also reviewed sources such as the World Bank for macro indicators, OECD digital economy publications for adoption readiness, and academic journals on mobile decision support, security, and usability constraints. Company annual reports, investor presentations, and product documentation were used to understand packaging, deployment mix, and how mobile access is sold inside broader analytics suites. Paid subscriptions were used selectively for company financial intelligence, patent checks, and shipment level import export data when relevant for validation. The sources listed here are illustrative, and we also relied on other public references to collect, cross-check, and clarify inputs.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with software providers, system integrators, and enterprise buyers that deploy mobile BI for field, sales, and executive users. These conversations were used to confirm what is treated as paid mobile BI versus bundled access, and to validate adoption pace across major regions and industry verticals where mobile workforces are common.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 48% |

| Mid tier: 54% | Functional/Unit leaders: 36% | EMEA: 31% |

| Smaller Players: 15% | Managers: 50% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where enterprise analytics spend and mobile workforce enablement indicators are converted into a realistic mobile BI demand pool, and then filtered by adoption and monetization behavior. To keep the totals practical, we corroborate the outcome with selective bottom-up approximations, such as sampled vendor revenue disclosures, channel checks on subscription pricing, and a volume by average selling price build for mobile-enabled BI seats in a few high-usage industries.

Key inputs that shape the model include smartphone and mobile broadband penetration, the share of employees working in field or distributed roles, cloud adoption in enterprise software, security and compliance requirements that influence services attachment, and the mix of bundled versus stand-alone mobile BI licensing. Where bottom-up signals are patchy, gaps are handled by using bracketed ranges from interviews, and then tightening those ranges with public product packaging logic so the same revenue is not counted twice.

For forecasting, scenario analysis is used, and the drivers are moved each year based on how experts expect mobile-first workflows, cloud migration, and AI-assisted querying to change rollout speed. The final path is chosen after checking that it stays consistent with macro IT spending direction and the observed pace of platform upgrades in large organizations.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and then stress-tested for variances that look too high or too low versus the adoption reality shared by practitioners. We check internal consistency across regions and user cohorts, and anomalies trigger follow-up calls to re-check assumptions such as bundling rates, service attachment, and currency timing.

Before sign-off, the model is reviewed in steps so calculations, definitions, and boundary conditions match the market description. Reports are refreshed annually, and interim updates are done when material events can shift demand, such as major platform changes, regulatory actions affecting mobile data access, or sharp macro slowdowns. Right before delivery, an analyst performs a fresh pass to make sure the latest public signals are reflected.

Mordor Intelligence's Mobile Business Intelligence Market Size Measured Against Other Published Estimates

Published market values for mobile business intelligence can differ quite a bit, even when the topic label looks identical. In our experience, the gaps usually come from what is counted as mobile BI revenue, how bundling inside broader analytics subscriptions is handled, and whether services are included as part of the same market.

By checking subscription packaging and refresh cadence, Mordor Intelligence keeps the scope tied to mobile-enabled BI software and related services, which avoids inflating totals with hardware, desktop-only analytics, or generic reporting access that is not truly mobile. Differences also show up when a study uses an older base year, applies aggressive adoption curves for mobile-first workstyles, or converts currencies using different timing, which can shift the reported USD size for the same calendar year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.93 B (2025) | |

| Industry Publisher A | USD 10.72 B (2024) | Uses an earlier base year and a different forecast window, and its scope treatment can vary by including broader enterprise BI revenues that are mobile-accessible, which can compress the stated 2024 total versus a later-year definition. |

| Research Portal B | USD 18.26 B (2024) | The estimate leans on a base year where mobile BI may be counted alongside wider analytics platform modules and business-function apps, and differences in currency timing and bundling assumptions can move the 2024 value up or down. |

The spread in the table is mostly explained by year alignment and what gets included when mobile access is sold inside a wider analytics subscription. When the boundary is kept consistent and inputs like adoption pace, bundling, and services attachment are checked with practitioners, the resulting number becomes easier to trace and repeat in future updates.

Key Questions Answered in the Report

What is the current size of the mobile business intelligence market?

The market is valued at USD 24.35 billion in 2026 and is forecast to climb to USD 66.28 billion by 2031, reflecting a 22.18% CAGR.

Which region is growing the fastest for mobile BI solutions?

Asia-Pacific shows the highest growth momentum with a projected 22.85% CAGR through 2031, powered by rapid 5G roll-outs and mobile-first digital initiatives.

Why are services outpacing software in growth?

Enterprises need specialized help with AI integration, edge deployments, and security hardening, so the services segment is expanding at a 23.70% CAGR despite software retaining the larger revenue share.

How do 5G and edge computing influence mobile BI adoption?

They cut latency to sub-millisecond levels, enabling real-time analytics for manufacturing, retail, and financial trading use cases, which adds a +3.8% uplift to the overall market CAGR.

What is the biggest barrier to broader enterprise uptake?

Security and privacy concerns on employee-owned devices remain the chief obstacle, subtracting an estimated 2.8% from the market’s CAGR forecast.

Which industry vertical will grow the fastest?

BFSI is projected to expand at a 22.65% CAGR as banks and insurers adopt mobile dashboards for fraud detection, compliance monitoring, and personalized customer engagement.

Page last updated on: