Mitochondrial Disease Therapies Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

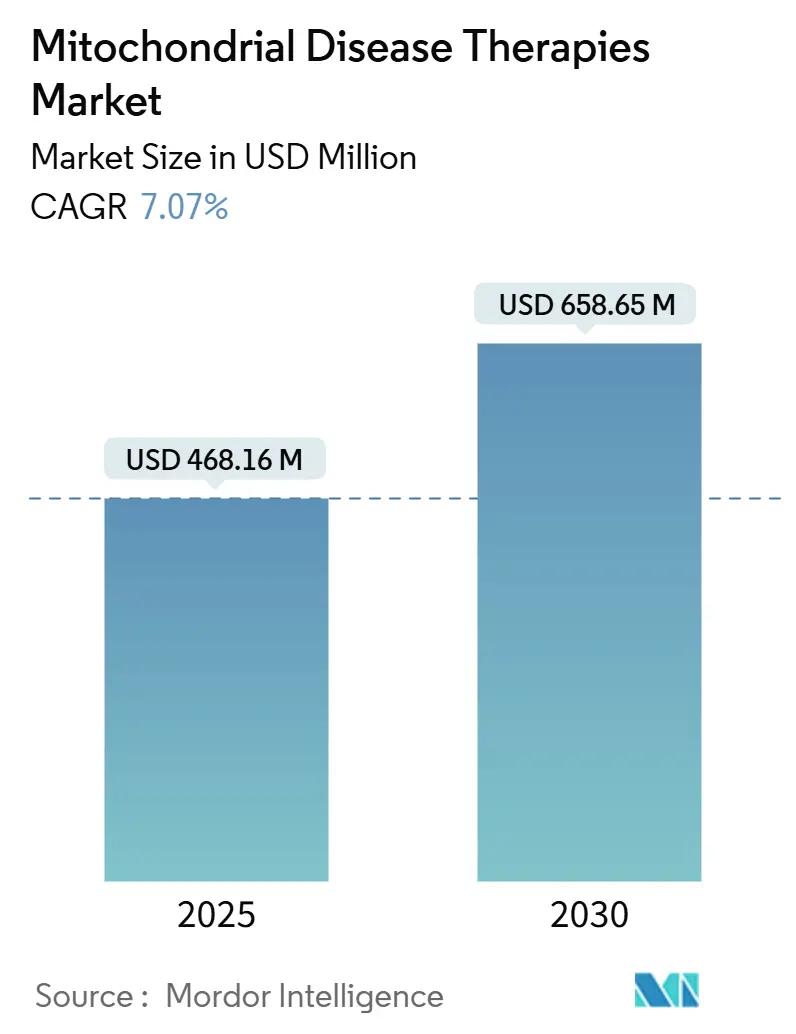

| Market Size (2025) | USD 468.16 Million |

| Market Size (2030) | USD 658.65 Million |

| Growth Rate (2025 - 2030) | 7.07% CAGR |

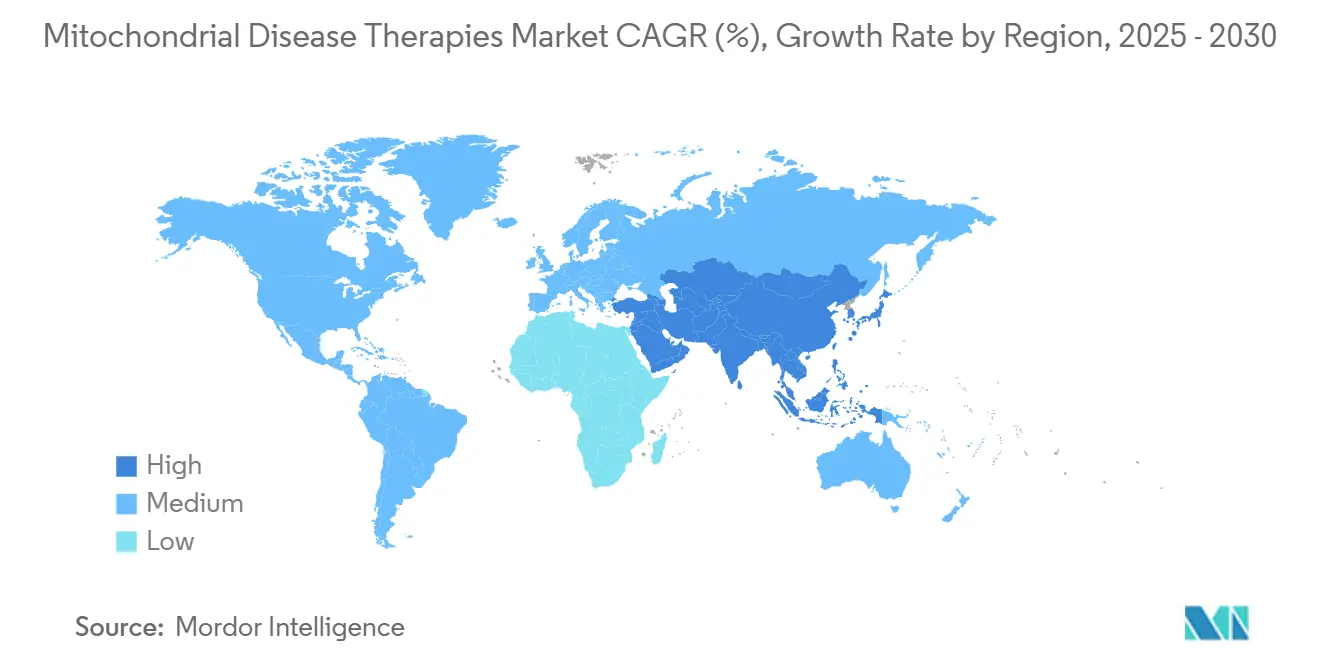

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mitochondrial Disease Therapies Market Analysis by Mordor Intelligence

The mitochondrial disease therapies market size reached USD 468.16 million in 2025 and is projected to climb to USD 658.65 million by 2030, translating to a 7.07% CAGR over the forecast window. Expansion is anchored in three mutually reinforcing forces: first, the maturing regulatory playbook that shepherded the LUMEVOQ gene therapy through European review; second, rising confidence in gene-editing precision tools such as TALEN and double-strand-break-free base editors; and third, an unprecedented influx of venture and philanthropic capital that offsets the high cost of trials involving ultra-rare patient pools. Clinical milestones in mitochondrial transplantation for Leigh syndrome and acute cardiac injury have widened the therapeutic horizon, while defense-funded research is translating battlefield insights into civilian care pathways. At the same time, real-world evidence registries are tightening trial designs and shortening recruitment cycles, giving the mitochondrial disease therapies market a structurally higher growth runway despite lingering cost and manufacturing constraints.

Key Report Takeaways

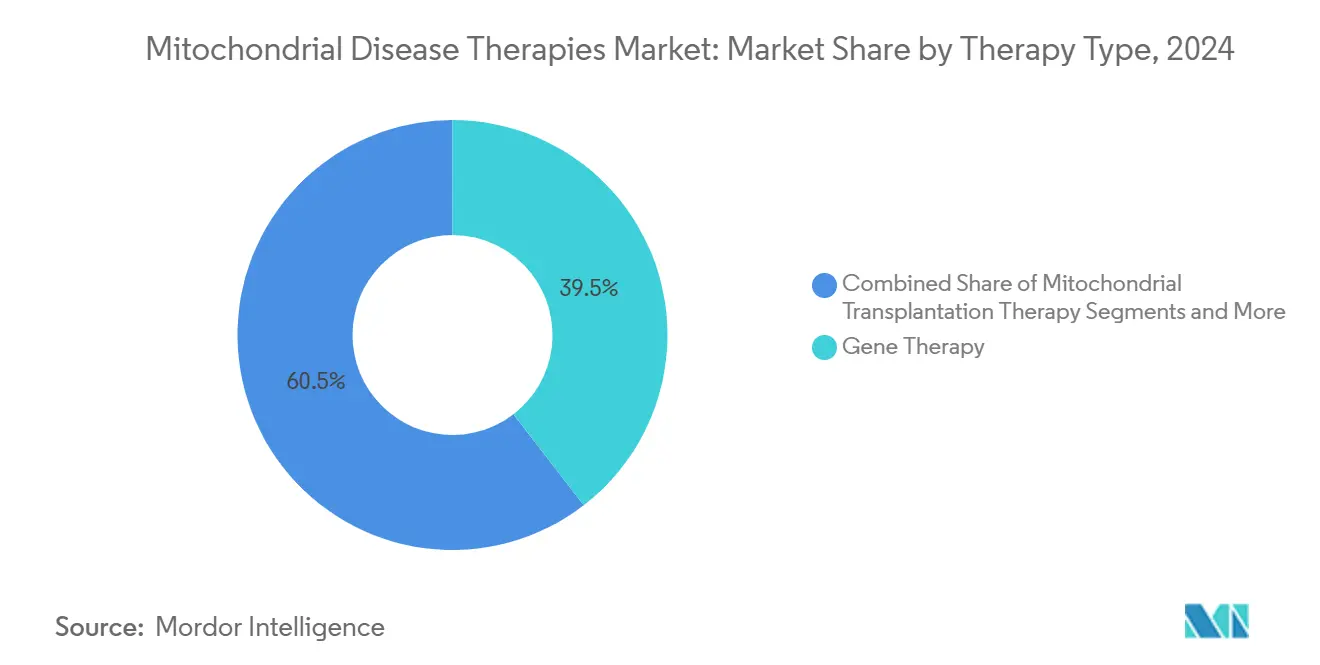

- By therapy type, gene therapy captured 39.54% of mitochondrial disease therapies market share in 2024, whereas mitochondrial transplantation therapy is forecast to expand at an 11.11% CAGR through 2030.

- By disease indication, Leber hereditary optic neuropathy accounted for 34.81% of the mitochondrial disease therapies market size in 2024, while Leigh syndrome is advancing at a 10.36% CAGR to 2030.

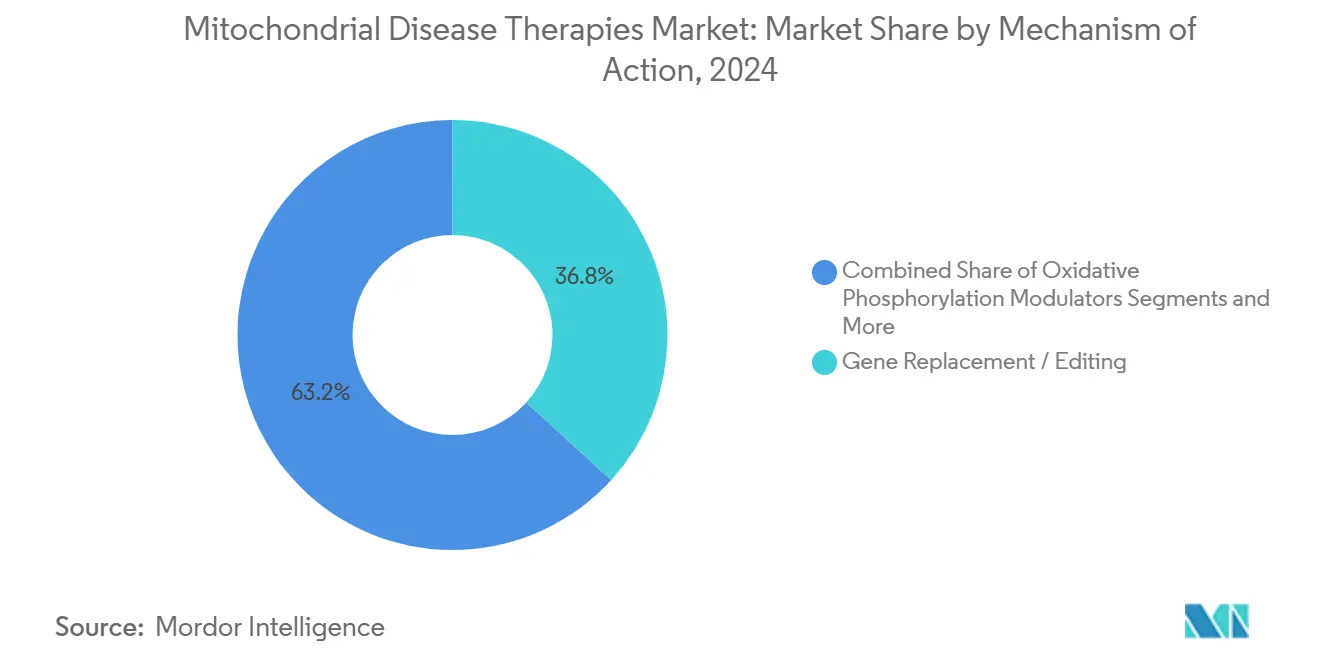

- By mechanism of action, gene replacement/editing held 36.78% share of the mitochondrial disease therapies market size in 2024, whereas mtDNA degradation tools are poised to grow at a 10.66% CAGR over the same period.

- By route of administration, the intravitreal route led with 41.28% share of the mitochondrial disease therapies market size in 2024, while the intravenous route shows the highest projected CAGR at 9.48% through 2030.

- By geography, North America commanded 44.36% of mitochondrial disease therapies market share in 2024, whereas Asia-Pacific is set to register a 9.83% CAGR through 2030.

Global Mitochondrial Disease Therapies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gene-Therapy Approvals For LHON & FA | +1.8% | Global, with early gains in US, EU | Medium term (2-4 years) |

| Orphan-Drug Incentives & Venture Funding Influx | +1.2% | North America & EU | Short term (≤ 2 years) |

| Advancing Mtdna-Editing Platforms (Talens, Ddcbe) | +1.5% | Global, concentrated in US, Japan | Long term (≥ 4 years) |

| AI-Guided Repurposing Of Metabolic Modulators | +0.9% | Global | Medium term (2-4 years) |

| Military Funding For Acute Mitochondrial Injury Counter-Measures | +0.6% | US, with spillover to allied nations | Long term (≥ 4 years) |

| Growing Use Of Real-World Evidence Registries | +0.8% | Global, led by US and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gene-Therapy Approvals for LHON & FA

Recent approvals and late-stage reviews of ocular and systemic gene therapies have reduced development risk across the mitochondrial disease therapies market. GenSight’s LUMEVOQ continues to meet efficacy benchmarks in LHON long-term follow-up data, reinforcing confidence in AAV-mediated delivery.[1]GenSight Biologics, “LUMEVOQ Receives Positive Regulatory Opinion,” gensight-biologics.com Parallel progress in Friedreich’s ataxia cardiomyopathy trials by Lexeo Therapeutics signposts the feasibility of systemic mitochondrial gene correction. Regulatory clarity generated by these programs is prompting portfolio expansion into other primary mitochondrial diseases, while standardizing surrogate endpoints such as heteroplasmy shift and ATP production. Investors are consequently accepting longer timelines, and big-pharma partners are structuring co-development deals that transfer vector platform know-how across indications. Collectively, these developments lift valuation multiples for early-stage assets and amplify deal flow in the mitochondrial disease therapies industry.

Orphan-Drug Incentives & Venture Funding Influx

Global venture deployment into mitochondrial disease programs surpassed USD 500 million in 2024, reflecting the combined pull of orphan-drug tax credits, seven-to-ten-year exclusivity windows, and payer tolerance for disease-modifying modalities. Abliva’s SEK 200 million raise and Mission Therapeutics’ GBP 25.2 million round showcase how dedicated funds can bridge capital gaps for programs serving fewer than 10,000 patients worldwide. Public-sector participation, illustrated by Khondrion’s EUR 5 million innovation credit, further stretches runway for pivotal trials. Funding momentum is also enabling multi-indication platform plays, where a single editing scaffold or antioxidant backbone is iterated across heterogeneous mutations. Policy makers view these incentives as catalysts for domestic bio-innovation, creating a virtuous cycle of grant funding, spinouts, and manufacturing infrastructure that reinforces regional leadership in the mitochondrial disease therapies market.

Advancing mtDNA-Editing Platforms (TALENs, DdCBEs)

Precision editing has crossed from bench to clinic as double-strand-break-free editors now achieve controlled heteroplasmy shifts without off-target nuclear edits. Fujita Health University demonstrated mutation-load reductions in MELAS syndrome cells using platinum TALENs, a finding that is currently being translated into first-in-human studies.[2]Naoki Yahata, “Engineered Enzymes Enable Precise Control of Mitochondrial DNA Mutation Levels,” Fujita Health University, phys.org Complementary lipid-nanoparticle carriers such as MITO-Porter have reached 20% in-cell editing efficiencies, clearing a key delivery hurdle.[3]Yuma Yamada, “Lipid Nanoparticle Delivery of CRISPR/Cas9 System Into Mitochondria,” Nature Scientific Reports, nature.com Process-development work is now focused on aligning plasmid-free manufacturing steps with good-manufacturing-practice (GMP) standards to satisfy regulatory reviewers. As editing pipelines mature, platform developers anticipate rapid mutation-agnostic indications, thereby enlarging the mitochondrial disease therapies market size addressable by a single therapeutic backbone. These advances underpin the fastest-growing mechanism-of-action segment and intensify competition for scarce GMP-grade vector capacity.

AI-Guided Repurposing of Metabolic Modulators

Machine-learning algorithms trained on mitochondrial interactomes are surfacing small molecules capable of enhancing oxidative phosphorylation or stabilizing POLG enzyme function. Pretzel Therapeutics’ PZL-A candidate, identified through graph-based screening, progressed from computational hit to IND-enabling studies within 18 months. Algorithm-informed repositioning curtails early-stage attrition by leveraging known safety data, and it aligns well with regulators’ push for real-world evidence to support label extensions. Integration of registry data enables refined subgroup matching, lowering enrollment thresholds for proof-of-concept studies. The approach is particularly beneficial in ultra-rare subsets where de novo discovery would be cost-prohibitive. As a result, AI-based pipelines now compete head-to-head with traditional high-throughput screening for venture backing, widening the funnel of candidates feeding the mitochondrial disease therapies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-Small Addressable Patient Pools Per Mutation | -1.4% | Global | Long term (≥ 4 years) |

| Clinical-Trial Recruitment Hurdles & Heterogenous Endpoints | -1.1% | Global, acute in US and EU | Medium term (2-4 years) |

| High COGS For AAV Vectors & Mitochondrial Isolation | -0.9% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Regulatory Uncertainty Around Mitochondrial Transplantation | -0.7% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-Small Addressable Patient Pools per Mutation

Individual mtDNA mutations often affect fewer than 1,000 patients globally, stalling commercial scale-up even if biological proof is iron-clad. Fragmented prevalence forces sponsors to pursue basket or mutation-agnostic designs that complicate statistical powering and regulatory engagement. Commercial models forecast high price points to recoup costs, yet payer pushback intensifies as more single-mutation therapies reach market. Programs therefore lean on platform economics—shared vectors, analytics, and manufacturing suites—to dilute fixed costs. Patient-advocacy groups are responding by building global mutation registries to tighten prevalence estimates and refine trial stratification. Until multiplexed editing or transplantation approaches mature, the mitochondrial disease therapies market must navigate a structurally constrained revenue base despite scientific optimism.

Clinical-Trial Recruitment Hurdles & Heterogeneous Endpoints

Phenotypic variability within and across mitochondrial diseases muddies endpoint selection and elongates follow-up periods. Functional scales validated in neuromuscular disorders may miss ophthalmologic gains, while biochemical markers lack universal cut-offs. Limited specialized centers mean travel burdens fall on families, reducing enrollment for already sparse populations. Sponsors increasingly adopt decentralized trial technologies and home-based biomarker collection to blunt attrition. Regulators are open to innovative designs but still demand clinically meaningful outcomes, pushing developers to hybridize objective and patient-reported measures. The result is elongated timelines that weigh on smaller firms’ cash positions, tempering the mitochondrial disease therapies market growth that would otherwise flow from scientific breakthroughs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Gene Therapy Dominance Amid Cellular Innovation

Gene therapy retained a commanding 39.54% slice of mitochondrial disease therapies market share in 2024, buoyed by AAV platforms that offer well-established manufacturing and regulatory moats. Early ophthalmologic success has de-risked systemic applications, and several sponsors now pursue multi-organ delivery protocols to capture larger patient pools. Although pharmacological agents and nutraceuticals continue to serve as symptomatic bridges, their incremental value propositions pale beside the mutation-level correction achievable with vectorized payloads. Mitochondrial transplantation therapy, while contributing the smallest revenue today, recorded an 11.11% CAGR and is positioned to reset clinical expectations by providing immediate ATP-generation capacity in acute contexts.

Competitive behavior is shifting accordingly. Vector suppliers are vertically integrating plasmid production to guarantee slot availability, while cell-therapy entrants court contract development and manufacturing organizations (CDMOs) for rapid scale-out. Developers are experimenting with hybrid regimens that pair gene editing with mitochondrial supplementation to bridge onset-of-action gaps. Such combinations enhance durability without sacrificing near-term functional gains, offering payers a clearer cost-benefit signal. As manufacturing costs decline and delivery efficiency rises, gene therapy is expected to retain pole position, but cellular modalities will chip away share as clinical evidence stacks up.

By Disease Indication: LHON Leadership Challenged by Leigh Syndrome Growth

Leber hereditary optic neuropathy held 34.81% of mitochondrial disease therapies market size in 2024, reflecting extensive natural-history knowledge, validated visual-acuity endpoints, and relatively straightforward intravitreal delivery. Therapeutic saturation in LHON, however, sets the stage for portfolio diversification. Leigh syndrome is advancing at a 10.36% CAGR, reflecting robust mitochondrial transplantation data and combination nucleoside therapies that mitigate POLG-related biochemical deficits.

Sponsors are recalibrating R&D priorities toward central-nervous-system and cardiometabolic phenotypes where unmet need is high and competitive density remains low. Basket trials that enroll across multiple POLG variants enable scale efficiencies, while adaptive-design protocols shorten development cycles. The success of these strategies will diffuse therapeutic attention across a broader set of indications, gradually reducing LHON’s share of the mitochondrial disease therapies market.

By Mechanism of Action: Gene Replacement Leads as Editing Tools Accelerate

Gene replacement and editing captured 36.78% of mitochondrial disease therapies market share in 2024, driven by the proven track record of AAV-mediated payloads. Rapid manufacturing learning curves and improved capsid libraries have lowered immunogenicity risks, hastening systemic-delivery programs. Base-editing and mtDNA degradation tools trail in absolute revenue but represent the fastest-growing sub-segment at 10.66% CAGR; their appeal lies in selectively extinguishing mutant genomes, a feat unachievable with conventional replacement approaches.

Oxidative-phosphorylation modulators and mitochondrial biogenesis enhancers continue to serve synergistic roles by optimizing cellular energy balance post-gene correction. Developers increasingly engineer combo products embedding both genetic and metabolic payloads, thereby widening indications and improving clinical-benefit durability. These convergent strategies are likely to reinforce the dominance of mechanism-platform companies in the mitochondrial disease therapies market.

By Route of Administration: Intravitreal Dominance Faces Systemic Challenge

Intravitreal injections accounted for 41.28% of mitochondrial disease therapies market size in 2024, thanks to LHON-centric portfolios and established delivery comfort among retinal specialists. Safety experience with ocular dosing de-risked the first wave of approvals and built clinician familiarity. Yet the systemic burden of many mitochondrial disorders fuels interest in intravenous platforms posting a 9.48% CAGR, supported by rising confidence in capsid engineering that navigates hepatic sequestration and off-target uptake.

Oral formulations preserve relevance in chronic management, especially for antioxidant and cofactor products tuned for long-term adherence. Subcutaneous depots under evaluation promise at-home administration and improved pharmacokinetic smoothing. Ultimately, route choice is evolving into a disease-manifestation algorithm: local ocular delivery for optic neuropathies, systemic dosing for multi-organ pathologies, and combination-route regimens for phenotypically complex patients.

Geography Analysis

North America controlled 44.36% of mitochondrial disease therapies market share in 2024, underpinned by FDA orphan-drug incentives, concentrated expertise in rare-disease centers, and investor appetite for high-return niche biopharma. Federal agencies such as the Department of Defense and Veterans Affairs pump non-dilutive funds into acute-injury and transplantation research, reinforcing domestic pipeline density. Reimbursement dialogues also tilt favorably due to established outcomes-based payment frameworks that accommodate single-infusion gene therapies.

Asia-Pacific is projected to expand at a 9.83% CAGR to 2030, buoyed by Japan’s regenerative-medicine fast tracks, Australia’s Maeve’s Law enabling mitochondrial donation trials, and China’s growing footprint of accredited gene-therapy manufacturing suites. Regional governments deploy grants and tax incentives to reduce entry barriers for domestic innovators, while multinational firms form joint ventures to secure capacity and navigate local compliance. Europe remains a steady performer, leveraging cross-border registries and Horizon Europe funding to sustain collaborative research hubs.

Competitive Landscape

Fragmentation defines today’s mitochondrial disease therapies market. No single mechanism dominates clinical practice, and the top five players collectively control well under 30% of revenue, creating white space for innovation. Companies differentiate on platform breadth, with Stealth BioTherapeutics focusing on mitochondria-targeted peptides, GenSight on ocular AAV vectors, and Minovia on autologous mitochondrial transplantation. The absence of entrenched incumbents lowers partnering friction, so pipeline-rich start-ups frequently syndicate trials with academic consortia that provide both patients and mechanistic expertise.

Manufacturing capacity acts as a bottleneck and strategic prize. CDMOs such as Lonza strike multi-year supply pacts for GMP-grade AAV, underpinning pipeline timelines and acting as kingmakers for cash-constrained biotechs. Meanwhile, modular point-of-care guidelines drafted by regulators like the UK MHRA hint at decentralized manufacturing models that could upend traditional supply chains. Intellectual-property strategy increasingly involves bundling vector capsid claims with disease-specific biomarker panels to create multi-layered moats.

Competition will intensify as proof-of-concept data accumulates across transplant and editing modalities. Strategic mergers aimed at marrying vector platforms with cell-processing know-how are likely, while big-pharma interest will hinge on the scalability of manufacturing and the predictability of payer uptake. Until then, nimble biotech specialists remain the primary value creators in the mitochondrial disease therapies industry.

________________________________________

Mitochondrial Disease Therapies Industry Leaders

Stealth BioTherapeutics

GenSight Biologics

Santhera Pharmaceuticals

Reata Pharmaceuticals

Astellas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Minovia Therapeutics received FDA Fast Track and Rare Pediatric Disease designations for MNV-201 in Pearson syndrome.

- May 2025: Khondrion secured up to EUR 5 million in Innovation Credit from the Netherlands Enterprise Agency to fund a Phase 3 trial of sonlicromanol.

- May 2025: Stealth BioTherapeutics reported an FDA-endorsed path forward for elamipretide in Barth syndrome.

- November 2024: The Mito Fund invested in Khondrion to accelerate Phase 3 development of sonlicromanol.

Global Mitochondrial Disease Therapies Market Report Scope

| Gene Therapy |

| Pharmacological Agents |

| Nutraceuticals & Supplements |

| Mitochondrial Transplantation Therapy |

| Mitochondria-Targeted Antioxidants |

| Leber Hereditary Optic Neuropathy (LHON) |

| Mitochondrial Myopathies |

| Leigh Syndrome |

| MELAS |

| Other Primary MDs |

| Oxidative Phosphorylation Modulators |

| Gene Replacement / Editing |

| Mitochondrial Biogenesis Enhancers |

| mtDNA Degradation Tools |

| Enzyme / Cofactor Replacement |

| Oral |

| Intravenous |

| Intravitreal |

| Subcutaneous |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Gene Therapy | |

| Pharmacological Agents | ||

| Nutraceuticals & Supplements | ||

| Mitochondrial Transplantation Therapy | ||

| Mitochondria-Targeted Antioxidants | ||

| By Disease Indication | Leber Hereditary Optic Neuropathy (LHON) | |

| Mitochondrial Myopathies | ||

| Leigh Syndrome | ||

| MELAS | ||

| Other Primary MDs | ||

| By Mechanism of Action | Oxidative Phosphorylation Modulators | |

| Gene Replacement / Editing | ||

| Mitochondrial Biogenesis Enhancers | ||

| mtDNA Degradation Tools | ||

| Enzyme / Cofactor Replacement | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intravitreal | ||

| Subcutaneous | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the mitochondrial disease therapies market?

The mitochondrial disease therapies market size stood at USD 468.16 million in 2025.

How fast is the market expected to grow through 2030?

The market is forecast to expand at a 7.07% CAGR, reaching USD 658.65 million by 2030.

Which therapy type is leading in revenue share?

Gene therapy leads with 39.54% market share, reflecting its regulatory traction and clinical efficacy.

Which region is growing the quickest?

Asia-Pacific is projected to post the fastest CAGR of 9.83% between 2025 and 2030.

What is the biggest challenge in developing treatments?

Ultra-small patient pools for individual mutations complicate trial design, scaling, and reimbursement.

Are there any approved mitochondrial transplantation therapies yet?

Clinical programs are advancing rapidly, but as of 2025 none have received full regulatory approval; Fast Track designations signal accelerating pathways.

Page last updated on: