Parkinson's Disease Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

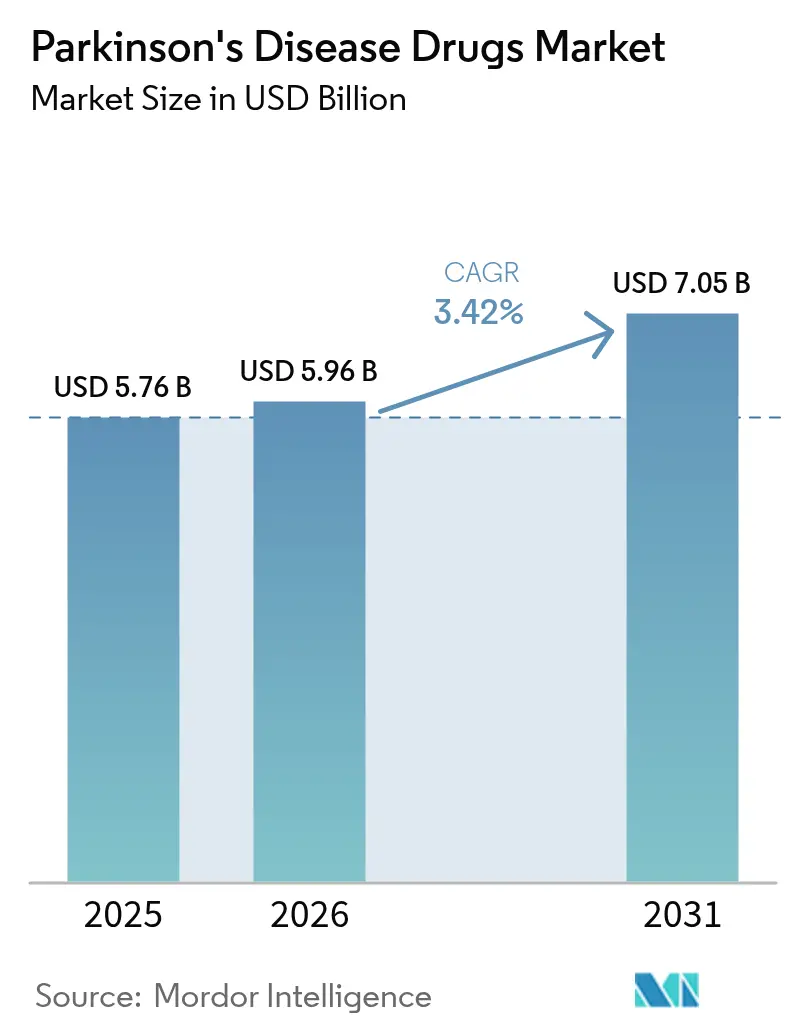

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 7.05 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

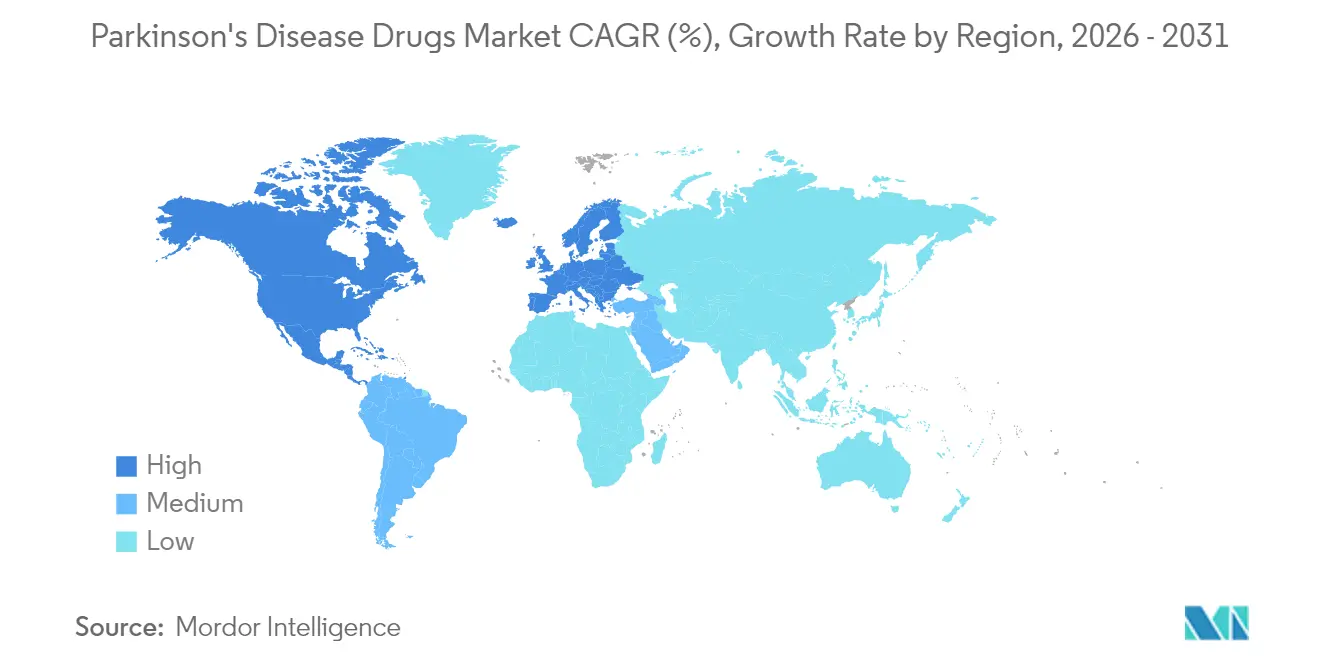

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Parkinson's Disease Drugs Market Analysis by Mordor Intelligence

The Parkinson's disease drugs market size was valued at USD 5.76 billion in 2025 and estimated to grow from USD 5.96 billion in 2026 to reach USD 7.05 billion by 2031, at a CAGR of 3.42% during the forecast period (2026-2031). Growth reflects an expanding patient pool and steady uptake of both symptomatic and disease-modifying options. Carbidopa–levodopa combinations retain commercial primacy, yet adenosine A2A antagonists advance fastest as clinicians seek complementary non-dopaminergic relief. Continuous infusion devices win clinical favor for reducing motor fluctuations, while digital pharmacies widen access to therapy. North America preserves revenue leadership, whereas Asia Pacific posts the quickest expansion as aging trends accelerate and reimbursement frameworks broaden.

Key Report Takeaways

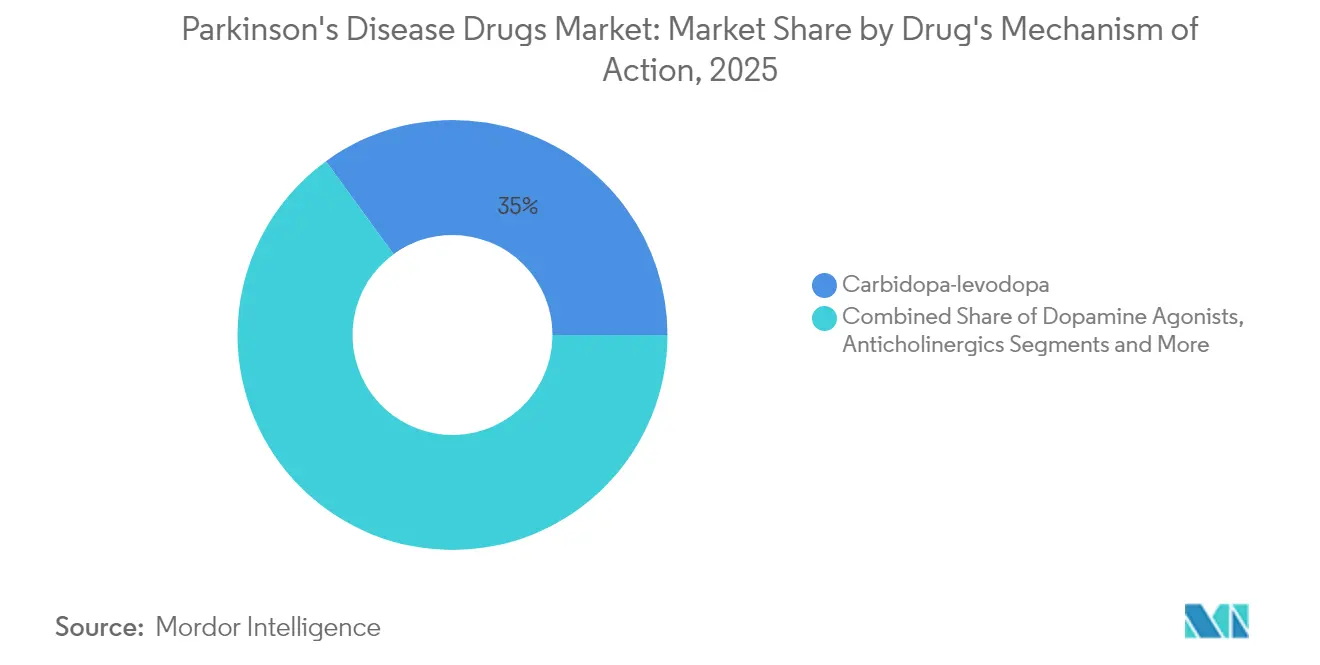

- By mechanism of action, carbidopa–levodopa commanded 35.02% of Parkinson's disease drugs market share in 2025; adenosine A2A antagonists are forecast to grow at 4.10% CAGR to 2031.

- By route of administration, oral formulations held 75.05% share of the Parkinson's disease drugs market size in 2025, while infusion systems are projected to expand at 4.21% CAGR through 2031.

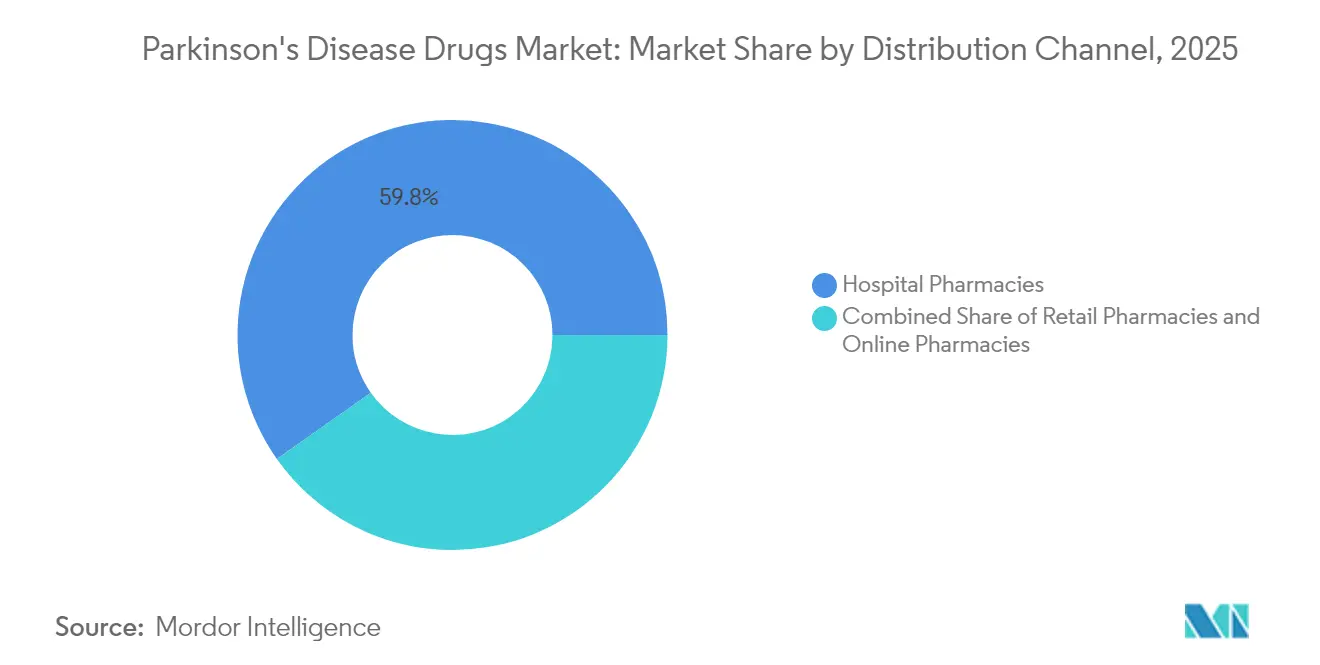

- By distribution channel, hospital pharmacies accounted for 59.78% revenue in 2025; online pharmacies are the fastest-growing channel at 4.93% CAGR to 2031.

- By geography, North America led with 44.02% share of the Parkinson's disease drugs market in 2025; Asia Pacific is advancing at a 5.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Parkinson's Disease Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population & disease burden | +1.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Growing awareness & early diagnosis initiatives | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expanding reimbursement & insurance coverage | +0.6% | North America & EU | Short term (≤ 2 years) |

| Increasing R&D investment & continuous approvals | +0.9% | Global, led by North America | Medium term (2-4 years) |

| Adoption of long-acting continuous infusions | +0.4% | North America & EU | Medium term (2-4 years) |

| AI-driven α-synuclein drug-repurposing pipelines | +0.3% | Global research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population & Rising Disease Burden

The global Parkinson patient base is projected to reach 25.2 million by 2050, more than doubling its 2021 level as longevity increases worldwide. East Asia shoulders the largest absolute case growth, while western Sub-Saharan Africa records the steepest percentage rise, steering investment toward region-tailored care models [1]Li Zhang, “Regional Differences in Parkinson’s Disease Growth Rates,” Frontiers in Aging Neuroscience, frontiersin.org. Annual U.S. economic burden already tops USD 52 billion, prompting payer emphasis on early intervention to curb long-term disability costs.

Growing Awareness & Early Diagnosis Initiatives

AI-enabled blood assays can predict disease onset seven years before overt symptoms, allowing enrollment into neuroprotective trials earlier than ever. Complementary smartwatch analytics on 100,000 participants validated motion-pattern biomarkers that flag prodromal cases. Thailand’s nationwide digital screening illustrates how low-cost tools enlarge detection in middle-income settings. Earlier diagnosis increases the addressable base for pipeline disease-modifying products.

Expanding Reimbursement & Insurance Coverage

Formulary wins boosted CREXONT coverage from 30% to beyond 50% of U.S. insured lives, underscoring the pull-through effect of broad access. Medicare payment frameworks for deep-brain stimulation have set benchmarks that newer device-based therapies now leverage [2]Lara Boyd, “Medicare Coverage for Deep Brain Stimulation,” PubMed, pubmed.ncbi.nlm.nih.gov. Coding updates for continuous infusions further ease adoption barriers.

Increasing R&D Investment & Continuous Drug Approvals

More than 10% of active global CNS trials now address Parkinson disease, reflecting sustained industry confidence. AbbVie’s USD 8.7 billion acquisition of Cerevel strengthens its dopamine-receptor pipeline. Bayer’s gene-therapy AB-1005 achieved Phase 2 milestones, exemplifying investor appetite for disease-modifying platforms [3]Bayer AG, “Bayer Gene Therapy Program AB-1005,” bayer.com.

Adoption of Long-Acting Continuous Infusion Formulations

Subcutaneous levodopa/carbidopa infusions deliver 2.7 additional hours of “on” time daily versus oral therapy, enhancing functional outcomes. Wearable pumps integrating Bluetooth telemetry permit dose titration by clinicians remotely, improving adherence.

AI-Driven Drug-Repurposing Pipelines Targeting α-Synuclein

University of Cambridge researchers shortened lead-candidate identification ten-fold using machine-learning on α-synuclein aggregation pathways. Such acceleration compresses overall development timelines and bolsters first-in-class potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse events linked to current therapeutics | -0.7% | Global, long-term users most affected | Short term (≤ 2 years) |

| High treatment & R&D costs | -0.5% | Global, amplified in emerging markets | Medium term (2-4 years) |

| Supply-chain constraints for levodopa APIs | -0.3% | Global, China-dependent supply chains | Short term (≤ 2 years) |

| Regulatory uncertainty around disease-modifying claims | -0.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse Events Associated With Current Therapeutics

Chronic levodopa exposure produces motor complications; benserazide regimens show odds ratios of 170.74 for on–off phenomena, markedly higher than carbidopa’s 67.5. Dopamine agonists carry impulse-control risks, and deep-brain stimulation involves surgical morbidity, limiting uptake outside high-resource centers.

High Treatment & R&D Costs

Continuous-infusion regimens can cost USD 119,000 annually, straining payer budgets even in developed economies. Development outlays rise as companies tackle complex biologics and connected devices, pressuring launch pricing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug's Mechanism of Action: Dopamine pathway dominance persists

The Carbidopa–levodopa segment led the Parkinson's disease drugs market with a 35.02% share in 2025, supported by decades of clinical familiarity. Adenosine A2A antagonists, though niche, are the quickest-growing class at 4.10% CAGR. Selective D1/D5 partial agonist tavapadon achieved significant MDS-UPDRS gains in Phase 3, reinforcing appetite for mechanisms that preserve dopaminergic signaling while reducing dyskinesia risk.

Pipeline diversification tempers reliance on dopamine modulation. AI-derived α-synuclein inhibitors and GDNF gene-therapy vectors illustrate a pivot toward disease modification. As these reach commercial stages, the Parkinson disease market size for non-dopaminergic categories is expected to widen, enhancing therapeutic choice and competitive differentiation.

By Route of Administration: Infusion systems challenge oral dominance

Oral formulations comprised 75.05% of Parkinson's disease drugs market share in 2025 owing to convenience and established reimbursement. Subcutaneous pumps, however, are advancing at 4.21% CAGR, propelled by superior pharmacokinetics that sidestep gastric variability.

Transdermal and intranasal alternatives cater to patients with dysphagia or erratic “off” periods. As real-time dose-adjustment platforms mature, the Parkinson disease market size attributable to infusion devices could exceed USD 1.08 billion by 2031, reshaping revenue distribution among manufacturers.

By Distribution Channel: Digital transformation accelerates

Hospital pharmacies retained 59.78% revenue in 2025, reflecting initiation of complex regimens under specialist oversight. Online channels, rising at 4.93% CAGR, benefit from e-prescription uptake and home-delivery preferences among elderly populations. Telehealth ecosystems integrate refill management and adherence analytics, expanding the Parkinson disease industry’s interface with consumer health technology.

Specialty pharmacies manage temperature-sensitive biologics and provide nurse-led counseling for infusion devices, solidifying their role as high-touch partners for manufacturers focused on patient outcomes.

Geography Analysis

North America contributed 44.02% of global value in 2025, leveraging well-funded health systems, comprehensive insurance, and dense movement-disorder specialist networks. Federal initiatives such as the National Plan to End Parkinson’s Act earmark additional research financing, sustaining innovation momentum. Yet rural communities still face longer diagnostic delays due to limited neurologist access.

Asia Pacific ranks as the fastest-growing region at 5.05% CAGR to 2031. China’s case load has soared since 1990, and clinician awareness of non-motor symptoms is improving, although rural treatment gaps persist. Japan’s super-aged demographics spur demand for advanced devices, while India’s expanding middle class boosts volume, albeit constrained by uneven specialist distribution. Regulatory harmonization across ASEAN members trims approval timelines, favoring multinational launches.

Europe enjoys consistent uptake backed by universal insurance, but individual-state reimbursement decisions create variability. Brexit-related customs changes caused occasional levodopa shortages in the United Kingdom, prompting calls for resilient supply strategies. Germany’s 2025 guideline update emphasizes early interdisciplinary management, reinforcing stable demand across drug classes. Latin America and Middle East & Africa display emerging opportunities parallel to rising life expectancy and improving neurologic care infrastructure.

Competitive Landscape

The Parkinson's disease drugs market features moderate fragmentation. Multinationals such as AbbVie, Amneal, and Bayer co-exist with agile biotechs developing gene and cell-based therapies. Strategic alliances fuse pharmaceutical scale with digital-health expertise; wearable-sensor partnerships shorten trial durations by providing continuous objective data. Patent clusters around continuous levodopa infusion and α-synuclein immunotherapies serve as high-entry barriers.

Price competition remains sharp for mature oral levodopa, yet differentiated delivery systems and proprietary biologics shield innovators from generic erosion. Supply-chain vulnerabilities for levodopa APIs, concentrated in a few Chinese producers, have encouraged dual-sourcing and Western onshoring initiatives to protect margins.

Market entrants target white-space areas: disease-modifying agents, combination products that address motor and non-motor domains concurrently, and precision-medicine approaches guided by genetic risk profiling. These niches promise outsized returns for first movers willing to invest in complex clinical validation.

Parkinson's Disease Drugs Industry Leaders

GlaxoSmithKline PLC

Boehringer Ingelheim International GmbH

Newron Pharmaceuticals SPA

F. Hoffmann-La Roche Ltd

AbbVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: MeiraGTx reported an 18-point UPDRS Part 3 gain at 26 weeks in its AAV-GAD bridging study, supporting Phase 3 initiation

- September 2024: Amneal launched CREXONT extended-release carbidopa/levodopa capsules in U.S. pharmacies, coupling immediate-release granules with controlled–release pellets for longer symptom relief.

- September 2024: AbbVie’s Phase 3 TEMPO-1 trial showed tavapadon monotherapy significantly improved combined MDS-UPDRS Parts II-III scores at both 5 mg and 15 mg doses.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Parkinson's disease drugs market as all prescription pharmaceuticals aimed at relieving motor and non-motor symptoms or slowing progression in diagnosed Parkinson's patients, across every mechanism of action and dosage form that reaches retail, hospital, or specialty pharmacies worldwide.

Scope exclusions include pipeline candidates without marketing approval and device-based interventions (deep-brain stimulators, infusion pumps) that are excluded.

Segmentation Overview

- By Drug's Mechanism of Action

- Dopamine Agonists

- Anticholinergics

- MAO-B Inhibitors

- Amantadine

- Carbidopa-levodopa

- Adenosine A2A Antagonists

- Other Mechanisms of Action

- By Route of Administration

- Oral

- Transdermal

- Subcutaneous

- Infusion

- Intranasal

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview neurologists, hospital pharmacy buyers, payor policy advisors, and manufacturing experts across North America, Europe, Asia-Pacific, and Latin America. These conversations validate prevalence inputs, dosage-day adherence, price corridors, and likely uptake of long-acting infusions that secondary data alone cannot capture.

Desk Research

We start by mapping the treated patient pool and therapy mix through publicly available datasets such as the World Health Organization morbidity files, UN Population Prospects, FDA Orange Book approvals, OECD Health Statistics, and European Medicines Agency safety updates. Trade associations like the Parkinson's Foundation and country-level neurology societies enrich incidence trends, while company filings and investor decks clarify brand life-cycle pricing. Paid databases, including D&B Hoovers for corporate revenue splits, Dow Jones Factiva for regulatory news flow, and Questel for patent expiry timelines, help our analysts cross-check source signals and spot discontinuities before numbers feed the model. The sources cited here are illustrative; many others underpin data gathering, validation, and clarification.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build anchors market value, followed by selective bottom-up checks using sampled average selling price times volume from distributor audits. Key variables, like diagnosed prevalence, treatment penetration, annual drug spend per patient, generic erosion rates, launch timelines of adenosine A2A antagonists, and reimbursement expansion milestones, drive the multivariate regression forecast to 2030. Gaps in bottom-up estimates are bridged through sensitivity ranges agreed with interviewed experts.

Data Validation & Update Cycle

Outputs undergo variance and anomaly checks, then a multi-step peer review before sign-off. We refresh models annually and trigger interim updates whenever material events, such as major approvals, safety withdrawals, or guideline shifts, alter baseline assumptions.

Why Mordor's Parkinson's Disease Drugs Baseline Commands Confidence

Published estimates frequently differ because firms choose dissimilar patient definitions, geography mixes, and price references, which can push totals in opposite directions. By aligning scope strictly to approved drugs and by updating inputs at least yearly, our baseline minimizes distortion for decision-makers.

Key gaps emerge when other publishers bundle surgical devices, assume constant list prices, rely on static prevalence rates, or extend forecast horizons without mid-course refreshes. Mordor's disciplined variable selection and regular recalibration curb these pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.76 B (2025) | Mordor Intelligence | - |

| USD 5.93 B (2025) | Global Consultancy A | Includes device-based therapies and applies list prices without discounting |

| USD 6.59 B (2024) | Industry Association B | Counts pipeline drugs under compassionate use and uses single prevalence source |

Differences highlight that credible sizing rests on transparent scope, multi-source validation, and disciplined update cadence. These are principles Mordor Intelligence applies so clients can rely on a balanced, reproducible baseline.

Key Questions Answered in the Report

How big is the Parkinson's Disease Drugs Market?

The Parkinson's Disease Drugs Market size is expected to reach USD 5.96 billion in 2026 and grow at a CAGR of 3.42% to reach USD 7.05 billion by 2031.

Which therapy class holds the largest share?

Carbidopa–levodopa combinations lead with 35.02% share in 2025.

Who are the key players in Parkinson's Disease Drugs Market?

GlaxoSmithKline PLC, Boehringer Ingelheim International GmbH, Newron Pharmaceuticals SPA, F. Hoffmann-La Roche Ltd and AbbVie Inc. are the major companies operating in the Global Parkinson's Disease Drugs Market.

Which is the fastest growing region in Parkinson's Disease Drugs Market?

Asia Pacific is the fastest-growing region, registering a 5.05% CAGR through 2031.

Which region has the biggest share in Parkinson's Disease Drugs Market?

In 2025, the North America accounts for the largest market share in Parkinson's Disease Drugs Market.

Page last updated on: