Migraine Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.02 Billion |

| Market Size (2031) | USD 9.74 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

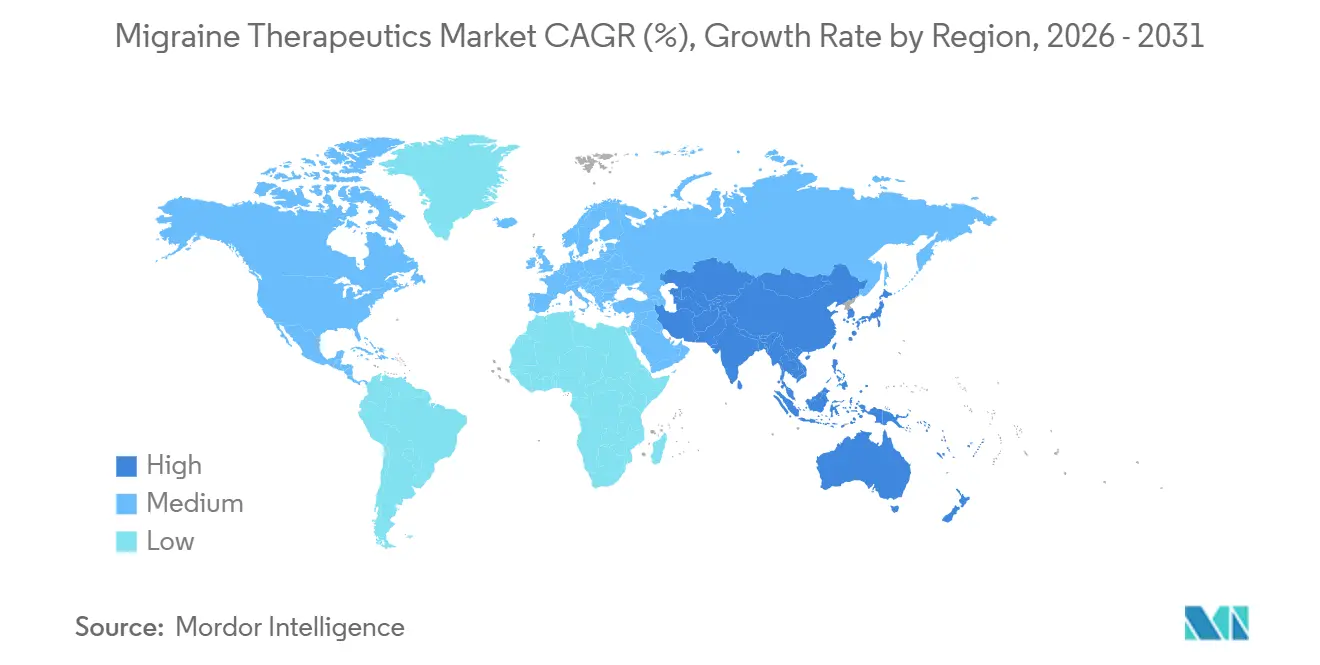

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

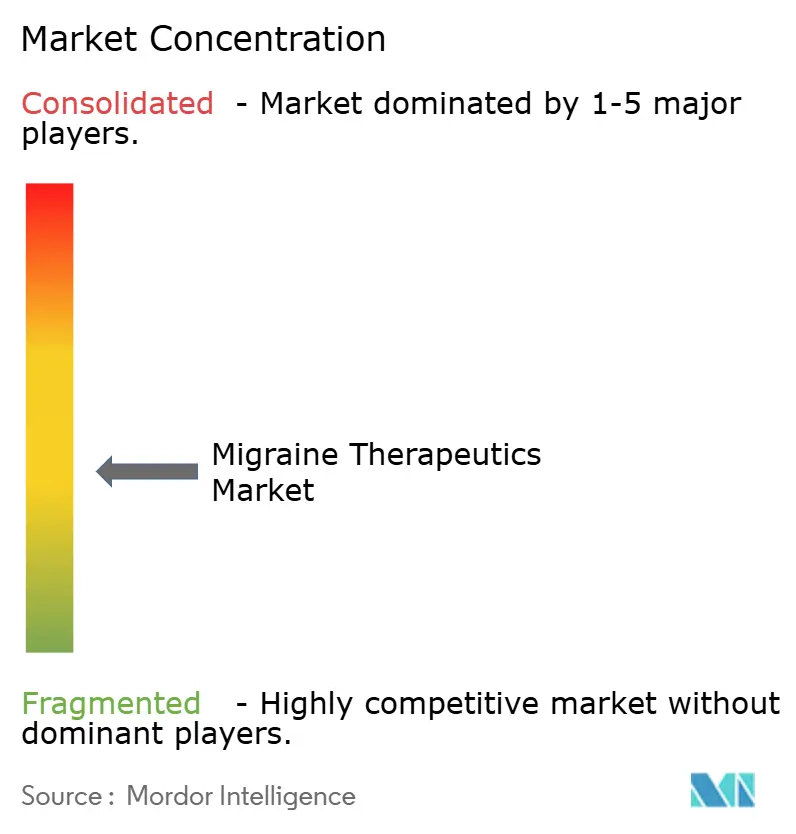

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Migraine Therapeutics Market Analysis by Mordor Intelligence

The migraine therapeutics market size expanded from USD 6.58 billion in 2025 to USD 7.02 billion in 2026 and is projected to reach USD 9.74 billion by 2031, advancing at a 6.75% CAGR over 2026-2031. Rising uptake of calcitonin gene-related peptide (CGRP) antibodies, fast-acting oral gepants, and intranasal zavegepant sprays accelerates the migraine therapeutics market, while triptans, NSAIDs, and ergot derivatives continue to anchor acute care portfolios. Manufacturers prioritize real-world adherence evidence, pediatric label extensions, and telehealth partnerships as differentiators, given that payers increasingly demand economic outcomes rather than head-to-head efficacy trials. Teleneurology bridges diagnostic gaps in Asia-Pacific, where up to 90% of migraine patients remained untreated before 2024, and now delivers guideline-concordant preventive prescriptions 22 percentage points more often than episodic emergency-department encounters. Intranasal delivery systems such as POD DHE offer sub-15-minute onset for patients who abandon subcutaneous biologics because of injection anxiety, estimated at 30-40% globally.

Key Report Takeaways

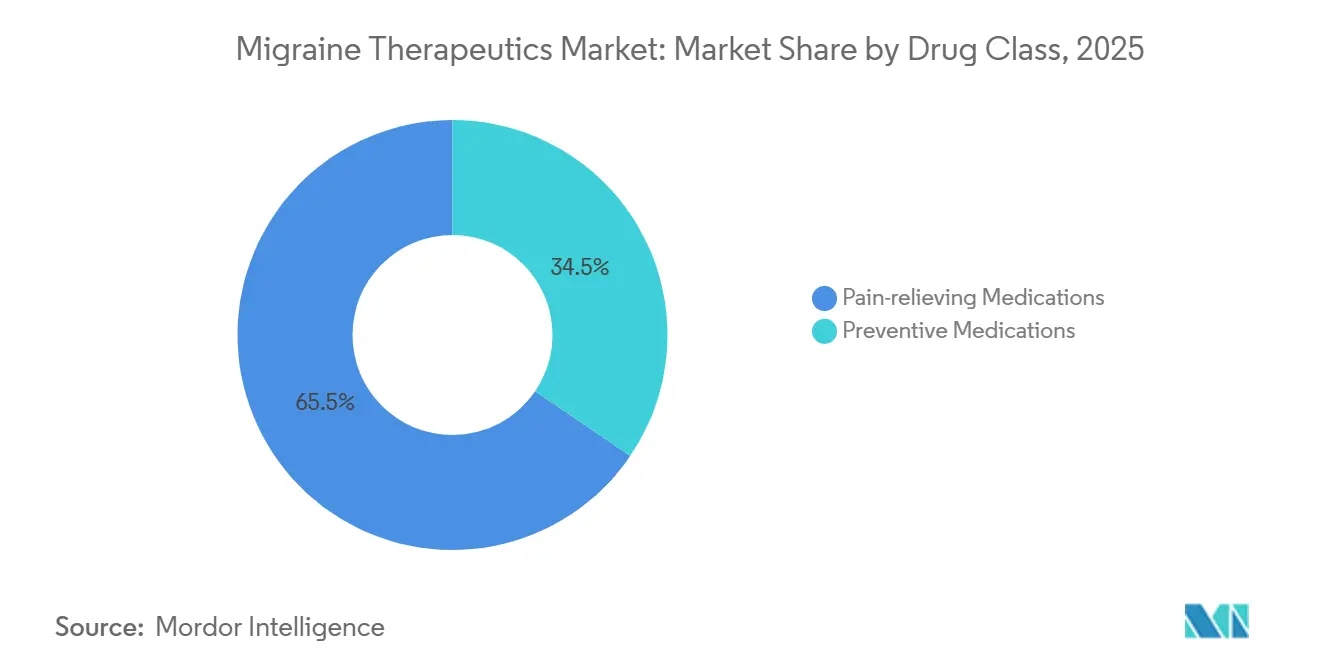

- By drug class, pain-relieving medications retained 65.55% of the migraine therapeutics market share in 2025, whereas preventive medications are forecast to expand at a 9.85% CAGR through 2031.

- By route of administration, intranasal delivery commanded 11.75% CAGR between 2026-2031, surpassing the growth of oral and subcutaneous formats.

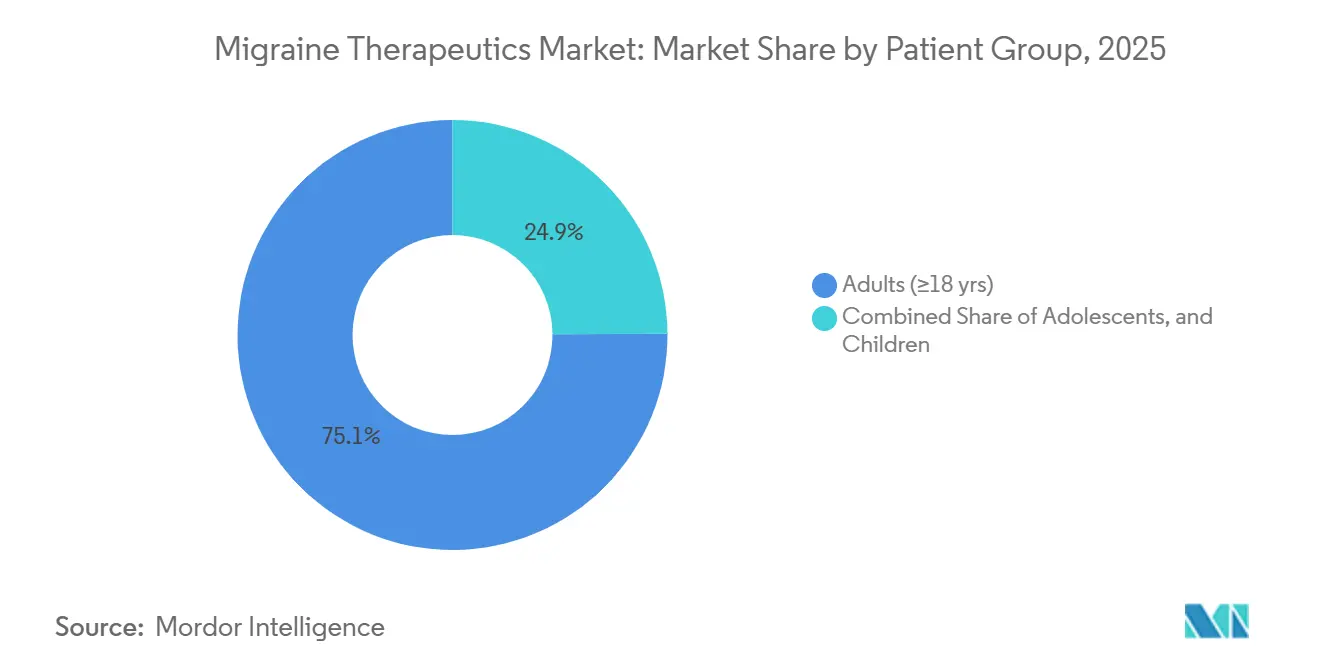

- By patient group, adolescents recorded a 10.82% CAGR from 2026-2031 after U.S. and EU regulators cleared fremanezumab and eptinezumab for ages 6-17.

- By geography, North America accounted for 42.55% revenue in 2025, while Asia-Pacific leads growth at 9.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Migraine Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid penetration of CGRP antibodies into first-line prevention | +2.8% | Global, led by North America & Western Europe | Medium term (2-4 years) |

| Oral gepants closing the "triptan-non-responder" gap | +1.9% | North America, Europe, Japan | Short term (≤2 years) |

| Post-pandemic telehealth adoption accelerates accurate diagnosis & Rx | +1.2% | Global, strongest in APAC & Latin America | Short term (≤2 years) |

| Favorable reimbursement in EU for preventive biologics | +0.9% | Western Europe (UK, France, Germany, Spain, Italy) | Medium term (2-4 years) |

| Devices enabling upper-nasal or POD DHE delivery | +0.7% | North America & Europe, early adoption in urban APAC | Medium term (2-4 years) |

| Employer-funded migraine-care programmes in Asia-Pacific | +0.4% | APAC core (Japan, China, Singapore), spill-over to India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of CGRP Antibodies Into First-Line Prevention

The American College of Physicians allowed CGRP antibodies after failure of a single preventive in its 2025 guideline, trimming median time to biologic from 18 months to 5.7 months for commercially insured U.S. adults. Real-world Danish registry tracking shows 52% 12-month adherence for rimegepant compared with 31% for topiramate, largely because gepants avoid cognitive side effects and weight gain. Eptinezumab’s quarterly infusion schedule attracts patients intolerant of monthly injections, capturing 18% U.S. biologic share within two years of launch and broadening into pediatrics after October 2024 approval for ages 6-17. Payers accept higher drug costs as emergency-department admissions fall 53% and inpatient stays drop 41% among chronic migraine patients treated with CGRP therapy, delivering USD 4,200 net savings per member annually. Meta-analysis positions erenumab and fremanezumab as superior to flunarizine or valproate by reducing monthly migraine days by 2.4-3.1 versus 1.6-2.0, fueling formulary prioritization.

Oral Gepants Closing the “Triptan-Non-Responder” Gap

Roughly 30-40% of migraine sufferers gain little benefit from triptans because of inadequate efficacy or cardiovascular contraindications, creating headroom for oral gepants that block CGRP receptors without vasoconstriction. The HeAD-US real-world study in 1,856 patients showed similar two-hour pain freedom between gepants and triptans (about 21%) but eight-point higher 24-hour pain relief for gepants, lowering risk of medication overuse. Atogepant became the first oral daily CGRP preventive for chronic migraine in December 2024, offering needle-free convenience that resonates with rural patients lacking refrigeration access. Zavegepant nasal spray delivers pain freedom in 24% within two hours and onset inside 15 minutes, bridging the speed gap between tablets and injections. Rimegepant’s dual acute-plus-preventive label simplifies regimens for episodic patients, improving adherence when attack frequency fluctuates.

Post-Pandemic Telehealth Adoption Accelerates Accurate Diagnosis & Rx

Neurology teleconsultations soared 340% between 2019-2023 and stabilized 220% above baseline through 2025, driven by specialist shortages and patient preference for at-home care. Italian registry evidence found virtual visits delivered guideline-correct preventive therapy in 68% of cases versus 46% for emergency departments, thanks to structured diaries and phenotype categorization. China leaned on policy to reimburse remote neurology in 2024, unlocking access for 180 million migraine patients who seldom saw specialists beforehand. Tele-prescribing of CGRP therapies trims treatment initiation time by 23 days compared with brick-and-mortar pathways, as integrated pharmacy services expedite prior authorization. Spanish data indicate adherence improves 19 points under tele-follow-up, reflecting more frequent dosage optimization touchpoints.

Favorable Reimbursement in EU for Preventive Biologics

NICE endorsed atogepant (TA973), eptinezumab (TA871), and erenumab (TA682) between 2021-2024 for adults with ≥4 migraine days monthly after two preventive failures, harmonizing payer criteria with clinician practice. France reimbursed atogepant in 2024 for patients with ≥8 migraine days per month but rejected rimegepant and all monoclonals, splitting EU demand between oral gepants in France and injectables in Germany and the UK. Germany awarded “considerable additional benefit” to fremanezumab and galcanezumab, enabling list-price premiums and unrestricted access that outpace Spain’s capped regional budgets. Italy negotiated 40-50% confidential discounts, maintaining volume growth without breaching healthcare budgets—a model eyed by Poland and Portugal. The EMA cleared atogepant for adolescents 12-17 in 2024, yet reimbursement lag of 18-24 months continues to temper uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High biologic list prices & step-therapy restrictions | -1.4% | North America & select EU markets (France, Spain, Italy) | Long term (≥4 years) |

| Safety concerns around ditans' driving-impairment label | -0.6% | Global, most acute in North America & Japan | Medium term (2-4 years) |

| Limited paediatric approvals outside US & JP | -0.4% | Europe (ex-UK), APAC (ex-Japan), Latin America, MEA | Medium term (2-4 years) |

| Supply-chain cold-chain gaps in GCC & Africa | -0.3% | GCC, Sub-Saharan Africa, select emerging APAC markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Biologic List Prices & Step-Therapy Restrictions

CGRP monoclonal antibodies list at USD 8,100-9,400 annually in the U.S., prompting step-therapy in 72% of commercial and 89% of Medicaid plans. Step protocols postpone CGRP use by 14.3 months and correspond with 38% higher emergency visits, adding USD 11,200 avoidable costs that eclipse the drug price. France assigned ASMR V (“no added benefit”) to monoclonals, denying reimbursement and steering neurologists to atogepant or off-label Botox. Absence of biosimilar CGRP antibodies before 2029-2031 preserves price rigidity, ensuring payer resistance will persist beyond the forecast window[1]European Medicines Agency, “Reyvow (lasmiditan) Product Information,” ema.europa.eu .

Safety Concerns Around Ditans’ Driving-Impairment Label

Lasmiditan requires an eight-hour driving restriction because dizziness affects 29.2% of users, limiting uptake to 12% of eligible U.S. adults who can avoid driving during attacks. Korean real-world data show 22% discontinuation within three months, almost double gepant discontinuation, because of dizziness and fatigue. European and Japanese regulators imposed similar driving cautions, further narrowing the addressable pool to home-based patients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Preventive Biologics Reshape Treatment Algorithms

Pain-relieving medications retained 65.55% of migraine therapeutics market share in 2025, led by triptans and NSAIDs, whereas preventive agents are forecast to grow 9.85% CAGR through 2031, increasing their slice of migraine therapeutics market size. Triptans stay dominant because of generic prices and prescriber familiarity, yet oral gepants capture up to 30-40% of triptan-non-responders, shrinking triptan volumes modestly over the period. Ditans remain niche as their driving label curbs weekday use. CGRP monoclonal antibodies and oral gepants propel preventive uptake after guidelines moved them to second-line status. Botulinum toxin A anchors chronic migraine prevention with long-standing efficacy, although atogepant’s chronic label now challenges its near-monopoly. Anticonvulsants and beta-blockers lose ground because of poor tolerability, evidenced by 28-35% 12-month persistence, fueling migration to CGRP options. Meta-analysis shows erenumab and fremanezumab lower monthly migraine days by 2.4-3.1 versus 1.6-2.0 for flunarizine, justifying payer preference for biologics despite cost premium. France’s refusal to fund monoclonals but coverage of atogepant illustrates divergent European formularies that influence brand strategy.

Shifts within migraine therapeutics market size mirror clinical innovation tempo. Quarterly eptinezumab infusions entice patients unwilling to self-inject monthly. Oral gepants such as atogepant appeal to chronic patients seeking daily, needle-free dosing. Rimegepant offers dual acute-plus-preventive versatility, easing pill burden for episodic sufferers. Ditans await label refinements to lift mobility restrictions. Ergot alkaloids slide because of vasoconstrictive risk. As biosimilars are unlikely before 2030, originators keep pricing power, while generic triptan suppliers defend share on volume and price.

By Route of Administration: Intranasal Delivery Gains Momentum

Oral therapies commanded 64.53% of migraine therapeutics market share in 2025; nevertheless, intranasal products are forecast to outpace all routes at 11.75% CAGR through 2031, lifting their slice of migraine therapeutics market size. Zavegepant spray secures 24% 2-hour pain freedom and sub-15-minute onset without injections, appealing to patients who abandon subcutaneous biologics over needle anxiety[2]U.S. FDA, “Zavzpret (zavegepant) Prescribing Information,” fda.gov. Impel’s POD DHE technology achieves 73.3% 2-hour pain freedom and pharmacokinetics resembling IV delivery, supplying hospital-level efficacy at home. Subcutaneous autoinjectors dominate preventive biologics but face adherence drag owing to injection-site reactions reported by 38% of users. Quarterly eptinezumab IV infusions offer less-frequent dosing yet require clinic visits, limiting uptake among rural patients. Oral gepants expand the oral segment further, particularly after atogepant’s chronic label. Transdermal patches and microneedle arrays promise discreet workplace administration for sumatriptan and other actives. Cold-chain deficits in GCC and Africa complicate biologic distribution, nudging prescribers toward ambient-stable oral and intranasal options.

Although oral remains the largest share, intranasal momentum reflects unmet need for rapid-onset, needle-free acute relief. Real-world audits show 30-40% of patients discontinue injectables within a year, and 40-50% develop gastroparesis during moderate attacks that slows tablet absorption, both factors that intranasal delivery directly addresses. Regulatory approvals for zavegepant in 2023 and growing POD device familiarity suggest sustained double-digit growth for nasal formats.

By Patient Group: Pediatric Approvals Unlock Adolescent Segment

Adults ≥ 18 years controlled 75.15% of migraine therapeutics market share in 2025, yet adolescents 12-17 are projected to grow at a 10.82% CAGR through 2031, lifting their weight in migraine therapeutics market size. Teva’s fremanezumab won the first pediatric CGRP approval in April 2024, quickly followed by Lundbeck’s eptinezumab in October 2024, opening a historically underserved cohort where off-label usage dominated. AbbVie’s atogepant read-outs expected late 2026 signal further adolescent competition. EMA’s clearance of atogepant for EU adolescents in 2024 enlarges the market by 12 million potential patients, although reimbursement lags will slow monetization. Children under 12 remain largely unserved, leaving scope for future label extensions as safety databases mature.

Adolescent prevalence spikes during puberty, yet diagnosis trails adults by 40% because headache symptoms overlap with tension-type disorders and few pediatric neurologists practice outside urban hubs. Telehealth reduces wait times and broadens subspecialty reach, accelerating earlier preventive intervention. Generic triptans still dominate acute care in youth, but gepants gain share among cardiovascular-contraindicated or refractory cases. As school schedules magnify the burden of frequent attacks, quarterly IV eptinezumab and monthly subcutaneous fremanezumab attract parents seeking convenient regimens, driving robust double-digit pediatric growth.

Geography Analysis

North America secured 42.55% of 2025 revenue thanks to high diagnosis rates, broad commercial coverage for CGRP biologics, and dense specialty-clinic networks. Yet step-therapy adds 14.3-month delays and 38% more emergency visits, undercutting optimal outcomes. Canada’s fragmented provincial formularies cause inconsistent access; Ontario funds biologics after four migraine days monthly, while Quebec restricts to chronic cases. Mexico’s private insurers reimburse CGRP agents for urban elites, but national coverage gaps leave most reliant on triptans.

Europe presents a split landscape. The UK funds atogepant, erenumab, and eptinezumab after two preventive failures, aligning with clinical norms. Germany’s positive “additional benefit” rulings give broad reimbursement, whereas Spain’s spending caps enforce mid-year pauses. France funds only atogepant among CGRP agents, channeling demand to oral therapy and Botox. Italy’s steep discounts keep biologic budgets manageable and volumes rising, offering a blueprint for other cost-sensitive EU states.

Asia-Pacific leads growth at 9.72% CAGR. China’s 2024 telemedicine reimbursement adds 180 million potential patients who previously lacked specialist care[3]OECD, “Health at a Glance: Asia/Pacific 2024,” oecd.org. India awaits its first CGRP approvals; until then, generic triptans and anticonvulsants dominate. Australia reimburses erenumab and fremanezumab for chronic migraine but not episodic disease, capturing the sickest cohort. South Korea listed rimegepant in 2024, the region’s first reimbursed oral gepant, catalyzing adoption momentum. Middle East and Africa confront 4-6-week biologic distribution delays because of cold-chain limitations, sustaining dominance of oral and intranasal drugs. South America’s growth focuses on Brazil and Argentina, where private insurance covers CGRP biologics, whereas public systems remain price-constrained.

Competitive Landscape

The migraine therapeutics market features moderate concentration: the five largest companies—AbbVie, Amgen, Eli Lilly, Pfizer, and Teva—accounted for a significant share of revenue in 2025. AbbVie leverages Botox plus atogepant, balancing injectable and oral franchises. Amgen’s Aimovig pioneered monoclonals but now faces share dilution from Lilly’s Emgality, Teva’s Ajovy, and Lundbeck’s Vyepti, each carving niches via dosing frequency or pediatric expansion. Generic firms Teva, Viatris, and Sun Pharma dominate triptan volumes, defending their turf as gepants erode non-responder pools.

Strategic focus shifts to real-world data generation. Danish registry findings showing higher rimegepant adherence allow manufacturers to differentiate without costly head-to-head trials. Pediatric approvals extend patent life and tap underserved segments, while geographic diversification adapts to reimbursement heterogeneity. Impel’s POD DHE represents an innovative entrant targeting rapid nasal rescue for post-triptan failure. Neuromodulation devices (Cefaly, Nerivio, gammaCore) occupy adjunctive niches but face reimbursement hurdles. Absent biosimilars postpone price erosion, preserving brand margins through 2031.

Migraine Therapeutics Industry Leaders

-

AbbVie Inc.

-

Amgen Inc.

-

Pfizer Inc.

-

Teva Pharmaceutical Industries Ltd.

-

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Amneal launched Brekiya, the first ready-to-use dihydroergotamine autoinjector for acute migraine and cluster headache in U.S. adults.

- September 2025: Lundbeck presented new long-term Vyepti data demonstrating sustained preventive effectiveness in severely impacted patients.

Global Migraine Therapeutics Market Report Scope

As per the scope of the report, migraine is a complex neurological condition characterized by frequent headaches that can last from 4 to 72 hours. The pain is often unilateral and pulsating in nature, which can often be worsened by physical activity. In most cases, migraine is associated with symptoms such as photophobia, phonophobia, osmophobia, nausea, vomiting, loss of appetite, and sometimes sensory disturbances.

The segmentation for the migraine therapeutics market is categorized by drug class, route of administration, patient group, and geography. By drug class, it includes pain relief medications such as analgesics, triptans, ergot alkaloids, ditans, and NSAIDs, along with preventive medications like blood pressure lowering agents, anticonvulsants, calcitonin gene-related peptide (CGRP) antagonists, botulinum toxin A, and antidepressants. By route of administration, the market is segmented into oral, subcutaneous injection, intranasal, intravenous, and transdermal/other novel methods. By patient group, it is divided into adults (18+ years), adolescents (12-17 years), and children (<12 years). By geography, the market covers North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Pain-relieving Medications | Analgesics |

| Triptans | |

| Ergot Alkaloids | |

| Ditans | |

| NSAIDs | |

| Preventive Medications | Blood-pressure-lowering Agents |

| Anticonvulsants | |

| Calcitonin Gene-related Peptide (CGRP) Antagonists | |

| Botulinum Toxin A | |

| Antidepressants |

| Oral |

| Subcutaneous Injection |

| Intranasal |

| Intravenous |

| Transdermal / Other Novel |

| Adults (Greater Than 18 yrs) |

| Adolescents (12-17 yrs) |

| Children (Less than 12 yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Pain-relieving Medications | Analgesics |

| Triptans | ||

| Ergot Alkaloids | ||

| Ditans | ||

| NSAIDs | ||

| Preventive Medications | Blood-pressure-lowering Agents | |

| Anticonvulsants | ||

| Calcitonin Gene-related Peptide (CGRP) Antagonists | ||

| Botulinum Toxin A | ||

| Antidepressants | ||

| By Route of Administration | Oral | |

| Subcutaneous Injection | ||

| Intranasal | ||

| Intravenous | ||

| Transdermal / Other Novel | ||

| By Patient Group | Adults (Greater Than 18 yrs) | |

| Adolescents (12-17 yrs) | ||

| Children (Less than 12 yrs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the migraine therapeutics market in 2031?

The migraine therapeutics market is forecast to reach USD 9.74 billion by 2031.

How fast will preventive medications grow compared with acute treatments?

Preventive medications are expected to expand at a 9.85% CAGR through 2031, outpacing the overall 6.75% CAGR.

Which region will register the quickest growth in demand?

Asia-Pacific is projected to advance at 9.72% CAGR between 2026-2031, the fastest among all regions.

Which delivery route is gaining popularity for rapid pain relief?

Intranasal formulations, led by zavegepant and POD DHE devices, are growing at 11.75% CAGR thanks to sub-15-minute onset.

Why are CGRP antibodies penetrating earlier therapy lines?

Updated guidelines allow their use after failure of one preventive, shortening time-to-biologic and leveraging superior real-world adherence.

What limits widespread adoption of lasmiditan?

An eight-hour post-dose driving restriction and high dizziness incidence confine its use to situations where patients can avoid vehicle operation.

Page last updated on: