Stroke Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

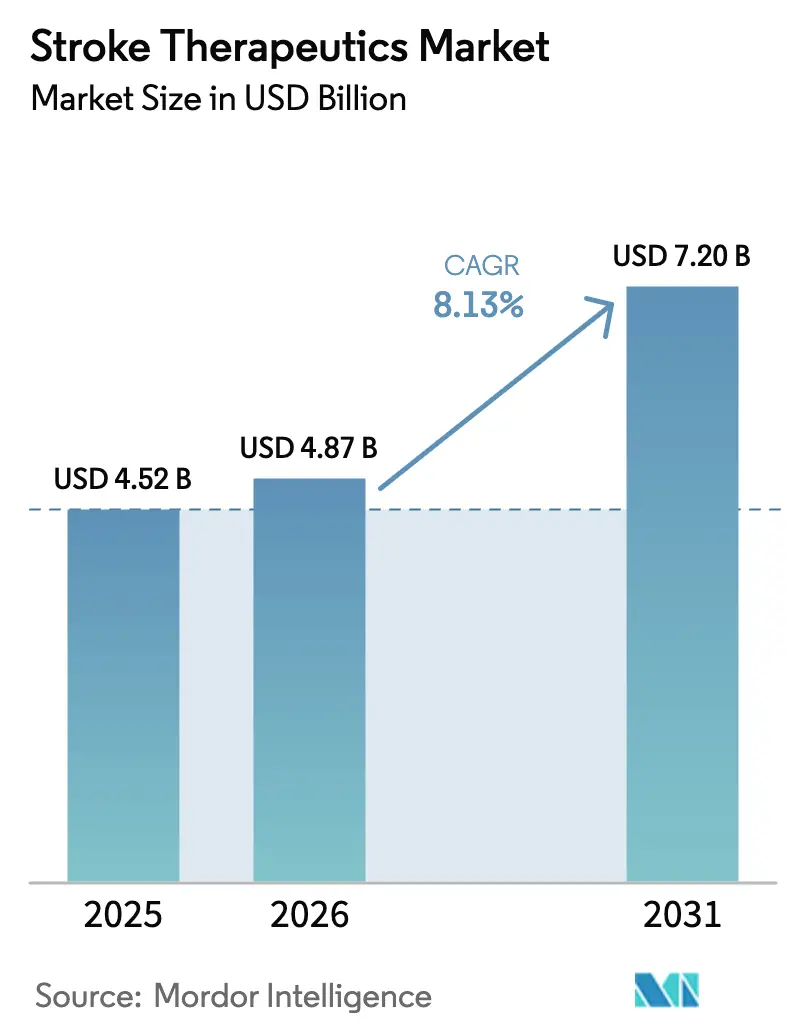

| Market Size (2026) | USD 4.87 Billion |

| Market Size (2031) | USD 7.20 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

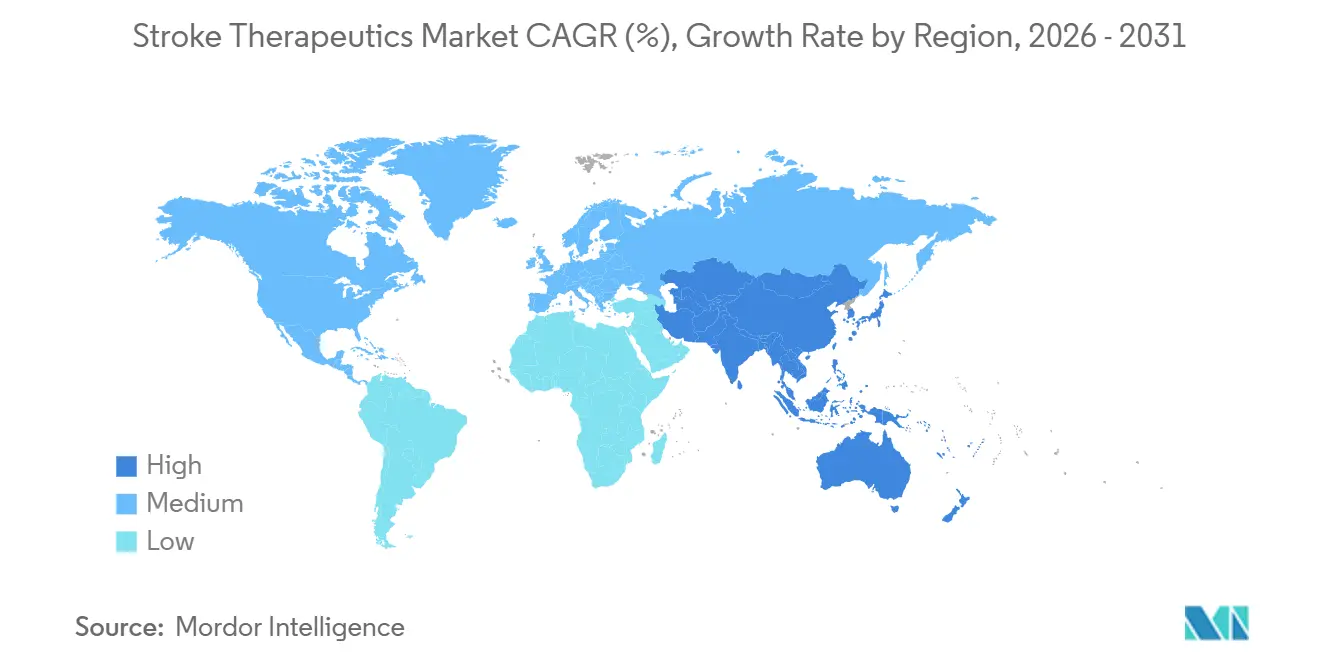

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stroke Therapeutics Market Analysis by Mordor Intelligence

The stroke therapeutics market size is estimated to reach USD 4.87 billion in 2026, and is projected to climb to USD 7.20 billion by 2031, at a CAGR of 8.13% during the forecast period (2026-2031). Demographic aging, rapid guideline shifts that tighten blood-pressure targets, and technology-enabled hyper-acute triage are coalescing to keep the stroke therapeutics market on a steady growth path. The robust adoption of direct oral anticoagulants supports steady revenue growth, even as generic erosion reshapes the older antiplatelet categories. Meanwhile, AI-supported imaging platforms, gene-based neuroprotective programs, and mobile stroke units are expanding the treatment window, increasing the eligible patient pool, and driving demand across the stroke therapeutics market. Continued reimbursement alignment for thrombolytic agents, coupled with productivity pressures from the USD 56.5 billion annual U.S. stroke cost burden, further strengthens the economic rationale for advanced pharmacologic options.

Key Report Takeaways

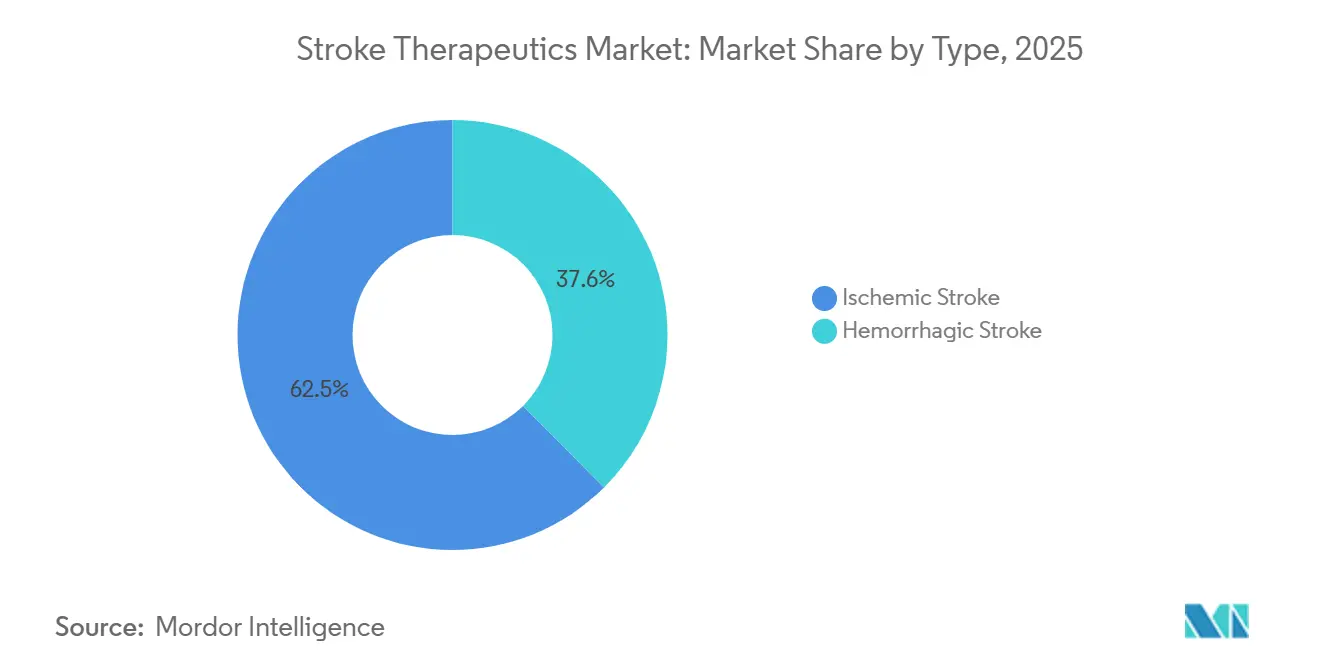

- By type, ischemic stroke led with 62.45% of the stroke therapeutics market share in 2025. Hemorrhagic stroke is forecast to advance at a 10.35% CAGR to 2031.

- By drug class, antithrombotic agents commanded 42.45% share of the stroke therapeutics market size in 2025. Antihypertensive agents are projected to rise at a 10.21% CAGR through 2031.

- By route of administration, oral formulations captured 55.67% revenue in 2025, while intravenous delivery is growing at a 10.65% CAGR.

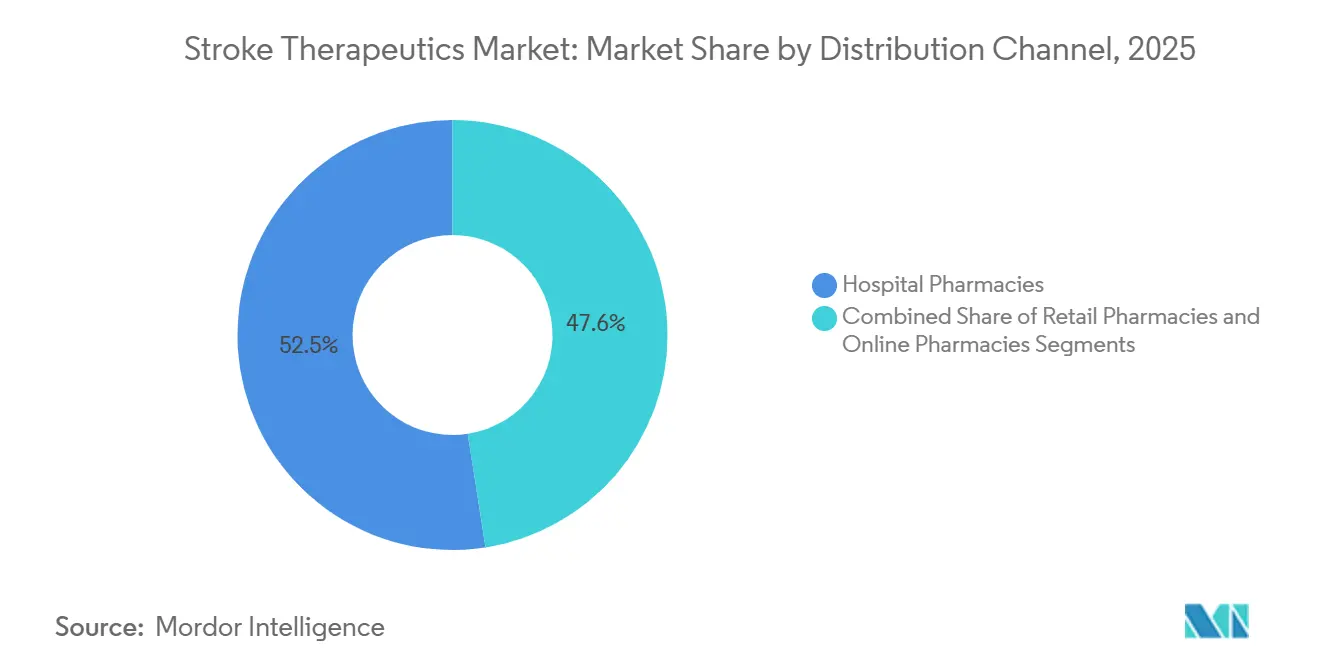

- By distribution channel, hospital pharmacies held 52.45% revenue share in 2025; online pharmacies are expanding at an 11.54% CAGR.

- By end user, hospitals accounted for 55.43% of the stroke therapeutics market size in 2025, whereas ambulatory surgical centers are expected to post an 11.34% CAGR.

- By geography, North America accounted for 41.35% of the revenue share in 2025; the Asia-Pacific region is projected to grow at a 9.54% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stroke Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Stroke in Aging Population | +2.1% | Global, highest in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Increasing Investments in R&D and Advanced Therapies | +1.8% | North America & EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Favorable Reimbursement Policies for Thrombolytic Agents | +1.3% | North America, Western Europe | Short term (≤ 2 years) |

| Emergence of Gene-Based Neuroprotective Platforms | +1.2% | North America & EU, early Japan adoption | Long term (≥ 4 years) |

| AI-Enabled Hyper-Acute Stroke Triage Systems | +1.0% | Global, early gains in U.S., China, Germany | Medium term (2-4 years) |

| Expansion of Mobile Stroke Units in Emerging Markets | +0.9% | Asia-Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Stroke in the Aging Population

Worldwide, the share of people aged ≥60 years will double between 2015 and 2050, and stroke risk doubles every decade after 55[1]World Health Organization, “Ageing and Health,” who.int. In the United States alone, about 795,000 strokes occur yearly, 610,000 of them first-ever events. Co-morbid hypertension, atrial fibrillation, and diabetes magnify demand for preventive anticoagulants and antihypertensives. Japan’s population already skews old, with 29% of the population aged 65 or older in 2024, resulting in high prescription volumes for secondary prevention medicines. The U.S. FDA's fast-track mechanisms are streamlining the development of geriatric-appropriate formulations that recognize the altered pharmacokinetics in older adults.

Increasing Investments in R&D and Advanced Therapies

Biopharmaceutical pipelines list more than 100 active stroke programs, backed by NIH’s USD 218 million stroke research allocation in FY 2024[2]National Institutes of Health, “Estimates of Funding for Various Research, Condition, and Disease Categories (RCDC),” nih.gov. Focus areas range from NMDA antagonists to stem-cell implants, aiming to lengthen or bypass the narrow 4.5-hour thrombolytic window. PhRMA notes that stroke joins Alzheimer’s and Parkinson’s as top neuro priorities, driving capital into cell-based regeneration platforms. Late-stage attrition remains high; however, the commercial upside of a first-in-class neuroprotectant continues to drive strong investor appetite.

Favorable Reimbursement Policies for Thrombolytic Agents

CMS reimburses tissue plasminogen activators under value-based models that reward door-to-needle times under 60 minutes[3]Centers for Medicare & Medicaid Services, “Hospital Inpatient Prospective Payment System,” cms.gov. Payment parity for tenecteplase, now guideline-endorsed as an alternative to alteplase, is accelerating switch momentum. Private payers are increasingly tying reimbursement to functional outcome metrics, prompting hospitals to deploy streamlined imaging and pre-notification protocols that increase thrombolytic utilization.

Emergence of Gene-Based Neuroprotective Platforms

Regenerative Medicine Advanced Therapy designations from the FDA are accelerating the development of cell and gene candidates that promise durable neuroprotection. EMA’s advanced therapy medicinal product pathway offers similar support. Investigational mesenchymal stem cell infusions aim to enhance neurogenesis and mitigate inflammation beyond the hyperacute window. Developers must still confirm long-term functional gains on modified Rankin outcomes, a hurdle that has stymied earlier neuroprotectant hopefuls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent Expiries Accelerating Generic Erosion | -1.4% | Global, pronounced in North America & Europe | Short term (≤ 2 years) |

| High Cost of Novel Biologics | -0.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Limited Cross-Border Cold Chain | -0.6% | Global, critical in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Physician Skepticism Toward DAPT De-Escalation | -0.5% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries Accelerating Generic Erosion

Clopidogrel and multiple direct oral anticoagulants are losing exclusivity, triggering price drops of over 80% within the first year of generics. While generics widen access, they compress revenue, prompting originators to adopt novel mechanisms and fixed-dose combinations. Apixaban’s initial generic entries in 2024 exemplify the looming revenue cliff.

High Cost of Novel Biologics

Cell and gene platforms can exceed USD 500,000 per patient, straining payer budgets. ICER assessments frequently flag affordability concerns, leading to outcomes-based contracts or delayed coverage. In low-income regions, the WHO’s Essential Medicines List still excludes high-priced biologics, resulting in minimal usage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ischemic Dominance Reflects Epidemiologic Reality

Ischemic stroke controlled 62.45% of the stroke therapeutics market in 2025, mirroring its 87% share of global stroke incidence. The stroke therapeutics market size for ischemic interventions is buoyed by widespread alteplase protocols and expanding thrombectomy eligibility. Tenecteplase adoption adds convenience, reducing nursing workload. Secondary prevention relies heavily on dual antiplatelet and direct oral anticoagulant regimens, anchoring recurring revenue.

Hemorrhagic stroke, though smaller, is projected to post a 10.35% CAGR, the fastest within the stroke therapeutics market. Novel reversal agents such as andexanet alfa address anticoagulant-related bleeds, while minimally invasive evacuation devices enhance outcomes. As Asian populations age and hypertension prevalence climbs, absolute hemorrhagic volumes support lucrative regional opportunities.

By Drug Class: Antithrombotics Anchor Market, Antihypertensives Gain Momentum

Antithrombotic agents represented 42.45% of the stroke therapeutics market size in 2025, driven by guideline-mandated lifelong prevention. Direct oral anticoagulants continue to outpace warfarin due to their fixed dosing and the elimination of routine monitoring. However, approaching patent cliffs bring generics that will redistribute value across the stroke therapeutics market.

Antihypertensives are on track for a 10.21% CAGR, reflecting tighter AHA target thresholds below 130/80 mmHg. Combination pills improve adherence and fuel premium pricing. For payers, sustained blood-pressure control offers proven stroke risk reduction, supporting favorable formulary placement.

By Route of Administration: Oral Dominates Chronic Care, IV Serves Acute Needs

Oral agents captured 55.67% revenue in 2025, underpinned by chronic secondary prevention. Nonetheless, intravenous formulations are expanding at a 10.65% CAGR as door-to-needle initiatives drive higher alteplase and tenecteplase penetration. The stroke therapeutics market share for IV lines also benefits from peri-thrombectomy antithrombotic adjuncts administered in the hospital.

By Distribution Channel: Hospital Pharmacies Dominate, Digital Channels Emerge

Hospital pharmacies held 52.45% of 2025 revenue - accreditation programs such as The Joint Commission mandate immediate availability of thrombolytics, ensuring steady institutional demand. Meanwhile, online pharmacies are expected to experience double-digit growth, reflecting post-COVID consumer comfort with mail-order refills and tele-management of chronic diseases.

By End User: Hospitals Anchor Acute Care, Outpatient Centers Rise

Hospitals generated 55.43% of the stroke therapeutics market size in 2025. Comprehensive stroke centers stock reversal agents, neuroprotective candidates, and adjunct anticoagulants. Ambulatory surgical centers, growing at an 11.34% CAGR, benefit from the migration of carotid stenting to outpatient settings, which boosts the per-procedure pharmaceutical pull-through.

Geography Analysis

North America accounted for 41.35% of the revenue in 2025. Regional stroke networks, CMS value-based purchasing, and broad insurance coverage facilitate the uptake of premium drugs. Canada follows similar universal-coverage pathways, albeit with province-specific formularies.

Europe contributes a consistent share, guided by EMA centralized approvals and national health systems that guarantee access to essential stroke drugs. The European Stroke Organisation harmonizes best practices, while individual countries fine-tune reimbursement according to cost-effectiveness dossiers.

The Asia-Pacific region is the fastest-growing, with a 9.54% CAGR. China’s basic medical insurance now lists generic direct oral anticoagulants, widening access. India’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases, and Stroke funds regional hub-and-spoke stroke units, fostering demand for acute thrombolytics. Japan maintains high penetration of premium therapies thanks to ageing demographics and generous reimbursement.

Competitive Landscape

The stroke therapeutics market remains moderately fragmented. Bristol-Myers Squibb and Pfizer’s apixaban franchise remains the leader in the anticoagulant segment but faces generic competition after 2024. Boehringer Ingelheim’s dabigatran pioneered the direct oral anticoagulant era yet now competes on pricing.

Emerging biotechs, such as Athersys and ReNeuron, are advancing cell-based neurorestorative programs in Phase III trials. FDA Breakthrough Therapy and EMA PRIME designations shorten pathways for first movers. Digital health entrants, such as Viz.ai, commercialize algorithmic triage platforms that enhance drug utilization and create partnership opportunities with pharmaceutical companies.

Strategic collaboration remains the dominant competitive theme, with large incumbents licensing new mechanisms, generics preparing for anticoagulant cliff events, and technology vendors integrating diagnostic software with hospital formularies. The market is moderately concentrated, with the top five companies commanding about two-thirds of global revenue. Ongoing venture funding and regulatory support facilitate a steady flow of innovative therapies and digital tools set to reshape the treatment landscape over the next five years.

Stroke Therapeutics Industry Leaders

Boehringer Ingelheim International GmbH

Bristol-Myers Squibb Company

F. Hoffmann La Roche Ltd.

Johnson & Johnson

Pfizer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Genentech, a member of the Roche Group, announced that the FDA has approved TNKase (tenecteplase) for treating acute ischemic stroke in adults. This marks Genentech’s second FDA approval for stroke treatment, following Activase. The approval highlights the company's ongoing commitment to stroke care innovation.

- May 2024: Argenica Therapeutics, a biotechnology firm based in Western Australia, has successfully recruited the initial five patients for its Phase 2 Clinical Trial. The trial focuses on a groundbreaking therapy aimed at minimizing brain tissue damage post-stroke. The neuroprotective agent, ARG-007, was co-developed by the Perron Institute in collaboration with The University of Western Australia.

- February 2024: Aruna Bio launched a Phase I/II trial to assess its cell therapy for ischemic stroke. Preclinical research conducted by Aruna Bio in collaboration with UGA highlights that AB126 provides neuroprotective benefits and also promotes neuroregeneration, with a significant emphasis on inflammation reduction.

Global Stroke Therapeutics Market Report Scope

As per the scope of this report, stroke therapeutics are medical treatments designed to prevent, manage, or recover from strokes by restoring blood flow or protecting brain tissue. They include clot-busting drugs, neuroprotective agents, and rehabilitation therapies.

The Stroke Therapeutics Market is segmented by Type (Ischemic Stroke and Hemorrhagic Stroke), Drug Class (Antithrombotic Agents, Neuroprotective Biologics, Antihypertensive Agents, and Anti-Inflammatory & Antioxidants), Route of Administration (Oral, Intravenous, and Intra-arterial, Subcutaneous/Intramuscular), Distribution Channel (Hospital, Retail, and Online Pharmacies), End-User (Hospitals, Specialty Clinics, ASCs, and Other End Users), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers values (in USD) for the above segments.

| Ischemic Stroke |

| Hemorrhagic Stroke |

| Antithrombotic Agents |

| Neuroprotective Biologics |

| Antihypertensive Agents |

| Anti-Inflammatory & Antioxidants |

| Oral |

| Intravenous |

| Intra-arterial |

| Subcutaneous / Intramuscular |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Type | Ischemic Stroke | |

| Hemorrhagic Stroke | ||

| By Drug Class | Antithrombotic Agents | |

| Neuroprotective Biologics | ||

| Antihypertensive Agents | ||

| Anti-Inflammatory & Antioxidants | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intra-arterial | ||

| Subcutaneous / Intramuscular | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What revenue level does the stroke therapeutics market target by 2031?

The market is forecast to reach USD 7.20 billion by 2031, reflecting an 8.13% CAGR.

Which stroke type currently drives most therapy sales?

Ischemic stroke leads with 62.45% of global revenue thanks to established thrombolytic and secondary prevention regimens.

Which region shows the fastest growth through 2031?

Asia-Pacific is projected to rise at a 9.54% CAGR, propelled by aging demographics and expanding healthcare infrastructure.

Which drug class is expected to outpace overall market growth?

Antihypertensive agents should expand at a 10.21% CAGR as guidelines push intensive blood-pressure control for survivors.

How are AI tools influencing acute stroke treatment uptake?

AI-enabled imaging shortens diagnosis time by about 20 minutes, enlarging the eligible pool for thrombolytics and boosting drug utilization.

What is the main barrier to cell-based stroke therapies?

Stringent cryogenic distribution requirements and high per-patient costs limit access, especially in low- and middle-income countries.

Page last updated on: