Complex Regional Pain Syndrome Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 122.57 Million |

| Market Size (2031) | USD 139.46 Million |

| Growth Rate (2026 - 2031) | 2.62% CAGR |

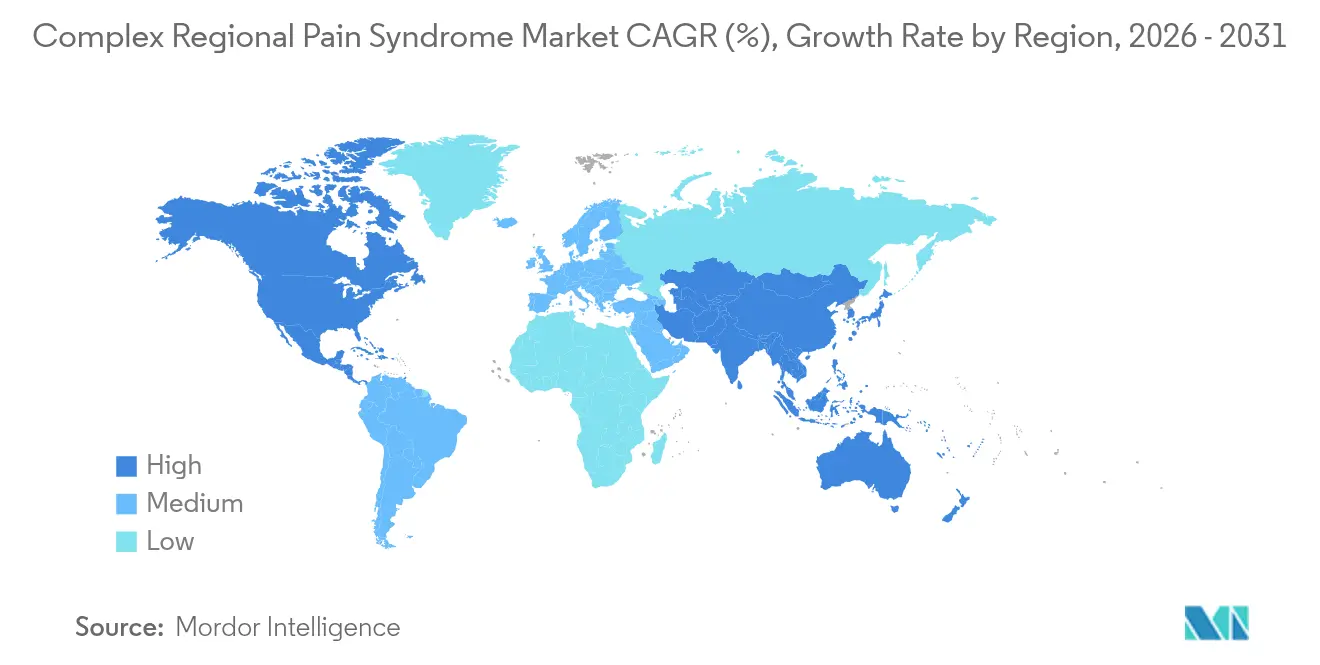

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

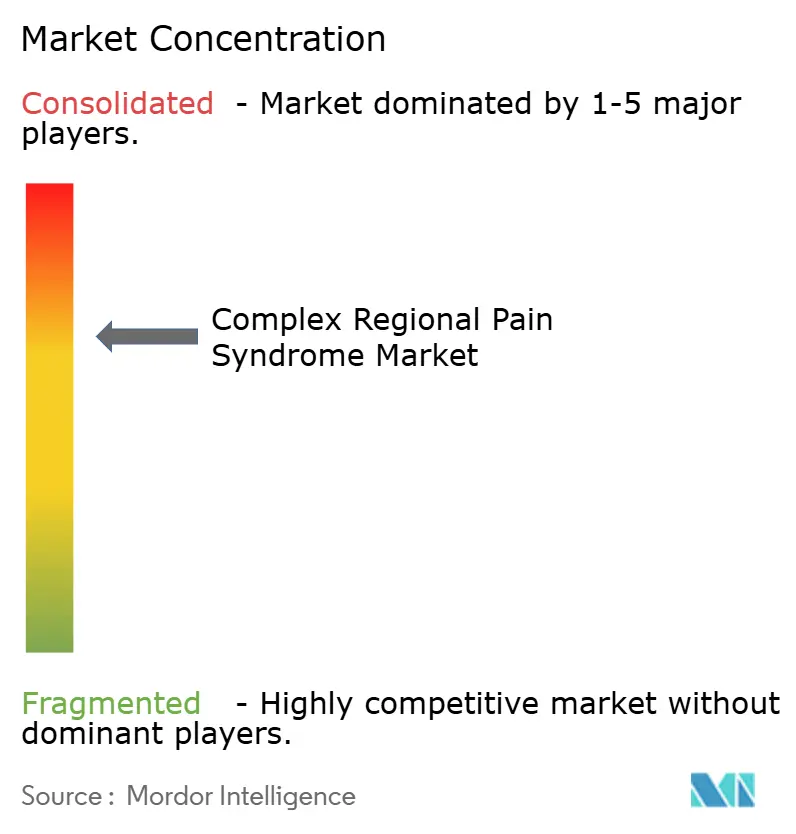

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Complex Regional Pain Syndrome Market Analysis by Mordor Intelligence

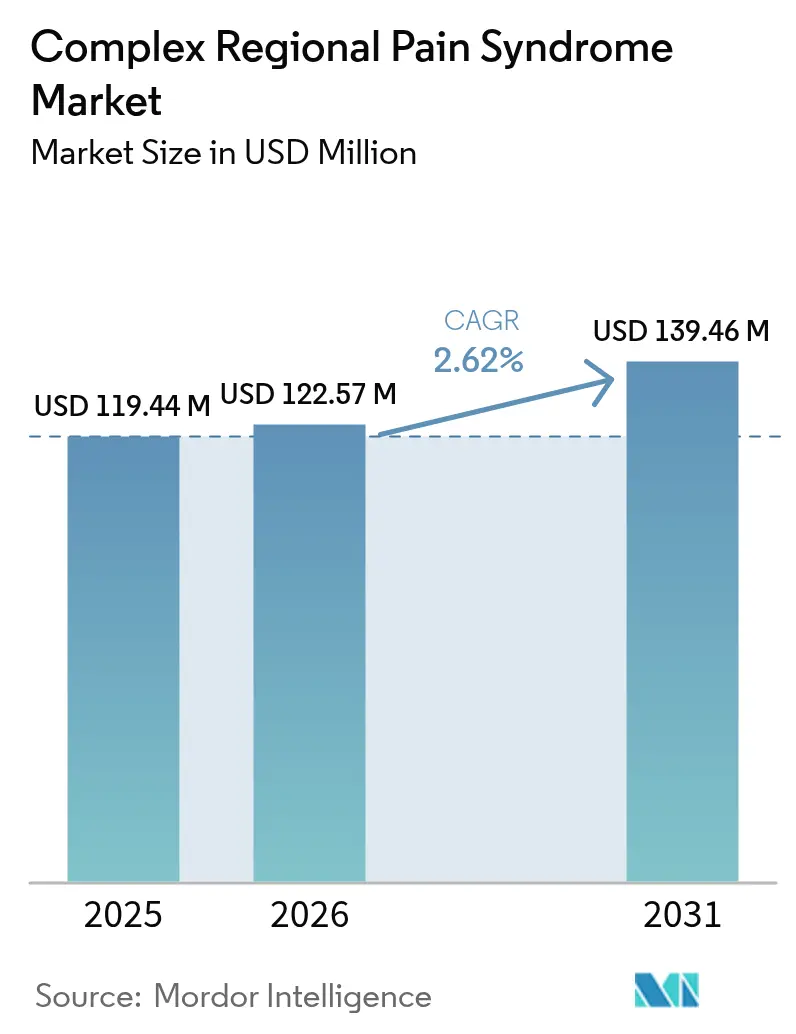

The Complex Regional Pain Syndrome market size is expected to grow from USD 119.44 million in 2025 to USD 122.57 million in 2026 and is forecast to reach USD 139.46 million by 2031 at 2.62% CAGR over 2026-2031.

Demand grows as clinicians confront a rare neuropathic condition that strikes about 200,000 people each year in the United States, yet still offers few disease-specific treatments. Expanding surgical volumes, especially orthopedic procedures with 0.34% CRPS incidence and 0.60% rates after upper-limb surgery, continually add new patients to the Complex Regional Pain Syndrome market [1]Genevieve‐Smith et al., “Neurological research offers 80% recovery in early CRPS,” unisa.edu.au . Breakthrough evidence showing 80% recovery when therapy begins early is shifting clinical objectives from lifelong symptom control toward potential cure and is spurring investment in neuromodulation platforms and mechanism-based drugs. Closed-loop spinal cord stimulators, dorsal root ganglion devices, and first-in-class sodium-channel antagonists now headline product pipelines, while recent reimbursement gains in the United States and Europe lower financial barriers to implantation. Collectively, these factors anchor the medium-term growth outlook even as the Complex Regional Pain Syndrome market remains comparatively small in absolute dollar terms.

Key Report Takeaways

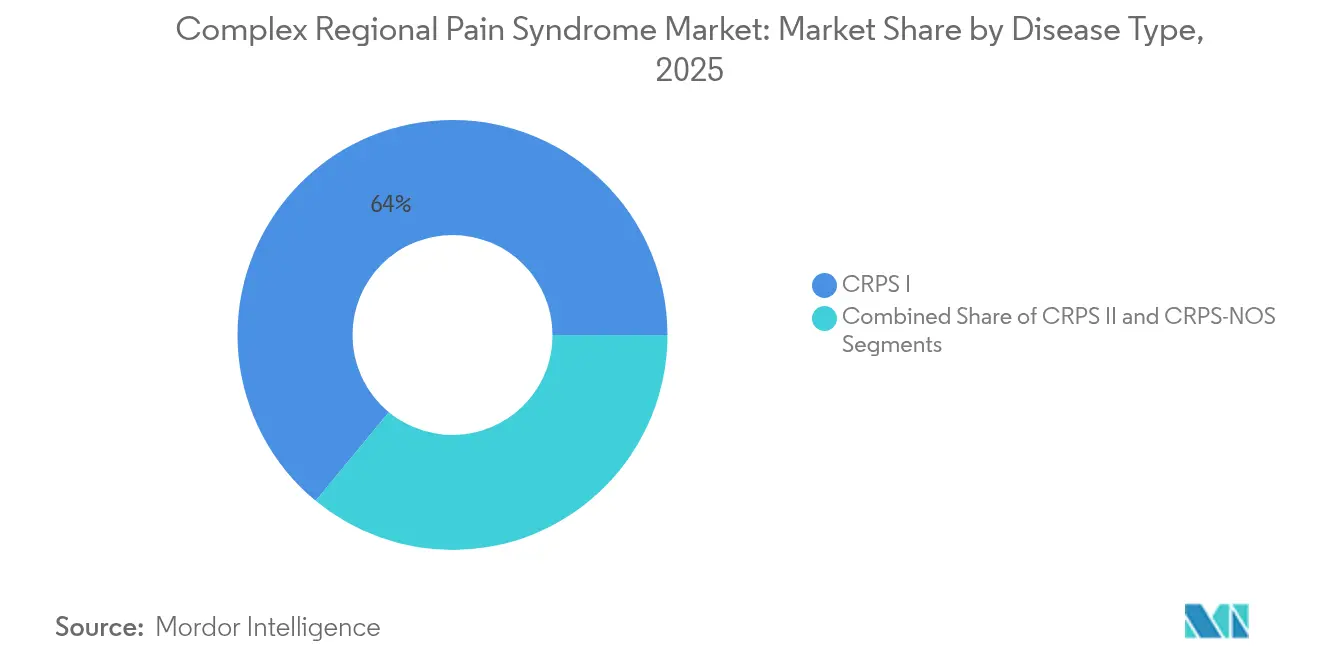

- By disease type, CRPS I led with 64.02% of Complex Regional Pain Syndrome market share in 2025; CRPS II is projected to expand at a 3.32% CAGR through 2031.

- By therapy, drug therapy accounted for 47.35% of the Complex Regional Pain Syndrome market size in 2025, while neuromodulation is advancing at a 3.33% CAGR to 2031.

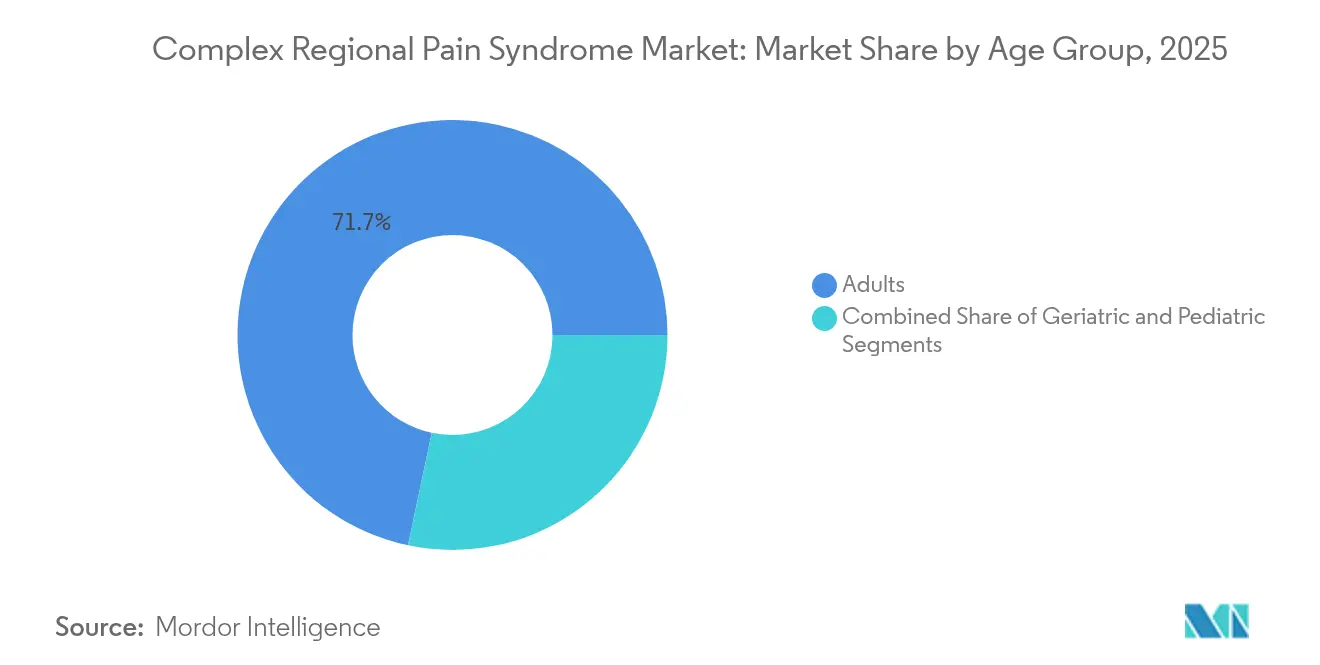

- By age group, adults held 71.68% revenue share in 2025; the geriatric cohort records the fastest 3.41% CAGR to 2031.

- By disease stage, early-stage cases captured 67.12% of the Complex Regional Pain Syndrome market size in 2025 and late-stage cases are increasing at a 3.39% CAGR.

- By region, North America commanded 41.88% share of the Complex Regional Pain Syndrome market in 2025, while Asia-Pacific is forecast to grow at a 3.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Complex Regional Pain Syndrome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence following orthopedic & trauma surgeries | +0.8% | North America, Europe, Global | Medium term (2-4 years) |

| Growing chronic pain population seeking long-term relief | +0.6% | Global developed markets | Long term (≥ 4 years) |

| Expanding adoption of closed-loop & DRG neuromodulation | +0.9% | North America, Europe, APAC | Short term (≤ 2 years) |

| Favorable reimbursement updates for implantable SCS in the US & EU | +0.4% | North America, Europe | Medium term (2-4 years) |

| Auto-immune insights driving IVIG & Mab pipeline activity | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Wearable biosensors enabling objective pain biomarkers | +0.2% | North America, Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Following Orthopedic & Trauma Surgeries

Insurance data covering 85,862 orthopedic procedures documented a 0.34% CRPS rate overall, with upper-limb operations carrying a 0.60% risk and lower-limb surgery 0.20% [2]Kessner K. et al., “Incidence of CRPS after surgery,” journals.lww.com . Distal radius fractures remain a focal concern, registering CRPS-I rates up to 37% in prospective series. Global population aging drives higher fracture and joint-replacement volumes, enlarging the Complex Regional Pain Syndrome market as new cases emerge. Diagnostic delays in pediatrics still range from 4 to 90 days, underscoring unmet clinical education needs. Broader application of Budapest criteria, together with imaging advances, is expected to improve early detection and further expand documented prevalence.

The Growing Chronic Pain Population Seeking Long-Term Relief

Chronic pain affects nearly 30% of US adults and imposes USD 500-600 billion in annual economic costs, intensifying demand for durable, non-opioid solutions. Surveyed Korean patients reported 48.07% unmet rehabilitation needs, emphasizing deficits beyond analgesia, such as memory and weight management support. Cognitive and social burdens heighten interest in mechanism-based treatments that target neuro-immune dysregulation rather than masking symptoms. Biomarker research involving microRNAs and inflammatory mediators paves the way for personalized regimens and underpins wider adoption of precision-guided neuromodulation [3]Burcu Candan, "Current and Evolving Concepts in the Management of Complex Regional Pain Syndrome: A Narrative Review," MDPI, mdpi.com. These shifts align with payer incentives to curb opioid use, reinforcing steady uptake within the Complex Regional Pain Syndrome market.

Expanding Adoption of Closed-Loop & DRG Neuromodulation

Dorsal root ganglion stimulation yields 81.2% responder rates versus 56.7% for conventional spinal cord stimulation in CRPS cohorts. Medtronic’s Inceptiv system, cleared in 2024, adjusts stimulation 50 times per second and cut overstimulation in 93% of users while halving pain for 82%. Nevro’s September 2024 FDA clearance for an AI-driven platform underscores rapid innovation in real-time therapy optimization. Wider clinical familiarity, procedure standardization, and device miniaturization accelerate commercial traction, especially in North America where reimbursement pathways are now clarified. Resulting momentum adds meaningful volume to the Complex Regional Pain Syndrome market despite historically modest unit sales.

Favorable Reimbursement Updates for Implantable SCS in the US & EU

Humana reversed earlier exclusions in 2025 by covering peripheral nerve stimulators under Medicare Advantage, closing a key access gap for older beneficiaries. Centers for Medicare & Medicaid Services already reimburse CRPS-specific solutions such as Abbott’s Proclaim DRG device, lowering average out-of-pocket costs and expanding candidate pools. European schemes provide broader coverage, though device costs of USD 15,000-50,000 still hinder adoption among uninsured populations. As payers refine coverage criteria to emphasize real-world outcomes, neuromodulation developers gain predictable revenue visibility that supports R&D investment, adding structural lift to the Complex Regional Pain Syndrome market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low disease awareness in emerging economies | -0.3% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| High upfront cost of neuromodulation devices & limited payor coverage | -0.5% | Global, emerging markets | Medium term (2-4 years) |

| Regulatory caution over psychedelic-based analgesics | -0.2% | US, EU | Long term (≥ 4 years) |

| Semiconductor & battery supply constraints for next-gen implants | -0.1% | Global, with APAC manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Disease Awareness in Emerging Economies

International clinician surveys cite fragmented care pathways and shortage of pain specialists as root causes of delayed CRPS diagnosis across Europe. Ecuador’s public hospitals exemplify resource scarcity, frequently lacking local anesthetics and palliative medicines because of fiscal constraints. Nordic and German pediatric centers manage only a handful of CRPS cases yearly, with 43% lacking dedicated multidisciplinary teams. Absence of standardized training perpetuates misdiagnosis, allowing symptoms to progress and limiting early-stage intervention. Consequently, latent demand remains sizable yet unrealized in many territories, restraining Complex Regional Pain Syndrome market expansion.

High Upfront Cost of Neuromodulation Devices & Limited Payor Coverage

Uninsured patients face USD 15,000-50,000 price tags for spinal or DRG stimulators, a hurdle magnified in lower-income regions. Economic evaluations confirm long-run cost-effectiveness, but cash-flow barriers slow adoption while public insurers debate budget impact. Coverage for adjunct modalities like Scrambler Therapy varies widely, with many plans reimbursing only a portion of the USD 2,000-5,000 course. Specialized implant programs cluster in tertiary hospitals, forcing travel and additional expense for rural patients. These financial frictions temper near-term growth in the Complex Regional Pain Syndrome market despite evident clinical utility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: CRPS I Dominance Drives Market Foundation

CRPS I accounted for 64.02% of Complex Regional Pain Syndrome market share in 2025, anchored by its higher post-trauma prevalence. Clinic registries show women aged 50-70 represent nearly 70% of new CRPS I diagnoses, reinforcing predictable demand in orthopedics and rehabilitation settings. CRPS II, once termed causalgia, posts the quickest 3.32% CAGR as improved imaging pinpoints nerve injury and eligibility for DRG stimulation expands.

Historically, limited objective diagnostics masked CRPS II incidence, but PET/MRI visualization of Sigma-1 receptors now raises detection accuracy. Breath-analysis “electronic nose” studies demonstrating 81% diagnostic precision further promise earlier subtype confirmation. Personalized protocols based on inflammatory and vasomotor profiles enable mechanism-aligned therapy selection, bolstering future revenue diversity in the Complex Regional Pain Syndrome market.

By Therapy Type: Neuromodulation Disrupts Traditional Drug Dominance

Drug therapy retained 47.35% of Complex Regional Pain Syndrome market size in 2025, yet neuromodulation leads growth at 3.33% CAGR. Common analgesics, including NSAIDs and opioids, show limited CRPS efficacy, prompting physicians to escalate quickly to interventional solutions.

Neuromodulation’s clinical traction stems from strong responder data, such as 81.2% success with DRG devices. Medtronic’s closed-loop Inceptiv and Abbott’s Proclaim systems shape competitive dynamics by offering adaptive or disease-specific programming. The January 2025 FDA nod for suzetrigine introduced the first NaV1.8 inhibitor for acute pain, though its chronic use profile remains under review. Stem-cell protocols funded by a USD 5.5 million NIH grant target neuro-immune modulation and could provide the first disease-modifying option, illustrating the technology breadth now fueling the Complex Regional Pain Syndrome market.

By Age Group: Adult Prevalence Masks Geriatric Growth Opportunity

Adults comprised 71.68% of patients in 2025, driven by workplace injuries and elective surgeries. Hormonal influences and higher rates of certain orthopedic procedures explain female over-representation.

The geriatric segment grows at 3.41% CAGR as aging populations undergo more joint replacements and sustain fragility fractures. Age-related changes in pain perception demand tailored dosing and device programming strategies. Pediatric CRPS remains rarer but responds well to early multidisciplinary care, achieving high remission rates when recognized promptly. Awareness campaigns and Medicare coverage for established stimulators together enlarge the Complex Regional Pain Syndrome market across age brackets.

By Disease Stage: Early Intervention Drives Better Outcomes

Early-stage cases held 67.12% of Complex Regional Pain Syndrome market size in 2025, emphasizing the importance of rapid diagnosis. Corticosteroids and bisphosphonates like neridronate deliver strong early-stage pain control, with 91.4% of patients halving pain after treatment.

Late-stage CRPS advances at 3.39% CAGR, reflecting chronic case accumulation and delayed access in underserved regions. These patients often develop central sensitization that necessitates advanced neuromodulation, ketamine infusions, and psychological support. Biomarker-driven screening seeks to shift the balance toward early-stage capture, which would meaningfully alter utilization patterns in the Complex Regional Pain Syndrome market over the long term.

Geography Analysis

North America led with 41.88% of the Complex Regional Pain Syndrome market in 2025 owing to sophisticated care networks, high surgical volumes, and payer coverage for DRG and spinal stimulation. Recent FDA approvals of AI-enabled systems further enhance therapeutic options. Canada mirrors US practice patterns, leveraging provincial plans to reimburse Abbott’s neuromodulation suite. Mexico remains nascent as infrastructure and specialist density evolve, signaling upside once training and reimbursement mature.

Europe exhibits mature but uneven adoption. Germany integrates CRPS care within structured pain centers, whereas Nordic countries report pediatric resource gaps despite national health coverage. Brexit-era policy changes only modestly affect device approval timelines, and continental reimbursement remains comparatively generous. Nonetheless, surveys reveal fragmented pathways and delayed referrals, suggesting operational—not regulatory—barriers curb full market realization.

Asia-Pacific is the fastest-growing region at 3.45% CAGR, propelled by expanding middle-class access to surgery and diagnostic imaging. Still, large treatment gaps persist in emerging economies where pain services are scarce. Traditional remedies, including Chinese herbal preparations for CRPS foot pain, coexist with modern implants. Australia and Japan act as regional technology bellwethers, adopting closed-loop stimulators soon after US launch. Long-term upside remains tied to payer reform and specialist training, keeping the Complex Regional Pain Syndrome market outlook robust yet varied across the continent.

Competitive Landscape

The Complex Regional Pain Syndrome market is moderately concentrated, anchored by global device leaders Abbott, Medtronic, Boston Scientific, and, following a pending USD 250 million deal, Globus Medical’s acquisition of Nevro. Abbott’s Proclaim DRG system holds unique FDA labeling for CRPS and averages 81.4% pain reduction in trials. Medtronic’s Inceptiv closed-loop device records high user satisfaction by dynamically tuning output every 20 milliseconds. Boston Scientific differentiates through full-body MRI compatibility and omnidirectional waveforms.

Globus Medical’s bid for Nevro, owner of HF10 high-frequency waveforms and new AI algorithms, intensifies competition and broadens Globus’s spine care franchise. Pharmaceutical contention centers on sodium-channel modulators and IVIG trials, with Vertex’s suzetrigine approved for acute pain and cannabinoid candidate BRC-002 awarded Orphan Drug status. Cleveland Clinic’s NIH-funded stem-cell project exemplifies academic-industry collaboration aimed at the first disease-modifying therapy.

Digital health integration has become a strategic differentiator. Abbott’s NeuroSphere platform allows clinicians to fine-tune stimulation remotely, enhancing adherence and offering granular real-world data for payer negotiations. Start-ups are experimenting with wearable biosensors that convert physiologic pain signatures into objective dosing triggers, a concept that could shift value toward software-as-a-medical-device models within the Complex Regional Pain Syndrome market.

Complex Regional Pain Syndrome Industry Leaders

-

Boston Scientific Corporation

-

Medtronic

-

Johnson & Johnson

-

Abbott

-

Nevro Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Globus Medical announced a USD 250 million acquisition of Nevro Corporation to add the Senza and AI-enhanced platforms to its chronic pain portfolio.

- January 2025: FDA approved suzetrigine, a NaV1.8 selective analgesic, for moderate-to-severe acute pain, with ongoing evaluation in neuropathic conditions including CRPS.

- December 2024: Biopharmaceutical Research Company secured FDA Orphan Drug Designation for cannabinoid candidate BRC-002 targeting CRPS, with Phase 2 trials slated for late 2025.

- September 2024: Nevro received FDA clearance for an AI-based spinal cord stimulation system that self-optimizes stimulation parameters.

Global Complex Regional Pain Syndrome Market Report Scope

As per the scope of the report, complex regional pain syndrome (CRPS) is a rare debilitating disorder characterized by severe pain affecting one or more limbs. The Complex Regional Pain Syndrome (CRPS) market is segmented by Disease Type (CRPS I, CRPS II, and CRPS-NOS), Therapy Type (Drugs (Analgesics, Antidepressants, and Corticosteroids), Spinal Cord Stimulation, Surgical Sympathectomy, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| CRPS I |

| CRPS II |

| CRPS-NOS |

| Drugs | Analgesics |

| Antidepressants | |

| Corticosteroids | |

| Others | |

| Neuromodulation | Spinal Cord Stimulation (SCS) |

| Dorsal Root Ganglion Stimulation | |

| Surgical Sympathectomy | |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| Early Stage CRPS |

| Late Stage CRPS |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | CRPS I | |

| CRPS II | ||

| CRPS-NOS | ||

| By Therapy Type | Drugs | Analgesics |

| Antidepressants | ||

| Corticosteroids | ||

| Others | ||

| Neuromodulation | Spinal Cord Stimulation (SCS) | |

| Dorsal Root Ganglion Stimulation | ||

| Surgical Sympathectomy | ||

| Others | ||

| By Age Group | Adults | |

| Pediatric | ||

| Geriatric | ||

| By Disease Stage | Early Stage CRPS | |

| Late Stage CRPS | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Complex Regional Pain Syndrome market?

The Complex Regional Pain Syndrome market size stood at USD 122.57 million in 2026 and is projected to reach USD 139.46 million by 2031.

Which disease subtype holds the largest Complex Regional Pain Syndrome market share?

CRPS I dominates with 64.02% share, owing to its higher prevalence after trauma and surgery.

Why is neuromodulation growing faster than drug therapy?

Closed-loop and dorsal root ganglion stimulators deliver higher pain-relief rates and now benefit from clearer reimbursement, driving a 3.33% CAGR through 2031.

Which region is expected to grow the fastest?

Asia-Pacific leads growth with a 3.45% CAGR as surgical volumes climb and diagnostic awareness spreads.

How is reimbursement evolving for implantable devices?

US insurers such as Humana added peripheral nerve stimulators to Medicare Advantage in 2025, and European payers maintain broad coverage, reducing patient cost barriers.

What recent innovations could reshape long-term treatment?

FDA approvals of AI-driven stimulators and NaV1.8 inhibitors, along with NIH-funded stem-cell trials, signal a shift toward adaptive neuromodulation and potential disease-modifying therapies.

Page last updated on: