Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

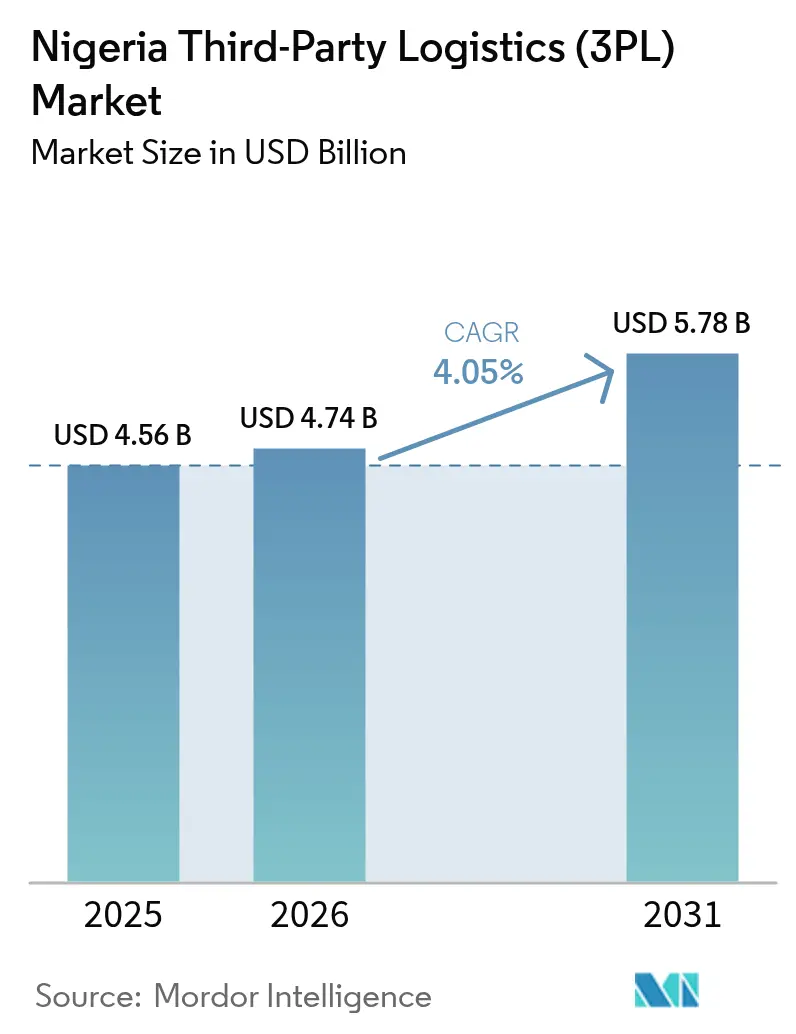

| Base Year Market Size (2025) | USD 4.56 Billion |

| Market Size (2026) | USD 4.74 Billion |

| Market Size (2031) | USD 5.78 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

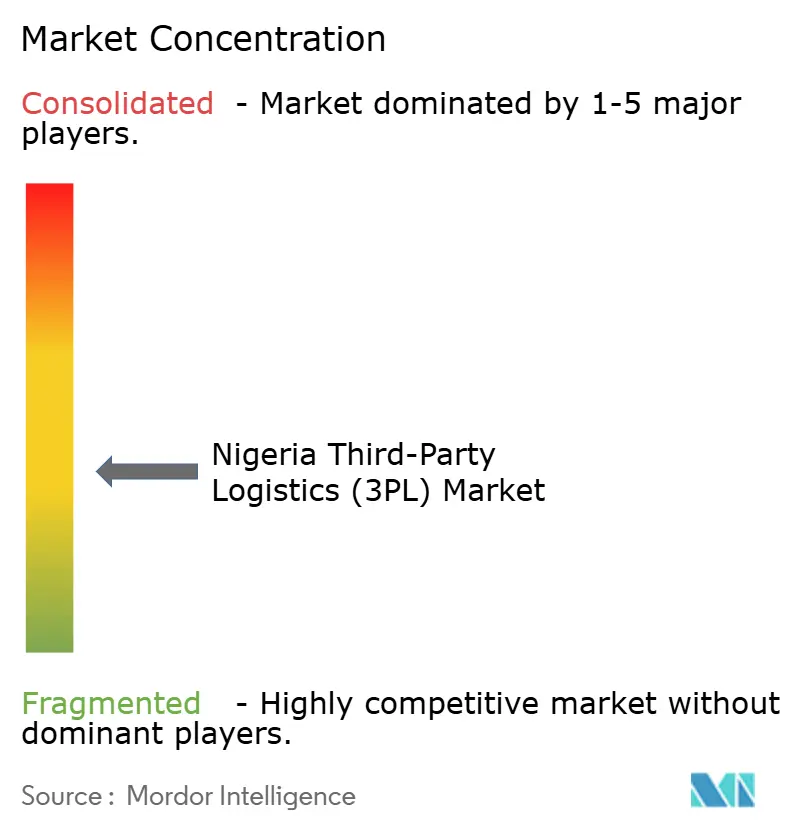

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The Nigerian third-party logistics market size is projected to expand from USD 4.56 billion in 2025 and USD 4.74 billion in 2026 to USD 5.78 billion by 2031, with a 4.05% CAGR between 2026 and 2031. Digitization is moving from pilot to production as the National Single-Window portal scheduled for March 2026 promises to cut clearance lead times from 18-21 days to fewer than 7 days and trim logistics costs by 25-30%. Simultaneously, the Lagos–Ibadan standard-gauge railway hauled 382,340 tons of containerized freight over January-August 2025, validating rail intermodal economics and easing road congestion. Fuel-subsidy removal in October 2024 increased diesel prices by more than 15%, accelerating the adoption of compressed natural-gas (CNG) vehicles, which save 40-50% on fuel costs. These developments redefine service mix choices, cost structures, and network design, positioning the Nigeria third-party logistics market for technology-led differentiation.

Key Report Takeaways

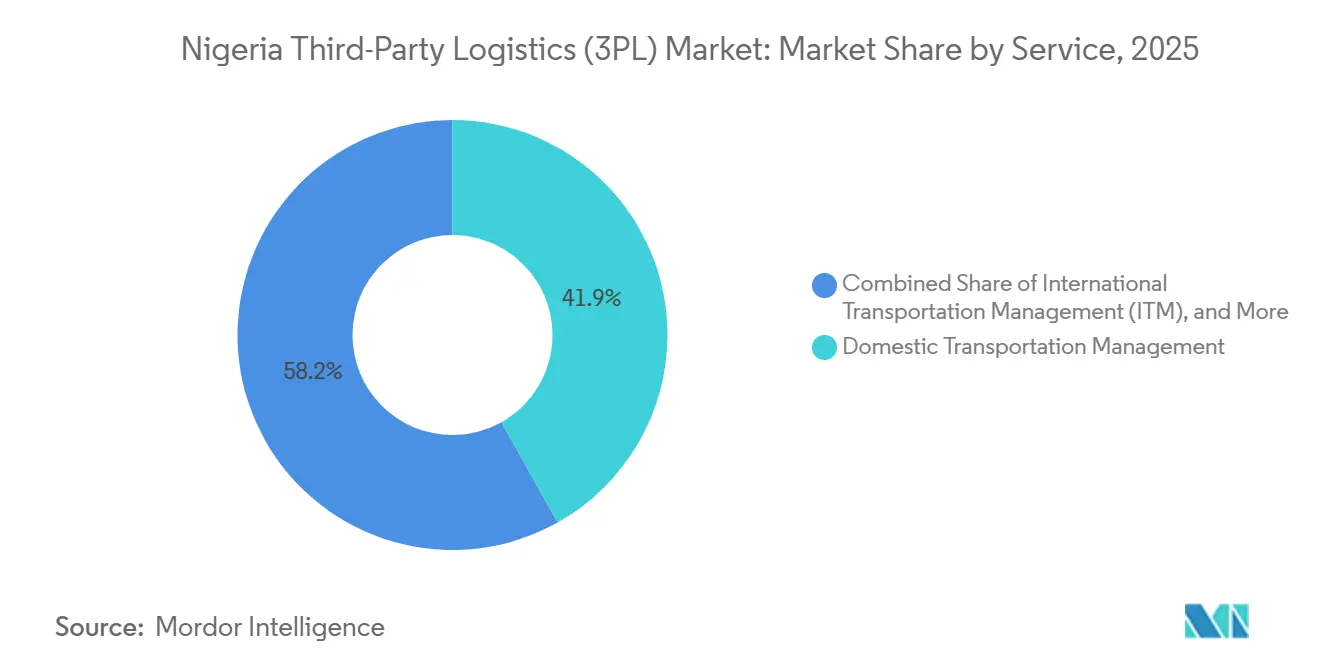

- By service, domestic transportation management led with 41.85% Nigeria third-party logistics market share in 2025, while international transportation management is forecast to expand at a 6.03% CAGR through 2031.

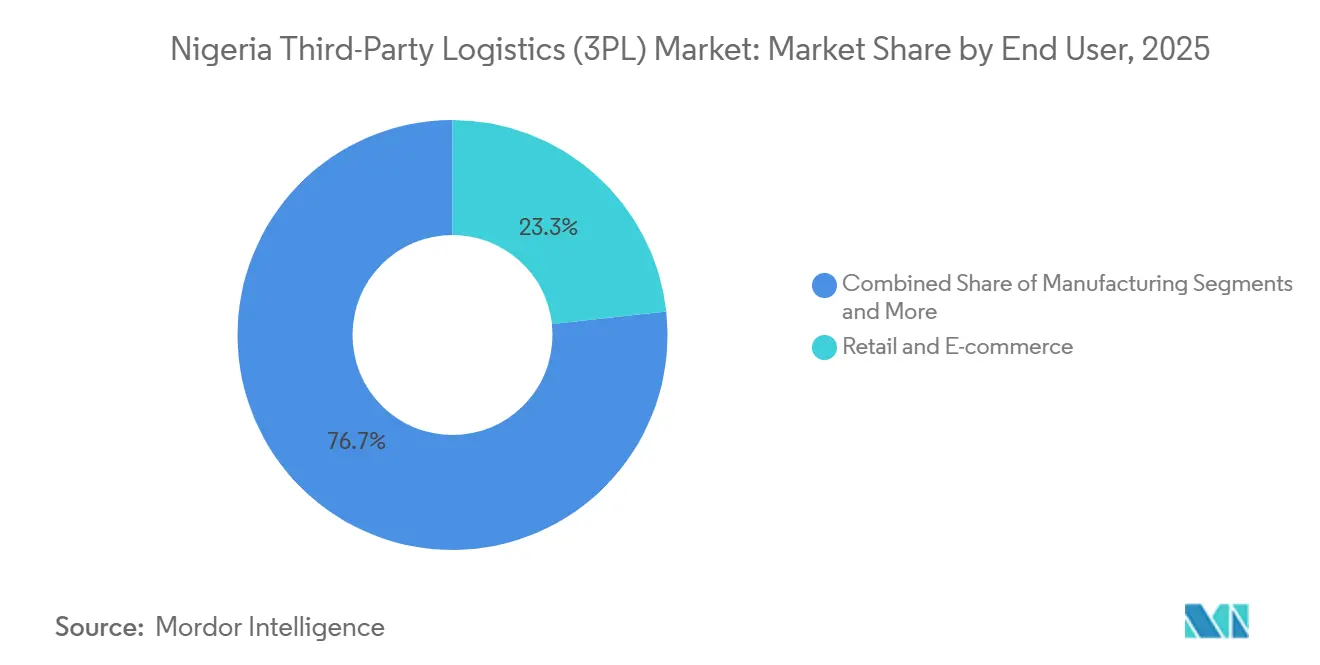

- By end user, retail and E-commerce accounted for 23.26% of the Nigeria third-party logistics market size in 2025, and life sciences and healthcare are advancing at a 6.16% CAGR through 2031.

- By logistics model, asset-light models captured 50.79% share of the Nigeria third-party logistics market size in 2025, whereas Hybrid configurations are projected to rise at a 5.39% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Single-Window roll-out slashing border-clearance lead-times | +1.1% | National, with primary impact at Lagos, Port Harcourt, Kano gateways | Medium term (2-4 years) |

| FMCG shift to vendor-managed inventory outsourcing | +0.8% | National, concentrated in Lagos, Onitsha, Kano distribution corridors | Medium term (2-4 years) |

| Fintech-backed pay-on-delivery insurance boosting B2C shipment volumes | +0.6% | Urban centers: Lagos, Abuja, Port Harcourt, Ibadan | Short term (≤ 2 years) |

| Lagos–Ibadan standard-gauge rail conversion for container freight | +0.5% | Southwest Nigeria, Lagos-Ogun-Oyo industrial axis | Short term (≤ 2 years) |

| Rapid expansion of the pharmaceutical and fresh-produce cold chain | +0.7% | National, with early concentration in Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Corporate ESG mandates accelerating green-fleet (EV/CNG) outsourcing | +0.4% | National, with early adoption in Lagos, Abuja, Kano | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Single-Window Roll-out Slashing Border-Clearance Lead-Times

The portal integrates 38 agencies into a unified platform that removes redundant paperwork and enables electronic permits, manifests, and duty payments. Importers gain predictable seven-day clearance windows that support just-in-time inventory and free working capital. Freight forwarders already piloting the system report lower demurrage, placing technology-enabled players ahead of manual brokers in the Nigeria third-party logistics market[1]“Nigeria Single Window Trade Portal to Go Live March 27,” Vanguard, vanguardngr.com . Alignment with AfCFTA protocols elevates Nigeria’s regional hub role, drawing multinational shippers that require clear service-level agreements.

FMCG Shift to Vendor-Managed Inventory Outsourcing

Consumer-goods makers are transferring forecasting, stock replenishment, and distribution-center operations to 3PLs with high-throughput warehouse-management systems. Outsourcing converts fixed warehousing costs into scalable variable expenses and leverages the multi-client density that 3PLs achieve. The arrangement reduces out-of-stock episodes in fragmented retail channels while slashing excess inventory, strengthening the Nigeria third-party logistics industry’s value-added revenue streams, and underpinning premium pricing[2]“Lagos-Ibadan Rail Generates N12 bn from Freight,” Punch, punchng.com.

Fintech-Backed Pay-on-Delivery Insurance Boosting B2C Shipment Volumes

API-driven insurance platforms cover in-transit loss and damage, lowering risk for e-commerce sellers and couriers in a cash-on-delivery culture. Claims that once took weeks now settle in days, unlocking demand from secondary cities that previously lacked reliable last-mile service. Logistics operators expand geographic reach without inflating bad-debt reserves, widening the Nigeria third-party logistics market addressable base for parcel delivery.

Lagos–Ibadan Standard-Gauge Rail Conversion for Container Freight

The rail service runs three weekly block trains, each moving 35 forty-foot equivalents, and generated NGN 12 billion (USD 8.26 million) revenue by August 2025. Rail trunk-haul cuts haulage cost by up to 40% when paired with last-mile trucking, prompting large 3PLs to sign volume commitments. The predictable timetable de-risks inventory positioning for manufacturers in Oyo and Ogun states, and underpins a modal shift that reduces highway wear and carbon intensity in the Nigeria third-party logistics market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-subsidy diesel price volatility inflating haulage tariffs | -0.8% | National, with acute impact on long-haul interstate operations | Short term (≤ 2 years) |

| Import-licence curbs on finished goods dampening inbound flows | -0.5% | National, concentrated at Lagos, Port Harcourt, Calabar ports | Medium term (2-4 years) |

| Shortage of warehouse-automation and WMS-skilled labour | -0.4% | National, most severe in secondary cities outside Lagos-Abuja axis | Long term (≥ 4 years) |

| Chronic port-scanner downtime driving berth-to-gate congestion | -0.6% | Lagos Apapa-Tin Can, Port Harcourt, Calabar port complexes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Subsidy Diesel Price Volatility Inflating Haulage Tariffs

Diesel now commands nearly NGN 1,000 (USD 0.68) per liter in Lagos, placing fuel at up to 50% of long-haul cost. 3PLs pass surcharges to shippers, eroding contract tenures and hurting budgeting accuracy. Smaller carriers defer maintenance and underinflate tires to stretch kilometers, risking safety and insurance premiums in the Nigeria third-party logistics market. The unpredictability constrains logistics operators' ability to commit to fixed-price contracts exceeding quarterly terms, limiting their attractiveness for clients seeking multi-year rate stability[3]“Import Prohibition List,” Nigeria Customs Service, customs.gov.ng.

Import-License Curbs on Finished Goods Dampening Inbound Flows

Prohibitions covering frozen poultry, older used vehicles, and instant noodles suppress containerized import demand that feeds customs brokerage revenues. Fewer inbound boxes also lift repositioning costs for exporters who need empties, complicating rate quotes for Nigeria third-party logistics market participants. The policy shift creates uncertainty for logistics operators' capacity planning as additional products face potential prohibition, constraining long-term infrastructure investment decisions[4]“Nigeria - Prohibited and Restricted Imports.” International Trade Administration, www.trade.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Rail Freight Emergence Reshapes DTM Economics

Domestic Transportation Management contributed 41.85% to the Nigeria third-party logistics market size in 2025, anchored in road trucking networks that crisscross 200,000 km of paved and unpaved roads. Diesel spikes translated into immediate surcharge clauses, prodding large shippers to test rail. With the standard-gauge line hauling 382,340 tons in eight months, rail-truck combinations now undercut road-only cost by up to 40%, improving delivered-unit economics. 3PLs that pre-book wagons enjoy fixed departures and reduced theft risk, while smaller brokers reliant on spot trucking lose share.

International Transportation Management is projected to register a 6.03% CAGR through 2031 as the Single-Window digitizes paperwork, trims dwell times, and elevates Nigeria’s AfCFTA hub aspirations. Value-Added Warehousing and Distribution gains from FMCG vendor-managed inventory contracts that migrate buffer stock into shared DCs. Collectively, these shifts elevate fee-based services, reinforcing multiproduct capability as the winning formula in the Nigeria third-party logistics market.

By End User: Healthcare Cold-Chain Mandates Drive Premium Growth

Life Sciences and Healthcare are set to grow at 6.16% CAGR to 2031, ahead of every other sector. Nationwide immunization and private-sector pharma demand drive GDP-compliant storage investment and temperature-validated delivery routes that fetch double the tariff of dry van moves. For shippers, validated chain-of-custody reduces spoilage and regulatory exposure, securing cold-chain premiums inside the Nigeria third-party logistics market.

Retail and E-commerce, with 23.26% share in 2025, leans on fintech-enabled delivery insurance to expand outside Tier-1 cities. Cash-rejection risk drops, orders rise, and 3PLs scale hub-and-spoke parcel networks that promise next-day service within 100 km radii. Automotive, Manufacturing, and Energy segments face import curbs and FX rationing that compress inbound volumes, yet offset declines through domestic component shipping that keeps assembly lines active.

By Logistics Model: CNG Economics Favor Hybrid Fleet Strategies

Asset-Light operators held 50.79% of the Nigeria third-party logistics market share in 2025, thriving on variable-cost capacity and tech platforms that match freight with vetted carriers. Exposure to spot-rate gyrations, however, narrows margins when diesel costs spike. Hybrid models, forecast to expand at 5.39% CAGR, blend owned CNG or diesel fleets on core lanes with brokered capacity elsewhere, balancing control and flexibility. The Presidential CNG Initiative bolsters this pivot by cutting per-kilometer cost and slashing CO₂ emissions by one-third.

Pure Asset-Heavy providers remain niche, focusing on cold chain, hazmat, and bulk liquids where specialized rigs create entry barriers. Capital outlays are mitigated through lease-back and manufacturer credit programs, allowing calculated expansion even as interest rates hover above 20%. The calculus underscores why the Nigeria third-party logistics market rewards adaptive capital allocation over one-size-fits-all models.

Geography Analysis

Lagos State dominates throughput thanks to Apapa and Tin Can ports, responsible for roughly 70% of container entries. Single-Window automation promises to compress Lagos clearance to under seven days, yet chronic scanner downtime and roadway chokepoints still impede last-mile fluidity. The Lagos-Ibadan rail link adds resiliency, ferrying containers to inland depots that bypass port gate queues and stabilize inventory cycles for manufacturers clustered in Ogun and Oyo.

Northern corridors anchored by Kano and Kaduna are seeing a rise in agricultural exports and CNG infrastructure. Five new LCNG stations commissioned in Kano in January 2026 extend refueling coverage, encouraging hybrid fleets that marry long-haul diesel legs with regional CNG shuttles. Abuja benefits from federal spending, positioning the capital as a cross-dock nexus between North and South.

Southern oil-producing states such as Rivers and Akwa Ibom specialize in project cargo for energy clients, but import-licence curbs on consumer goods dampen full-container flows through Port Harcourt. Nevertheless, AfCFTA-linked overland trade via Seme and Jibia borders is set to climb once the Single-Window integrates with regional customs nodes, deepening the Nigeria third-party logistics market’s West African footprint.

Competitive Landscape

The Nigeria third-party logistics market features moderate fragmentation: the top five providers account for roughly 35% of reported revenue, leaving ample room for mid-tier specialists. International players such as DHL Group, Bollore Transport and Logistics, and DSV leverage global trademarks, ISO certifications, and multimodal reach to court multinationals. Local champions like GIG Logistics, SIFAX Logistics, and Intels Nigeria exploit indigenous knowledge, flexible pricing, and port access concessions to compete effectively.

Technology adoption is the new frontier. DHL’s EUR 300 million (USD 352.89 million) African capex allocates funds for warehouse automation, bonded gateways, and data visibility upgrades that promise end-to-end tracking. GIG Logistics integrates electric trucks supplied by Jet Motor Company, shaving operating costs and ticking ESG boxes valued by consumer-product principals. SIFAX’s outbound LCL consolidation service taps SME exporters priced out of full-container bookings, enlarging share without heavy asset bets.

Green credentials are rising in bid evaluations as corporations request lane-by-lane emissions metrics. Operators that retrofit to CNG or deploy electric three-wheelers pick up last-mile contracts in Lagos, Kano, and Port Harcourt. Fintech alliances with Curacel enable embedded insurance that differentiates premium parcel tiers. Expect selective mergers: systems-ready mid-caps will acquire yard space, rail sidings, or cold-chain nodes to broaden their Nigeria third-party logistics market portfolios.

Nigeria Third-Party Logistics (3PL) Industry Leaders

ABC Transport

DHL Group

CMA CGM Group (Including Bollore Logistics)

Aramex

LXGlobal-Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: DHL Group earmarked more than EUR 300 million (USD 352.89 million) for Sub-Saharan Africa, including gateway upgrades and life-sciences facilities in Nigeria.

- April 2025: DHL Group signed a Memorandum of Understanding with Temu to enhance e-commerce delivery capabilities in Nigeria.

- August 2024: DHL Express launched the DHL Africa eShop platform across 11 African markets, including Nigeria, enabling consumers to shop directly from over 200 United States and the United Kingdom-based online retailers with door-to-door delivery.

- July 2024: SIFAX Logistics Limited partnered with ECU Worldwide through FMA-Line Nigeria Limited to launch Nigeria's first outbound LCL consolidation service for exporters.

Nigeria Third-Party Logistics (3PL) Market Report Scope

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing and Distribution (VAWD) |

By End User

| Automotive |

| Energy and Utilities |

| Manufacturing |

| Life Sciences and Healthcare |

| Technology and Electronics |

| E-commerce |

| Consumer Goods and FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet and Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing and Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy and Utilities | ||

| Manufacturing | ||

| Life Sciences and Healthcare | ||

| Technology and Electronics | ||

| E-commerce | ||

| Consumer Goods and FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet and Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the forecast value of the Nigeria third-party logistics market by 2031?

It is projected to reach USD 5.78 billion by 2031, expanding at a 4.05% CAGR between 2026 and 2031.

Which service segment currently holds the largest share?

Domestic Transportation Management commanded 41.85% Nigeria third-party logistics market share in 2025.

Which end-user vertical is growing the fastest?

Life Sciences and Healthcare is forecast to grow at 6.16% CAGR through 2031 due to cold-chain vaccine and pharma needs.

How will diesel subsidy removal affect logistics costs?

Diesel price volatility has lifted haulage tariffs and triggered widespread fuel-surcharge clauses that raise total landed costs.

What infrastructure projects most influence future competitiveness?

The National Single-Window portal, Lagos–Ibadan rail freight, expanded port scanners, and nationwide CNG refueling stations collectively reshape clearance time, modal mix, and fuel economics.

Page last updated on: