Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

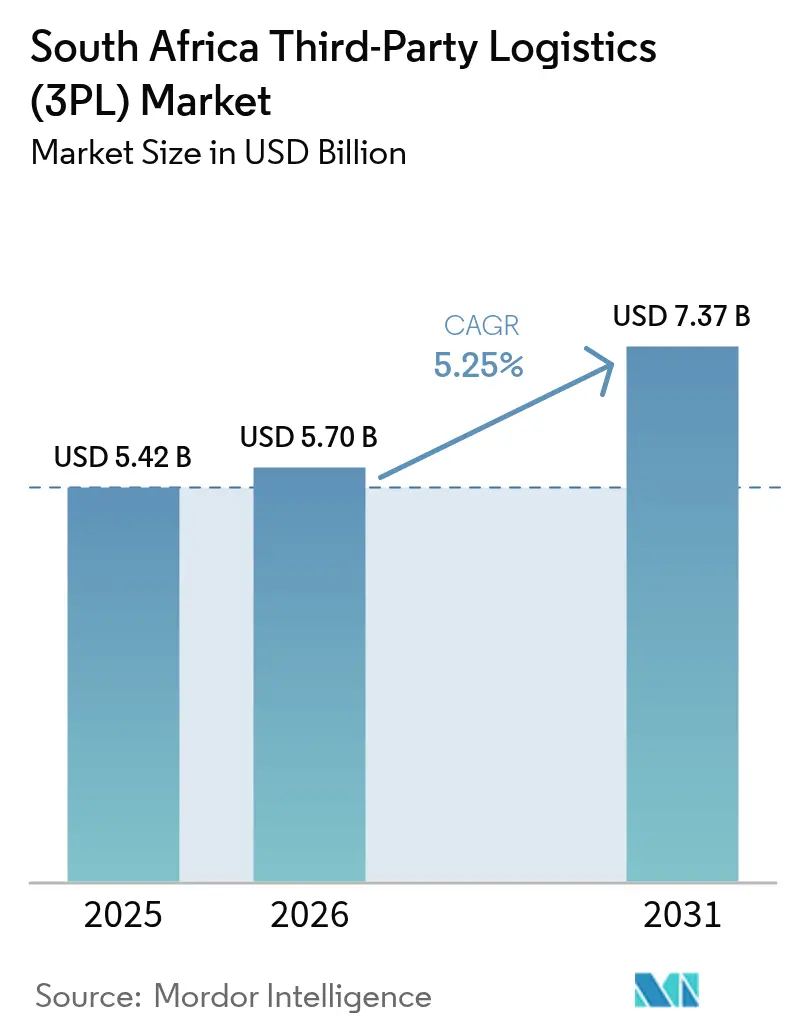

| Base Year Market Size (2025) | USD 5.42 Billion |

| Market Size (2026) | USD 5.7 Billion |

| Market Size (2031) | USD 7.37 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

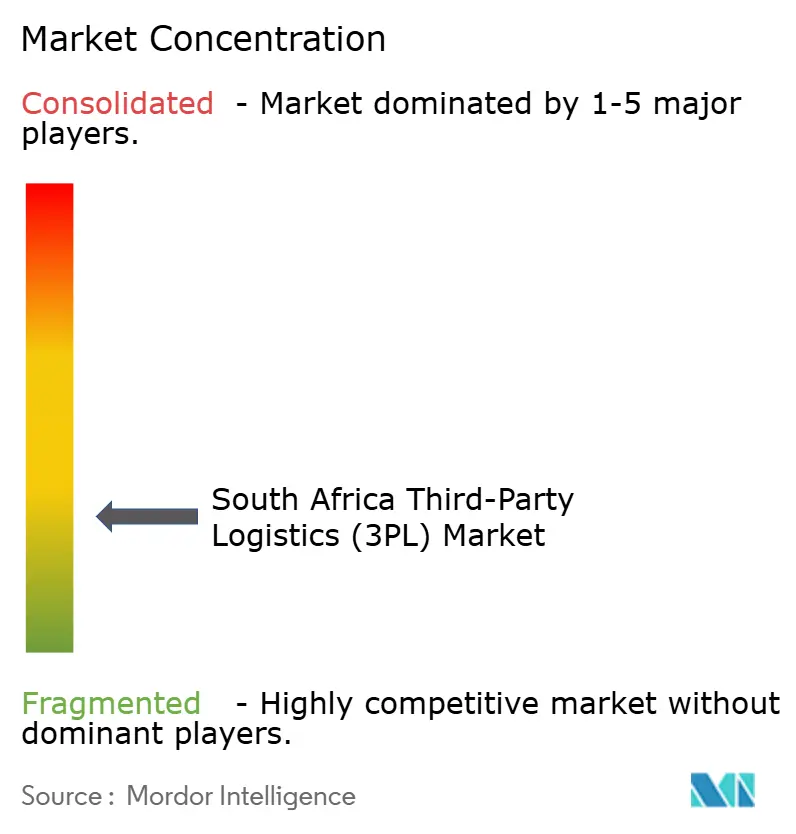

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The South Africa Third-Party Logistics Market size in 2026 is estimated at USD 5.70 billion, growing from 2025 value of USD 5.42 billion with 2031 projections showing USD 7.37 billion, growing at 5.25% CAGR over 2026-2031.

Spending on logistics still exceeds 11% of national GDP, yet the shift from road-only freight toward multimodal solutions is steadily lowering total landed costs and widening service offerings. E-commerce fulfillment, automotive exports, and infrastructure upgrades along the Durban–Gauteng corridor are reshaping service portfolios, while technology investments in telematics and AI are improving asset utilization and security. Asset-light models remain prevalent, but hybrid fleets are gaining traction as operators balance capital efficiency with capacity control. Rising cross-border demand under the African Continental Free Trade Area (AfCFTA) reinforces South Africa’s position as a gateway for regional trade growth.

Key Report Takeaways

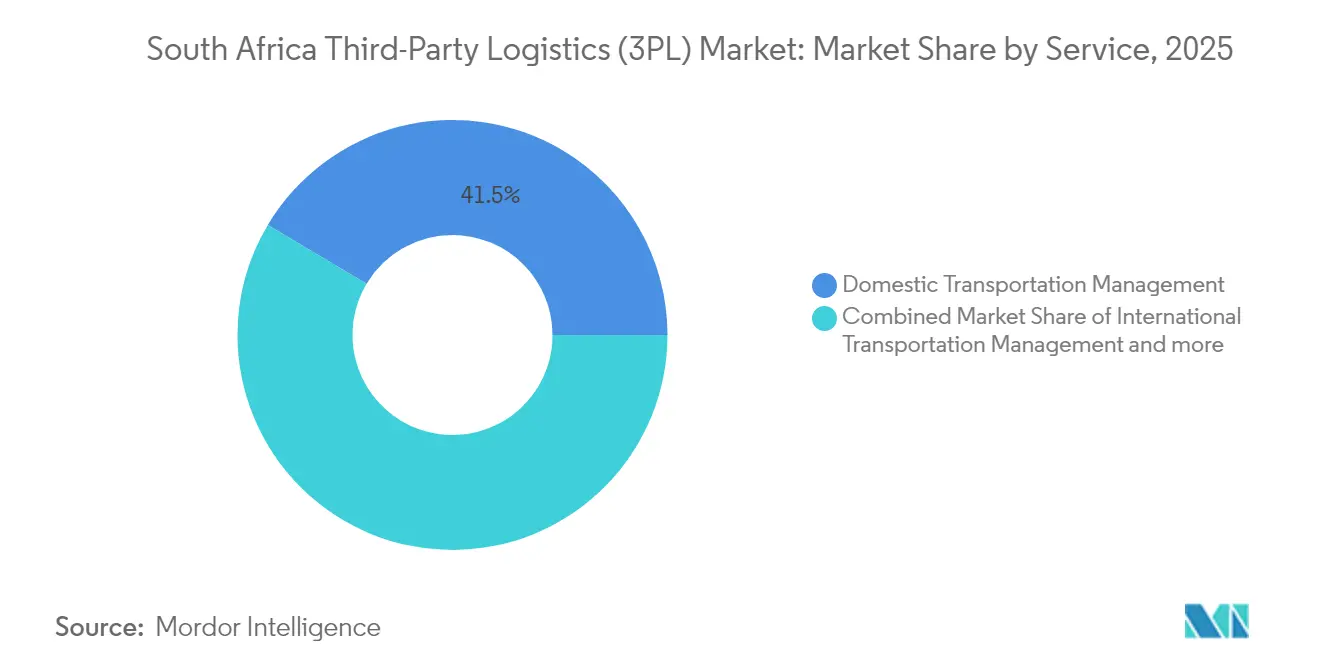

- Domestic Transportation Management held 41.45% of the South Africa third-party logistics market share in 2025.

- Value-Added Warehousing & Distribution is projected to post the fastest segment growth at 7.29% CAGR through 2031.

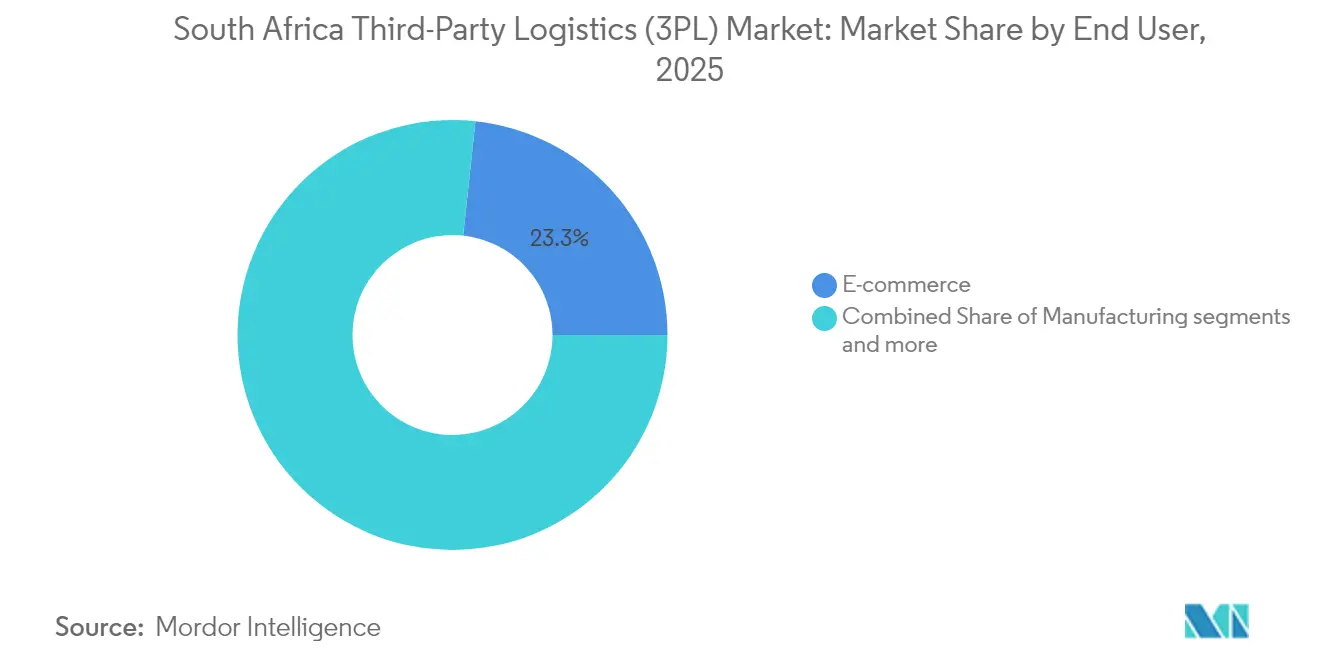

- E-commerce accounted for 23.30% of the South Africa third-party logistics market size in 2025, while Life Sciences & Healthcare is poised to expand at an 8.08% CAGR over the same horizon.

- Asset-light providers commanded a 51.35% share of the South Africa third-party logistics market in 2025; hybrid models are expected to grow at a 6.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom & last-mile demand | +1.2% | National, concentrated in Gauteng, Western Cape, KZN | Short term (≤ 2 years) |

| Automotive export-led logistics growth | +0.8% | Eastern Cape, Gauteng, KZN coastal corridors | Medium term (2-4 years) |

| Infrastructure upgrades on N3 & Durban port | +0.9% | KZN-Gauteng corridor, Durban metropolitan area | Medium term (2-4 years) |

| AfCFTA-driven cross-border trade flows | +0.7% | Border provinces, Gauteng hub, port cities | Long term (≥ 4 years) |

| Near-shoring of global supply chains into SA | +0.5% | Industrial corridors, Special Economic Zones | Long term (≥ 4 years) |

| Telematics-enabled cost efficiency for 3PLs | +0.6% | National, early adoption in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce boom & last-mile demand

Online retail turnover reached ZAR 71 billion (USD 3.9 billion) in 2024, a 29% rise year on year, and the last-mile segment is expected to exceed USD 2.3 billion by 2030. Grocery shoppers ordering online now represent 53% of the customer base, accelerating demand for urban micro-fulfillment nodes. Locker networks have expanded to roughly 1,200 units, cutting door-to-door costs and boosting delivery density. Platforms such as Bob Go processed 1.9 million shipments during H1 2025, evidencing SME appetite for outsourced fulfillment. Warehouse investments that feature automated guided vehicles and AI-based inventory controls, typified by Huawei’s 30,000 sqm Cape Town center, illustrate the sophistication required to maintain delivery velocity.

Automotive export-led logistics growth

The automotive sector contributes 6.2% to GDP and sustains over 93,000 manufacturing jobs, generating sizable volumes for component consolidation and vehicle exports via Eastern Cape ports. Chinese automakers lifted domestic market share from 12% to 21% between 2019 and 2024, intensifying competitive pressures on local assembly lines and the supporting logistics network. Containerized vehicle-transport platforms such as Kar-Tainer mitigate ro-ro lead-time spikes and protect units in transit. Incentives under the Automotive Production and Development Programme underpin further OEM production volume commitments, opening opportunities for specialized just-in-time delivery and reverse-logistics services.

Infrastructure upgrades on N3 & Durban port

Transnet allocated R233 million to rehabilitate 16 critical roads inside the Port of Durban, which handles 60% of national container volumes[1]Khulekani Magubane, “Transnet Starts R233 Million Durban Port Road Rehabilitation,” South African Government News Agency, sanews.gov.za. The privately financed R3.4 billion Newlyn PX Bayhead Rail Terminal will manage 1,400 daily truck moves within a multimodal precinct. SANRAL’s R48 billion N2/N3 widening will double lane capacity and cut congestion between Durban and Gauteng[2]Siyabonga Gama, “Durban Container Terminal Roadworks Fact Sheet,” Transnet National Ports Authority, transnetnationalportsauthority.net. Upgrades target the 20% rise in cross-border transit times that added R170 million in annual delay costs and will give 3PLs more predictable transit schedules.

AfCFTA-driven cross-border trade flows

Duty-free access to 1.3 billion consumers is expected to lift intra-African trade to USD 192.2 billion in 2024. Customs brokerage demand is rising as operators navigate varied border processes; South African 3PLs are investing in digital pre-arrival systems to speed clearances. The Maputo Development Corridor positions Mpumalanga for mineral and agricultural exports, while the Single African Air Transport Market promises lower freight costs for time-sensitive commodities. Compliance with the Border Management Authority’s risk-based controls is pushing the adoption of advanced cargo-tracking and electronic documentation capabilities.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail & port bottlenecks | -1.1% | National, concentrated at Durban, Richards Bay, Cape Town ports | Short term (≤ 2 years) |

| High and volatile diesel prices | -0.8% | National, affecting road transport operations | Short term (≤ 2 years) |

| Skilled labour gap in warehouse automation | -0.6% | Urban centers, industrial hubs | Medium term (2-4 years) |

| Cargo-theft hotspots along N3 corridor | -0.4% | N3 corridor, Gauteng province | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rail & port bottlenecks

Durban continues to face berth congestion and equipment shortages that depress vessel productivity and increase dwell times. Richards Bay’s annual shutdowns to unlock rail slots succeeded in removing 1,035 daily truckloads from roads, yet underscore structural capacity deficits. Private-sector entry onto the Transnet rail network was formally approved in 2024, aiming to mobilize investment and restore reliability for bulk and container flows. Shippers diverted more than one-quarter of long-haul volumes from rail to roads over the past five years, boosting highway congestion and freight costs. Stakeholder alignment on open-access frameworks is critical to attract capital and modernize rolling stock.

High and volatile diesel prices

Diesel accounts for close to 50% of daily trucking costs, and pump prices climbed by up to ZAR 1.50 per liter during 2024. Extended client payment cycles reaching three months stretch operator liquidity. Some fleets respond by deploying load-planning software, rigorous driver coaching, and fuel procurement agreements to cap expenditure volatility. Leaders are piloting battery-electric trucks; Takealot reported 19% lower total cost of ownership and 14 tons of annual CO₂ cuts per vehicle. Wider electrification hinges on charging-station density and targeted incentives to offset higher upfront capital costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Multimodal Integration Drives Efficiency

Domestic Transportation Management led with 41.45% of the South Africa third-party logistics market share in 2025, reflecting the road freight dominance in inland movements. Value-Added Warehousing & Distribution is projected to register a 7.29% CAGR, supported by automated facilities such as Shoprite’s Cilmor hub featuring 133 dock doors and high-density picking systems. The South Africa third-party logistics market size attached to international transport will benefit from AfCFTA-induced volume, but remains constrained by port congestion. Multimodal solutions that blend road, rail, and coastal shipping are increasingly specified in large tenders, indicating a structural pivot away from single-mode contracting.

Investment in supply-chain visibility is rising across all services. DSV opened a 100,000 sqm logistics campus near O.R. Tambo International Airport, consolidating air, ocean, road, and cross-dock operations within one technology-enabled platform. Grindrod leverages IoT sensors and cloud analytics to offer real-time cargo location dashboards, shortening exception-response cycles. Such capabilities set new performance baselines, reinforcing the market’s drift toward integrated, data-rich service contracts.

By End-User: Healthcare Logistics Accelerates Growth

E-commerce retained 23.30% of the South Africa third-party logistics market size in 2025, buoyed by more than 1 billion online transactions annually. Life Sciences & Healthcare is forecast to expand at an 8.08% CAGR, propelled by vaccine storage requirements and growing biologics imports. DHL commissioned a specialized cold-chain facility adjacent to O.R. Tambo Airport, illustrating the capital intensity required to secure pharmaceutical integrity. The maritime reefer trade for citrus and grapes supports demand for validated temperature-controlled trucking networks, while regulatory oversight under the Foodstuffs, Cosmetics and Disinfectants Act tightens compliance obligations.

Automotive exports stimulate specialized parts sequencing and milk-run services, but component supply volatility linked to global steel market shifts adds complexity. Consumer Goods and FMCG players focus on mixed-case palletization and rural route-to-market coverage; security-sensitive Technology & Electronics shippers mandate sealed trailer operations and dual-driver protocols. The South Africa third-party logistics market share associated with cold-chain foodservice has risen as quick-service restaurant chains expand footprint, pushing 3PLs to add multi-temperature vehicles and hazard-analysis protocols.

By Logistics Model: Hybrid Approaches Gain Traction

Asset-light operators accounted for 51.35% of the South Africa third-party logistics market in 2025, relying on subcontracted fleets and leased warehouses to limit capital exposure. Hybrid models are projected to post a 6.61% CAGR, combining owned assets in strategic nodes with flexible partner capacity elsewhere, enabling service continuity during peak demand. Imperial Logistics exemplifies the model, integrating owned fleet operations with third-party alliances across 25 countries. Asset-heavy providers remain relevant in contract logistics requiring dedicated, high-spec equipment; Vector Logistics’ voice-directed picking technology raises accuracy and labor productivity in temperature-controlled distribution.

Telematics penetration is set to climb from 47.3% to 70% by 2028 as 98% of fleet managers budget for additional digital tools. Predictive maintenance and driving-behavior analytics lower unplanned downtime, supporting higher on-time delivery metrics. The South Africa third-party logistics industry continues to recalibrate capital allocation between trucks, IT, and warehouse automation to sustain margins in an environment of cost-plus pricing pressure.

Geography Analysis

Gauteng generates 34% of national GDP and anchors the country’s freight flows; the province secured R52.3 billion in new investment during 2023/24, including R21.6 billion from foreign investors, reinforcing its role as the core consolidation hub. The R21 corridor linking Pretoria to O.R. Tambo Airport is evolving into an inland port zone, attracting multinationals such as DSV and Takealot with bonded-warehouse incentives and rapid freeway access.

KwaZulu-Natal’s Port of Durban moves 60% of containers but grapples with quay congestion and variable truck turnaround times. Upgrades at the Dube TradeZone Special Economic Zone provide uninterruptible power and in-park customs offices, appealing to electronics assembly and high-value manufacturing tenants. Western Cape exports wine, fruit, and finished foods through Cape Town, necessitating chilled reefers and EU-compliant phytosanitary handling. Limited rail connectivity prompts intermodal operators to truck reefers north to inland depots before railing to ports.

Eastern Cape hosts automotive clusters around Gqeberha (Port Elizabeth), generating demand for sequencing centers and line-side deliveries. The Vaal Special Economic Zone in Gauteng seeks to integrate air, road, rail, and inland water transport to support mining supply chains. New rail spur links to Botswana and Zimbabwe via Limpopo are under feasibility study, aimed at diverting mineral exports from congested coastal ports. Across all regions, SARS’ mandatory 24-hour advance manifest filing incentivizes documentation digitization and promotes early-stage customs pre-clearance, cutting dwell time at entry points.

Competitive Landscape

Market concentration is fragmented, with incumbent multinationals and large domestic groups holding material share while specialist entrants target high-growth niches. DP World’s USD 883 million acquisition of Imperial Logistics in March 2025 gave the port operator an integrated continental network and signaled intensifying competition from global players. Grindrod earmarked R8 billion for bulk-cargo, container, and rail expansions across South Africa and Mozambique, underlining the importance of corridor control for AfCFTA freight.

Five telematics providers—Cartrack, Tracker, MiX by Powerfleet, Ctrack, and Netstar—control 70% of installed fleet-management units, offering bundled routing, fuel management, and theft-recovery services. White-space remains in value-added warehousing for life-science cargo, digitally enabled cross-border brokerage, and green-fleet leasing. Operators that embed AI-driven demand planning and predictive analytics inside control-tower models are achieving cycle-time and cost advantages that widen competitive moats.

South Africa Third-Party Logistics (3PL) Industry Leaders

Bidvest International Logistics

Kuehne + Nagel

DSV

Barloworld Logistics

Onelogix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DP World completed the USD 883 million buy-out of Imperial Logistics, bolstering end-to-end African coverage and enhancing trade connectivity.

- May 2025: Grindrod reported R7.4 billion revenue for 2024 and confirmed R8 billion infrastructure outlay, including further Maputo port capacity.

- February 2025: DSV opened Africa’s largest integrated logistics hub near Johannesburg, adding 100,000 sqm of warehousing to support e-commerce growth.

- January 2025: Kuehne + Nagel finalized the takeover of Morgan Cargo, expanding perishables forwarding of 40,000 t air freight and 20,000 TEU sea freight per year.

South Africa Third-Party Logistics (3PL) Market Report Scope

A comprehensive background analysis of the South Africa Third-Party Logistics (3PL) Market, covering the current market trends, restraints, technological updates and detailed information on various segments and competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the projected value of the South Africa third-party logistics market by 2031?

The market is forecast to reach USD 7.37 billion by 2031, expanding at a 5.25% CAGR.

Which service segment is growing fastest?

Value-Added Warehousing & Distribution is expected to post the highest growth at 7.29% CAGR to 2031.

How large is the e-commerce segment within logistics?

E-commerce accounted for 23.30% of market revenue in 2025, supported by more than 1 billion online transactions that year.

Why are hybrid logistics models gaining favor?

Hybrid models balance owned assets with flexible partner capacity, enabling 6.61% CAGR growth while preserving capital flexibility.

Page last updated on: