Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

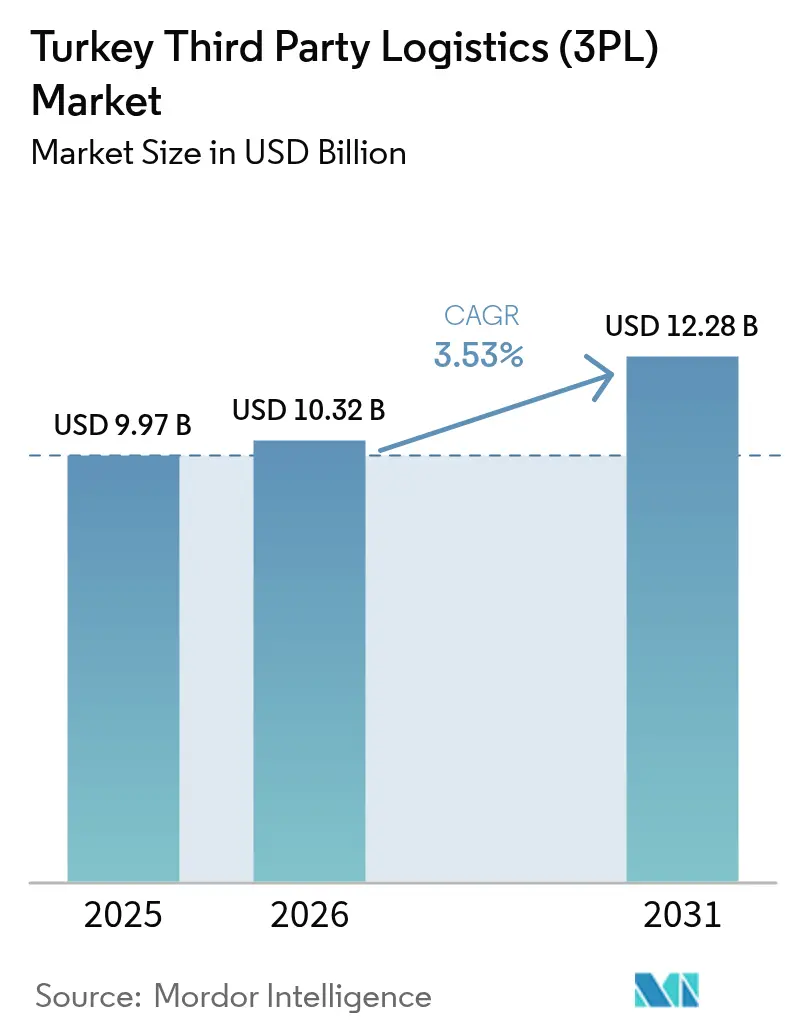

| Base Year Market Size (2025) | USD 9.97 Billion |

| Market Size (2026) | USD 10.32 Billion |

| Market Size (2031) | USD 12.28 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

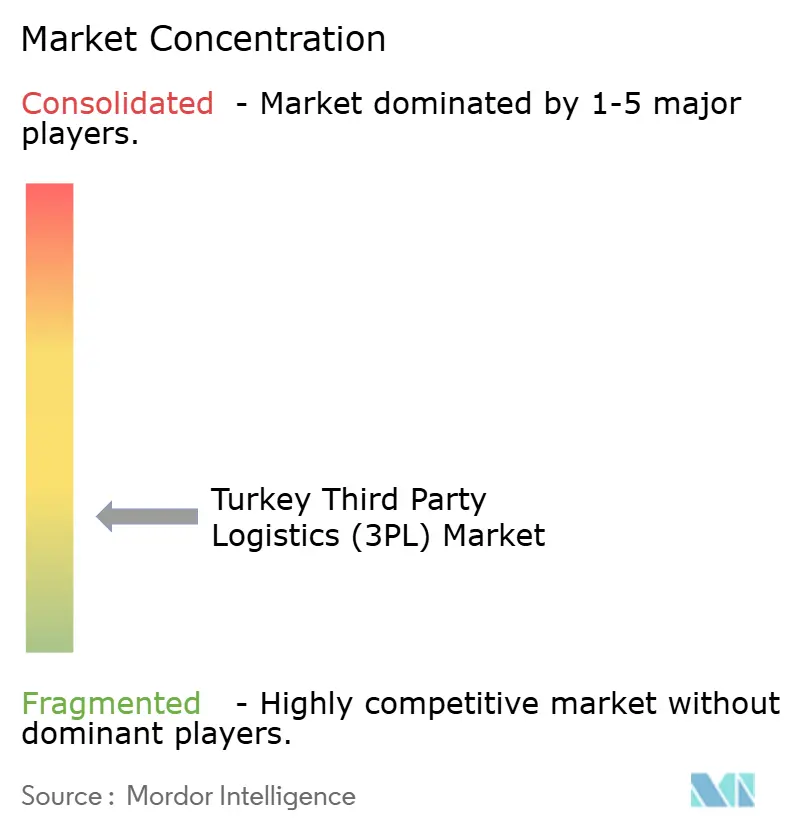

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Third Party Logistics (3PL) Market Analysis by Mordor Intelligence

The Turkey Third Party Logistics Market size was valued at USD 9.97 billion in 2025 and estimated to grow from USD 10.32 billion in 2026 to reach USD 12.28 billion by 2031, at a CAGR of 3.53% during the forecast period (2026-2031).

The country’s role as a land-bridge between Europe, Asia, and the Middle East underpins steady demand, while government spending on highways, railways, and 25 dedicated logistics centers strengthens network efficiency [1]Invest in Türkiye, “Turkey’s Logistics Performance and Infrastructure Investments,” Invest in Türkiye, invest.gov.tr. Rising e-commerce parcels, expanding cold-chain requirements in pharmaceuticals and food, and EU near-shoring of production continue to widen the customer base for third-party providers. Operators are favoring asset-light strategies to mitigate currency risk and scale capacity quickly, yet acquisitions such as CEVA’s purchase of Borusan Tedarik and DHL’s takeover of MNG Kargo show that well-located distribution assets still command a premium. Supply-side constraints are visible in a projected driver shortfall of 200,000 positions and looming EU Carbon Border Adjustment Mechanism costs, but Turkey’s target of a top-25 Logistics Performance Index ranking by 2028 indicates sustained policy support.

Key Report Takeaways

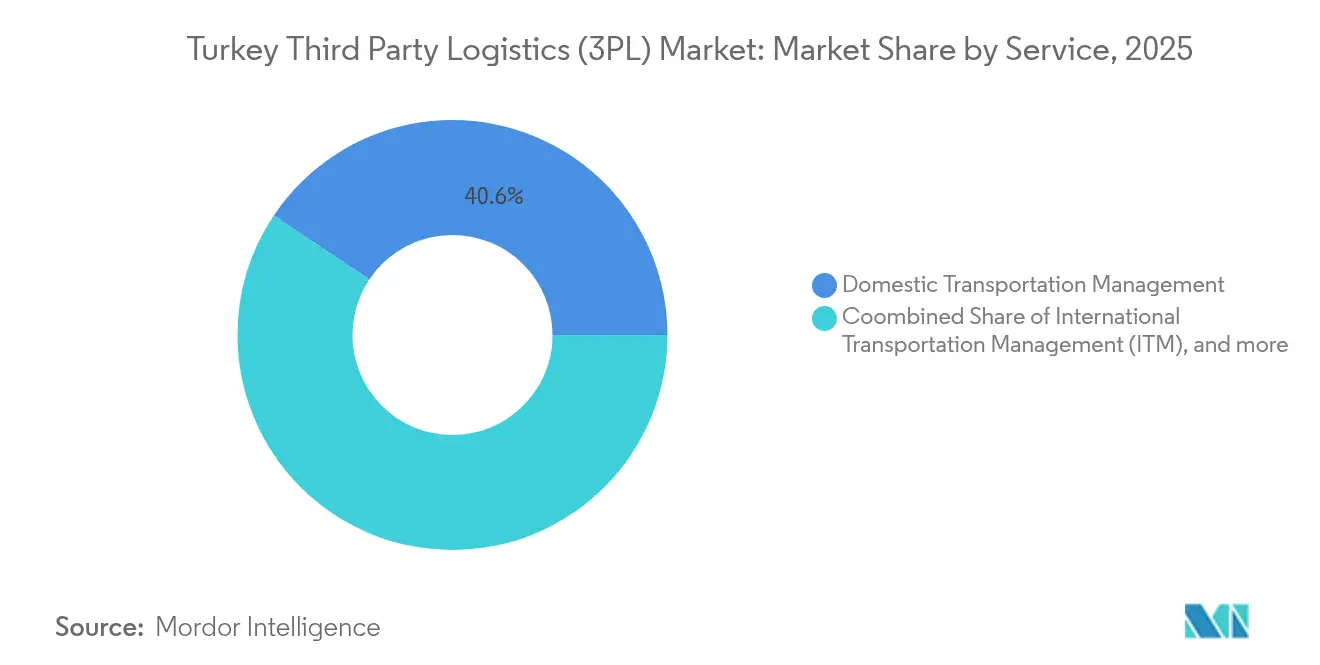

- By service, Domestic Transportation Management led with 40.62% of the Turkey third-party logistics market share in 2025, while Value-Added Warehousing & Distribution is advancing at a 7.66% CAGR, between 2026-2031

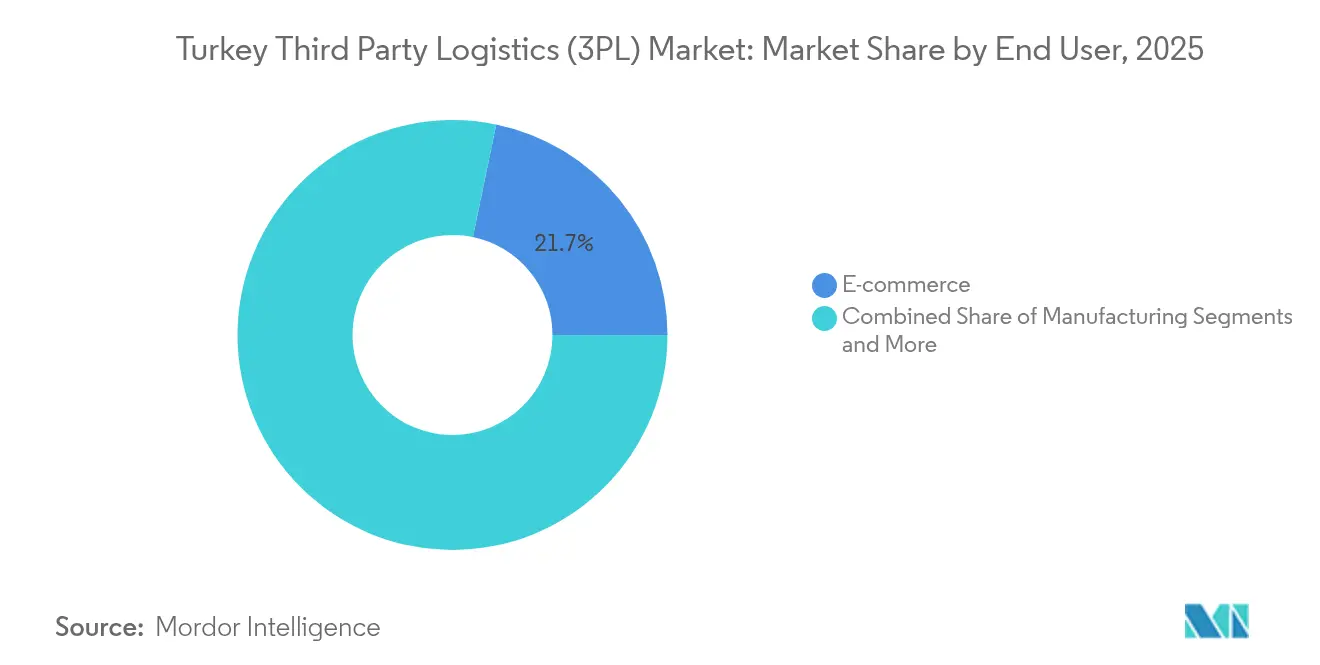

- By end user, E-commerce held 21.74% of the Turkey third-party logistics market share in 2025. while Life Sciences & Healthcare is projected to post a 6.97% CAGR during 2026-2031.

- By logistics model, Asset-Light operators controlled 49.61% of the Turkey third-party logistics market share in 2025, while Hybrid models are expected to expand at a 6.69% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Third Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom & omnichannel retailing | +0.8% | National, concentrated in Istanbul, Ankara, Izmir | Short term (≤ 2 years) |

| Logistics Master Plan infrastructure upgrades | +0.6% | National priority corridors | Medium term (2-4 years) |

| Near-shoring of EU supply chains to Turkey | +0.7% | Western border provinces, Marmara Region | Medium term (2-4 years) |

| Expansion of cold-chain demand (pharma & food) | +0.4% | Nationwide pharma hubs & farm belts | Long term (≥ 4 years) |

| Incentives for free-zones & bonded warehouses | +0.3% | Port-adjacent free zones | Medium term (2-4 years) |

| SME adoption of digital TMS/WMS platforms | +0.2% | Export-oriented industrial centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom & Omnichannel Retailing

Fast grocery pioneer Getir’s USD 11.8 billion valuation epitomizes Turkey’s online shopping surge, with pandemic-era downloads up 60% and order volumes up 65%. Traditional retailers have reacted by integrating store and online inventories, which drives demand for high-velocity fulfillment centers, smart sorters, and route-optimization software. DHL’s purchase of parcel specialist MNG Kargo, whose automated hubs can sort 65,000 packages an hour, illustrates the capital intensity required to meet one-day delivery promises. Small exporters gain scale through cross-border portals such as DHgate, which has trained 2,500 local merchants and exceeded USD 1 billion in Turkish trade, further inflating parcel volumes. Rapid shopper uptake across Istanbul, Ankara, and Izmir makes e-commerce the single largest incremental contributor to the Turkey third-party logistics market.

Logistics Master Plan Infrastructure Upgrades

An earmarked USD 280 billion investment program since 2003 has allocated 55% to rail, while 38,000 km of divided roads and 8,300 km of highways are targeted for completion by 2053[2]Turkey 2053 Transport and Logistics Master Plan,” Ministry of Transport and Infrastructure, uab.gov.tr. Nine of 25 planned logistics centers are already online, creating 35.6 million tons of annual capacity and dovetailing with port modernization that lifted 2024 maritime throughput to 542.6 million tons. Konya Logistics Center alone aims to raise annual tonnage from 634,000 to 1.679 million, demonstrating how inland nodes will relieve coastal congestion. The 1,200 km Development Road Project, linking Iraq’s Grand Faw Port to Turkey and on to Europe by 2030, promises a time-saving southern corridor that complements the Middle Corridor rail route. Improved connectivity lowers transit costs and reliability risks, lifting demand for contract logistics, intermodal coordination, and cross-dock services across the Turkey third-party logistics market.

Near-shoring of EU Supply Chains to Turkey

Post-pandemic resilience strategies have compelled European manufacturers to shorten supply lines, making Turkey a preferred alternative to East Asia. Blue Water Shipping, DFDS, and InterRail have opened Turkish subsidiaries or added Ro-Ro rotations to speed Marmara–EU flows, while BLG Logistics has set up an automotive logistics unit to support local production of 1.4 million vehicles and imports of 626,000 cars. The uptick in component shuttles and finished-goods exports demands temperature-controlled warehousing, bonded storage, and customs-compliant consolidation—all services intrinsic to the Turkey third-party logistics market. Near-shoring also boosts back-haul utilization, reducing empty-run costs and enhancing 3PL margins, particularly for providers with flexible asset-light fleets.

Expansion of Cold-Chain Demand (Pharma & Food)

Turkish Cargo’s CEIV-Pharma-certified SMARTIST hub now handles 55,000 t of medicines and has delivered 330 million vaccine doses worldwide, highlighting technical competence in GDP-compliant handling. National cold storage already totals 35,000 m³ in Ankara, supplemented by 360 regional facilities and a fleet of insulated trucks serving all 81 provinces. The EBRD’s EUR 25 million investment in Netlog’s new temperature-controlled warehouses confirms institutional confidence in long-haul frozen and chilled chains. Çelebi’s IoT-enabled cargo WMS and Mars Logistics’ move to electric rail traction underline the sustainability imperative in cold logistics. Rising biologic drug output and fresh-produce exports ensure that cold-chain logistics remains the most technology-intensive growth pocket of the Turkey third-party logistics market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lira volatility inflating import costs | -0.6% | Nationwide, import-heavy sectors | Short term (≤ 2 years) |

| Bureaucratic customs procedures | -0.3% | Ports & border crossings | Medium term (2-4 years) |

| Driver shortages & rising labor costs | -0.4% | Major logistics hubs | Medium term (2-4 years) |

| EU CBAM & decarbonization compliance costs | -0.2% | Export-oriented clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lira Volatility Inflating Import Costs

The lira’s depreciation raises truck procurement, fuel, and IT hardware expenses because roughly 70% of equipment is priced in euros or dollars. Customs Law No. 4458 was amended to cut the express-cargo duty-free limit from EUR 150 to EUR 30, boosting clearance volumes but squeezing margins on low-value shipments. Mars Logistics is still committed to EUR 70 million to new tractors in 2024 after spending EUR 65 million in 2023, showing the capex needed to preserve service quality despite currency swings. Smaller 3PLs lacking natural hedges face higher working-capital requirements when leasing trailers or importing scanners, which limits their ability to scale. These pressures subtract 0.6% from the forecast CAGR of the Turkey third-party logistics market.

Driver Shortages & Rising Labor Costs

Turkey anticipates a deficit of 200,000 professional drivers—28% of demand—by 2027, driven by an aging workforce and EU migration. Wage hikes of 27% in 2024 outpaced inflation-adjusted freight rates, compressing margins for haulers and forcing 3PLs to invest in retention bonuses and driver-friendly scheduling[3]International Road Transport Union, “Driver Shortage Report 2025 – Turkey Focus,” IRU, iru.org. Autonomous platooning trials remain limited to controlled corridors, so relief via automation is unlikely before 2030. Large fleets charter additional sub-contractors, but this raises coordination complexity and service-quality variance. Shortages subtract an estimated 0.4% from the Turkey third-party logistics market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominates, Warehousing Accelerates

Domestic Transportation Management controlled 40.62% of the Turkey third-party logistics market share in 2025, supported by a 68,494 km road grid that lets truckers complete Istanbul–Gaziantep hauls in under 16 hours. The segment remains price sensitive because diesel accounts for over 30% of trip cost, yet a premium applies for time-definite and GDP-certified moves. International Transportation Management benefits from Ro-Ro frequency gains on the Trieste, Bari, and Toulon loops, but bureaucratic customs and CBAM risks temper its expansion pace. Value-Added Warehousing & Distribution is on track for a 7.66% run-rate, doubling its revenue share by 2030 as fulfillment models shift toward micro-hubs and multi-temperature storage. CEVA’s acquisition of Borusan Tedarik enlarged its national pallet footprint to 1.19 million m², confirming the land-grab underway for urban DC slots near Istanbul’s highway rings.

The Turkey third-party logistics market size for warehousing services is projected to advance at a pace that lifts its absolute revenue by USD 0.94 billion through 2031. Automation orders for shuttle systems and AMRs have risen 18% year-on-year because parcel sortation speed is now a retail KPI. Rail investment—55% of the transport capex budget—introduces fresh intermodal competition that could divert 15% of long-haul trucking volume to wagonload services by 2028. Mars Logistics’ plan for 40 weekly electric-traction trains illustrates how 3PLs hedge fuel price uncertainty while offering CO₂-optimized routes. Turkey third-party logistics market participants that integrate road, rail, and cross-dock assets are set to earn higher EBITDA margins by balancing load factors across modes.

By End User: Retail Leads, Healthcare Surges

E-commerce accounted for 21.74% of the Turkey third-party logistics market share in 2025, underpinned by marketplace sales that grew 35% on GMV and by an urban population with 75% smartphone penetration. High SKU churn and seasonal demand spikes create a constant need for fourth-party orchestration, vendor-managed inventory, and same-day delivery. Life Sciences & Healthcare is forecast to reach a 6.97% CAGR as domestic biologic drug plants and vaccine fill-finish lines expand capacity; Turkish Cargo’s CEIV-Pharma hub sets industry handling benchmarks. Automotive logistics stays a core volume generator with 1.4 million vehicle assemblies and 626,000 imports, requiring just-in-time inbound sequencing and finished-vehicle compound management.

Turkey third-party logistics market size for healthcare shipments could surpass USD 1.07 billion by 2031, assuming present growth trajectories hold. Cold boxes with IoT probes, passive packaging, and GDP-trained handlers are mandatory for serum and insulin cargoes, raising service premiums over ambient freight. Manufacturing and Technology & Electronics together broaden contract-logistics scope through demand for pick-to-light, bonded postponement, and regional hubbing for EU, CIS, and MENA deliveries. Food & Beverages leverage Turkey’s position as a top exporter of cherries, citrus, and frozen fish, calling for reefer consolidation and HACCP-compliant warehousing in Mersin and Izmir. Energy, Utilities, and project cargo segments book steady but lumpy demand, typified by Arkas Logistics’ wind-turbine hub solutions on the Aegean coast.

By Logistics Model: Asset-Light Preference, Hybrid Growth

Asset-Light operators held 49.61% of the Turkey third-party logistics market share in 2025, thanks to subcontracted fleets, leased depots, and digital control towers that minimize currency-denominated asset exposure. Netlog’s SAP-TM deployment coordinates 4,000 vehicles and 1.2 million m² of multi-client space across nine countries, demonstrating the global scalability of a non-asset-heavy balance sheet. Asset-heavy players still dominate hazardous bulk and project cargo, where owned equipment removes reliability risk, but financing costs in a high-interest environment hamper expansion. Hybrid models are growing at 6.69% annually as firms selectively own cross-dock terminals, e-fulfillment hubs, or reefer trailers while subcontracting line-haul or last-mile to local carriers.

Turkey's third-party logistics market size growth in hybrid operations is supported by shippers that demand assured capacity during peak periods yet want variable pricing structures. Transporeon’s cloud platform now connects over 1,400 shippers and 150,000 carriers in Turkey, adding API integrations for status messaging and customs e-declaration. Blockchain pilots for transferable e-CMR documents may further reduce administrative latency, positioning hybrid 3PLs as trusted partners in end-to-end orchestration. ESG reporting requirements, especially Scope 3 emissions accounting under CBAM, will favor hybrids that combine owned low-carbon assets with access to green capacity suppliers, strengthening their competitive stance in the Turkey third-party logistics market.

Geography Analysis

Turkey's third-party logistics market activity is heaviest in the Marmara Region, which hosts 43% of the nation’s 216 coastal facilities and processes the majority of EU-bound Ro-Ro and container flows. Istanbul’s mega-city status concentrates omnichannel fulfillment centers, but land costs drive suburban relocation toward Çorlu and Gebze, where rail-linked inland container terminals cut drayage times by 30%. The ongoing Kemalpaşa Logistics Hub in Izmir addresses Aegean capacity gaps and is forecast to handle 4 million t annually when fully operational, broadening distribution reach to Mediterranean and Balkan customers.

Central Anatolia’s Konya corridor emerges as a strategic cross-dock node due to network intersectionality between north–south and east–west freight flows; capacity upgrades will raise annual tonnage to 1.679 million, supporting agri-bulk and construction materials traffic. Southeastern provinces gain traction from the Development Road Project that links Iraq’s Grand Faw Port via 1,200 km of highway and rail, potentially shifting Gulf transit cargo northward to Turkish ports and on to Europe. The Middle Corridor rail route through Kars avoids Black Sea bottlenecks, and government projections call for tripling throughput by 2030, bolstering the Turkey third-party logistics market size tied to Eurasian land-bridge trade.

The national rail grid measures 10,546 km, of which 51% is electrified and 14% double-tracked; urban bottlenecks near Ankara and Istanbul are being addressed by 5,600 km of high-speed lines planned for completion by 2025, cutting inter-city transit times by half. Coastal regions such as Mersin and Iskenderun benefit from new quay cranes and yard automation, augmenting Turkey third-party logistics market capacity for cold-chain citrus exports and steel imports. Free zones near Izmir, Antalya, and Samsun continue to attract value-added assemblers who require integrated 3PL services for bonded storage, kitting, and reverse logistics, thereby dispersing market growth beyond Istanbul.

Competitive Landscape

Turkey's third-party logistics market competition is moderate but trending toward higher concentration as multinationals seek domestic platforms. CEVA’s USD 440 million purchase of Borusan Tedarik doubled its warehouse footprint and added nearly 1 million annual domestic shipments, underscoring the appetite for scale. DHL’s acquisition of MNG Kargo places 27 automated sort centers and 800 branches under the German group, enhancing one-day delivery coverage and cross-border parcel synergies. Mars Logistics pursues vertical integration, funding EUR 70 million in new tractors while signing power-purchase agreements to run 100% electric rail services, which differentiates it on ESG compliance.

Technology adoption remains the central battlefield. Netlog’s SAP-TM platform timestamps every pallet movement, providing sellers with real-time ETA and carbon metrics; Turkish Cargo’s AI-driven ULD planning raises load factors on pharma lanes, while Transporeon’s lane-matching engine slashes spot tender time from 4 hours to 15 minutes. Cold-chain capability is the new white space: EBRD funding for Netlog, Çelebi’s IoT sensors, and warehouse retrofits for minus-40 °C blast freezing forecast robust entry barriers. Free-zone exemptions create cost advantages for 3PLs embedded in Mersin and Aliağa, though customs-rule volatility remains a strategic threat.

International entrants, from DFDS to InterRail, increase seaborne and rail capacity to convert near-shoring trade, forcing incumbent Turkish firms to widen service portfolios that now include duty paid/duty free inventory management, sustainability reporting, and chartering of specialized equipment. Asset-light challengers use digital freight platforms to aggregate return loads, but the top five 3PLs still command roughly 45% of gross revenue, suggesting ample room for both consolidation and niche specialization. ESG, digitalization, and cold-chain competencies will likely determine the winner’s circle in the Turkey third-party logistics market through 2030.

Turkey Third Party Logistics (3PL) Industry Leaders

CEVA Logistics

DHL International GmbH.

UPS

Schenker

DSV Panalpina

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CEVA Logistics completed the USD 440 million acquisition of Borusan Tedarik, adding 1.19 million m² of warehousing and boosting domestic shipments to nearly 1 million a year.

- May 2025: DHL Group agreed to acquire MNG Kargo, incorporating 27 sort centers and more than 800 branches to reinforce parcel capacity in Turkey and neighboring markets.

- May 2025: The European Bank for Reconstruction and Development extended a EUR 25 million loan to Netlog to scale temperature-controlled infrastructure for pharmaceuticals and perishables.

- January 2025: Transporeon launched its cloud Transportation Management Platform that links 1,400 shippers with 150,000 carriers.

Turkey Third Party Logistics (3PL) Market Report Scope

The Turkey Third-Party Logistics (3PL) Market, covering the current market trends, restraints, technological updates and detailed information on various segments and competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the current value of the Turkey third-party logistics market?

It is valued at USD 10.32 billion in 2026 and is expected to reach USD 12.28 billion by 2031.

Which service segment generates the most revenue?

Domestic Transportation Management leads with 40.62% market share, supported by an extensive national road network.

Which end-user group will grow the fastest through 2031?

Life Sciences & Healthcare is forecast to expand at a 6.97% CAGR during 2026-2031 due to rising pharma production and cold-chain upgrades.

How are acquisitions affecting competition?

High-profile deals such as CEVA–Borusan and DHL–MNG Kargo are enlarging warehouse footprints and accelerating market concentration.

What infrastructure projects will influence logistics flows?

The Development Road Project linking Iraq’s Grand Faw Port to Turkey and the national program for 25 logistics centers will reshape trade corridors.

How will EU carbon rules impact Turkish 3PLs?

Compliance with the Carbon Border Adjustment Mechanism could add EUR 138 million in annual costs by 2027, prompting investment in low-carbon fleets and rail services.

Page last updated on: