Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

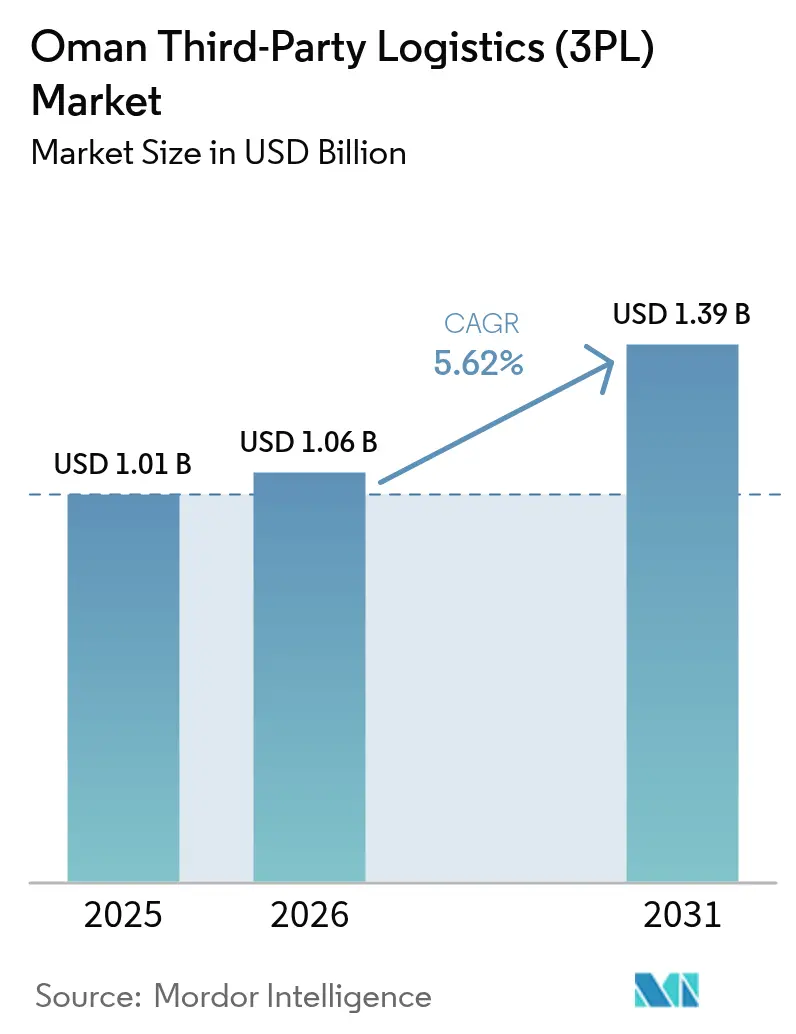

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

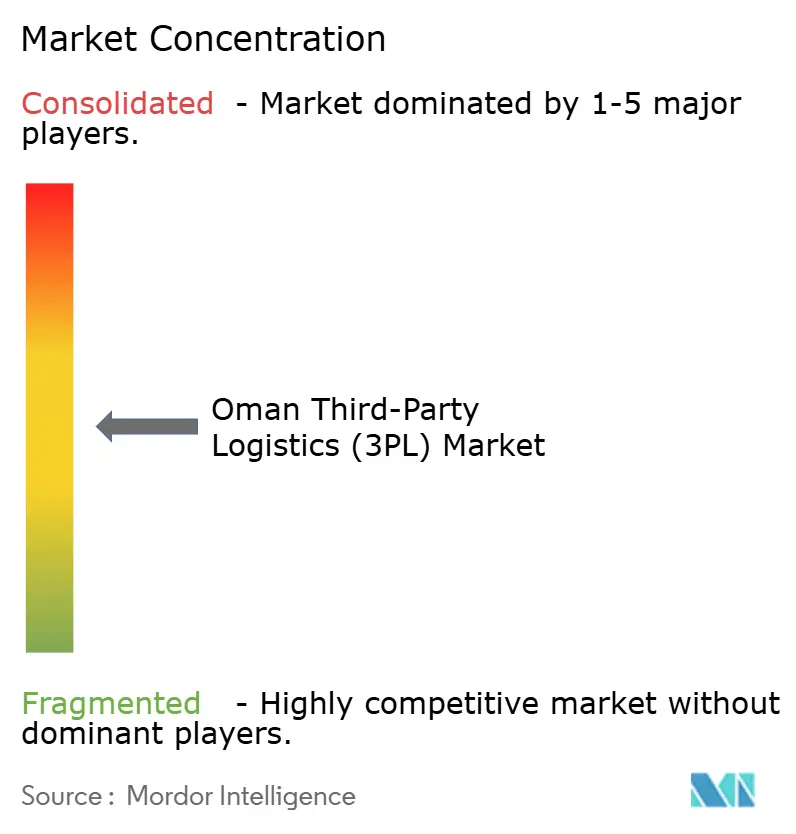

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The Oman third-party logistics (3PL) market size is expected to grow from USD 1.01 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.39 billion by 2031 at a 5.62% CAGR over 2026-2031.

Rapid port throughput gains at Salalah and Sohar, the rollout of Bayan Next customs automation, and a USD 3 billion rail link that connects Sohar Port with the UAE are reshaping freight flows and lifting service sophistication. Petrochemical mega-projects in Sohar and Duqm convert the Sultanate from a pure transshipment stop into an origin-destination node that demands hazmat storage, project cargo handling, and ISO-tank operations. Expatriate population growth back to 1.78 million residents in 2024 strengthens FMCG volumes, while bonded e-fulfillment hubs at Duqm and Salalah siphon Africa-bound parcels away from traditional Dubai routing. Competitive intensity rises as bunker fuel volatility, Omanisation wage premiums, and scarce green warehousing squeeze margins, forcing providers to automate and differentiate via certifications.

Key Report Takeaways

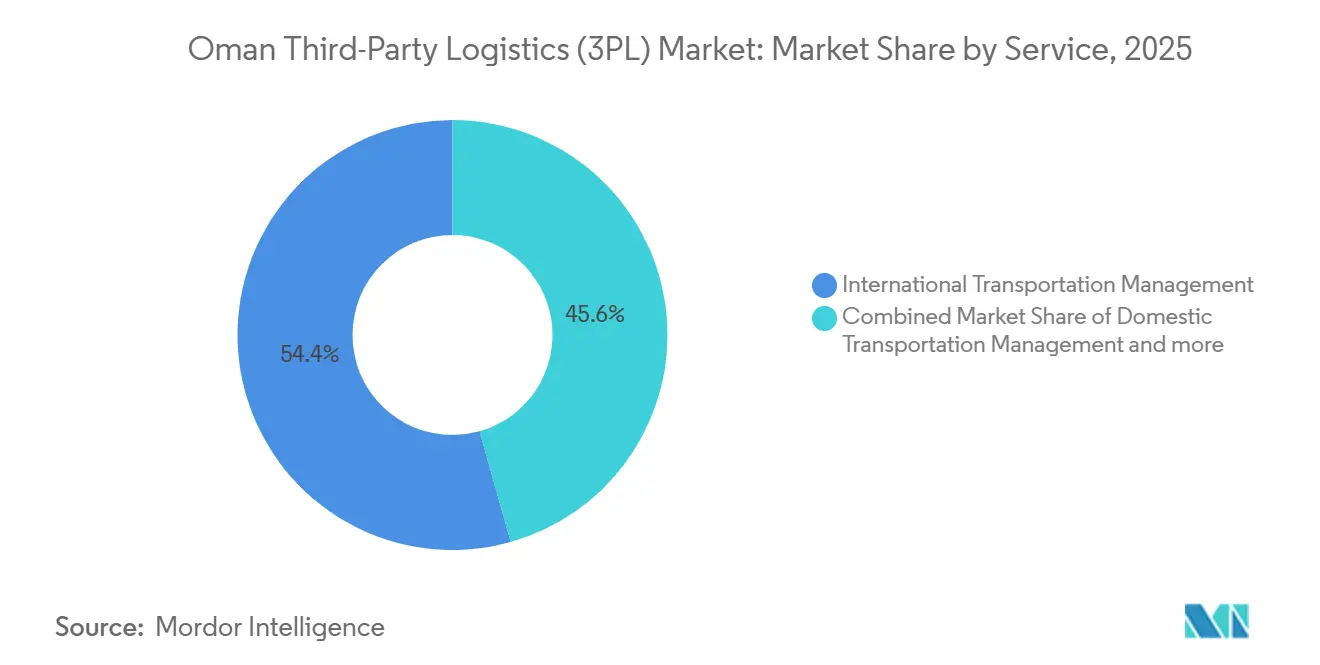

- By service type, international transportation management led with 54.37% of the Oman third-party logistics (3PL) market share in 2025, while value-added warehousing and distribution is forecast to advance at a 7.61% CAGR through 2031.

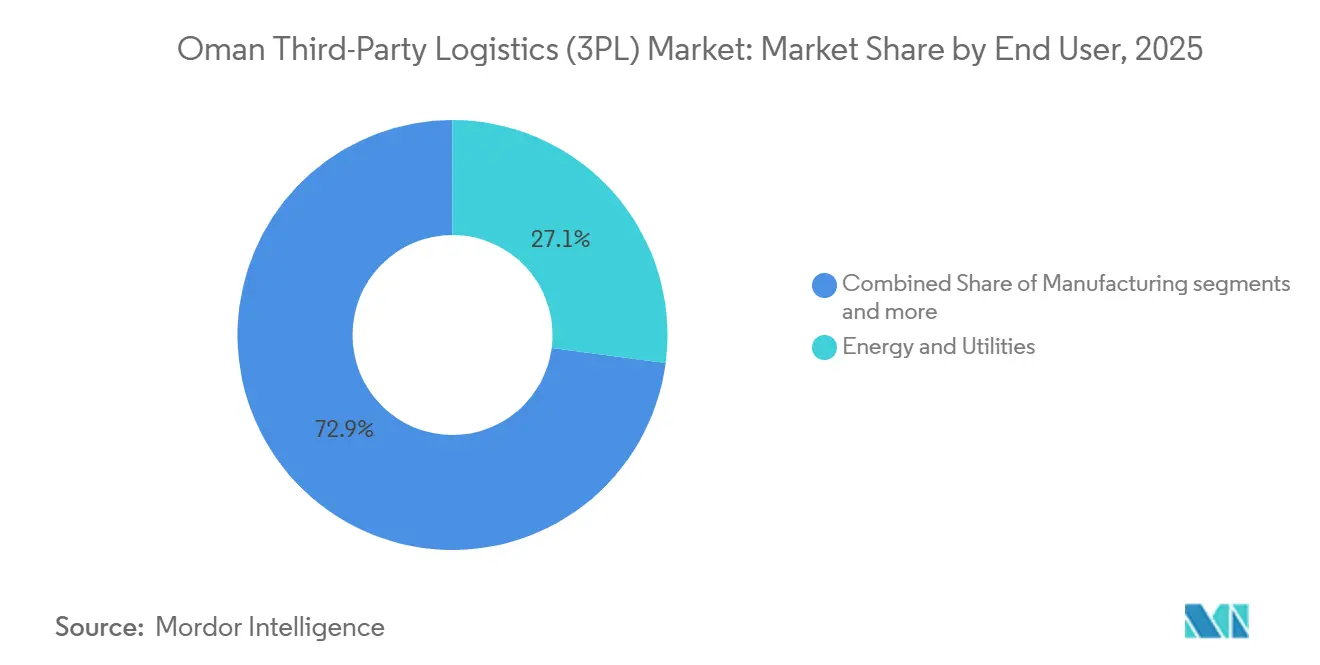

- By end user, energy and utilities held 27.08% of the Oman third-party logistics (3PL) market size in 2025; e-commerce records the fastest trajectory at a 7.95% CAGR to 2031.

- By logistics model, asset-light providers commanded 51.33% of the Oman third-party logistics (3PL) market share in 2025, whereas hybrid models were expected to grow the quickest at 6.48% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep-water port trans-shipment growth (Sohar, Duqm, Salalah) | +1.3% | National ports with concentration in Salalah and Duqm | Medium term (2-4 years) |

| Rebound in FMCG demand from expatriate population expansion | +0.8% | National, concentrated in Muscat, Sohar, and Salalah urban clusters | Short term (≤ 2 years) |

| Oman Rail–Etihad Rail corridor enabling road-rail intermodal flows | +1.1% | Sohar-Buraimi corridor with extension to Duqm by 2032 | Long term (≥ 4 years) |

| Downstream petrochemical mega-projects are boosting project logistics | +0.9% | Sohar Port and Freezone, Duqm Refinery complex | Medium term (2-4 years) |

| Nationwide roll-out of Bayan Next electronic cargo community system | +0.6% | National, all customs entry points and ports | Short term (≤ 2 years) |

| Bonded e-fulfilment hubs targeting Africa-bound cross-dock trade | +0.7% | Duqm and Salalah free zones with Africa maritime connectivity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Deep-Water Port Trans-Shipment Growth Anchors Regional Connectivity

Salalah, Sohar, and Duqm handled a combined 8.2 million TEUs in 2024, positioning Oman as the GCC’s third-largest container gateway. Salalah alone moved 3.96 million TEUs, up 22% year over year, thanks to services that bypass the Strait of Hormuz. Duqm’s 2,200-meter quay now accepts six ULCCs simultaneously, while Sohar posted 77% growth in general cargo on the back of break-bulk demand. Trans-shipment volumes translate into USD 180-220 per TEU in ancillary inland revenue for 3PLs. As carrier alliances rationalize routings, the Oman third-party logistics market benefits from consistent feeder calls and greater demand for customs brokerage, temporary warehousing, and repositioning moves[1].National Centre for Statistics and Information, “Population Statistics,” data.gov.om

Expatriate Population Rebound Revitalizes FMCG Networks

Expatriates climbed back to 1.78 million in 2024 after pandemic contractions, with 42% concentrated in Muscat. These residents spend 35-40% more per capita on packaged goods than nationals, pushing organized retail chains such as Lulu and Carrefour to add 20 new outlets in 2024-2025. Retail expansion drives daily cold-chain replenishment and elevates SKU complexity. Bayan Next’s six-hour clearance window lets FMCG 3PLs pre-position imports, shaving inventory days. Consequently, the Oman third-party logistics market absorbs new multi-temperature cross-docks and contract-packing lines that raise service margins.

Oman Rail-Etihad Rail Corridor Unlocks Multimodal Efficiencies

The 303 km Sohar-Buraimi rail spine, operational by 2030, enables double-stack 120 km/h container trains that cut transit times to UAE hubs by 40% and trim per-ton-kilometer costs by up to 32%. Phase 2 will extend to Duqm by 2032, funneling mineral exports and project cargo. 3PLs gain rail-road service offerings that de-risk fuel-price shocks and curb CO₂ by 65% versus diesel trucking. New intermodal yards at Sohar, Ibri, and Duqm spawn value-added opportunities such as container stuffing, cross-docking, and bonded storage, expanding the Oman third-party logistics (3PL) market beyond coastal corridors.

Petrochemical Mega-Projects Generate Specialized Demand

USD 6.8 billion of petrochemical complexes approved in 2024 add 4.2 million tpa capacity in Sohar, including methanol-to-olefins and aromatics units. Construction mobilizes 180-220 daily heavy-lift moves that require 800-ton cranes and route surveys. During operations, ISO-tank rotations, hazmat warehousing, and bulk-liquid terminals drive recurring logistics spend of USD 45-55 per ton, triple crude oil intensity. As projects ramp up, the Oman third-party logistics (3PL) market attracts operators certified for dangerous goods and project cargo engineering.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile bunker fuel surcharges are compressing 3PL margins | -0.9% | National, affecting ocean freight and coastal shipping operations | Short term (≤ 2 years) |

| Mandatory localisation quotas are elevating labour cost base | -0.7% | National, concentrated in urban logistics hubs | Medium term (2-4 years) |

| Scarcity of Grade-A solar-ready warehousing for ESG-focused clients | -0.5% | Muscat, Sohar, and Salalah industrial zones | Medium term (2-4 years) |

| Rising cyber-risk insurance premiums after GCC port ransomware events | -0.3% | National, affecting digitally-integrated logistics operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Bunker Fuel Surcharges Erode Ocean Freight Margins

Spot bunker surcharges swung between USD 150-280 per TEU in 2024-2025, pulling 120-180 basis points from integrator profitability. Small regional carriers lack hedging tools, while surcharge pass-through lags 30-45 days, exposing 3PLs on fixed contracts. IMO 2020 rules added USD 180-220 per ton for LSMGO, and limited bunkering options inside Oman force deviations to Fujairah. With Maersk introducing USD 50-75 green-vessel surcharges from 2026, the Oman third-party logistics (3PL) market’s margin volatility intensifies until carriers secure alternative fuels.

Omanisation Mandates Elevate Labor Cost Structures

Logistics firms must lift national employment to 30% by 2026 or risk permit curbs. Omani salaries stand 35-45% above expatriate equivalents and raise the sector’s wage bill 18-22%. Providers invest in training academies. GAC’s 18-month program graduated 47 nationals in 2024, yet new hires need up to nine months to reach productivity benchmarks. Higher payroll and onboarding costs dilute cash flow, nudging the Oman third-party logistics market toward automation and shared-services hubs to protect operating margins.[2]Ministry of Labour, Oman, “Omanisation Requirements,” mol.gov.om

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: International routes underpin current revenue strength

The Oman third-party logistics (3PL) market size in 2025 shows international transportation management holding 54.37% market share, while value-added warehousing and distribution is forecast to grow at 7.61% CAGR through 2031. Automated systems at facilities such as Asyad’s Sohar site lift picks per hour fourfold, attracting FMCG and e-commerce accounts. International transportation management remains a dominant segment, though its growth moderates as carriers consolidate rotations. The market now prizes multi-temperature storage, kitting, and postponement services, reflecting a shift toward value-added offerings.

Domestic transportation management remains constrained by dispersed demand centers and empty backhauls. Rail commissioning after 2030 is expected to cut trunk-haul prices and improve slot reliability, supporting palletized food and building-material flows. Airfreight continues as a niche option, providing a viable express solution for life sciences and electronics shippers. As value-add services deepen, service providers see EBITDA margins widen above pure trucking averages, reinforcing the structural pivot within the Oman third-party logistics (3PL) market.

By End-User Industry: E-Commerce Disrupts Traditional Hierarchies

Energy and utilities controlled 27.08% of the Oman third-party logistics market size in 2025 through crude, LNG, and pipeline spares flows. In contrast, e-commerce revenues rise 7.95% CAGR on 95% internet penetration and digital-payment mandates that slash cash on delivery to 34%. Noon and Asyad Express manage 15,000 daily Muscat orders, illustrating two-day fulfillment expectations.

Retail and FMCG logistics widen through modern-trade growth to 58% of FMCG sales by 2026. Agriculture self-sufficiency goals add cold-chain runs from Al Batinah farms to urban grocers. Collectively, these shifts intensify SKU velocity and reinforce omnichannel demands across the Oman third-party logistics (3PL) market[3].International Trade Administration, “Oman – eCommerce,” trade.gov

By Logistics Model: Hybrid Strategies Gain Momentum

Asset-light operators held 51.33% of Oman third-party logistics (3PL) market share in 2025, thanks to brokered fleet access and variable cost structures. Yet hybrid models mixing owned cold-chain rigs with outsourced general cargo grow 6.48% CAGR. Kuehne+Nagel’s Muscat pharma hub shows why: validated temperature spaces require ownership, but non-critical consignments ride subcontracted trucks. Asset-heavy providers struggle with 35-45% seasonality gaps that idle cranes and reefers from June-August.

Solar-ready warehouses highlight ownership advantages. Al Madina’s 2.1 MW rooftop array recoups cost in 3.2 years and wins 8-12% price premiums from ESG-minded shippers. Yet most players balance 25-35% owned assets with 65-75% brokered capacity to hedge utilization swings, a pattern now defining competitive fitness inside the Oman third-party logistics (3PL) market.

Geography Analysis

Muscat’s capital corridor houses 38% of national warehousing demand and 45% of last-mile volumes, anchored by 1.6 million residents and half of retail expenditure. Still, Sohar’s port-adjacent freezone outpaces it with 77% 2024 cargo growth, fueled by USD 6.8 billion petrochemical inflows. The Al Batinah North logistics economy policy fast-tracks land leases and utilities, luring 3PLs to purpose-built parks.

Duqm Special Economic Zone represents the fastest-expanding cluster, offering indefinite bonded storage and Africa-centric cross-dock privileges. Aramex processes 120,000 daily parcels through its 45,000 m² Salalah freezone hub, shaving three days off Nairobi deliveries. Salalah’s isolation, 1,000 km south of Muscat, nonetheless secures 3.96 million TEUs and 14 direct Africa feeders, a cornerstone for transshipment-driven revenue within the Oman third-party logistics (3PL) market[4] Port of Duqm, “Port Overview,” portduqm. om.

The 303 km railway will re-map inland flows, with intermodal depots at Ibri and Adam creating new demand nodes in Al Dhahirah and Al Dakhliyah. These interior governorates presently lack Grade-A cold-chain footprints, depending on small distributors. Road upgrades and the rail Phase 2 spur to Duqm by 2032 will integrate hinterland produce into export corridors, enlarging domestic legs inside the Oman third-party logistics market.

Competitive Landscape

Top players CEVA Logistics, DHL Supply Chain, Aramex, Kuehne+Nagel, and Asyad Express control roughly 38% of revenue, signalling moderate concentration. Asyad’s port, rail, and fleet assets underpin public-sector contracts, while the 2025 plan to float 20% of Asyad Shipping introduces market-based discipline.

DHL commits USD 570 million Gulf-wide for robotics and bonded hubs, allocating USD 85 million to a Duqm pharma and electronics center. Differentiation leans on certifications. Providers with GDP, IMO hazmat, or LEED Gold sites secure sticky verticals and eight-point price premiums. Al Madina’s solar-powered warehouse exemplifies ESG traction.

Bonded Africa e-fulfillment, project logistics for green hydrogen plants, and temperature-controlled healthcare networks remain white-space arenas. Technology adoption is uneven; leaders deploy WMS, TMS, and IoT fleets, but many SMEs still plan via spreadsheets, creating 40-55% productivity gaps and widening capability rifts inside the Oman third-party logistics market.

Oman Third-Party Logistics (3PL) Industry Leaders

DHL Supply Chain

Asyad Express

Al Madina Logistics

Aramex

CEVA Logistics (CMA CGM Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL expanded its airside logistics capacity in Oman by investing about EUR 30 million (USD 34.67 million) in new facilities and increased flight connectivity (including near-daily Bahrain flights) to boost export capacity and supply-chain connectivity.

- December 2025: Asyad Express partnered with global brands including Amazon, ASOS, and Landmark Group to enhance cross-border e-commerce logistics and last-mile delivery across Oman, GCC, and MENA markets.

- September 2025: Aramex partnered with Bank Muscat and Asyad Group to provide secure logistics and courier delivery services for banking cards across Oman, improving last-mile delivery and customer service efficiency.

- May 2025: Al Madina Logistics signed an agreement with Global Laboratories and Testing LLC to establish an advanced import-export testing facility at Sohar Port and Freezone, improving logistics compliance and trade facilitation.

Oman Third-Party Logistics (3PL) Market Report Scope

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy and Utilities |

| Manufacturing |

| Life Sciences and Healthcare |

| Technology and Electronics |

| E-commerce |

| Consumer Goods and FMCG |

| Food and Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet and Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy and Utilities | ||

| Manufacturing | ||

| Life Sciences and Healthcare | ||

| Technology and Electronics | ||

| E-commerce | ||

| Consumer Goods and FMCG | ||

| Food and Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet and Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the current size of the Oman third-party logistics market?

The Oman third-party logistics market size stands at USD 1.01 billion in 2025 and is set to reach USD 1.39 billion by 2031.

Which segment is growing fastest within Omani 3PL services?

Value-Added Warehousing & Distribution leads growth at a 7.61% CAGR as shippers seek kitting, labeling, and bonded storage.

How will the Oman–UAE rail link affect logistics costs?

The 303 km corridor is expected to cut per-ton-kilometer costs by up to 32% and shorten transit times by 40%.

Why are hybrid logistics models gaining ground in Oman?

Shippers need dedicated cold-chain and hazmat assets yet demand cost-flexibility, making hybrid models the optimal balance.

What challenges limit 3PL profit margins in Oman?

Fuel surcharge volatility and higher payroll under Omanisation mandates together shave up to 180 basis points from margins.

Which ports anchor Oman's transshipment strategy?

Salalah, Sohar, and Duqm handle more than 8 million TEUs combined, serving Asia–Europe–Africa trade lanes.

Page last updated on: