Middle East EV Dealership Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

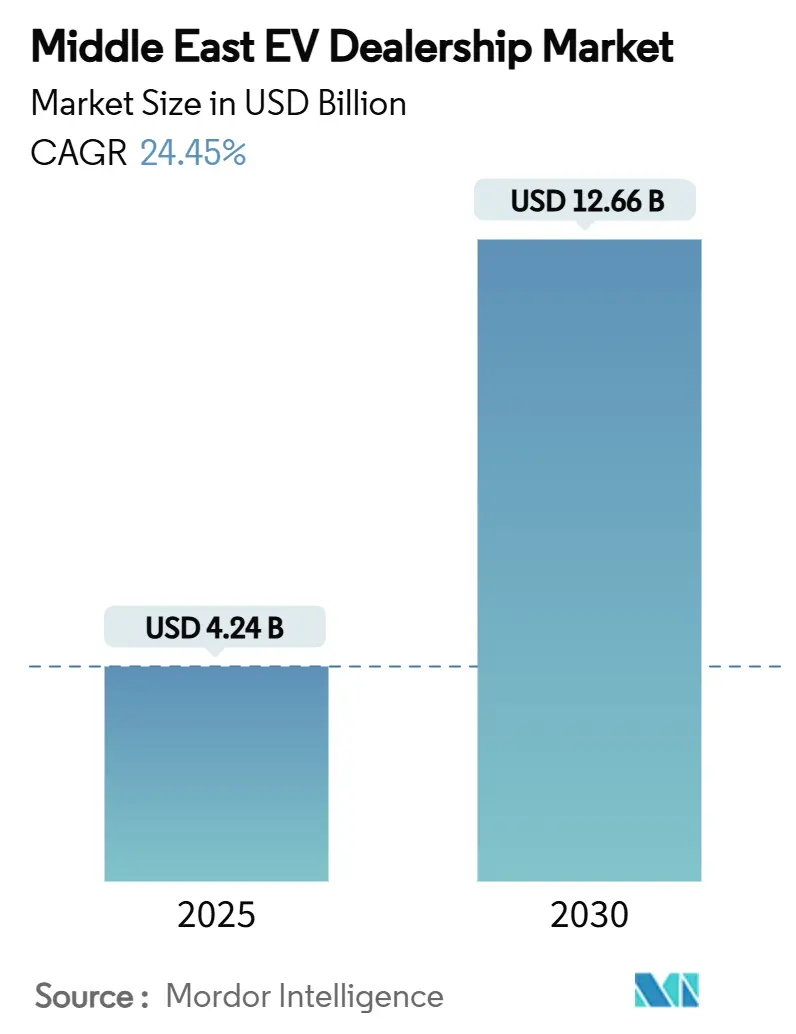

| Market Size (2025) | USD 4.24 Billion |

| Market Size (2030) | USD 12.66 Billion |

| Growth Rate (2025 - 2030) | 24.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East EV Dealership Market Analysis by Mordor Intelligence

The Middle East EV dealership market size was valued at USD 4.24 billion in 2025 and is forecasted to expand to USD 12.66 billion by 2030 at a 24.45% CAGR. Fueled by sovereign investment funds, vision-driven mandates, and rapid charging-network rollouts, the Middle East EV dealership market is rapidly transitioning from pioneer to early-mass-adoption phase. Government incentives underpin demand floors, while OEM–dealer joint ventures localize assembly capacity and shorten lead times. Digital sales channels grow quickly, but physical showrooms remain crucial for education and after-sales support. Fragmented competition, coupled with unique climate challenges, creates opportunities for retailers capable of offering heat-resilient battery warranties and integrated charging services.

Key Report Takeaways

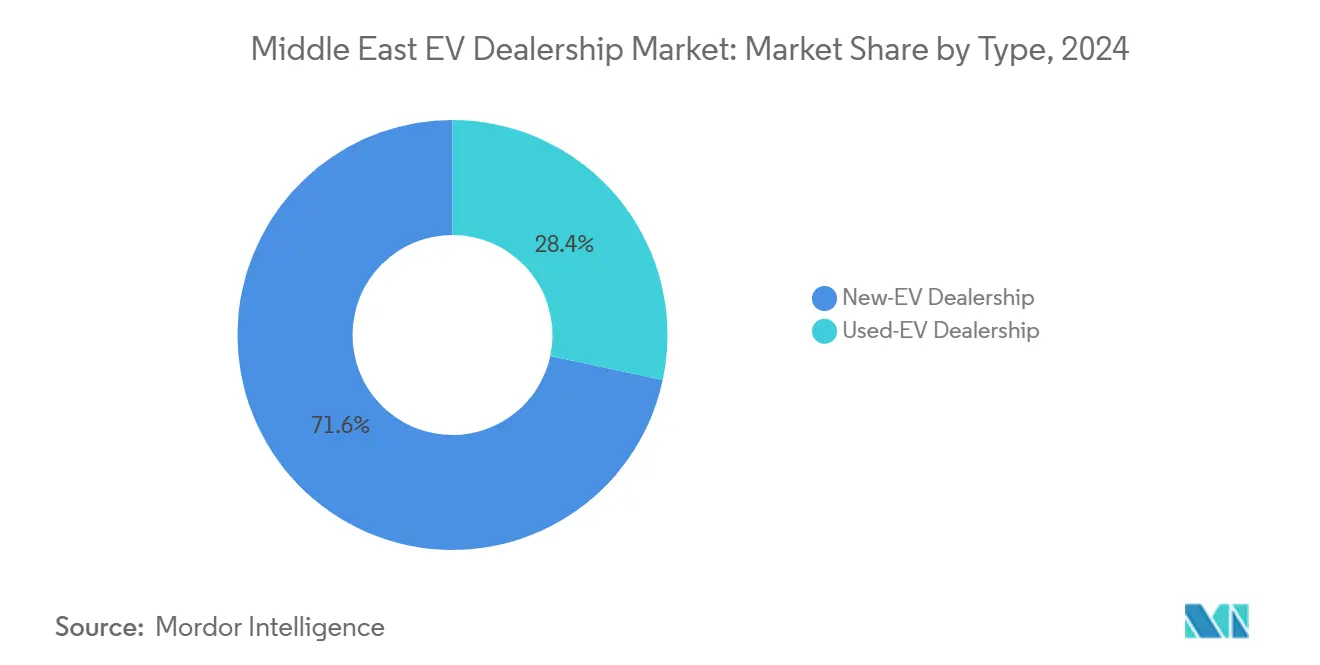

- By type, new-EV dealerships led with 71.64% of the Middle East EV dealership market share in 2024; used-EV dealerships are projected to advance at a 29.44% CAGR through 2030.

- By retailer, franchised networks controlled 66.52% of the Middle East EV dealership market share in 2024, while non-franchised platforms are set to expand at a 33.36% CAGR to 2030.

- By vehicle type, passenger electric cars accounted for 83.92% of the Middle East EV dealership market size in 2024; commercial EVs are growing at a 32.32% CAGR between 2025-2030.

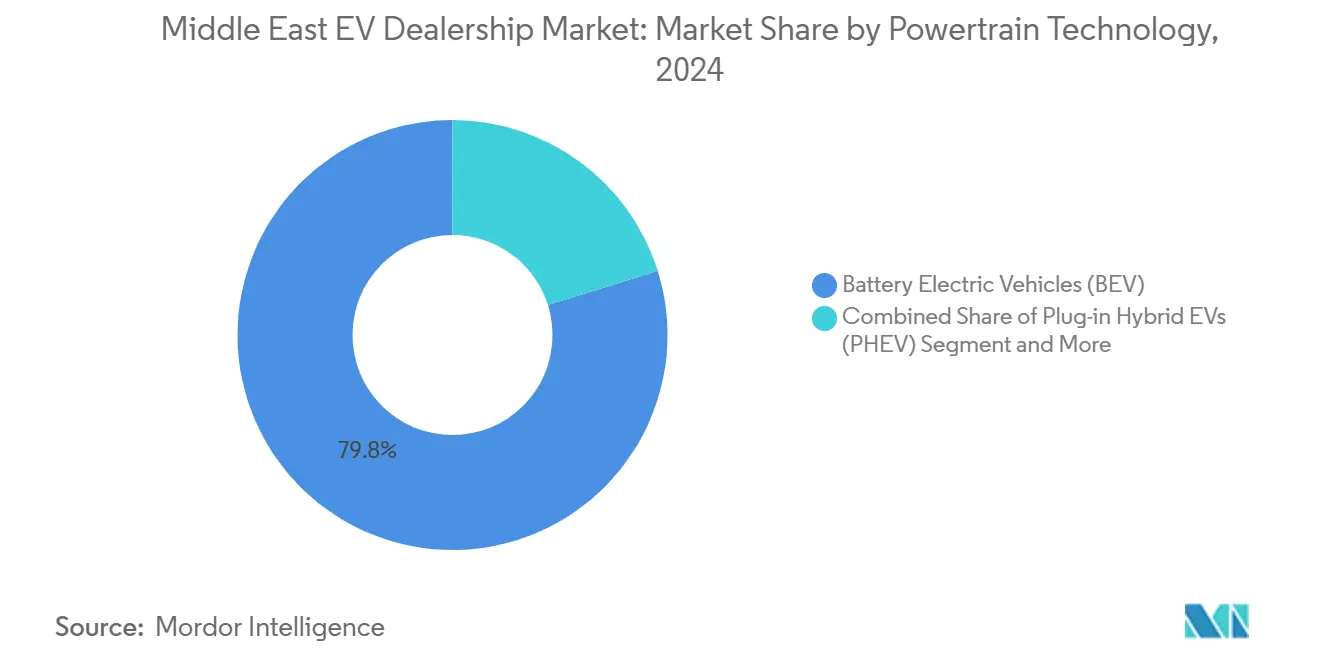

- By powertrain technology, BEVs captured 79.83% of the Middle East EV dealership market share in 2024, whereas FCEVs are expected to exhibit the highest 40.66% CAGR outlook to 2030.

- By sales channel, brick-and-mortar showrooms retained 77.78% of the Middle East EV dealership market share in 2024; online platforms are climbing at a 33.36% CAGR through 2030.

- By country, Saudi Arabia dominated with a 47.08% share in 2024; the UAE is expected to post the fastest 35.45% CAGR through 2030.

Middle East EV Dealership Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Focused Fiscal Incentives | +5.2% | Saudi Arabia, UAE, Qatar, Egypt | Long term (≥ 4 years) |

| Investment in Ultra-Fast Chargers | +3.8% | Saudi Arabia, UAE, Kuwait, Bahrain | Medium term (2-4 years) |

| JV Model for Local EV Assembly | +3.5% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| EV-Friendly Fleet Tenders Surge | +2.9% | UAE, Qatar, Saudi Arabia, Jordan | Short term (≤ 2 years) |

| Grey-Market Risk | +1.8% | UAE, Saudi Arabia, Kuwait, Oman | Medium term (2-4 years) |

| Heat-Resilient Battery Warranties | +1.3% | Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government EV-Focused Fiscal Incentives and Vision-Driven Mandates

Cash rebates in Egypt and Jordan’s EV tax rates create structural demand floors that stabilize dealer revenue streams[1]“National Electric Vehicles Policy,” UAE Government, u.ae. Mandates such as Saudi Arabia’s requirement that 30% of Riyadh vehicles be electric by 2030 compel dealerships to shift inventory toward zero-emission models. Long-range policy visibility under the UAE National Electric Vehicles Policy enables retailers to justify charging bays and technician training investments. Qatar’s plan for eco-friendly public transportation by 2030 expands government fleet opportunities. Yet, fiscal-budget pressures may cause incentive reductions that threaten volume forecasts if dealerships remain overly subsidy-dependent.[2]"Saudi Arabia’s Automotive Industry: Progress Towards Becoming a Regional Hub", The Saudi Press Agency (SPA), spa.gov.sa

Rapid Public-Private Investment in Ultra-Fast Charging Corridors

Saudi Arabia’s EVIQ program targets 5,000 fast chargers by 2030, while the UAE plans 70,000 charge points, shrinking range anxiety and enlarging dealership catchment areas[3]“EV Green Charger Initiative,” Dubai Electricity and Water Authority, dewa.gov.ae. Dealerships situated near charging hubs enjoy higher foot traffic and can bundle charging subscriptions with vehicle sales. Partnerships with utilities allow dealers to share charging-fee revenue, diversifying income beyond car margins. Standardized regulations in Abu Dhabi reduce technical complexity for retailers deploying chargers. However, the capital intensity of infrastructure favors well-funded incumbents and may accelerate consolidation.

OEM–Dealer JV Model for Local EV Assembly

OEM-dealer joint ventures are now assembling EVs locally, bolstering competitive advantages for dealerships and diminishing the region's historical reliance on imports. Lucid’s “Made in Saudi” certification and Ceer’s local-content agreements illustrate how joint ventures lock in government procurement preference and speed inventory turnarounds. Assembly proximity lets dealers offer GCC-climate adaptations such as enhanced cooling systems. Egypt’s automotive strategy signals similar localized opportunities. Capital demands, though, may exclude smaller operators, creating a two-tier dealership ecosystem.

Surge in EV-Friendly Fleet Tenders

EV dealerships are reaping the benefits of predictable, high-volume revenue streams, thanks to government mandates pushing fleet electrification. Dubai’s 30% government-fleet electrification goal and Qatar’s eco-public transportation drive generate large, multi-year contracts. These deals produce recurring service and parts revenue that smooths dealership cash flow. Last-mile delivery electrification multiplies commercial-vehicle demand. Yet fleet tenders yield thinner unit margins and lengthy payment cycles, challenging dealers’ working-capital management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Charging Infrastructure | -2.1% | Jordan, Lebanon, Egypt, Turkey, Oman | Medium term (2-4 years) |

| Premium EV Pricing Vs. ICE Parity | -1.7% | Lebanon, Jordan, Egypt, Turkey | Long term (≥ 4 years) |

| Technician and Parts Skills Gap | -1.2% | Saudi Arabia, UAE, Kuwait, Bahrain, Qatar, Oman | Medium term (2-4 years) |

| Import-Driven Lead-Time Volatility | -0.9% | UAE, Saudi Arabia, Qatar, Kuwait, Bahrain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sparse Charging Infrastructure in Secondary Cities

Primary metropolitan areas such as Amman and Cairo dominate the charging infrastructure landscape, imposing geographic constraints on EV dealerships. As a result, these dealerships face hurdles when trying to expand into secondary cities. The lack of infrastructure in these secondary locales not only diminishes sales potential but also complicates efforts to attract customers. Consumers outside major hubs face service-access hurdles, curbing dealership aftermarket income. Government retrofit programs are still embryonic, so retailers cannot scale footprints efficiently across national territories.

Premium Upfront EV Pricing Vs. ICE Parity

Higher sticker prices hinder adoption among price-sensitive buyers in Egypt and Jordan. Limited battery-lease or total-cost-of-ownership financing pushes shoppers to prioritize upfront cost, where ICE vehicles remain cheaper. Uneven tariff regimes distort segment profitability across commercial and passenger categories, complicating dealer pricing strategies. As battery costs decline toward parity post-2027, dealerships must emphasize operating-cost savings to bridge the interim affordability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: New-EV Dominance Drives Market Foundation

New-EV dealerships captured 71.64% of the Middle East EV dealership market share in 2024, underscoring the early-adoption stage where first-time buyers dominate transactions. OEM support programs, extended warranties, and attractive financing make new vehicles the default option for affluent urban consumers. Lucid’s local assembly in Saudi Arabia shortens delivery cycles and allows dealerships to offer GCC-specific customizations that build trust. Inventory depth in flagship showrooms across Riyadh and Dubai reinforces the perception that electric mobility is now mainstream rather than niche. These factors collectively anchor dealership profitability even as competitive intensity rises.

While smaller, the used-EV channel is advancing at a 29.44% CAGR and will meaningfully expand the Middle East EV dealership market size through 2030. Certified-pre-owned programs and battery-health guarantees reduce residual-value anxiety, drawing price-sensitive buyers who previously opted for ICE cars. Regulatory bans on written-off imports in the UAE and quality inspections at Jordan’s free zones elevate consumer confidence, stimulating trade-in activity that feeds used-vehicle inventory. Digital marketplaces streamline discovery and financing, widening geographic reach beyond traditional dealer footprints.

By Retailer: Franchised Networks Face Digital Disruption

Franchised retailers held 66.52% of the Middle East EV dealership market share in 2024 thanks to OEM-backed technician training, parts pipelines, and compliance expertise. Exclusive brand rights enable coordinated marketing campaigns and volume rebates that protect margins despite rising competition. Centralized service centers certified for high-voltage repairs create customer stickiness not easily replicated by smaller independents. Government fleet tenders often mandate franchised bidders, further reinforcing the channel’s dominance. These structural advantages give franchised groups the scale needed to co-invest in charging hubs and showroom retrofits.

Non-franchised platforms are scaling at a 33.36% CAGR, capturing buyers who prefer transparent online pricing and doorstep delivery, a shift that enlarges the Middle East EV dealership market size. Lower overhead and agile inventory sourcing let these retailers undercut traditional markups, particularly on high-volume Chinese brands. Partnerships with third-party service providers, mobile mechanics, and subscription-based maintenance plans close after-sales gaps that once hindered credibility. As omnichannel habits solidify, franchised and non-franchised models are converging around hybrid retail journeys blending digital research with showroom validation.

By Vehicle Type: Commercial Segment Emerges as Growth Engine

Passenger electric cars commanded 83.92% of the 2024 Middle East EV dealership market size, benefiting from consumer incentives and growing model variety across hatchback, sedan, and SUV categories. Cash rebates in Egypt and reduced import duties in Jordan lower acquisition costs enough to sway mainstream shoppers. Wide public-charger coverage in the UAE simplifies daily use cases, reinforcing adoption among city commuters. High social visibility of early adopters further normalizes EV ownership and accelerates word-of-mouth referrals. Dealerships leverage test-drive events and bundled home-charger offers to convert interest into sales.

Commercial EVs, although a minority today, are accelerating at a 32.32% CAGR and will gradually chip away at the passenger-car lead within the Middle East EV dealership market share. Government procurement of electric buses and taxis provides anchor contracts that validate performance and resale values. Fleet operators favor EVs for predictable operating costs, enabling dealers to pitch total-cost-of-ownership savings rather than sticker-price comparisons. Service contracts, telematics subscriptions, and bulk-charging solutions create recurring revenue streams that smooth earnings volatility. Retailers investing early in fleet-management expertise position themselves to capture this high-growth, higher-margin segment.

By Powertrain Technology: Hydrogen Emerges Despite BEV Dominance

Battery Electric Vehicles (BEVs) occupied 79.83% of the 2024 Middle East EV dealership market share, supported by falling battery costs and increasingly dense charging corridors. OEM line-ups span micro-cars to premium SUVs, giving dealers a broad price ladder to address diverse budgets. Quick charging times below 30 minutes at 350-kW stations in Saudi Arabia alleviate range anxiety for inter-city drivers. Utility incentives for home chargers further drive BEV penetration among suburban households. This ecosystem effect cements BEVs as the default choice for most private buyers.

Fuel-Cell Electric Vehicles (FCEVs) post the highest 40.66% CAGR outlook, adding optionality to the Middle East EV dealership market size as hydrogen refueling stations roll out along freight corridors. Low refuel times and long driving ranges appeal to logistics fleets and government agencies operating in hot desert climates where battery thermal management is complex. Sovereign investments in green hydrogen production lower projected fuel costs, improving lifetime economics. Early dealer participation through pilot leases builds servicing know-how ahead of wider market adoption. Plug-in Hybrids act as transitional offerings yet remain niche due to maintenance complexity and fewer policy incentives.

By Sales Channel: Digital Transformation Accelerates

Brick-and-mortar showrooms still generate 77.78% of the 2024 Middle East EV dealership market share because high-value purchases benefit from tactile inspection, test drives, and personal consultation. Flagship stores in malls and auto megacities double as brand-experience centers, educating first-time buyers about charging etiquette and warranty coverage. In-house finance desks expedite credit approvals, reducing abandonment rates common in purely digital journeys. Service bays staffed with EV-certified technicians drive repeat visits for battery health checks and software updates. These physical touchpoints create community hubs that bolster brand loyalty.

Online platforms, expanding at a 33.36% CAGR, are enlarging the Middle East EV dealership market size by removing geographic barriers and compressing transaction timelines. AI-driven configurators allow shoppers to visualize total-cost-of-ownership scenarios, addressing upfront price concerns in real time. End-to-end e-commerce flows integrate trade-in valuation, financing approval, insurance, and registration, delivering vehicles to doorsteps within days. Compliance with GCC VIN-upload regulations is automated through secure APIs, turning a potential bottleneck into a seamless back-office routine. As connectivity improves and consumer trust grows, leading dealers blend virtual storefronts with concierge delivery and mobile servicing for an omnichannel experience that satisfies all demographics.

Geography Analysis

Saudi Arabia accounted for 47.08% of the 2024 market value, underpinned by Vision 2030 mandates and Public Investment Fund backing for local assembly plants with a yearly capacity of 155,000 vehicles. Strong sovereign funding de-risks infrastructure projects and accelerates dealership rollout across Riyadh, Jeddah, and Dammam clusters. Inventory advantages from domestic manufacturing curb import-related delays and reduce logistics costs, bolstering dealer margins.

The UAE is the fastest-growing territory, charting a 35.45% CAGR through 2030 as its National Electric Vehicles Policy targets 50% adoption and finances 70,000 public charge points. High per-capita income and favorable loan terms lift consumer affordability, while tourism-linked rental fleets create additional volume. Qatar, Kuwait, and Bahrain form a second-tier growth arc where government-fleet electrification goals secure baseline demand, yet smaller populations necessitate multi-country dealership strategies.

Levant markets display heterogeneous dynamics. Jordan enjoys robust Chinese-brand penetration under 10% EV tax rates, whereas Lebanon’s economic constraints slow uptake. Egypt’s EGP 50,000 incentive bolsters Cairo-Alexandria sales, but charging-network scarcity in secondary cities restrains nationwide expansion. Turkey’s manufacturing base offers export potential, yet currency volatility dampens immediate dealership investment. Oman’s proximity to UAE charging corridors supplies growth spillover, but political stability and income levels will determine long-term scalability.

Competitive Landscape

The Middle East EV dealership market exhibits fragmented competition, creating white-space opportunities for new entrants and consolidation potential as the market matures toward higher concentration ratios typical of automotive retail. The remainder is split among regional conglomerates and emerging digital platforms. Joint-venture assembly deals, such as Lucid’s Saudi partnership, illustrate how supply-chain integration can vault newcomers into meaningful share positions quickly.

Strategic patterns emphasize technology integration and service differentiation. Leaders invest in ultra-fast chargers, mobile maintenance vans, and technician certification programs aligned with GCC heat-resilience requirements. Digital investments, ranging from AI-based inventory planning to immersive online configurators, help incumbents counter pure-play e-commerce entrants.

International OEMs increasingly choose local partners for speed-to-market. Recent tie-ups between VinFast and Al Tayer Motors, and XPeng with AG Auto, underscore the value of entrenched distribution and regulatory know-how. Capital intensity of EV infrastructure favors well-funded incumbents, yet fast-growing online platforms may catalyze consolidation waves as they seek physical service presence.

Middle East EV Dealership Industry Leaders

-

Al-Futtaim Automotive

-

Abdul Latif Jameel Motors

-

Electromin

-

VinFast – Al Mana Holding

-

Lucid Motors KSA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ceer signed 11 deals worth SAR 5.5 billion (USD 1.4 billion) with over 80% local suppliers for its 2026 launch.

- November 2024: PURE EV partnered with Arva Electric to deliver 50,000 two-wheelers across the Middle East and Africa over two years.

- October 2024: VinFast and Al Tayer Motors opened the first UAE dealership in downtown Dubai.

Middle East EV Dealership Market Report Scope

| New-EV Dealership |

| Used-EV Dealership |

| Franchised EV Retailer |

| Non-Franchised EV Retailer |

| Passenger Electric Cars |

| Commercial Electric Vehicles |

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid EVs (PHEV) |

| Fuel-Cell EVs (FCEV) |

| Online Platforms |

| Brick-and-Mortar Showrooms |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| Israel |

| Jordan |

| Lebanon |

| Egypt |

| Turkey |

| Rest of Middle East |

| By Type | New-EV Dealership |

| Used-EV Dealership | |

| By Retailer | Franchised EV Retailer |

| Non-Franchised EV Retailer | |

| By Vehicle Type | Passenger Electric Cars |

| Commercial Electric Vehicles | |

| By Powertrain Technology | Battery Electric Vehicles (BEV) |

| Plug-in Hybrid EVs (PHEV) | |

| Fuel-Cell EVs (FCEV) | |

| By Sales Channel | Online Platforms |

| Brick-and-Mortar Showrooms | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Israel | |

| Jordan | |

| Lebanon | |

| Egypt | |

| Turkey | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the forecast value of the Middle East EV dealership market in 2030?

It is projected to reach USD 12.66 billion by 2030, reflecting a 24.45% CAGR.

Which country holds the largest share today?

Saudi Arabia leads with 47.08% of 2024 sales, driven by Vision 2030 mandates.

Which segment is growing fastest?

Used-EV dealerships are expanding at 29.44% CAGR as the replacement cycle begins.

How fast are online sales channels expanding?

Online platforms are growing at a 33.36% CAGR, although brick-and-mortar stores still hold 77.78% share.

Why are FCEVs attracting attention despite low share?

FCEVs post a 40.66% CAGR because planned hydrogen corridors support heavy-duty and long-range applications.

What is the main infrastructure restraint outside capitals?

Sparse charging networks in secondary cities reduce dealership expansion potential and service accessibility.

Page last updated on: