UAE Electric Commercial Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

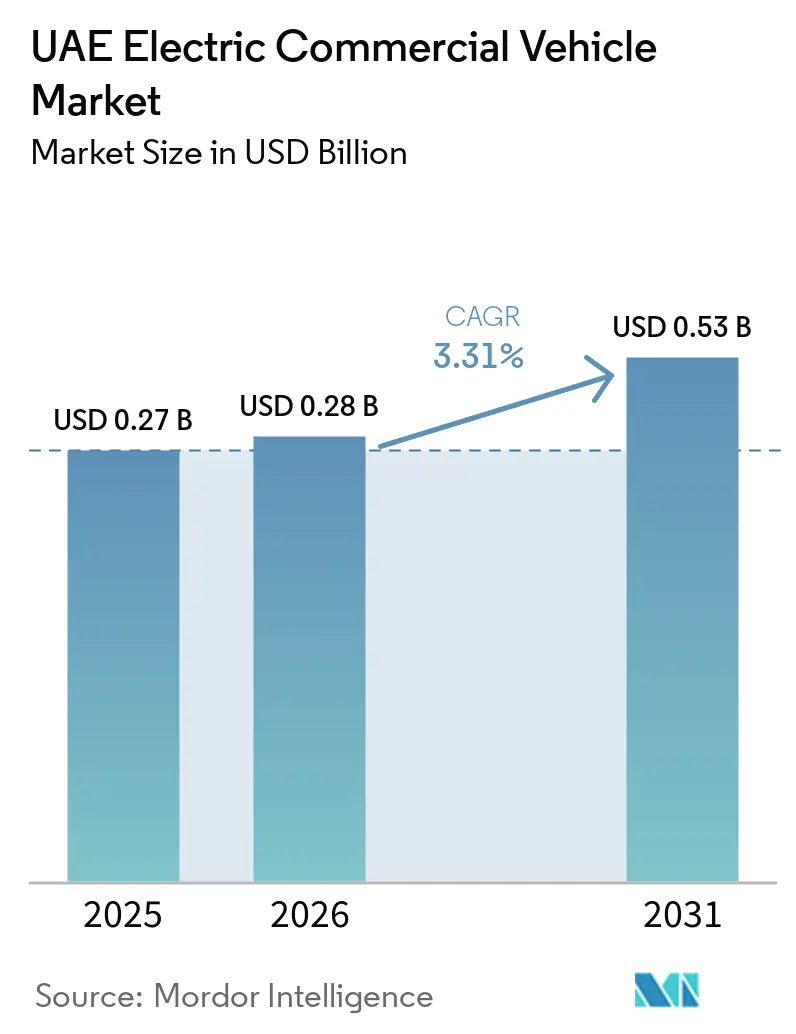

| Base Year Market Size (2025) | USD 0.27 Billion |

| Market Size (2026) | USD 0.28 Billion |

| Market Size (2031) | USD 0.53 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Electric Commercial Vehicle Market Analysis by Mordor Intelligence

The UAE electric commercial vehicle market size was valued at USD 0.27 billion in 2025 and estimated to grow from USD 0.28 billion in 2026 to reach USD 0.53 billion by 2031, at a CAGR of 3.31% during the forecast period (2026-2031). Federal climate mandates, wider last-mile e-commerce activity, and the declining total cost of ownership for delivery vans continue to encourage fleet managers to replace diesel units with battery-electric models. At the same time, progress is held back by grid-capacity ceilings around industrial clusters and the slow emergence of a single heavy-duty fast-charging protocol. Local distributors have begun bundling vehicles with turnkey charging services, reducing integration risk for operators. Market fragmentation remains moderate as incumbent global brands and newer Chinese entrants seek share through differentiated service packages rather than price alone.

Key Report Takeaways

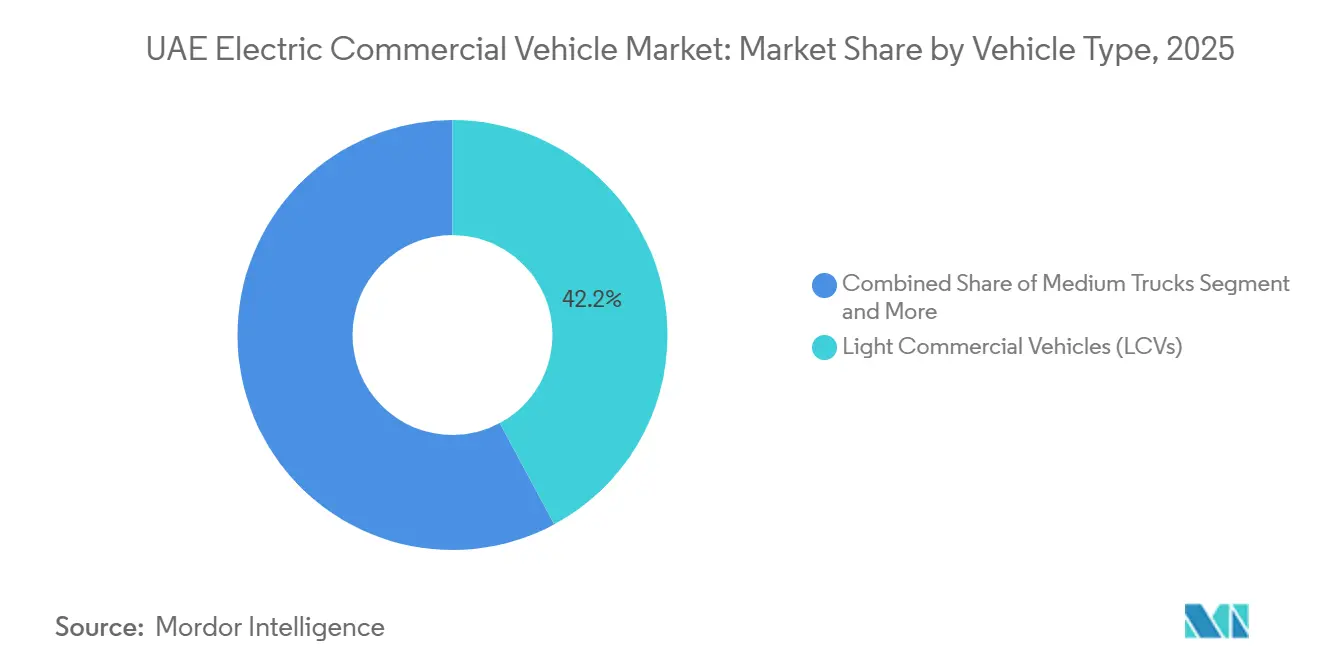

- By vehicle type, light commercial vehicles commanded 42.15% of the UAE electric commercial vehicle market share in 2025, while heavy trucks are projected to expand at the fastest 4.68% CAGR through 2031.

- By propulsion type, battery-electric platforms held 78.33% of the UAE electric commercial vehicle market share in 2025; fuel-cell models are set to record the fastest 7.56% CAGR over the same period.

- By drive type, rear-wheel-drive units accounted for 57.25% of the UAE electric commercial vehicle market share in 2025, whereas all-wheel-drive lines are forecast to grow at a 5.24% CAGR to 2031.

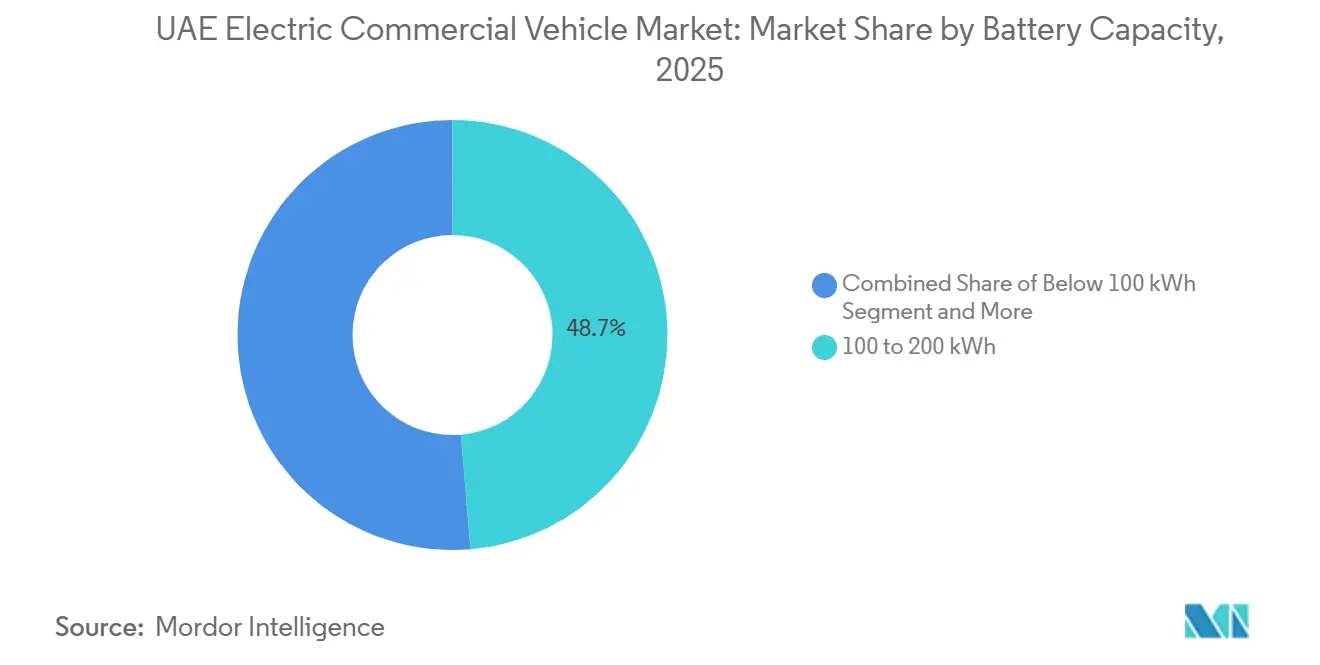

- By battery capacity, 100-200 kWh systems commanded 48.66% of the UAE electric commercial vehicle market share in 2025; packs above 200 kWh will lead growth at 4.17% CAGR through 2031.

- By end-use industry, urban transit applications captured 39.12% of the UAE electric commercial vehicle market share in 2025, while mining is projected to climb at a 5.88% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Electric Commercial Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Mandates Drive Fleet Electrification | +1.2% | UAE national; early gains in Dubai and Abu Dhabi | Medium term (2-4 years) |

| TCO Parity for Delivery Vans | +0.8% | UAE national; dense urban centers | Short term (≤2 years) |

| Expansion of UAE Hydrogen Corridors | +0.6% | Nationwide, with spill-over to GCC | Long term (≥4 years) |

| Integrated Charging Depots in Free-Zones | +0.4% | Dubai and Abu Dhabi free-trade zones | Medium term (2-4 years) |

| Carbon Offset Requirements in Bids | +0.3% | UAE national | Short term (≤2 years) |

| Desert Climate Battery Thermal Advances | +0.2% | UAE and wider Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government Fleet-Electrification Mandates

Federal and emirate-level procurement targets continue to underpin manufacturers' volume certainty. Dubai’s Road and Transport Authority added electric buses to its fleet, while multiple ministries converted a fifth of their vehicle stock by 2025[1]"Dubai introduces first electric buses as part of 2050 zero-emission transport drive", The National, thenationalnews.com. The public sector thereby provides residual-value benchmarks that reassure private buyers. Municipal tenders now specify zero-emission options as a base requirement, forcing bidders to align investment plans with electrification milestones. Together, these measures accelerate local after-sales network expansion and raise competitive thresholds for late entrants.

TCO Parity for Urban Delivery Vans by 2026

Sharp battery price declines and regulated diesel surcharges push operating costs for light vans toward breakeven with legacy powertrains. Fleet trials that track real-world service intervals, energy bills, and residual values have begun to confirm modeled savings, boosting lender confidence. Local insurers respond by carving out discounted policies for operators that meet factory telematics requirements, trimming premium gaps versus diesel. Together, these gains shorten payback horizons to within standard leasing cycles, nudging procurement teams toward electric as the default. Supplier finance programs then layer in warranty extensions that further de-risk adoption.

Expansion of UAE Green-Hydrogen Corridors

Oil-and-gas majors redirect part of their decarbonization budgets toward high-flow hydrogen pumps situated at inter-emirate truck stops. Early demonstrations with aviation-logistics partners validate long-range fuel-cell haulers on time-critical lanes where battery mass erodes payload economics. Memoranda of understanding signed with rail operators hint at future multimodal nodes, broadening the addressable freight base. While firm subsidies are still pending, the political capital invested in the national hydrogen strategy lends credibility to long-term price trajectories. Fleets therefore hedge by locking in pilot allotments that keep future technology options open.

Integrated Charging Depots in Free-Trade Zones

Land-use authorities inside logistics free zones award fast-track permits for high-capacity chargers, bundling grid upgrades with warehouse expansions. Hub operators exploit shared-use models: multiple carriers tap the same depot during staggered shift windows, boosting asset utilization and lowering per-plug capital costs. Because customs clearance, bonded storage, and charging now co-exist on a single plot, trucks avoid detours to public stations, saving driver hours. Utilities reciprocate by offering demand-response tariffs that reward overnight scheduling and smooth local load curves. The resulting ecosystem turns each free-zone depot into a showcase, enticing other landlords to replicate the template.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Grid Capacity at Clusters | −0.7% | Major Dubai and Abu Dhabi industrial zones | Medium term (2-4 years) |

| Scarcity of Fast-Charging Standards | −0.5% | UAE national | Short term (≤2 years) |

| Higher Insurance Premiums for E-trucks | −0.4% | UAE national | Short term (≤2 years) |

| Residual Value Uncertainty for EVs | −0.3% | UAE national | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited Grid Capacity at Industrial Clusters

Substations serving key free-zone logistics hubs operate near nameplate limits, and upgrade lead times average three years. Utility regulations restrict on-site generation, preventing operators from installing private solar-storage systems that could shave peak demand. As a result, fleets postpone mass adoption or confine electrified vehicles to low-power overnight charging schedules. In parallel, load-management software and staggered charging windows serve as short-term mitigations but do not fully address daytime fast-charging needs. Unless distribution upgrades coincide with vehicle-deployment plans, adoption will continue at a measured pace.

Scarcity of Heavy-Duty Fast-Charging Standards

Two rival megawatt-level protocols remain in play, obliging fleets to gamble on hardware that could strand assets if the alternative wins out. Interim solutions rely on lower-power connectors that stretch charging windows into multi-hour blocks, trimming daily mileage ceilings for long-haul rigs. Private station investors are hesitant to underwrite the cost of liquid-cooled cables until a clear winner emerges, slowing geographic coverage. OEMs hedge by offering adapter kits, a compromise that adds weight and service complexity without resolving root incompatibilities. Uncertainty, therefore, inflates the total cost of ownership calculations, delaying board-level purchase approvals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Urban Vans Dominate, Heavy Trucks Accelerate

Light commercial vans captured 42.15% of the UAE electric commercial vehicle market share in 2025. Their popularity stems from tight last-mile delivery routes where regenerative braking and compact footprints outperform diesel peers. Depot-based operations simplify overnight charging logistics, allowing managers to integrate electric vehicles without redesigning routes. Driver familiarity with van ergonomics speeds training, and municipal incentives often reserve curb space for zero-emission deliveries. Together, these factors entrench the segment as the market’s anchor.

Heavy trucks exhibit the fastest 4.68% CAGR through 2031. Mining and construction firms pilot battery- and fuel-cell-powered rigs to reduce on-site diesel handling and comply with tightening emissions norms. Early adopters negotiate bulk-energy contracts with utilities, offsetting higher vehicle sticker prices by locking in predictable operating costs. Demonstrated reliability in harsh desert conditions convinces financiers to extend longer-tenor leases. As duty-cycle data accumulates, adoption is expected to move from pilots into scaled fleet roll-outs.

By Propulsion Type: BEV Leads, FCEV Gains Niche Momentum

Battery-electric vehicles held a dominant 78.33% share of the UAE electric commercial vehicle market in 2025. Mature supply chains and a growing charger network make BEVs the default choice for fleets focused on urban and regional routes. Software advances provide accurate range prediction, reducing dispatchers’ anxiety about mid-shift downtime. Investors favor the simpler drivetrain, citing lower maintenance risk versus dual-energy systems. This reliability perception reinforces repeat purchasing among courier and municipal operators.

Fuel-cell electric vehicles will post the quickest 7.56% CAGR through 2031. Long-haul carriers eye hydrogen’s higher energy density to protect payload when crossing sparsely populated corridors. Energy majors sponsor the first refueling nodes, pairing them with captive fleet commitments that guarantee demand. As early field data de-risks residual-value estimates, leasing firms broaden eligibility criteria, unlocking new customer segments. These converging developments allow FCEVs to build beachheads in heavy-duty niches.

By Drive Type: RWD Holds Sway, AWD Advances

Rear-wheel-drive layouts secured the highest 57.25% of the UAE electric commercial vehicle market share in 2025. A simpler mechanical architecture keeps curb weight low, preserving cargo volume in city vans. Established workshop familiarity with RWD components shortens service downtimes, a critical metric for high-utilization fleets. Torque delivery to the rear axle also enhances stability under variable payloads. These practical advantages cement RWD as the baseline specification for most commercial buyers.

All-wheel-drive variants are projected to expand at the fastest 5.24% CAGR to 2031. Construction and mining operators value the additional traction on unpaved worksites, enabling year-round deployment despite shifting sand or gravel surfaces. OEMs now package AWD with reinforced battery enclosures, mitigating underbody impact risk. Software that automatically shifts torque between axles reduces driver workload on slippery ramps. Combined, these features justify the premium, as uptime under harsh conditions outweighs the capital cost.

By Battery Capacity: Mid-Range Packs Lead, High-Capacity Rises

Battery systems rated between 100 and 200 kWh commanded the largest 48.66% of the UAE electric commercial vehicle market share in 2025. They balance range with weight, matching typical urban duty cycles without eroding payload limits. Fleet managers appreciate that mid-size packs fit existing chassis without expensive reinforcements. Overnight depot charging easily replenishes them, sidestepping peak-hour tariffs. These advantages collectively underpin mainstream appeal.

Packs above 200 kWh show the fastest CAGR of 4.17% through 2031. Long-distance shippers select larger batteries to avoid en-route charging stops that disrupt tight delivery windows. Manufacturers couple these packs with active thermal management, ensuring performance during the Gulf’s extreme summer temperatures. Financing structures that spread higher upfront costs over extended service lives ease adoption hurdles. As charger power ratings climb, high-capacity platforms become increasingly practical for regional haulage.

By End-Use Industry: Transit Commands, Mining Quickens

Urban transit applications accounted for 39.12% of the UAE electric commercial vehicle market share in 2025. Public transport agencies set multi-year fleet-conversion targets that translate into predictable order pipelines for bus makers. Dedicated depot chargers simplify scheduling and allow batteries to cool overnight, prolonging service life. Passenger comfort benefits from quiet, vibration-free rides, supporting favorable user surveys. Positive rider feedback reinforces political backing for further procurement rounds.

Mining exhibits the fastest CAGR of 5.88% toward 2031. Site owners view electrification as a pathway to lower ventilation costs in enclosed pits and to meet corporate decarbonization pledges demanded by global commodity buyers. Pilot programs pair heavy trucks with on-site energy generation, reducing reliance on diesel logistics over long supply lines. Successful demonstrations create templates transferable to quarries and construction mega-projects. Each proof point shortens the decision cycle for the next operator evaluating a zero-emission fleet.

Geography Analysis

Dubai and Abu Dhabi together account for the bulk of fleet deployments thanks to stronger purchasing power, supportive municipal policies, and denser charging grids. Dubai’s Green Charger network now exceeds 1,860 publicly accessible points, with a target of 10,000 by 2026[2]"Dubai Launches 10,000 EV Charging Stations by 2026: DEWA Green Charger Network Expansion — Locations, Pricing & App Guide", DigitalDubai.ai, www.digitaldubai.ai. Abu Dhabi complements this with highway megahubs that link industrial zones to seaports, enabling inter-emirate electric freight itineraries. Sharjah leverages cross-border transit routes to pilot electric buses that feed passengers into Dubai Metro terminals. The Northern emirates are studying similar models, positioning themselves for follow-on infrastructure once anchor fleets expand.

Free-trade zones such as Jebel Ali and Dubai South concentrate third-party logistics providers that operate large mixed-make truck fleets. Land-use policies in these zones facilitate dedicated charging depots co-located with warehouses, reducing dwell time lost to refueling. Conditional rent rebates linked to sustainability metrics indirectly promote the uptake of zero-emission vehicles. Conversely, legacy industrial parks without sub-metering provisions face higher demand charges, delaying their transition. This divergence leads to a patchwork adoption pattern across the federation.

Grid resilience remains the pivotal variable. Utilities schedule incremental capacity upgrades tied to confirmed fleet orders, but component lead times expose roll-out plans to delay risk. Stakeholders therefore experiment with load-balancing software and partial on-site battery storage to smooth peak demand. Interim solutions reduce but do not eliminate the risk of transformer overloads during simultaneous fast-charging events. Broad-based deployment will depend on synchronized investment in both vehicles and infrastructure.

Competitive Landscape

The UAE electric commercial vehicle market is moderately fragmented. Global truck majors compete with agile Chinese brands and local distributors that pair vehicle sales with financing, telematics, and charging solutions. The resulting service ecosystems raise switching costs and shift emphasis from sticker price to lifecycle support. BYD deepened its footprint through a February 2026 equity partnership with Al-Futtaim, paving the way for future local assembly once annual volumes justify the investment in tooling.

Volvo, Daimler Truck, and Scania focus on premium heavy-duty niches, betting that early compliance with emerging megawatt charging standards will secure anchor accounts. Start-ups such as Einride differentiate through autonomous-drive stacks that promise higher asset utilization, courting customers willing to pilot mixed-technology fleets. Standards convergence remains a competitive lever. Early adopters of the Megawatt Charging System potentially lock in long-haul clients seeking future-proof assets.

Conversely, uncertainty over protocol dominance forces caution among price-sensitive operators. Local distributors mitigate this by offering upgrade clauses that swap charging hardware if standards shift, cushioning buyer risk. Such contractual innovations may weigh as heavily on purchasing decisions as vehicle specifications themselves.

UAE Electric Commercial Vehicle Industry Leaders

-

Daimler Truck AG

-

BYD Co. Ltd.

-

Volvo Group

-

Yutong Bus Co. Ltd.

-

Scania AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dubai debuted the all-electric eCanter light truck, highlighting the region's shift toward sustainable transportation. This launch was the result of a partnership between Mitsubishi Fuso and Al Habtoor Motors to address the growing demand for eco-friendly urban logistics solutions.

- September 2025: JBM Electric Vehicles partnered with Al Habtoor Motors to launch a new lineup of electric buses in the Emirates.

- April 2025: Jameel Motors and Farizon Auto jointly introduced the Farizon H9E electric truck during the Electric Vehicle Innovation Summit in Abu Dhabi.

UAE Electric Commercial Vehicle Market Report Scope

The UAE Electric Commercial Vehicle market is analyzed across vehicle type, propulsion type, drive type, battery capacity, and end-use industry.

By Vehicle Type, the market is segmented into Light Commercial Vehicles, Medium Trucks, Heavy Trucks, and Buses and Coaches. By Propulsion Type, the market includes Battery Electric Vehicles (BEVs), Plug-in Hybrid EVs (PHEVs), and Fuel-Cell EVs (FCEVs). By Drive Type, the market is categorized into Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), and All-Wheel Drive (AWD). By Battery Capacity, the market is segmented into Below 100 kWh, 100-200 kWh, and Above 200 kWh. By End-Use Industry, the market is analyzed across Urban Transit, Logistics and Delivery, Construction, Mining, and Municipal Services.

The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Light Commercial Vehicles (LCVs) |

| Medium Trucks |

| Heavy Trucks |

| Buses and Coaches |

| Battery Electric Vehicles (BEVs) |

| Plug-in Hybrid EVs (PHEVs) |

| Fuel-Cell EVs (FCEVs) |

| Front-Wheel Drive (FWD) |

| Rear-Wheel Drive (RWD) |

| All-Wheel Drive (AWD) |

| Below 100 kWh |

| 100-200 kWh |

| Above 200 kWh |

| Urban Transit |

| Logistics and Delivery |

| Construction |

| Mining |

| Municipal Services |

| By Vehicle Type | Light Commercial Vehicles (LCVs) |

| Medium Trucks | |

| Heavy Trucks | |

| Buses and Coaches | |

| By Propulsion Type | Battery Electric Vehicles (BEVs) |

| Plug-in Hybrid EVs (PHEVs) | |

| Fuel-Cell EVs (FCEVs) | |

| By Drive Type | Front-Wheel Drive (FWD) |

| Rear-Wheel Drive (RWD) | |

| All-Wheel Drive (AWD) | |

| By Battery Capacity | Below 100 kWh |

| 100-200 kWh | |

| Above 200 kWh | |

| By End-Use Industry | Urban Transit |

| Logistics and Delivery | |

| Construction | |

| Mining | |

| Municipal Services |

Key Questions Answered in the Report

What is the market size of UAE electric commercial vehicle market in 2026?

The market size was valued at USD 0.27 billion in 2025 and estimated to grow from USD 0.28 billion in 2026 to reach USD 0.53 billion by 2031, at a CAGR of 3.31% during the forecast period (2026-2031).

What charging standard should a fleet consider for future heavy-duty truck purchases?

Operators increasingly monitor the Megawatt Charging System, certified in 2026, yet many hedge by installing dual CCS-compatible hardware that can be retro-fitted.

Are fuel-cell trucks commercially available in the UAE in 2026?

Yes, pilot fuel-cell units ordered by logistics and aviation operators are scheduled for delivery during 2026 along the new green-hydrogen corridor.

Can smaller emirates like Ajman adopt electric buses cost-effectively?

Sharjah’s cross-border routes demonstrate that pooling demand with Dubai Metro links can make electric transit financially viable for neighboring emirates.

Page last updated on: