Europe Automotive Dealership Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

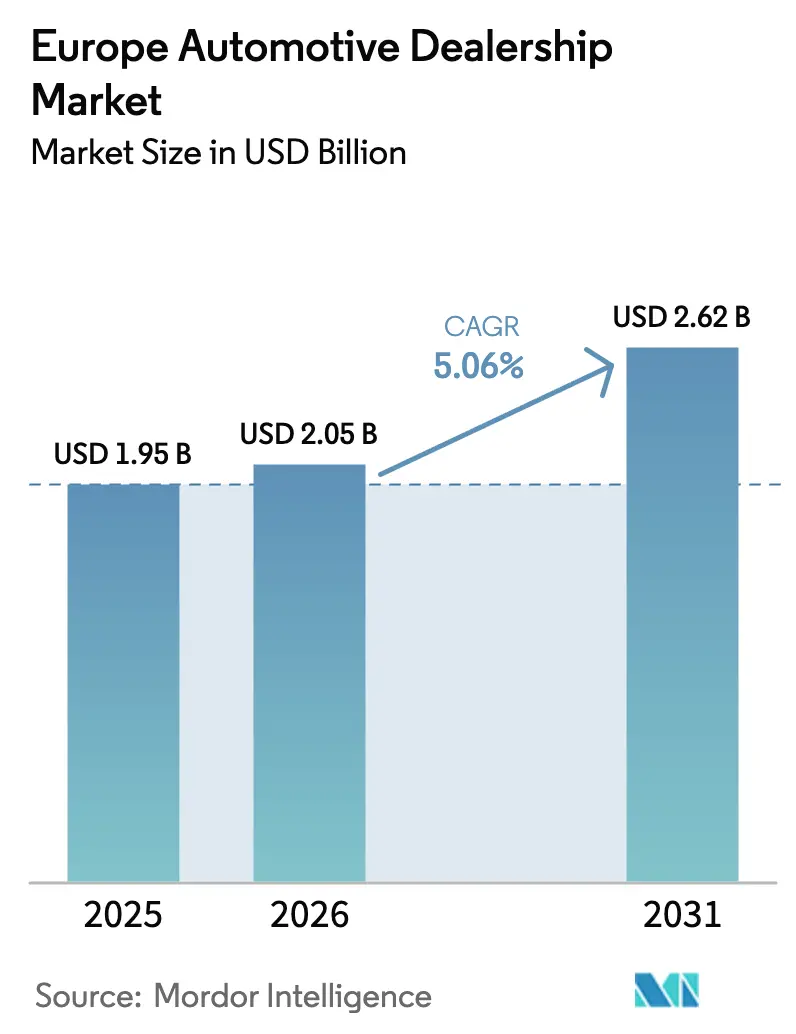

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Dealership Market Analysis by Mordor Intelligence

The European automotive dealership market size is expected to grow from USD 1.95 billion in 2025 to USD 2.05 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 5.06% CAGR over 2026-2031. The forecast underscores how sustained vehicle demand, rapid battery-electric adoption, and an accelerating shift toward omnichannel retail keep the European automotive dealership market on a stable expansion path. Franchise groups are pouring capital into charging infrastructure, technician up-skilling, and digital sales portals to meet stricter emissions rules and rising online expectations. Cross-border used-car e-commerce networks continue to broaden sourcing pools, while Chinese original-equipment brands leverage local dealers to secure showroom visibility. Consolidation opportunities remain abundant because no single operator holds more than 4% revenue share, leaving strategic acquirers able to unlock scale economics and technology synergies.

Key Report Takeaways

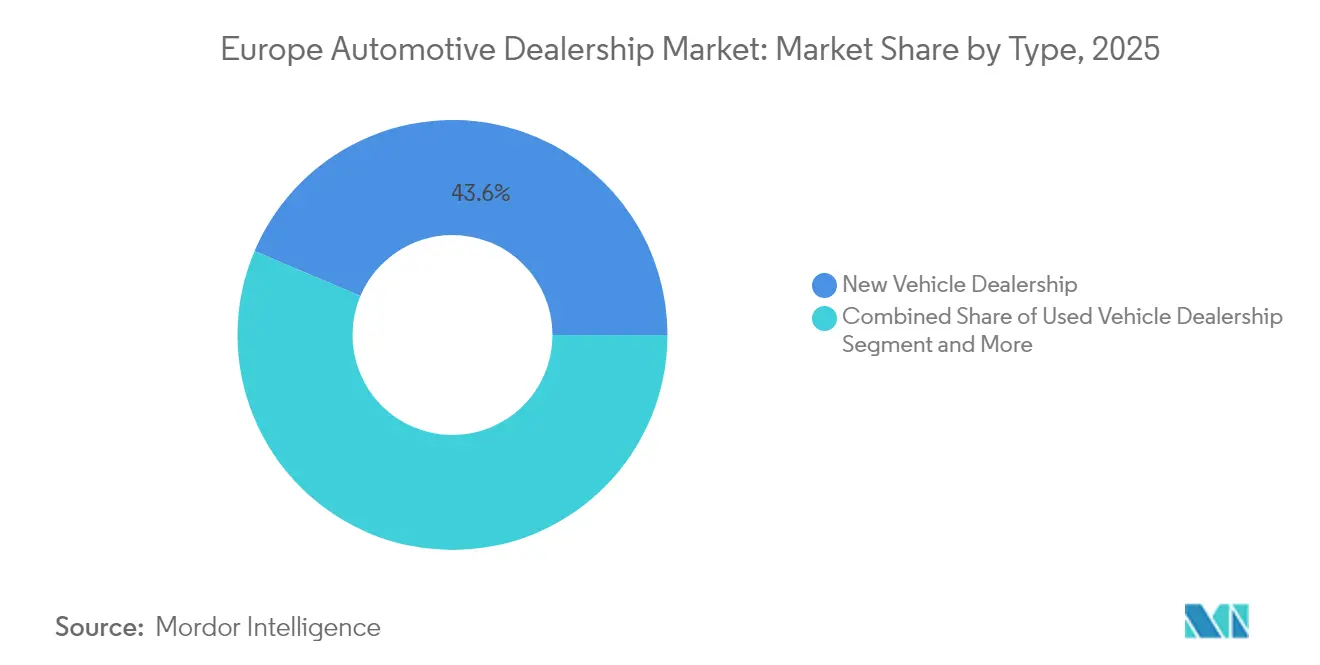

- By type, New Vehicle Dealership held 43.62% of the Europe automotive dealership market share in 2025; Parts and Service is forecast to expand at an 7.72% CAGR through 2031.

- By retailer, Franchised Dealers commanded 61.12% of the Europe automotive dealership market share in 2025, while Independent Dealers are expected to register the highest projected CAGR at 6.33% to 2031.

- By vehicle type, Passenger Cars accounted for 77.05% of the Europe automotive dealership market share in 2025, and Light Commercial Vehicles are advancing at a 6.09% CAGR through 2031.

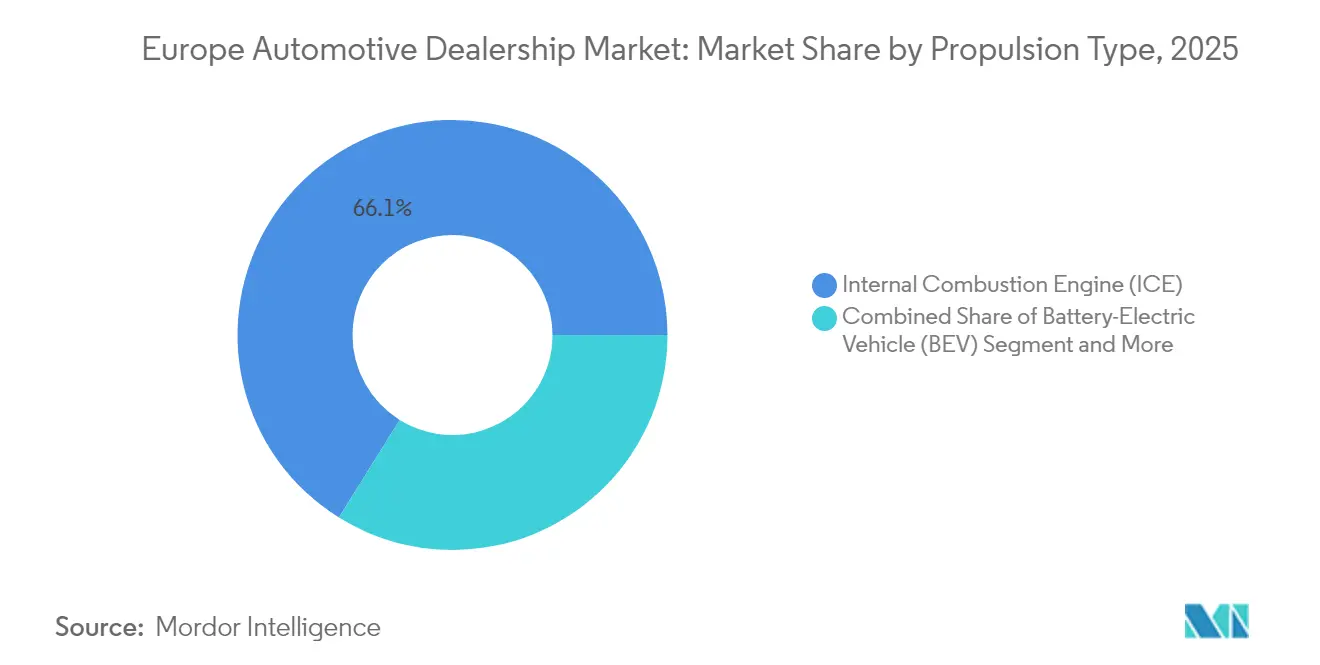

- By propulsion type, ICE-powered vehicles dominated with 66.14% of the Europe automotive dealership market share in 2025; Battery-Electric Vehicles post a 15.92% CAGR for 2026-2031.

- By sales channel, Offline/Showroom retained 92.88% of the Europe automotive dealership market share in 2025, whereas Online Direct channels rose at an 11.02% CAGR to 2031.

- By country, Germany led with 24.96% of the Europe automotive dealership market share in 2025 and the Rest of Europe block records a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Dealership Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In BEV Registrations | +2.8% | Germany, France, Netherlands, Norway | Medium term (2-4 years) |

| Used-Car E-Commerce Platforms | +1.9% | Germany, France, UK, Italy, Spain | Short term (≤ 2 years) |

| Aftermarket Revenue Streams | +1.5% | Germany, UK, France, Italy | Long term (≥ 4 years) |

| Agency Retail Model | +1.2% | Germany, UK, Sweden, Italy, Poland | Medium term (2-4 years) |

| Digital Omnichannel Purchasing Expectations | +0.9% | Germany, France, UK, Netherlands | Short term (≤ 2 years) |

| Chinese OEM Partnerships | +0.7% | Germany, Netherlands, UK, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth In Battery-Electric Vehicle Registrations

During Jan-April 2025, BEV registrations increased by 43%, lifting BEV penetration above 16% of total registrations and compelling retailers to upgrade workshops with high-voltage tooling and 50-hour certification programs for technicians. Partnerships like XPENG’s roaming agreement with Plugsurfing give customers seamless access to 940,000 charging points across 27 countries and open ancillary revenue for dealers offering subscription-based charging bundles. Lower service complexity curtails traditional oil-change income but propels demand for battery diagnostics and software updates. Public incentives, including Poland’s subsidy scheme, shorten BEV payback periods. Overall, the electrification surge boosts showroom footfall yet forces dealer networks to rebalance profit models away from routine maintenance toward digital services.

Surge In Cross-Border EU Used-Car E-Commerce Platforms

Digital marketplaces grow liquidity by linking French, German, and Spanish stock pools, trimming search times for specific trims, and driving a 5.1% average used-car price lift in H1 2025. Narrow margins on new vehicles motivate dealers to source margin-rich second-hand inventory via online auctions with real-time logistics calculators. Specialized portals focusing on battery-health disclosure accelerate residual-value confidence for used BEVs, while blockchain-based vehicle passports promise tamper-proof odometer histories. The European automotive dealership market thus captures incremental trade-in volumes from consumers who value transparent pricing and remote paperwork completion.

Expansion Of Aftermarket Service Revenue Streams

As connected-car penetration deepens, dealers diversify into predictive maintenance, over-the-air software updates, and subscription-based safety features. Cloud-enabled diagnostics slash repair lead times and permit just-in-time parts ordering, reducing working-capital lock-up. Sustainability regulations spur demand for remanufactured parts and circular-economy services, helping offset declining ICE maintenance tasks. Strategic alliances with software providers let retailers monetize real-time vehicle data, converting one-off transactions into recurring revenue. Consequently, the European automotive dealership market gains a defensible income pillar less sensitive to new vehicle cycles.

Agency Retail Model Adoption by OEMs

Manufacturers that move to direct invoicing free dealers from stocking risk, replacing gross-margin variability with a stable commission per unit. Early adopter pilots generated higher lead-to-conversion ratios owing to transparent, fixed pricing that eliminates haggling anxiety. Dealers, however, assume new digital-consultant roles requiring investment in customer-relationship management platforms and omnichannel appointment scheduling. While commission levels trail historic gross margins, working-capital relief and marketing support from OEMs partially compensate, encouraging more networks to sign agency contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Requirements | -1.8% | Germany, France, UK, Italy | Short term (≤ 2 years) |

| Margin Compression From Pricing Transparency | -1.4% | Germany, UK, France, Netherlands | Medium term (2-4 years) |

| Declining ICE Vehicle Parc | -0.9% | Germany, France, UK, Italy | Long term (≥ 4 years) |

| Dealer-Network Consolidation | -0.6% | UK, Germany, France, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Requirements for EV Tooling and Training

Dealerships collectively commit specialized lifts, insulated tools, and on-site chargers, with individual sites spending from USD 100,000 to USD 1 million.[1]“Dealerships on Track to Invest $5.5 Billion in EV Infrastructure,” National Automobile Dealers Association, nada.org Certification mandates keep payroll budgets elevated as technicians rotate through high-voltage safety courses. Smaller rural outlets lacking sufficient throughput struggle to recoup costs, accelerating mergers or closures. Required public-charging density, estimated at 6.8 million points by 2030, adds further strain, prompting networks to seek joint-venture financing.[2]“European EV Charging Infrastructure Masterplan,” European Automobile Manufacturers’ Association, acea.auto

Margin Compression from Pricing Transparency

Uniform online pricing and OEM agency invoicing shrink negotiation leeway, pushing gross profit per new vehicle down by one-third in 2024. Digital marketplaces let consumers cross-shop in seconds, so competitive edge shifts to after-sales service quality and lifetime-value programs. Dealer groups respond with cost-optimization drives, centralizing back-office functions and deploying AI for inventory planning to protect overall profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Service revenue takes center stage

New Vehicle Dealerships commanded 43.62% of the Europe automotive dealership market share in 2025, while parts and service contribute to rising cash-flow resilience as they expand at an 7.72% CAGR between 2026 and 2031. Subscription-based diagnostic packages, extended-warranty sales, and battery lifecycle management reinforce profitability when unit sales slow. Dealers that bundle predictive maintenance with charging-station access lock in multi-year customer relationships. The European automotive dealership market size for parts-centric operations is projected to widen steadily as vehicle complexity and average age grow.

Meanwhile, the European automotive dealership market share of New Vehicle Dealerships gradually eases, but showroom refurbishments featuring immersive product displays continue to attract first-time BEV buyers. Smaller Used Vehicle Dealerships gain relevance because elevated lending rates keep many consumers in the second-hand channel. Finance and insurance desks digitalize documentation to comply with revised consumer protection rules, shrink contract cycle time, and enhance customer experience scores. Wider take-up of online service-booking portals reinforces margins on labor hours amid commodity-price fluctuations for parts.

By Retailer: Independents capture momentum

Franchised chains retained 61.12% of the Europe automotive dealership market share in 2025, yet Independent Dealers indicate the fastest 6.33% CAGR owing to specialization in cross-border remarketing and localized customer service. As agency contracts proliferate, franchisees shift from inventory risk to commission structures, freeing balance-sheet capacity for digital investments. The European automotive dealership market size flowing to independents increases as online platforms equalize brand visibility. Independents employ data-driven stocking models that optimize country-specific demand gaps and capitalize on tariff-free intra-EU movement.

Consolidators utilize shared back-office systems and centralized procurement to secure volume rebates. The European automotive dealership market share for the five largest groups remains in single digits, leaving scope for roll-up strategies. Technology adoption, such as AI-based lead-scoring, levels the playing field, letting niche operators compete for high-value fleet contracts.

By Vehicle Type: Commercial fleet electrifies quickly

Passenger Cars generated 77.05% of the Europe automotive dealership market share in 2025, yet Light Commercial Vehicles show the greatest upward slope at 6.09% CAGR. Last-mile delivery commitments by major e-commerce retailers accelerate BEV van purchases, pushing demand for dealer-installed depot chargers. The European automotive dealership market size tied to commercial segments benefits from higher service-interval frequency and accessories such as telematics.

Passenger-car volume remains substantial, but profit margins migrate toward optional software features and personalization packages. City-center emission zones promote fleet renewal, and warranty packages bundling battery health guarantees appeal to small-business owners wary of residual-value risk. Consequently, Light Commercial Vehicles gradually lift their European automotive dealership market share despite passenger-car dominance.

By Propulsion Type: Battery-electric surge reshapes economics

ICE models delivered 66.14% of the Europe automotive dealership market share in 2025; however, Battery-Electric Vehicles escalated at 15.92% CAGR through 2031. Stricter EU fleet-average standards compel manufacturers to allocate production quotas to zero-emission models, and tax policy, such as accelerated depreciation in Germany, sweetens corporate uptake. The European automotive dealership market size is attributable to BEVs, forcing workshops to carry high-voltage service bays and insulated toolkits.

Plug-in hybrids maintain a transitional role, accounting for meaningful showroom traffic where charging grids are still maturing. Used-BEV resale channels expand, with dealers offering certified battery-health reports to reassure buyers. Software-defined vehicle architectures introduce recurring revenue via feature unlocks and infotainment subscriptions, broadening post-sale monetization.

By Sales Channel: Online direct evolves from niche to norm

Offline/Showroom environments still booked 92.88% of the Europe automotive dealership market share in 2025, but Online Direct grows at 11.02% CAGR as self-service configurators, e-signature finance contracts, and doorstep delivery gain acceptance. Shoppers now interact with an average of three digital touchpoints before their first physical visit, compelling dealers to unify inventory visibility across channels. The European automotive dealership market size derived from online storefronts is expected to double by 2031.

Live-chat video walk-arounds, augmented-reality accessories previews, and AI loan-eligibility engines allow buyers to finalize decisions remotely, preserving showroom bandwidth for complex consultations. Physical touchpoints remain critical for test drives and trade-in appraisals. Dealers integrate appointment scheduling with digital price-locking to eliminate queue times. The European automotive dealership market share of purely virtual sales remains modest but accelerates in metropolitan areas with high broadband coverage.

Geography Analysis

Germany commands 24.96% of the Europe automotive dealership market share in 2025, leveraging its position as Europe's largest automotive market and manufacturing hub, while the Rest of Europe segment demonstrates the fastest growth at 6.05% CAGR from 2026-2031. High GDP per capita, dense dealership networks, and early adoption of agency agreements underpin revenue resilience. Franchise groups capitalize on public fast-charging density and robust fleet-lease markets to keep showroom traffic steady. Regulatory clarity around zero-emission zones motivates corporate fleet managers to move purchasing cycles forward, bolstering order books for BEV and PHEV models.

Southern European markets such as Spain and Italy enter a catch-up phase. EU recovery funds earmarked for sustainable mobility finance new charging corridors, while consumer incentive schemes encourage households to migrate from older ICE vehicles. Rising tourism flows also lift light commercial rental demand, indirectly boosting service revenues for local dealerships. The European automotive dealership market size in these countries gains extra momentum as Chinese brands select partner dealers to accelerate nationwide rollouts.

Central and Eastern Europe deliver the highest percentage growth, albeit from a smaller base. Improved highway infrastructure and increased foreign direct investment in battery-cell plants catalyze regional capacity expansions. Cross-border e-commerce platforms optimize vehicle sourcing, giving dealers in Poland, Czechia, and Hungary streamlined access to Western-European lease returns. Dealers that develop multi-lingual online portals and flexible financing solutions secure early-mover advantages here, nudging up the European automotive dealership market share for the sub-region.

Competitive Landscape

European automotive retail remains highly fragmented. Emil Frey Group, Penske Automotive Group, and Inchcape PLC collectively commanded less than one-fourth of the market share in 2024. This leaves fertile ground for roll-ups and private-equity-backed buy-and-build programs, especially because EBITDA multiples average 3–4× versus roughly double in North America [IMF]. Technology adoption differentiates leaders: Emil Frey deploys centralized data lakes to forecast service-bay utilization, while Penske Automotive pilots AI chatbots for after-hours lead capture.

Chinese OEM alliances intensify competitive dynamics. BYD secures showroom space via exclusive agreements with established dealer groups, offering immediate volume flow and margin incentives that help retailers diversify brand mix. Simultaneously, digital-first used-car platforms scale through partnerships that give brick-and-mortar dealers incremental supply without inventory risk. As margins compress on new-unit sales, groups focus on expanding high-margin finance, insurance, and subscription services.

Van Mossel Automotive Group expanded into northern Germany, while Penske acquired a Ferrari outlet in Modena. Cross-border synergies include unified procurement, shared training academies, and consolidated marketing budgets. Investors prioritize portfolios with robust omnichannel capabilities and EV-service readiness, anticipating higher customer lifetime value and lower cost-to-serve. Dealer groups that lag in digital transformation risk becoming acquisition targets or losing franchise rights when OEMs renew network contracts.

Europe Automotive Dealership Industry Leaders

Emil Frey Group

Penske Automotive Group (Sytner)

Arnold Clark Automobiles

Inchcape PLC

Pendragon PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Penske Automotive Group completed the acquisition of a Ferrari dealership in Modena, Italy, expected to add USD 40 million annual revenue.

- June 2025: Athenaeum International Holdings agreed to acquire Johnsons Cars, placing the merged entity among the UK’s top-ten retail groups.

- November 2024: Reynolds and Reynolds partnered with Skaivision to deploy AI video analytics that streamline service-lane workflows.

- September 2024: Van Mossel Automotive Group signed an agreement to acquire Nord-Ostsee Automobile SE & Co KG, expanding its German footprint.

Europe Automotive Dealership Market Report Scope

| New Vehicle Dealership |

| Used Vehicle Dealership |

| Parts and Service |

| Finance and Insurance (FandI) |

| Franchised Dealer |

| Independent Dealer |

| Passenger Cars |

| Light Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) |

| Plug-in Hybrid (PHEV) |

| Offline / Showroom |

| Online Direct |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Rest of Europe |

| By Type | New Vehicle Dealership |

| Used Vehicle Dealership | |

| Parts and Service | |

| Finance and Insurance (FandI) | |

| By Retailer | Franchised Dealer |

| Independent Dealer | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| By Propulsion Type | Internal Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) | |

| Plug-in Hybrid (PHEV) | |

| By Sales Channel | Offline / Showroom |

| Online Direct | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the European automotive dealership market be by 2031?

It is forecast to reach USD 2.62 billion, expanding at a 5.06% CAGR over 2026-2031.

Which sales channel is growing fastest in the region?

Online Direct transactions are rising at an 11.02% CAGR as consumers embrace seamless digital purchasing journeys.

Why are battery-electric vehicles important for dealerships?

BEVs drive new revenue through charging partnerships and software services while requiring specialized workshop investments.

What share do Germany’s dealers hold within Europe?

Germany generated 24.96% of regional turnover in 2025, the largest single-country contribution.

Which retail segment offers the strongest growth outlook?

Parts and Service operations lead with an 7.72% CAGR as predictive maintenance and connected-car services gain traction.

Page last updated on: