South East Asia Automotive Dealership Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

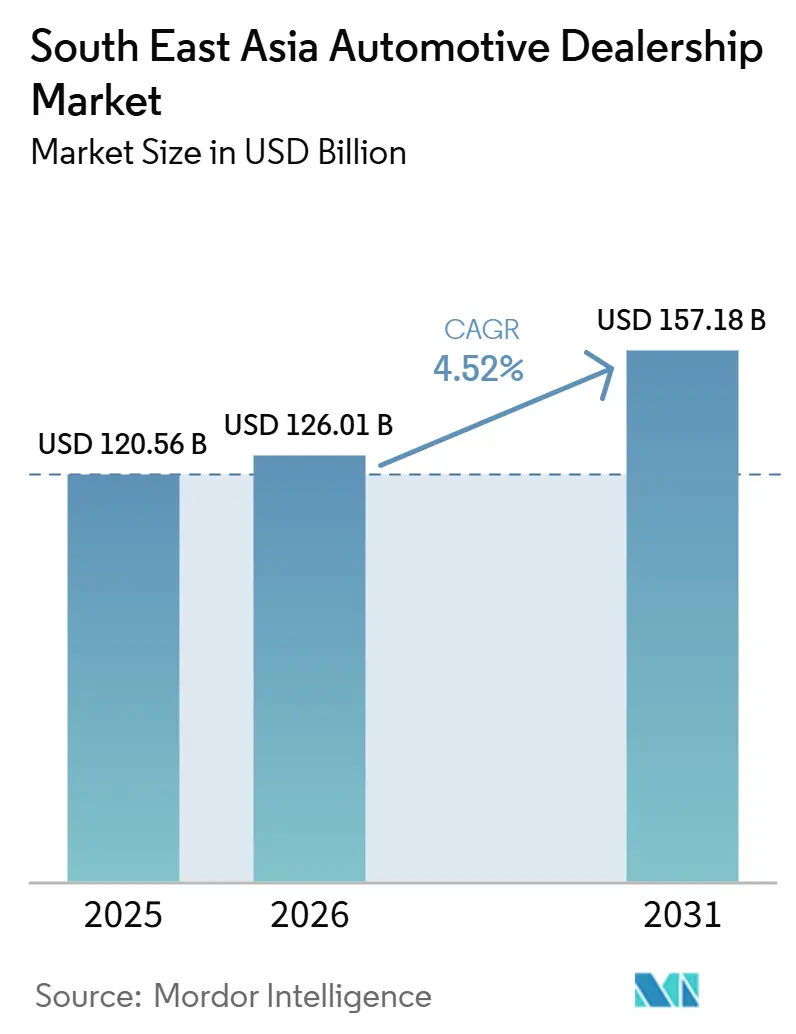

| Base Year Market Size (2025) | USD 120.56 Billion |

| Market Size (2026) | USD 126.01 Billion |

| Market Size (2031) | USD 157.18 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

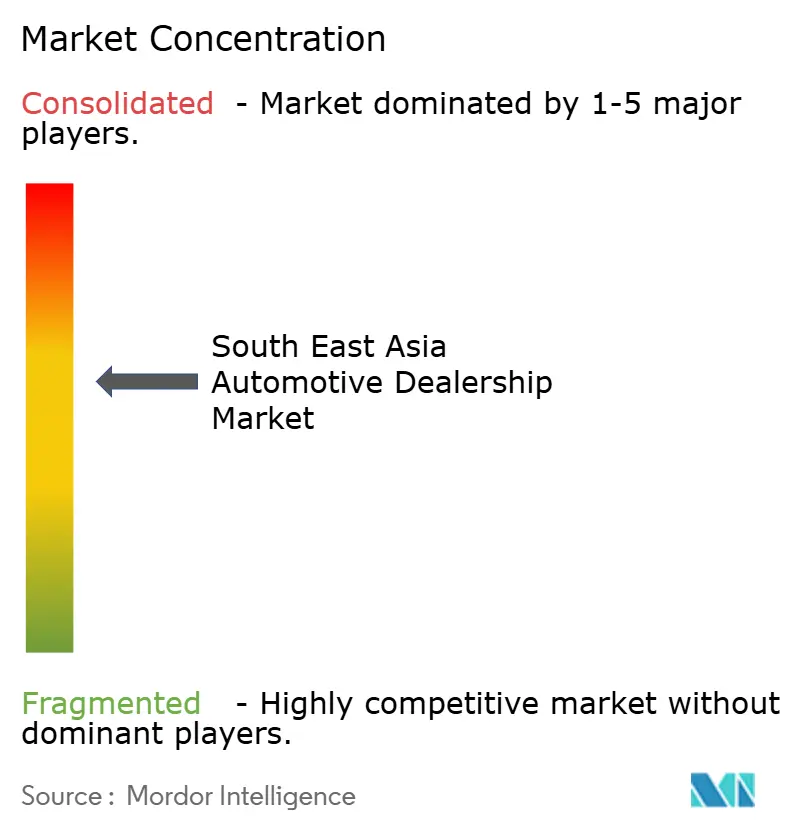

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South East Asia Automotive Dealership Market Analysis by Mordor Intelligence

The Southeast Asia automotive dealership market size is expected to grow from USD 120.56 billion in 2025 to USD 126.01 billion in 2026 and is forecast to reach USD 157.18 billion by 2031, advancing at a 4.52% CAGR during the forecast period (2026-2031). The Southeast Asian automotive dealership market continues to benefit from stronger consumer confidence, favorable policy incentives for electric vehicles, and digital-first retailing. Strategic OEM–dealer alliances, omnichannel platforms, and government-supported electrification all underpin the medium-term outlook for the Southeast Asia automotive dealership market. Dealer groups are re-balancing revenue toward parts, service, and financing as new-vehicle margins tighten. Meanwhile, the Southeast Asia automotive dealership market faces cost inflation, tighter credit, and the disruptive potential of direct-to-consumer pilots.

Key Report Takeaways

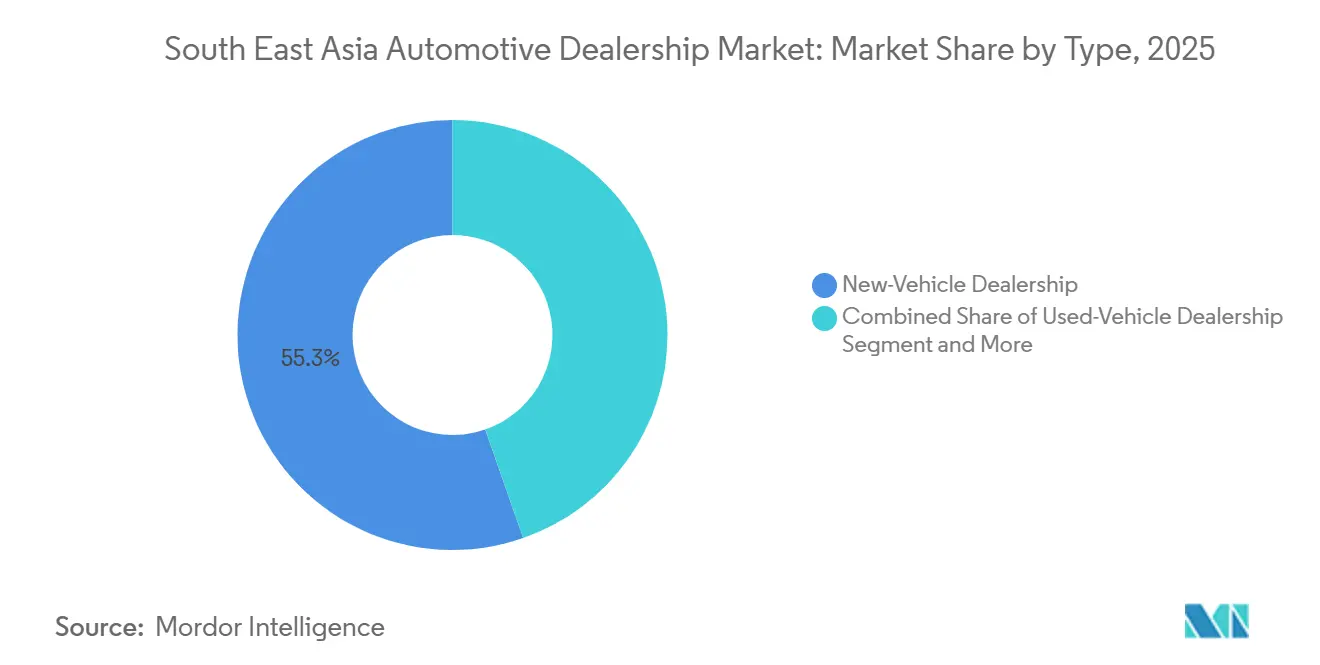

- By type, new-vehicle dealerships captured 55.33% of the Southeast Asia automotive dealership market share in 2025 and are forecast to grow at a 6.12% CAGR through 2031.

- By retailer, franchised networks held 64.47% of the Southeast Asia automotive dealership market share in 2025 and represented the fastest expansion, with a 6.21% CAGR to 2031.

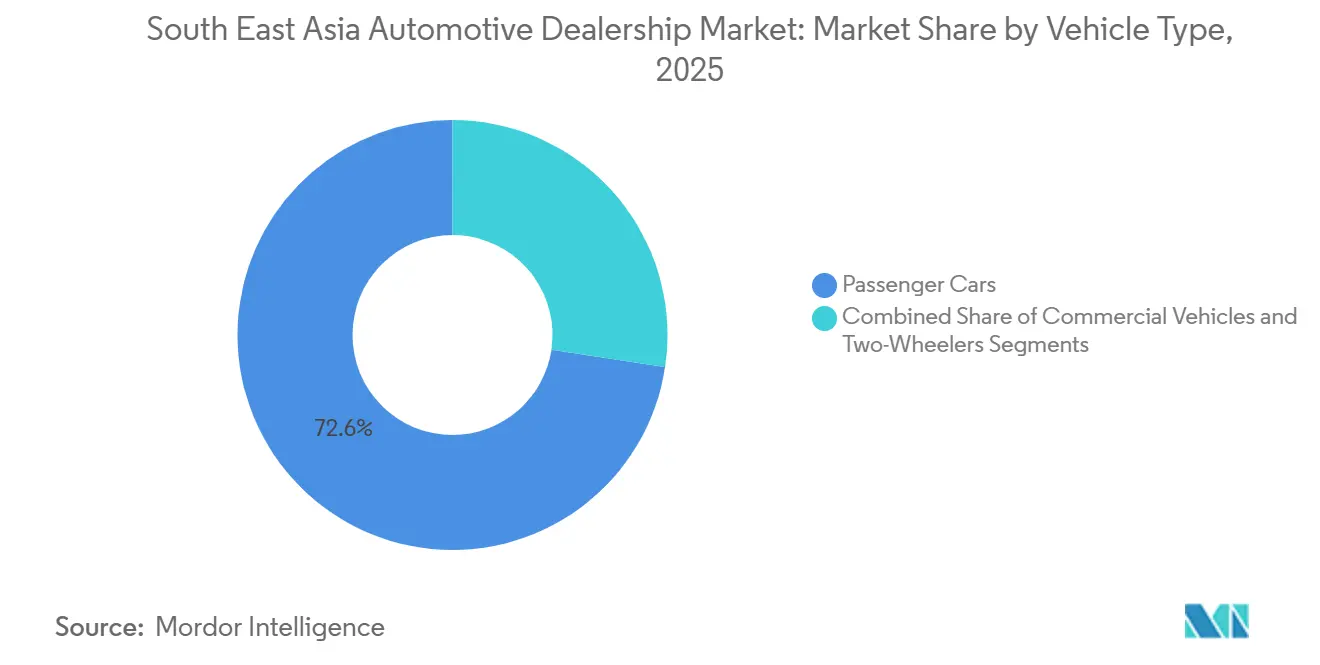

- By vehicle type, passenger cars led with 72.63% share of the Southeast Asia automotive dealership market size in 2025; commercial vehicles are projected to expand at a 7.08% CAGR through 2031.

- By propulsion, internal-combustion vehicles accounted for 94.12% of the Southeast Asia automotive dealership market share in 2025, whereas electric vehicles are advancing at a 10.53% CAGR to 2031.

- By geography, Indonesia dominated with a 28.64% of the Southeast Asia automotive dealership market share in 2025, and the Philippines is expected to record the highest growth at an 8.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South East Asia Automotive Dealership Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging New-Vehicle Demand | +1.2% | Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Digital Retailing and Omnichannel Buying | +1.1% | Singapore, Malaysia, Thailand, Indonesia | Short term (≤ 2 years) |

| After-Sales Service Expansion | +0.9% | Indonesia, Thailand, Malaysia, Philippines | Long term (≥ 4 years) |

| Pre-Owned Vehicle Platforms and Classifieds | +0.8% | Malaysia, Indonesia, Thailand, Singapore | Medium term (2-4 years) |

| EV-Exclusive Dealership Formats | +0.7% | Thailand, Indonesia, Malaysia, Philippines | Long term (≥ 4 years) |

| ASEAN Grey-Market Liberalisation | +0.6% | Thailand, Malaysia, Indonesia, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging New-Vehicle Demand Across Indonesia, Thailand and Vietnam

Combined new-vehicle registrations across three markets surpassed significant volumes, enabling dealer groups to justify the establishment of new outlets and service bays. Indonesian conglomerate Indomobil is eyeing additional sites to enhance its presence in Jakarta, Bandung, and Surabaya. Meanwhile, Vietnam's THACO is setting up rural showrooms to make maintenance services more convenient for customers. In Thailand, robust commercial vehicle pipelines are bolstered by public infrastructure spending, which in turn fuels demand for light trucks. Dealer financiers are enticing first-time buyers—who had delayed purchases during the pandemic—with bundled low-down-payment offers and manufacturer cash rebates. These combined factors not only bolster foot traffic but also highlight the growing influence of online configurators in the early stages of vehicle consideration.

Rapid Digital Retailing and Omnichannel Buying Journeys

Consumers now expect price transparency, virtual vehicle walk-arounds, and at-home test drives, pushing the Southeast Asia automotive dealership market toward full inventory visibility across apps and showroom tablets. Toyota Philippines’ end-to-end SAP rollout reduces quotation time and synchronizes parts availability, boosting conversion rates and service retention. Partnerships such as GAC-Grab fold ride-hailing data into cockpit interfaces, hinting at future subscription revenue for dealers that manage fleet uptime. VinFast’s web portal allows 90% financing approvals within minutes, raising the competitive bar on loan processing speed. Dealers embracing click-to-buy funnels can capture browsing signals that guide stocking decisions, whereas legacy outlets reliant on walk-ins lose share to digitally native rivals [1]“An Inclusive Digital Economy in the ASEAN Region,” ASEAN Secretariat, asean.org.

After-Sales Expansion by OEM-Backed Dealer Groups

As vehicle sales face margin compression, the importance of parts and services becomes paramount. Stellantis’ hub in Malaysia efficiently ships a wide range of SKUs, boasting short lead times. This agility enhances fill-rates for Jeep and Peugeot retailers across multiple countries. In a strategic move, BMW Malaysia expanded its Johor warehouse significantly, bolstering regional support for high-voltage battery repairs. Meanwhile, THACO, a leading player in Vietnam, is pioneering mobile workshops in rural provinces and utilizing proprietary apps for seamless maintenance bookings. Their investment in certified technician programs not only tackles the intricacies of EV drivetrains but also ensures precise recalibration of advanced driver-assistance systems. This expertise allows them to command labor rates that surpass inflation [2]“Electrified Experience Dealer Network,” Honda, hondaoutsidejava.co.id. Such a robust after-sales infrastructure not only fortifies customer loyalty but also shields dealership profitability, even during cyclical downturns in sales volume.

Booming Pre-Owned Vehicle Platforms and Classifieds

Carsome achieved significant EBITDA growth, while Carro secured substantial capital, underscoring the growing investor confidence in online used-car platforms. Advanced algorithms now benchmark book values, standardize vehicle reconditioning, and assess battery health for older electric vehicles (EVs), bolstering buyer trust. Listings that come certified not only offer extended warranties but also provide doorstep delivery, diminishing the trade-in edge that physical dealers once monopolized. In response, traditional dealerships are launching branded pre-owned programs and leveraging instant digital appraisal tools to prevent inventory losses. Meanwhile, credit providers, including MUFG-backed JACCS, are expanding financing options for second-hand vehicles, adding a layer of professionalism to the industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex And Working-Capital Needs | -0.5% | Indonesia, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Direct-To-Consumer Online Sales | -0.4% | Singapore, Malaysia, Thailand | Medium term (2-4 years) |

| Import /Tariff Uncertainty | -0.3% | Malaysia, Thailand | Medium term (2-4 years) |

| Certified EV Technicians Shortage | -0.2% | Thailand, Indonesia, Malaysia, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Working-Capital Needs for Multi-Brand Showrooms

Flagship outlets integrating EV chargers, digital screens, and certified workshops can top USD 10 million, stretching dealer leverage ratios. Perodua's capital plan underscores the unpredictable nature of cash outflows, especially when investments in production, retail, and services converge. As the proliferation of models demands a deeper stock to meet immediate fulfillment expectations, inventory carrying costs inevitably escalate. Small independent entities, lacking OEM co-investment programs, frequently merge into larger groups, hastening consolidation. Meanwhile, access to green financing and vendor-managed inventory programs emerges as a key differentiator, influencing the speed of network expansion.

Direct-to-Consumer Online Sales Pilots by Global OEMs

VinFast operates self-branded showrooms and continues to promote online transactions, leaving dealers with minimal after-sales benefits. Inspired by Tesla's global triumph, traditional brands are experimenting with fixed-price portals in major urban centers across ASEAN, limiting franchisees' room for negotiation. If regulators ease restrictions on the agency model, dealers could jeopardize finance and insurance revenues, which currently contribute significantly to their gross profit. In response, some dealers are launching white-label e-commerce platforms, enabling them to offer same-day deliveries from their local inventory. Ultimately, the future of this dynamic will depend on whether consumers prioritize in-person handovers and personalized service consultations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: New-Vehicle Sales Drive Market Leadership

The Southeast Asia automotive dealership market size for new-vehicle outlets accounted for 55.33% in 2025 and is projected to grow at a 6.12% CAGR to 2031. OEMs prioritize these channels for EV rollouts, offering co-funded charger installations that reduce payback periods. BMW's new store in Jakarta features digital configurators and lounge spaces, enhancing the brand's storytelling. As battery-electric vehicles gain popularity, inventory is shifting toward models with higher gross margins. This adjustment helps mitigate the downward pressure caused by online price transparency.

Used-vehicle operations, though fragmented, remain a profitable market. Platforms are utilizing AI for valuations to expand beyond traditional physical lot capacities. Dealer groups are also partnering with insurers to offer bundled extended warranties. Finance and insurance products tied to pre-owned purchases generate additional yield, offsetting narrower profit margins on vehicle sales. Additionally, new-vehicle dealers are increasingly operating adjacent certified lots. This approach enables them to quickly recycle trade-ins, reducing the risk of losing sales to independent e-commerce marketplaces.

By Retailer: Franchised Networks Maintain Dominance

Franchised retailers accounted for 64.47% of the Southeast Asia automotive dealership market share in 2025 and are projected to grow at a 6.21% CAGR through 2031, underscoring OEM commitment to brand-compliant environments that host EV chargers and software update zones. Multi-brand halls lower per-brand capex, and regional conglomerates leverage centralized parts warehouses to support dozens of badges with leaner inventory. Digital integration lets customers transition from the website to the showroom to the service bay under a single sign-on, bolstering retention rates.

Independent dealers excel in agility and price competition, particularly in the used-car arena. Carsome’s profitability milestone is pressuring franchised operators to match its seven-day buyback guarantees. Non-aligned outlets often pivot to niche imports or performance models excluded from franchised catalogs. As agency sales models spread, franchised groups may morph into service-centric businesses, charging OEMs for handover and maintenance while ceding transactional control.

By Vehicle Type: Commercial Vehicles Accelerate Growth

Passenger models delivered 72.63% of the Southeast Asia automotive dealership market share in 2025, reflecting urbanization and easier credit approval for sedans and SUVs. Small crossovers like the Honda HR-V attract young professionals, while entry-level hatchbacks remain staples for first-time buyers. Dealers deploy mobile sales kiosks in malls to capture impulse interest and schedule test drives.

Commercial vehicles are poised for faster expansion, with a 7.08% CAGR, as e-commerce drives demand for light trucks and electric vans. Fleet customers prioritize total cost of ownership, prompting dealers to bundle maintenance contracts and telematics to improve uptime. Integration of parts depots with warehouse districts shortens service downtime, strengthening dealer relationships with logistics firms. Passenger-to-cargo conversions also appear, with dealers retrofitting MPVs for last-mile delivery roles.

By Propulsion: Electric Vehicles Transform Market Dynamics

Internal-combustion sales accounted for 94.12% of the Southeast Asia automotive dealership market share in 2025, driven by established refueling infrastructure and lower sticker prices. Dealers still rely on gasoline models for volume incentives, but slow inventory turnover risks residual-value erosion as EV adoption rises. Battery-electric models already account for more than half of new registrations in Singapore, signaling future tipping points in other metro areas.

Electric variants expand at a 10.53% CAGR to 2031, powered by subsidies and domestic battery plants. Showrooms dedicate separate zones for live charging demonstrations and battery health reports, building consumer confidence. Hybrid traction meets transitional demand in regions with sparse charging grids. Dealers rationalize workshop layouts to segregate high-voltage service bays, ensuring technician safety and process efficiency.

Geography Analysis

Indonesia retained a 28.64% share of the Southeast Asia automotive dealership market in 2025, buoyed by a population exceeding 270 million and government incentives that attracted nine EV assembly commitments. As Chinese competitors proliferate, Astra International's market share has dipped. However, capitalizing on the Ramadan travel surge, the group has rolled out pop-up service posts and deployed roadside assistance fleets. Meanwhile, Indomobil is expanding with new outlets, strategically targeting secondary cities with growing demand, bolstered by rising disposable incomes. In the archipelago, logistics hurdles present lucrative opportunities for groups adept at integrated parts distribution, significantly reducing lead times between islands.

Both Thailand and Vietnam are driving significant momentum in the automotive sector. In Thailand, the electric vehicle program has spurred new showroom investments and a push to upskill technicians. In Vietnam, total sales have grown, with THACO boasting numerous service centers. Notably, THACO's mobile units extend their reach to the mountainous provinces. Furthermore, local component manufacturing enhances the cost competitiveness of domestically assembled Kia and Mazda vehicles, thereby bolstering dealer margins.

The Philippines has the fastest trajectory, with a 8.26% CAGR through 2031, as banks adopt data-driven credit scoring to expand vehicle loans. Sales reached significant levels, with projections indicating substantial year-over-year growth. Malaysia's pre-owned vehicle segment is driving dealerships to diversify into certified used cars, providing a buffer against stagnation in new-car sales. Singapore's strong adoption of electric vehicles (EVs) highlights a policy-driven shift and attracts cross-border shoppers seeking firsthand product experiences. Meanwhile, in emerging markets like Cambodia and Laos, an enhanced logistics corridor is boosting cross-border flows, enabling dealers to access a broader model portfolio.

Competitive Landscape

The Southeast Asia automotive dealership market is moderately concentrated, leaving ample headroom for regional consolidation. Price-led competition intensifies as Chinese OEMs scale localized production, enabling dealers to offer feature-rich models at mass-market price points. Established Japanese brands defend their market share through customer loyalty programs and residual-value guarantees, yet younger buyers are increasingly receptive to new entrants.

Dealer groups prioritize vertical integration by acquiring digital marketplaces and financing arms, thereby internalizing leads and capturing interest-income streams. PT Astra International’s used-car platform and Sime Darby Motors’ EV-charging venture exemplify strategic diversification that offsets thinner new-car margins. Data-driven CRM suites, predictive maintenance analytics, and online-to-offline purchase paths become key differentiators as consumers demand seamless experiences.

Talent shortages in EV servicing and omnichannel sales management spur cross-border recruitment and internal academy programs. Early adopters of technician upskilling and AI-assisted sales tools achieve productivity gains and higher customer satisfaction scores. Overall, the competitive dynamic rewards scale, technology adoption, and multi-segment portfolio management within the Southeast Asia automotive dealership market.

South East Asia Automotive Dealership Industry Leaders

PT Astra International Tbk

Sime Darby Motors

Cycle and Carriage

Tan Chong Motor Holdings Bhd

Inchcape plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VinFast debuted its right-hand-drive VF 6 SUV at IIMS Surabaya, unveiling 22 dealerships and 20 service centers in Indonesia with free charging through March 2028.

- January 2025: Geely Auto entered Indonesia with the pre-sale of its EX5 electric SUV, partnering locally for assembly slated in Q3 2025.

South East Asia Automotive Dealership Market Report Scope

The Southeast Asia automotive dealership market report is segmented by type (new-vehicle dealership, used-vehicle dealership, parts and service, and finance and insurance), retailer (franchised retailer and non-franchised retailer), vehicle type (passenger cars, commercial vehicles, and two-wheelers), propulsion (internal-combustion-engine and electric vehicles), and country (Indonesia, Thailand, Malaysia, Philippines, Vietnam, Singapore, and Rest of Southeast Asia). The market forecasts are provided in terms of value (USD).

| New-Vehicle Dealership |

| Used-Vehicle Dealership |

| Parts and Service |

| Finance and Insurance |

| Franchised Retailer |

| Non-franchised Retailer |

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| Internal-Combustion-Engine Vehicles |

| Electric Vehicles |

| Indonesia |

| Thailand |

| Malaysia |

| Philippines |

| Vietnam |

| Singapore |

| Rest of South East Asia |

| By Type | New-Vehicle Dealership |

| Used-Vehicle Dealership | |

| Parts and Service | |

| Finance and Insurance | |

| By Retailer | Franchised Retailer |

| Non-franchised Retailer | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheelers | |

| By Propulsion | Internal-Combustion-Engine Vehicles |

| Electric Vehicles | |

| By Country | Indonesia |

| Thailand | |

| Malaysia | |

| Philippines | |

| Vietnam | |

| Singapore | |

| Rest of South East Asia |

Key Questions Answered in the Report

What is the projected value of the South East Asia automotive dealership market in 2031?

The market is forecast to reach USD 157.18 billion by 2031.

Which country leads South East Asia in dealership revenue share?

Indonesia held the largest share at 28.64% in 2025.

How fast are electric vehicles growing in regional dealerships?

EV sales are set to rise at a 10.53% CAGR between 2026 and 2031.

How are digital platforms influencing used-car sales?

Companies like Carsome and Carro use data analytics, warranties and home delivery to professionalize the segment and divert trade-ins from traditional dealers.

What challenges do dealers face with EV adoption?

Capital outlays for charging, technician shortages, and lower routine-maintenance revenue are key hurdles.

Page last updated on: