Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

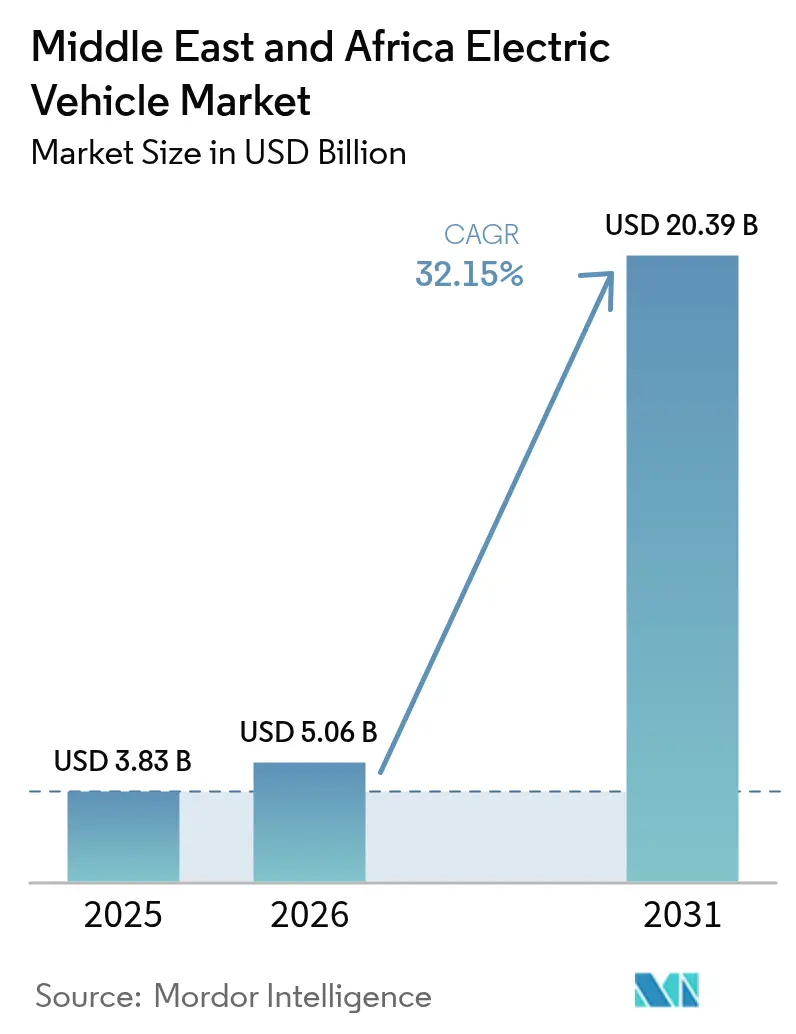

| Base Year Market Size (2025) | USD 3.83 Billion |

| Market Size (2026) | USD 5.06 Billion |

| Market Size (2031) | USD 20.39 Billion |

| Growth Rate (2026 - 2031) | 32.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Electric Vehicle Market Analysis by Mordor Intelligence

The electric vehicle market size in the Middle East and Africa was valued at USD 3.83 billion in 2025 and estimated to grow from USD 5.06 billion in 2026 to reach USD 20.39 billion by 2031, at a CAGR of 32.15% during the forecast period (2026-2031). Sovereign wealth funds are directing multibillion-dollar allocations toward domestic production ecosystems, and oil-exporting nations are leveraging abundant solar resources to lower charging costs and attract global original-equipment manufacturers (OEMs). Binding decarbonization mandates, falling battery costs, and the rollout of public fast-charging corridors reinforce demand momentum even as used internal-combustion-engine (ICE) imports remain a short-term headwind. Passenger cars retain the most extensive installed base, yet commercial fleets increasingly dominate incremental volume as oil-and-gas operators issue bulk electrification tenders. Strategic partnerships between energy majors and automakers and hot-climate battery-thermal innovations are positioning the region as a technical test bed for extreme-heat EV performance.

Key Report Takeaways

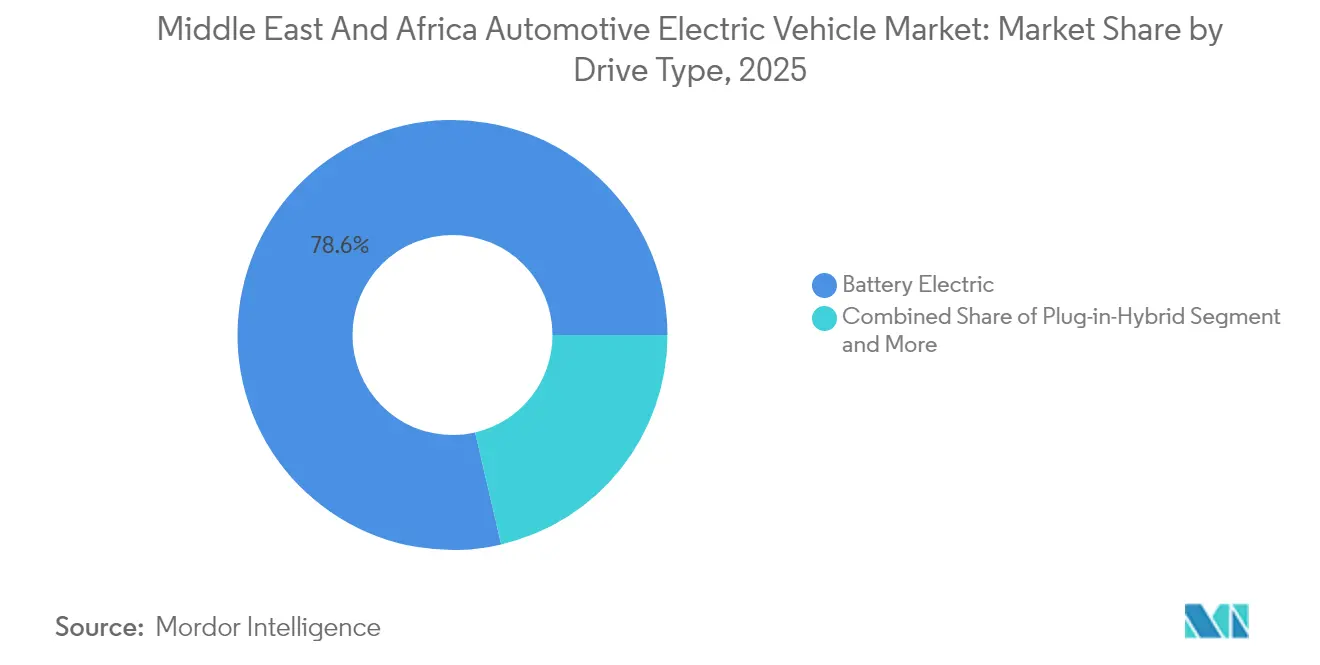

- By drive type, battery-electric vehicles held 78.64% of the Middle East and Africa automotive electric vehicle market share in 2025, while fuel-cell models are forecast to advance at a 35.90% CAGR through 2031.

- By vehicle type, passenger cars accounted for 64.05% of the Middle East and Africa automotive electric vehicle market share in 2025, and medium & heavy commercial vehicles are projected to expand at a 35.05% CAGR to 2031.

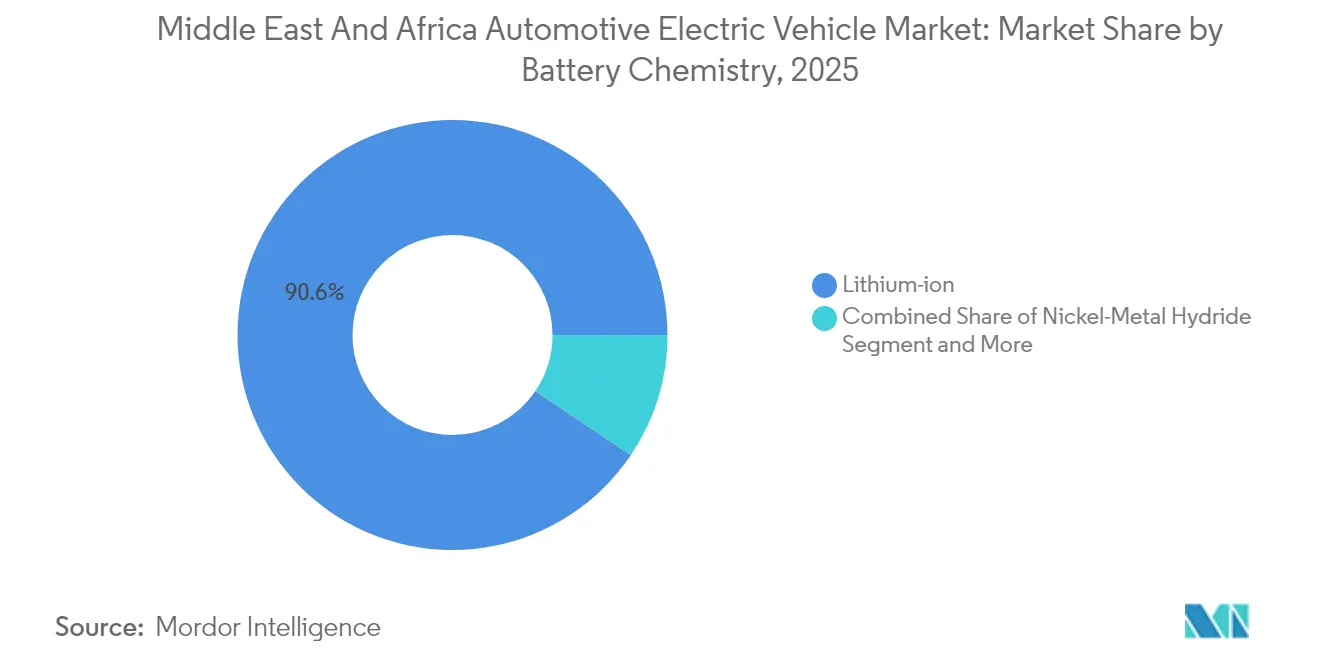

- By battery chemistry, lithium-ion captured 90.55% of the Middle East and Africa automotive electric vehicle market share in 2025, whereas “other” chemistries are poised for the fastest 39.40% CAGR through 2031.

- By charging level, AC installations below 7 kW dominated the Middle East and Africa automotive electric vehicle market share in 2025 deployments, with 50.62%; DC fast chargers above 22 kW are expected to climb at a 38.95% CAGR over the forecast horizon.

- By country, the UAE led with a 32.20% of the Middle East and Africa automotive electric vehicle market share in 2025, and Saudi Arabia is projected to record the highest 32.10% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization Mandates and ICE Bans | +8.2% | GCC, Egypt, South Africa | Medium term (2-4 years) |

| DC Fast-Charger Corridor Rollout | +6.3% | Saudi Arabia, UAE, Morocco | Medium term (2-4 years) |

| EV Import Subsidies And Zero Duties | +5.7% | UAE, Saudi Arabia, Qatar, Oman | Short term (≤ 2 years) |

| Falling Battery Costs And Longer Range | +4.9% | Global spillover to MENA | Long term (≥ 4 years) |

| Solar Surplus And Low-Tariff Charging | +4.4% | MENA & Sub-Saharan Africa | Long term (≥ 4 years) |

| Oil And Gas Fleet Electrification | +3.8% | Saudi Arabia, other GCC members | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Decarbonization Mandates and ICE-Ban Targets

Gulf Cooperation Council (GCC) members have embedded electric-mobility quotas into national development agendas, creating demand floors that anchor OEM investment decisions. Saudi Arabia’s Vision 2030 compels 30% of Riyadh’s vehicles to be electric by 2030, while the UAE’s federal strategy targets a 50% electric-vehicle mix by 2050[1]“UAE Net-Zero Strategy,”, UAE Ministry of Industry & Advanced Technology, moiat.gov.ae. These directives funnel public-sector procurement toward zero-emission models, catalyze private-sector fleet conversions, and standardize certification under Gulf Standardization Organization (GSO) rules, which ease cross-border trade. Morocco’s mandates 2,500 charging points by 2026, illustrating how firm policy anchors accelerate infrastructure scale-up. Binding targets dovetail with COP28 commitments, giving investors long-cycle visibility, compensating for initial demand volatility.

Rapid Rollout of Public DC Fast-Charging Corridors

Intercity fast-charging corridors convert EVs from urban runabouts into region-wide mobility options. EVIQ’s flagship 150 kW site on the Riyadh–Qassim motorway demonstrates highway viability and signals forthcoming coverage of the kingdom’s 10 busiest arterial routes. In parallel, the UAE plans 70,000 public chargers across Abu Dhabi by 2030, while Dubai targets 1,000 sites by 2025, effectively eliminating intra-emirate range anxiety[2]“Green Charger Initiative,”, DEWA, dewa.gov.ae. Morocco’s plan links Casablanca, Rabat, and Tangier with green-energy-powered DC units that supply sub-30-minute stops. Nigeria’s 2025 inauguration of West Africa’s largest assembled charging hub widens the infrastructure map to frontier markets. Corridor density materially lifts commercial-vehicle uptime, unlocking electrification for freight operators serving ports such as Jebel Ali.

Day-Time Solar-PV Surplus Driving Ultra-Low-Cost Charging Tariffs

With levelized solar costs already under USD 0.02 per kWh in parts of MENA, midday generation surpluses have opened a pathway to sub-USD 0.10 / L-gasoline-equivalent charging tariffs. Saudi Arabia aims for 58.7 GW of renewables by 2030, aligning solar peaks with workplace-charging demand[3]“Solar PV in MENA,”, International Energy Agency, iea.org. Morocco’s renewables-backed Tangier-Kenitra automotive zone feeds car plants and charging forecourts from the same grid, erasing fossil-linked price volatility. Vehicle-to-grid programs in Jordan and Israel now monetize idle battery storage during evening peaks, creating ancillary revenue streams that sweeten fleet business cases.

Oil-and-Gas Fleet-Electrification Pledges Unlocking Bulk Orders

Hydrocarbon producers increasingly hard-wire sustainability into capital plans, spawning predictable multi-thousand-unit purchase orders that justify local assembly lines. Aramco’s acquisition of 10% of HORSE Powertrain Limited for EUR 7.4 billion (USD 8.1 billion) facilitates hybrid and battery-electric conversion [4]“Investment in HORSE Powertrain,”, Aramco, aramco.com. Saudi hydrogen pilots expand the business case to fuel-cell trucks servicing refinery clusters. Similar pledges by ADNOC, ENOC, and Sonangol are enlarging the regional addressable fleet pool beyond passenger cars. These enterprise contracts shorten OEM payback periods, lowering break-even volumes for Saudi Arabia’s Ceer, Turkey’s Togg, and Hyundai-PIF’s new King Abdullah Economic City plant.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Price and Weak Financing | -4.8% | Africa, lower-income MENA markets | Short term (≤ 2 years) |

| Cheap Used ICE Imports | -3.7% | Africa, with spillover to MENA | Long term (≥ 4 years) |

| Limited Hot-Climate EV Models | -3.2% | GCC countries, North Africa | Medium term (2-4 years) |

| Grid Unreliability and Charger Downtime | -2.9% | Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Vehicle Price and Limited Consumer Financing

Purchase-price premiums continue to deter mass-market adoption in lower-income segments even as batteries cheapen. Egypt’s EV share remains just 0.1% of new-car sales due to limited installment plans and hard-currency outlays that expose buyers to exchange-rate swings. Traditional lenders, accustomed to securitizing used imports, lack residual-value benchmarks for electric vehicle market loans, inflating interest spreads. In Sub-Saharan Africa, microfinance mechanisms target two-wheeler taxis rather than four-wheeler purchases, further stalling scale economics for OEMs.

Influx of Cheap Used ICE Imports Undermines EV Demand

Eighty-five percent of Africa’s circulating fleet comprises second-hand ICE vehicles shipped from stricter-emission jurisdictions, maintaining a low-price alternative that undercuts new EVs [5]“Used Vehicle Imports in Africa,”, United Nations Environment Programme, unep.org. Loosely enforced age caps in markets like Nigeria and Benin prolong the diesel influx, weakening policy-driven electrification signals. This saturation compresses residual-value forecasts for new models, complicating lease and loan product design. Regulatory fragmentation also impedes harmonized scrap and recycling standards, allowing high-emission units to cross borders and dilute air-quality gains promised by the electric vehicle market. Policymakers in Kenya and Ghana have begun tightening import-age ceilings, but enforcement capacity remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: Battery-Electric Vehicles Consolidate Dominance

Battery-electric vehicles (BEVs) commanded 78.64% of the electric vehicle market share in 2025, validating the region’s preference for fully electric drivetrains and sidestepping the fuel-duty complexity of plug-in hybrids. BEV appeal stems from simpler maintenance and the rollout of destination chargers at malls, airports, and industrial parks. The segment’s robust margin structure has enticed Tesla, BYD, and Geely to launch direct-to-consumer sales portals that bypass traditional dealerships.

Fleet operators adopt BEVs for depot-night charging, reducing daytime operational disruptions. Fuel-cell electric vehicles post a 35.90% CAGR through 2031 as Saudi Arabia scales green-hydrogen refueling nodes around its industrial corridors, underscoring their long-haul potential. Meanwhile, plug-in hybrids remain transitional, offering range security where grid reliability lags. The drive-type mix therefore mirrors infrastructure maturity, with BEVs prevailing in the urban Gulf and fuel-cells rising along desert freight links.

By Vehicle Type: Commercial Fleets Gain Share Momentum

Passenger cars controlled 64.05% of 2025 revenue, yet medium and heavy commercial vehicles are forecast to outpace with a 35.05% CAGR to 2031, expanding the electric vehicle market size in corporate procurement channels. Oil-field service trucks and last-mile delivery vans accrue higher daily mileage, magnifying fuel savings and carbon audit benefits. Logistics firms in the Jeddah free zone now specify electric models in tenders to comply with port authority emissions limits. Bus electrification pilots in Cairo and Cape Town indicate growing public-transport appetite, while ride-hailing operators deploy small hatchback EVs to meet city-center clean-air mandates. OEMs are responding with region-tuned payload ratings, enhanced cabin HVAC, and reinforced suspensions for unpaved routes. As commercial volumes climb, supply-chain localization deepens because truck bodies, battery enclosures, and telematics services can all be sourced domestically.

By Battery Chemistry: Lithium-Ion Retains Supremacy Amid Emerging Alternatives

Lithium-ion technologies captured 90.55% of 2025 sales and underpin the current electric vehicle market size due to mature supply chains and favorable energy-density-to-cost ratios. Morocco’s fast-growing cathode-materials cluster and UAE-based cell-pack assemblers shorten lead times and reduce import duties. However, sodium-ion and lithium-iron-manganese-phosphate (LFMP) chemistries are gaining ground, driving a 39.40% CAGR in the “other” category through 2031. These chemistries reduce cobalt dependency and offer superior thermal tolerance for Gulf summers, aligning with OEM ambitions to cut material volatility. Recycling capacity expansions in South Africa and Bahrain aim to recover nickel and manganese, supporting a circular ecosystem. Nickel-metal hydride batteries continue in hybrid niches where cost is paramount, particularly in lower-income North-African fleets. Overall, chemistry diversification lowers supply-security risks and encourages domestic R&D investments.

By Charging Level: Fast-Charging Surge Reinforces Intercity Viability

AC units below 7 kW represented 50.62% of the the installed base in 2025, reflecting home-garage and workplace dominance during the early adoption phase of the electric vehicle market. Nonetheless, DC fast chargers exceeding 22 kW are projected to have a 38.95% CAGR by 2031 as governments co-finance highway corridors. Saudi Arabia’s plan for 5,000 high-power plugs will fill desert gaps and relay trucks between ports and inland dry docks. Emerging megawatt-scale systems support heavy-duty rigs, trimming recharge downtime to mandated driver-rest windows. Solar-roof canopies and grid-storage batteries offset peak-time draws, demonstrating integrated energy-mobility business models. Semi-fast AC (7–22 kW) bridges suburban malls and fleet depots where dwell times sit below eight hours. The charging-mix evolution thus underpins mass adoption by matching dwell patterns across user segments.

Geography Analysis

The UAE held 32.20% of 2025 sales, testimony to early infrastructure, streamlined import duties, and affluent buyers willing to pay premiums for advanced infotainment packages. Dubai Electricity and Water Authority’s target of 42,000 on-road EVs by 2030 cements a flywheel where charging density and consumer uptake reinforce each other. Saudi Arabia’s 32.10% CAGR through 2031 reflects Vision 2030’s USD 39 billion ecosystem investment spanning mining, cathode materials, and final vehicle assembly. Egypt is positioning itself as an export base to Africa and Europe by targeting over 60% of local content, which is helped by free-trade access to EU markets. Morocco leverages its rail-connected Atlantic ports for battery precursor exports, while South Africa banks on automotive tooling expertise to capture drivetrain and thermal-management contracts. Israel’s software sector supplies battery analytics firmware, widening the region’s value-chain spectrum.

North Africa is maturing into a dual manufacturing-and-demand hub. Morocco targets 100,000 EV units by 2025 and 2,500 public chargers by 2026, using integrated supply parks that bundle battery precursors, vehicle assembly, and export logistics. Egypt’s CKD partnerships with Chinese OEMs aim at 30,000-unit annual lines in Giza, leveraging Suez-Canal proximity for export flow. Tunisia and Algeria are drafting net-zero roadmaps that earmark fiscal credits for R&D spend, intending to piggyback on Morocco’s established export lanes.

Sub-Saharan Africa remains nascent but strategically important for minerals. South Africa’s seasoned auto workforce, coupled with nickel and manganese reserves, positions the country for component clusters once grid stability improves. Kenya, Ghana, and Nigeria deploy policy toolkits such as duty rebates, assembly credits, and state-backed lease schemes to stimulate adoption amid used-car dominance. Zimbabwe’s lithium and the Democratic Republic of Congo’s cobalt reserves anchor upstream leverage, but road networks and port congestion still curb cost-effective extraction logistics. Regional development banks are stepping in with concessional lines for charging and grid reinforcement.

Competitive Landscape

The electric vehicle market exhibits moderate concentration as global titans blend with sovereign-backed newcomers. BYD logged CNY 777.1 billion (USD 107.2 billion) in 2024 revenue and shipped 4.27 million units, setting the performance benchmark for Asia-to-Gulf exports. Hyundai and Saudi Arabia’s Public Investment Fund have earmarked USD 500 million for a 50,000-unit King Abdullah Economic City plant, marrying Korean drivetrain IP with local workforce incentives. Tesla maintains a showroom presence in Dubai and a concierge delivery model for Riyadh, though it has yet to localize assembly.

Regional startups inject competitive spice. Ceer targets 30,000 jobs and multiple crossover models by 2034, leveraging Foxconn’s MIH platform and Siemens’ digital-twin design suite. Turkey’s Togg is finalizing GCC homologation and eyeing Saudi distribution partners. Strategic tie-ups are proliferating: Aramco’s EUR 7.4 billion (USD 7.8 billion) stake in HORSE secures hybrid propulsion optionality, while ADNOC collaborates with NIO on battery-swap depots in Abu Dhabi industrial zones. OEMs differentiate through desert-tuned HVAC, battery-cooling trickery, and IoT-based predictive maintenance.

Competition also plays out in charging and software ecosystems. DEWA’s “EV Green Charger” network grants loyalty credits redeemable on utility bills, whereas EVIQ bundles subscription charging for Saudi fleet operators. Israeli startups offer over-the-air battery-health analytics now embedded by Chinese automakers to enhance residual-value assurances. Taken together, the market’s competitive theater spans hardware, energy integration, and digital services—broadening consumer choice while compressing incumbents’ price umbrellas.

Middle East And Africa Electric Vehicle Industry Leaders

Volkswagen AG

Nissan Motor Co. Ltd

Hyundai Motor Company

Tesla Inc.

BYD Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BYD launched three EV models in South Africa (SHARK 6, SEALION 6, SEALION 7), widening its African footprint.

- June 2025: Sino-Moroccan COBCO began local production of EV battery materials, reinforcing Morocco’s supply-chain depth.

- May 2025: Hyundai commenced construction of an additional Saudi EV assembly line aligned with Vision 2030 goals.

- April 2025: Aramco and BYD unveiled a technology partnership focused on new-energy vehicles.

Middle East And Africa Electric Vehicle Market Report Scope

An electric vehicle (EV) operates on an electric motor instead of an internal combustion engine that generates power by burning a mix of fuel and gases. Therefore, such a vehicle is seen as a possible replacement for current-generation automobiles to address rising pollution, global warming, depleting natural resources, etc.

The Middle East electric vehicle market is segmented into drive type, vehicle type, and geography. Based on the drive type, the market is segmented into plug-in hybrid and pure electric. Based on vehicle type, the market is segmented into passenger cars and commercial vehicles. Based on geography, the market is segmented into the United Arab Emirates, Saudi Arabia, Egypt, and the Rest of the Middle East. The report offers market size and forecasts for all the above segments in value (USD).

By Drive Type

| Battery-Electric (BEV) |

| Plug-in Hybrid (PHEV) |

| Fuel-Cell Electric (FCEV) |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| Two and Three Wheelers |

By Battery Chemistry

| Lithium-ion (NMC / NCA / LFP) |

| Nickel-Metal Hydride |

| Others |

By Charging Level

| AC below 7 kW (Slow) |

| AC above 7 kW - 22 kW (Semi-fast) |

| DC above 22 kW (Fast / Ultra-fast) |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Israel |

| Egypt |

| South Africa |

| Nigeria |

| Kenya |

| Qatar |

| Oman |

| Rest of Middle East and Africa |

| By Drive Type | Battery-Electric (BEV) |

| Plug-in Hybrid (PHEV) | |

| Fuel-Cell Electric (FCEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches | |

| Two and Three Wheelers | |

| By Battery Chemistry | Lithium-ion (NMC / NCA / LFP) |

| Nickel-Metal Hydride | |

| Others | |

| By Charging Level | AC below 7 kW (Slow) |

| AC above 7 kW - 22 kW (Semi-fast) | |

| DC above 22 kW (Fast / Ultra-fast) | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Kenya | |

| Qatar | |

| Oman | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa electric vehicle market in 2031?

The market is forecast to reach USD 20.39 billion by 2031, expanding at a 32.15% CAGR.

Which country currently leads regional EV adoption?

The UAE commanded a 32.20% revenue share in 2025 thanks to dense charging infrastructure and import-duty relief.

Which vehicle category is expected to grow fastest by 2031?

Medium and heavy commercial vehicles are set to grow at a 35.05% CAGR as fleet operators electrify trucks and buses.

How significant is lithium-ion technology in regional battery supply?

Lithium-ion batteries accounted for 90.55% of 2025 sales and remain the dominant chemistry despite emerging alternatives.

Which policy lever most accelerates consumer uptake in GCC markets?

Subsidies and near-zero customs duties sharply reduce upfront prices, tipping total cost of ownership in favor of EVs.

Page last updated on: