Mexico E-commerce Warehouse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

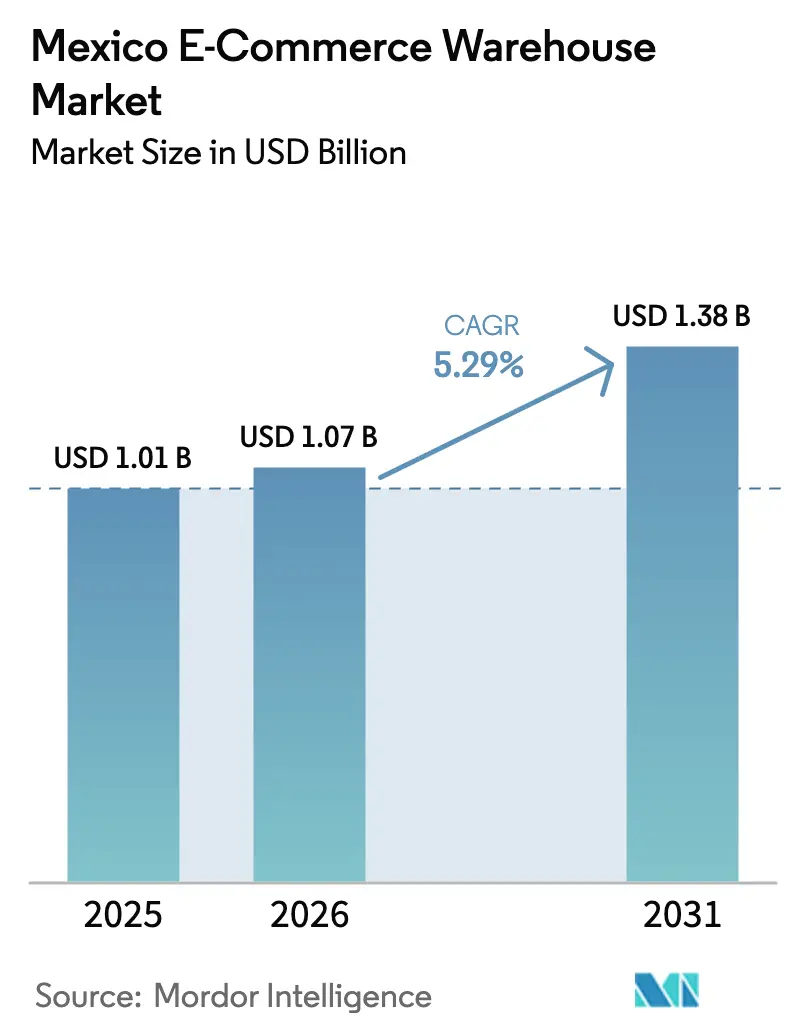

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

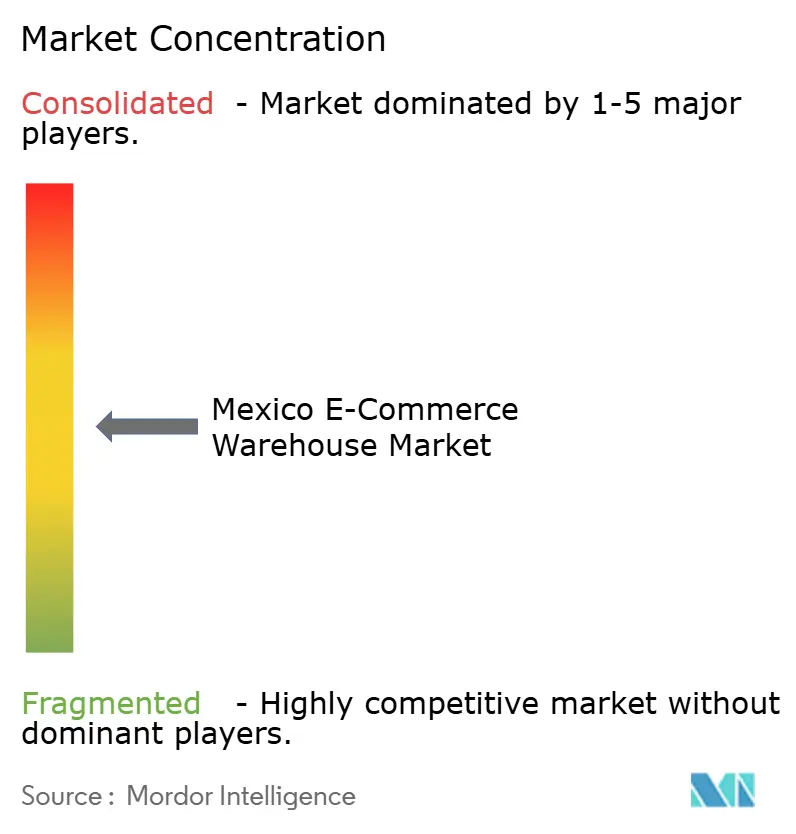

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico E-commerce Warehouse Market Analysis by Mordor Intelligence

The Mexico E-commerce Warehouse Market size is projected to expand from USD 1.01 billion in 2025 and USD 1.07 billion in 2026 to USD 1.38 billion by 2031, registering a CAGR of 5.29% between 2026 to 2031.

Favorable trade rules, mobile-first shopping behavior, and soaring digital-wallet usage are redefining how operators choose locations, configure inventories, and deploy automation. Smartphone penetration climbed to 76% in 2024, and mobile devices already drive 68% of all online purchases, pushing demand toward micro-fulfillment nodes located inside large metropolitan areas. Digital wallets and the rapid emergence of Buy-Now-Pay-Later (BNPL) products are removing cash-on-delivery frictions for a growing segment of online shoppers and cutting cart-abandonment rates, thereby lifting warehouse throughput requirements. Customs modernization under the “Despacho 24 Horas” program now clears air freight in under 24 hours, spurring airport-adjacent distribution centers and shortening order cycles. Meanwhile, federal tax credits for green buildings are steering developers toward energy-efficient, LEED-certified facilities, helping operators rein in long-term operating costs.[1]U.S. Green Building Council, “LEED in Latin America,” usgbc.org

Key Report Takeaways

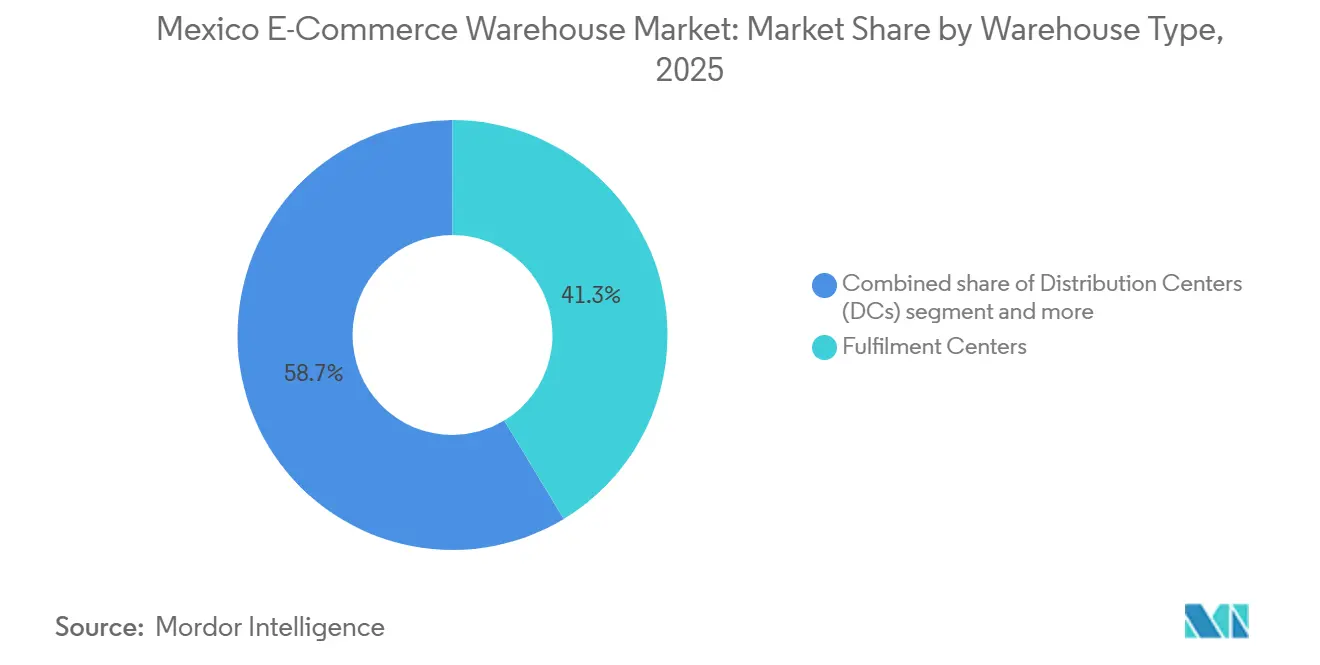

- By warehouse type, fulfillment centers captured 41.34% of the Mexico E-commerce Warehouse Market share in 2025, and dark stores and micro-fulfillment centers are projected to grow at 10.53% CAGR between 2026 and 2031.

- By service type, storage services held 42.6% of the Mexico E-commerce Warehouse Market size in 2025, and value-added services are forecast to advance at a 10% CAGR over 2026-2031.

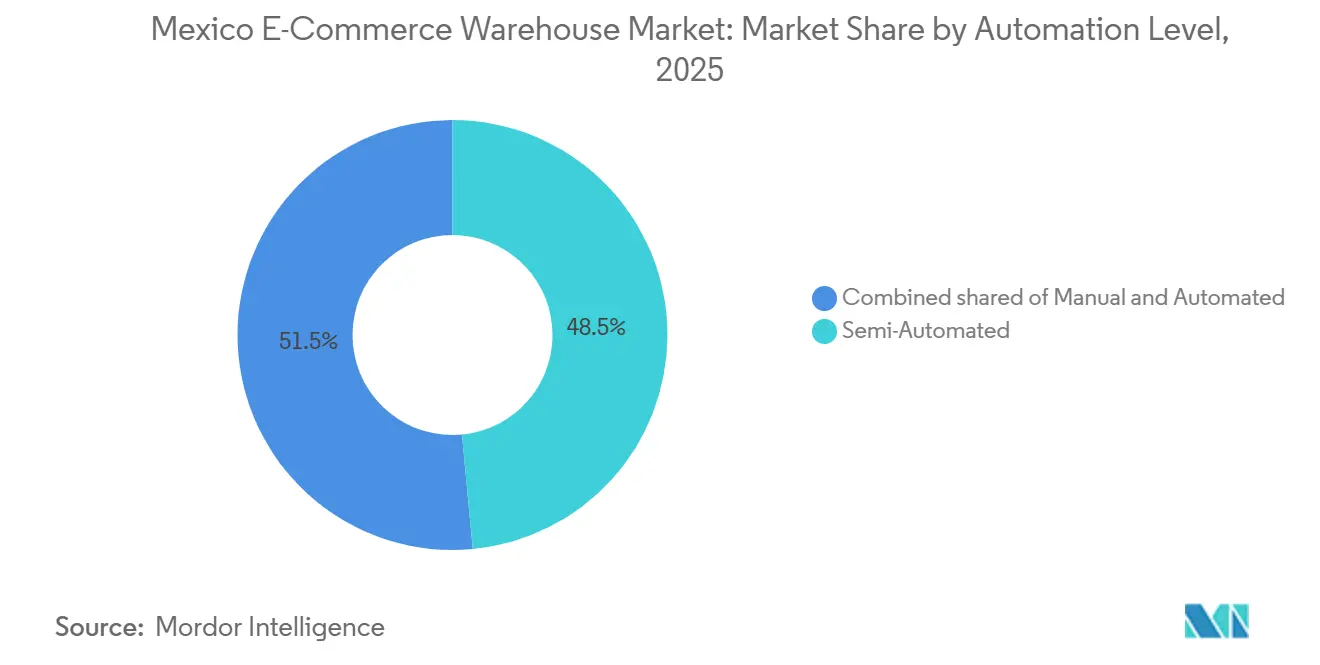

- By automation level, semi-automated facilities represented 48.5% of the market in 2025, and fully automated warehouses are on track for a 9.61% CAGR during 2026-2031.

- By End-user industry, grocery and fast-moving consumer goods (FMCG) commanded 27.89% of the 2025 demand, and pharmaceuticals, beauty, and wellness should accelerate at a 10.11% CAGR out to 2031.

- By region, Nuevo Leon contributed 28.91% of 2025 revenue, and Queretaro is anticipated to expand at a 7.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico E-commerce Warehouse Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-Commerce Driven Order Surge | +1.4% | National, high in Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Fintech Wallets & BNPL Adoption | +1.1% | National, urban concentration | Medium term (2-4 years) |

| USMCA De-Minimis Thresholds | +0.8% | Border states, major customs hubs | Medium term (2-4 years) |

| “Despacho 24 Horas” Fast-Release Program | +0.7% | Airport zones in Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Federal Green-Warehouse Tax Credits | +0.5% | Nationwide; early take-up in Querétaro, Jalisco | Long term (≥ 4 years) |

| Social-Commerce Flash-Sale Models | +0.6% | Urban centers with strong social-media use | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mobile-Commerce Driven Order Surge

Mexico’s 76% smartphone penetration and 68% mobile share of online transactions have shifted buying toward smaller baskets ordered more often, forcing warehouse operators to install dense networks of micro-fulfillment sites inside city limits. Order frequency climbed 47% on mobile channels, making pick-rate efficiency and rapid replenishment critical. Quick-commerce specialists now position inventory within 2 hours of the end customer, and many keep 15-20% extra safety stock to absorb sudden viral demand. These changes also heighten demand for value-added services such as gift wrapping and same-day returns processing. Collectively, mobile-commerce dynamics accelerate the push toward distributed, tech-enabled facilities.

Fintech Wallets and BNPL Adoption Boosting Basket Conversion

Digital wallets reached 42% of shoppers in 2025, while BNPL continues to accelerate its share of checkouts, collectively shrinking cash-on-delivery dependence and driving a rise in warehouse throughput. Installment plans encourage higher-ticket purchases in electronics and home goods, broadening SKU complexity inside facilities. The fall in cash handling trims failed deliveries by nearly one-third, improving inventory turns and lowering working-capital needs. Loyalty programs built into wallet apps create more predictable demand, letting operators cut safety stock by as much as 15%. Cross-border merchants gain most, because frictionless peso-dollar payments widen their reachable customer base.

USMCA De-Minimis Thresholds Streamlining Reverse Logistics

The USMCA framework has modernized cross-border returns by allowing sellers to leverage Mexico’s USD 117 duty-free ceiling for southbound imports and the USD 800 US de minimis threshold to recover merchandise duty-free[2].U.S. Customs and Border Protection, “USMCA De-Minimis Rules,” cbp.gov Within Mexico, e-commerce leaders like Amazon and Mercado Libre have embedded advanced triage and refurbishment zones into their mega-hubs in Nuevo León and Querétaro. These localized hubs provide a disproportionate advantage for processing high-return categories such as apparel and electronics, which routinely experience return rates of 18 to 25%. Through effective sorting and secondary-market resale, operators can now recover a substantial portion of the merchandise value that was previously discarded as a financial loss. As a result, third-party logistics specialists focused on warranty management, component harvesting, and refurbishment are rapidly scaling to meet the escalating demands of this reverse-logistics niche.

“Despacho 24 Horas” Fast-Release Fueling Airport E-DC Demand

The Servicio de Administración Tributaria (SAT) slashed average air-cargo clearance from 3-5 days to under 48 to 72 hours, spurring a wave of airport-proximate distribution centers despite rents that sit 25-35% above suburban industrial parks.[3]Servicio de Administración Tributaria, “Despacho 24 Horas Operational Report,” sat.gob.mx Electronics and beauty brands accept the premium to guarantee next-day delivery, and some global sellers even bypass sea freight entirely, shipping direct from Asia into Mexico by air and flowing product straight through these centers. Bonded facilities offering automated documentation now post 95% first-pass clearance, turning customs speed into a competitive weapon. The model also favors high-value items where inventory velocity outweighs transport cost.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Road Congestion Around Key Metros | -0.9% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Peso Exchange-Rate Volatility | -0.7% | Nationwide; acute in cross-border trade | Medium term (2-4 years) |

| Water-Use Quotas at Industrial Parks | -0.5% | Bajío region, northern states | Long term (≥ 4 years) |

| Limited Tier-III Data-Center Grid Capacity | -0.4% | Secondary markets outside the three largest metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Road Congestion Around Key Metros Inflating Last-Mile Costs

Average speeds in Mexico City, Guadalajara, and Monterrey fall to 12-15 km/h during peaks, double or triple delivery times, and inflate last-mile costs by up to 25% compared with secondary locales. Vehicle-restriction programs such as “Hoy No Circula” remove 20% of fleets from the road one day each week, compelling operators to keep idle capacity that ties up capital. Many firms now deploy satellite micro-fulfillment hubs despite rent that can be 60% higher than suburban plots, betting that proximity offsets traffic delays. Route-optimization software and electric cargo bikes lessen emissions but introduce new cost layers. Failure rates on same-day promises climb to nearly 20% during peak congestion.

Peso Exchange-Rate Volatility Complicating Inventory Valuation

The peso swings an average of 12% per year against the US dollar, eroding margins on imported stock if rates move adversely between purchase and sale dates. Long-cycle inventory, such as furniture, is especially exposed, prompting larger platforms to adopt dynamic pricing algorithms tied to real-time FX data. Hedging tools like forwards and options shield some risk but add up to 3% to landed costs. Smaller operators lacking treasury expertise often accept thinner spreads or shorten assortment cycles. Returns processed months later must also be re-valued, adding accounting complexity and impacting refund timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Fulfilment Centers Anchor National Networks

Fulfillment centers held 41.34% of the Mexico E-commerce Warehouse Market size in 2025, reflecting their role as multi-channel hubs that consolidate cross-border imports and domestic inventory for both business-to-consumer (B2C) and business-to-business (B2B) flows. These large facilities typically exceed 500,000 sq ft, and host advanced warehouse-management systems (WMS) that push average picking productivity above 140 lines per hour. Operators favor border-state clusters such as Nuevo León because they combine inland-port rail access with four-lane highway links to Mexico City in under ten hours, keeping national service times competitive. Rental rates average USD 7 per sq ft in Class A parks, yet tenants accept the premium because centralized stock lets them hedge currency swings by pooling safety inventory.

Dark stores and micro-fulfillment centers are the fastest-growing cohort, set to climb at a 10.53% CAGR through 2031. Positioned within 5 km of dense urban consumers, these sites support 15 to 30 minute delivery promises popularized by social-commerce flash sales. Facility footprints rarely exceed 10,000 sq ft, but inventory turns reach 8 to 12 per month, double typical fulfillment-center velocity freeing working capital. Operators deploy autonomous mobile robots (AMRs) that cost USD 25,000 to 30,000 each and lift labor productivity by 60%, a critical lever as Mexico’s warehouse wages climb 8-10% annually. Land shortages inside Mexico City have triggered multistory dark-store conversions of disused retail space, a trend likely to sustain outsized rental growth in prime ZIP codes.

By Service Type: Storage Dominates, Value-Added Services Accelerate

Storage services accounted for 42.6% of the Mexico E-commerce Warehouse Market size in 2025 as virtually every online order, regardless of speed or channel, still needs pallet or bin space Leading operators currently charge USD 15 to 22 per pallet a month in primary metros, with cold-room surcharges typically adding 25 to 35% to the base rate for goods requiring 2–8 °C integrity. High utilization surpassing the 85 to 90% efficiency threshold has triggered widespread investment in mezzanine installations and high-density automated storage (AS/RS) to expand cubic capacity without the lead times of greenfield development.

Value-added services (VAS), including kitting, customization, and localized packaging, are the primary profit drivers for 3PLs, projected to grow at a 10 % CAGR through 2031. In the beauty sector, on-site clean rooms for influencer sets and "viral SKU" assembly allow for rapid market entry, often capturing 20% price premiums. Pharmaceutical logistics, governed by strict Good Distribution Practice (GDP) rules, require serial-number aggregation and continuous thermal monitoring, commanding 35 to 50% mark-ups over standard ambient storage. To meet sustainability targets and combat rising freight costs, warehouses are increasingly adopting on-demand packaging technology. These systems reduce box void space by an average of 20 to 30%, leading to a correlated 5 to 10% reduction in outbound shipping costs by optimizing dimensional weight (DIM) charges.

By Automation Level: Robotics Become Standard

Semi-automated facilities owned 48.5% of the Mexico E-commerce Warehouse Market share in 2025, balancing conveyor systems, RF scanners, and WMS software with human labor for complex picking. This hybrid model strongly suits Mexico’s mid-scale operations, maintaining an attractive payback period even as robotics prices fall. Meanwhile, labor-only sites persist, especially among regional third-party logistics (3PL) providers that win contracts on price and absorb seasonal fulfillment peaks using temporary staff.

Fully automated warehouses, projected to post a 9.61% CAGR, driven by two converging forcessuch as a steady, mandated rise in baseline warehouse wages and the need to eliminate margin-sapping picking errors in sensitive sectors like pharmaceuticals and consumer electronics. Major enterprise retailers are increasingly deploying automated storage and retrieval systems to drastically reduce order fulfillment times and significantly improve overall order accuracy compared to legacy manual processes. Robotics vendors, eager to penetrate Latin America, are offering lease-to-own packages that align monthly fees with labor savings, easing the capital expenditure barriers for local 3PLs. Nonetheless, a severe shortage of specialized robotics technicians who command a steep wage premium over manual operators may slow widespread adoption outside of the major metropolitan areas.

By End-User Industry: Grocery Retains Prime Share

Grocery and fast-moving consumer goods (FMCG) contributed 27.89% of 2025 demand, buoyed by platforms such as Justo and the expansion of quick-commerce on major delivery apps that now offer fresh, ambient, and frozen assortments under strict delivery guarantees. To hit freshness targets, operators segment warehouses into three temperature zones and use cross-docks that merge vendor-delivered produce with in-house inventory minutes before dispatch. National retailers such as OXXO have also converted 20,000 convenience stores into neighborhood pick-up points, easing last-mile density constraints.

Pharmaceuticals, beauty, and wellness will expand at a brisk 10.11% CAGR through 2031. Mexican health agency COFEPRIS tightened GDP audits in 2025, pushing companies to install redundant temperature loggers, shock sensors, and comprehensive security surveillance across all sensitive storage areas. The beauty sector adds a customization twist. Social commerce sellers now increasingly demand rapid-turnaround value-added services like gift wrapping and influencer co-branding, incentivizing warehouses to integrate light manufacturing cells. BNPL usage lifts average ticket sizes for personal-care devices by 35%, deepening fulfillment volumes without comparable head-count jumps.

Geography Analysis

Nuevo Leon generated 28.91% of Mexico E-commerce Warehouse Market revenue in 2025, a lead it owes to nearshoring inflows that pumped record-breaking levels of manufacturing FDI into the state. The state’s Interpuerto rail hub speeds containerized imports from Laredo, Texas, to the rest of the country in under 24 hours, positioning local warehouses as cross-border gateways. Warehouse clusters along Highway 85 operate at a tight 96% occupancy, nudging annual rents to USD 6.20 per sq ft.

Jalisco and Estado de Mexico together account for another quarter of the Mexico E-commerce Warehouse Market, thanks to Guadalajara’s electronics corridor and the State of Mexico’s proximity to 22 million consumers in the capital. Guadalajara’s airport freight volumes jumped 18% year on year after “Despacho 24 Horas” rolled out, prompting major international logistics providers to heavily invest in expanding their automated sorting capacities within the region to keep pace with demand. Toluca’s industrial parks, 60-90 minutes from Mexico City, remain a cost-effective fallback for tenants squeezed by urban land scarcity, with land prices still 40-50% lower than inside the federal district.

Queretaro stands out as the fastest-growing region, forecast at a 7.79% CAGR to 2031. Its international airport has experienced a massive surge in air cargo volumes, driving regional authorities to advance plans for a new cargo terminal that will significantly increase throughput capacity over the next few years.[4]Grupo Aeroportuario del Centro Norte, “Querétaro Cargo Expansion,” oma.aero Airport-adjacent warehouses rent for a premium often reaching USD 8 per sq ft yet tenants accept the markup to guarantee 48-hour delivery on high-value imports. Water-use quotas in Bajío industrial parks create headwinds, but developers respond with rain-harvesting roofs that recoup added costs via federal green-building tax breaks.

Competitive Landscape

The Mexico E-commerce Warehouse Market remains moderately fragmented; the five largest providers hold only 35–40% combined share, leaving ample room for specialists. Global integrators such as DHL, FedEx, UPS, and CEVA leverage multiregional IT platforms and air-express capacity, letting them promise rapid delivery across the vast majority of the country's population centers. Domestic champions such as Grupo Traxion and Solistica counter with denser last-mile fleets and local zoning savvy, translating into faster permits for urban dark stores.

Technology is the new battleground. Operators with predictive inventory engines are drastically reducing stockout rates and raising client retention. DHL’s USD 120 million Querétaro hub embeds automated sorters that process 41,000 parcels an hour, a scale unmatched by local peers. Mercado Libre, meanwhile, invests USD 300 million in Hidalgo to safeguard fulfillment independence amid Temu and Shein’s push into Mexico. New entrants are building multi-level urban warehouses that maximize vertical space to counter severe land scarcity in Mexico City.

Vertical specialization is ripening. 3PLs focused solely on pharmaceuticals install redundant power and dual-temperature vaults to capture wellness demand. Reverse-logistics experts cluster in border states where USMCA de minimis rules erase duty on returns, recovering a substantial portion of merchandise value. Green-warehouse developers attract multinational tenants with ESG targets, leveraging tax credits that shorten depreciation cycles. As automation spreads, third-party robotics-maintenance firms emerge, selling subscription service packages that offer high-reliability system uptime guarantees.

Mexico E-commerce Warehouse Industry Leaders

DHL Supply Chain

GXO Logistics

DSV

Kuehne Nagel

CMA CGM Group (Including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Traxión issued MXN 2.0 billion (USD 0.11 billion) in local bonds to fund fleet renewals, technology investments, and strategic growth across its Mexican logistics and e-commerce warehousing operations.

- January 2026: FedEx filed to officially spin off FedEx Freight into the largest standalone North American LTL carrier to aggressively target high-growth cross-border and B2B logistics.

- January 2026: DSV broke ground on a 950,000-square-foot regional logistics headquarters in Mesa, Arizona, representing a USD 14.5 million investment.

- March 2025: Amazon unveiled a USD 6 billion plan to add mega-sites in Nuevo León and Jalisco, each designed for 900,000 daily picks, to widen same-day coverage.

Mexico E-commerce Warehouse Market Report Scope

| Fulfilment Centres |

| Distribution Centres (DCs) |

| Cold-Chain Warehouses |

| Dark Stores / Micro-Fulfillment Centers |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.) |

| Storage |

| Picking and Packing |

| Value-Added Services and Others (Kitting, Labelling) |

| Manual |

| Semi-Automated |

| Automated |

| Apparel and Footwear |

| Consumer Electronics |

| Grocery and FMCG |

| Pharmaceuticals, Beauty and Wellness |

| Home Essentials and Furnishings |

| Others |

| Mexico (State of Mexico) |

| Nuevo Leon |

| Jalisco |

| Queretaro |

| Rest of the States |

| By Warehouse Type | Fulfilment Centres |

| Distribution Centres (DCs) | |

| Cold-Chain Warehouses | |

| Dark Stores / Micro-Fulfillment Centers | |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.) | |

| By Service Type | Storage |

| Picking and Packing | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Automation Level | Manual |

| Semi-Automated | |

| Automated | |

| By End-User Industry | Apparel and Footwear |

| Consumer Electronics | |

| Grocery and FMCG | |

| Pharmaceuticals, Beauty and Wellness | |

| Home Essentials and Furnishings | |

| Others | |

| By States | Mexico (State of Mexico) |

| Nuevo Leon | |

| Jalisco | |

| Queretaro | |

| Rest of the States |

Key Questions Answered in the Report

How fast is warehouse demand growing in Mexico’s e-commerce sector?

The Mexico E-commerce Warehouse Market size is set to rise from USD 1.07 billion in 2026 to USD 1.38 billion by 2031 at a 5.29% CAGR.

Which facility type leads current demand?

Fulfilment centers captured 41.34% of 2025 revenue, anchoring national multi-channel distribution networks.

What segment will expand the quickest?

Dark stores and micro-fulfillment centers are forecast to grow at 10.53% CAGR because they satisfy urban same-hour delivery promises.

Which region offers the highest growth potential?

Queretaro should post a 7.79% CAGR through 2031, helped by a 24-hour customs-clearance airport corridor.

How is automation changing operations?

Fully automated warehouses, aided by falling robot prices, will grow 9.61% annually and can lift picking accuracy above 99.5%.

What is the main infrastructure hurdle?

Chronic road congestion in Mexico’s three biggest metros lifts last-mile costs by up to 25% versus secondary markets.

Page last updated on: