France E-Commerce Warehouse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

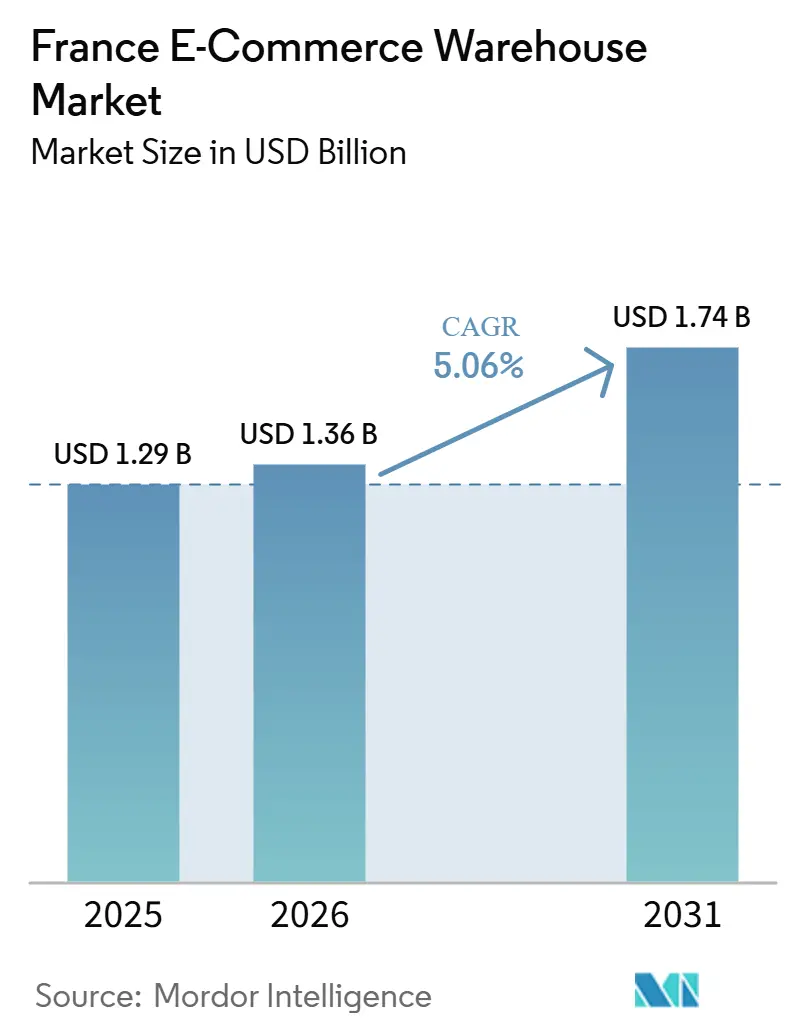

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

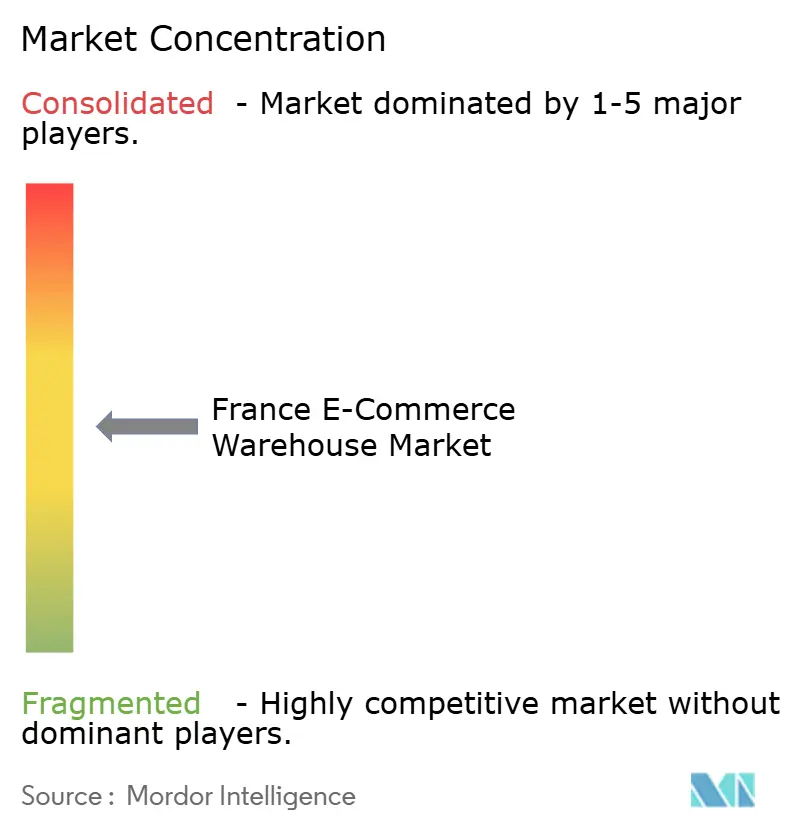

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France E-Commerce Warehouse Market Analysis by Mordor Intelligence

The France E-Commerce Warehouse Market size is projected to be USD 1.29 billion in 2025, USD 1.36 billion in 2026, and reach USD 1.74 billion by 2031, growing at a CAGR of 5.06% from 2026 to 2031.

Rising cross-border consolidation hubs, Gen Z’s heavy online spending, and growing quick-commerce footprints keep warehouse demand high, while land scarcity in dense regions pushes developers toward brownfield conversions to unlock capacity. Automation adoption has quadrupled in a decade, enabling higher throughput and lower error rates even as labor shortages for robotics maintenance persist[1]U.S. Commercial Service, “France – eCommerce,” trade.gov. Sustainability targets, such as La Poste’s net-zero commitment and SNCF’s rail-freight expansion, shape site selection and facility design by prioritizing multimodal access, renewable energy, and electric-vehicle (EV) charging capability. Meanwhile, municipal regulations reclassifying dark stores as warehouses create zoning hurdles that redirect quick-commerce operators toward micro-fulfillment formats in peri-urban locations.

Key Report Takeaways

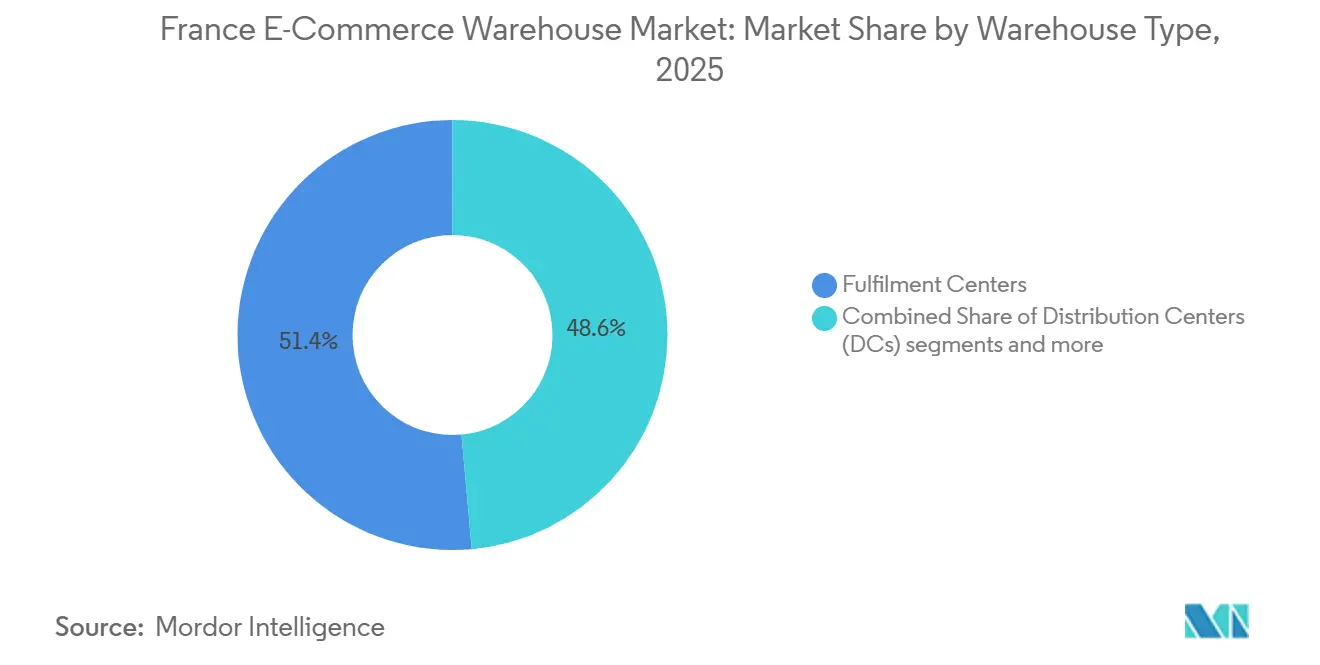

- By warehouse type, fulfillment centers led with 51.43% of France e-commerce warehouse market share in 2025, while dark-store and micro-fulfillment formats are projected to advance at a 10.26% CAGR through 2031.

- By region, Ile-de-France accounted for 27.77% of the France e-commerce warehouse market size in 2025, and Auvergne-Rhone-Alpes is set to record the highest growth at 7.77% CAGR between 2026 and 2031.

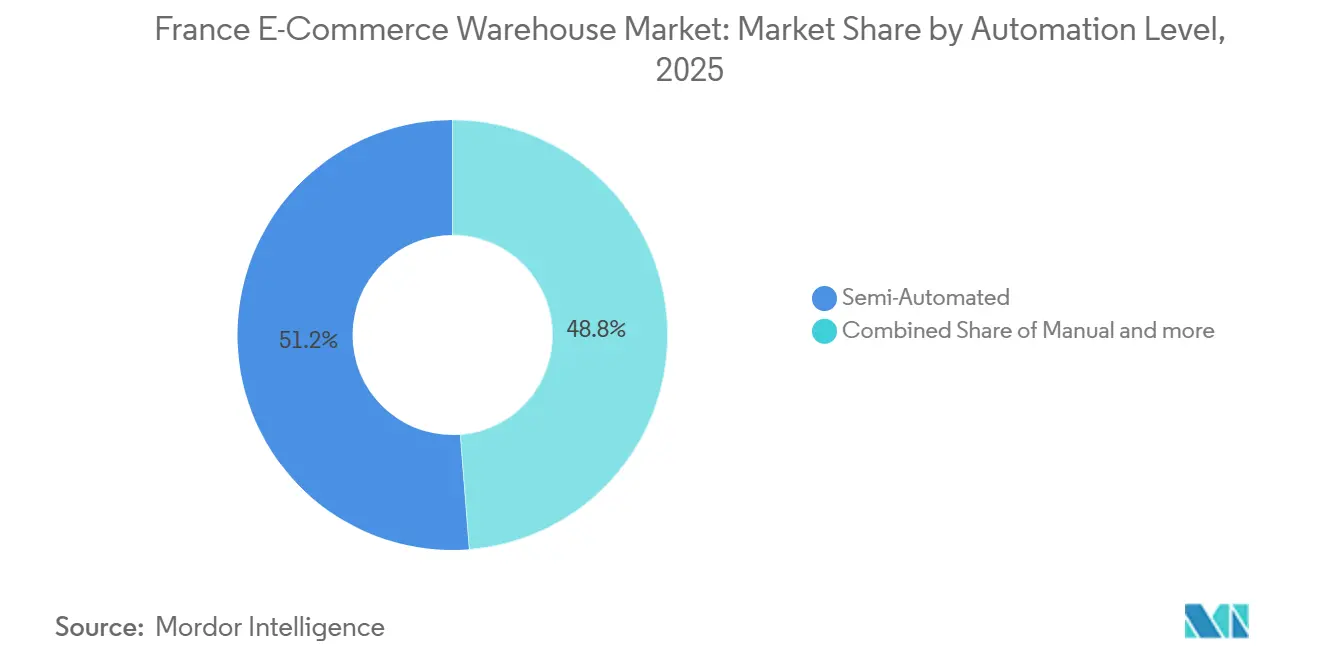

- By automation level, semi-automated sites held 51.25% France e-commerce warehouse market share in 2025, whereas fully automated facilities are forecast to expand at 9.39% CAGR to 2031.

- By service, storage services represented 45.16% of France e-commerce warehouse market size in 2025, and picking-and-packing services are poised to rise at 9.54% CAGR through 2031.

- By end-user, apparel and footwear captured 25.28% share of the France e-commerce warehouse market in 2025, while grocery and fast-moving consumer goods (FMCG) are on track to grow at 11.65% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France E-Commerce Warehouse Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for EU cross-border consolidation hubs | +1.5% | National; focus on lle-de-France and Auvergne-Rhone-Alpes | Medium term (2-4 years) |

| Government subsidies for brownfield warehouse conversions | +0.6% | Major metropolitan areas | Long term (≥ 4 years) |

| Omnichannel click-and-collect surge boosting regional hub needs | +1.1% | Urban and peri-urban France | Short term (≤ 2 years) |

| AI-driven inventory analytics improving facility ROI | +0.8% | Nationwide technology adopters | Medium term (2-4 years) |

| Rapid rise of subscription delivery models requiring temperature-controlled space | +0.7% | High-density cities | Medium term (2-4 years) |

| Expansion of EV last-mile fleets needing charging-ready warehouses | +0.4% | Core urban nodes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for EU Cross-Border Consolidation Hubs

France sits at the heart of the European Union, letting operators dispatch parcels to 115 million consumers within a single-day delivery radius. Large 3PLs such as Kuehne+Nagel fold customs-clearance expertise into direct-to-consumer offerings, betting on faster growth in cross-border flows than in purely domestic traffic. Peripheral sites like Vaucluse leverage lower land prices and motorway links to Spain and Italy to attract consolidation hubs that relieve pressure on Ile-de-France. DHL’s Chronopost network of 19,555 drop-off points underscores the node density required to make international e-commerce seamless. Regulatory harmonization under the EU Digital Single Market further reduces friction, steering pan-European brands toward French warehouses that balance speed, cost, and customs simplicity.

Government Subsidies for Brownfield Warehouse Conversions

Limited land in big cities drives policymakers to subsidize the reclamation of disused industrial parcels. The Schéma Directeur de la Region Ile-de-France steers logistics toward already-urbanized plots, offering fiscal incentives and faster permits to developers that commit to environmental remediation[2]L’Alsace, “Dépôt Amazon Augny,” lalsace.fr. Paris-Saclay’s government-backed science hub includes logistics zones where investors benefit from streamlined approvals, helping operators like Prologis meet sustainability mandates while enlarging their footprint. Upgrading brownfields cuts greenfield resistance, aligns with national net-zero goals, and keeps warehouses near end consumers to preserve delivery lead times.

Omnichannel Click-and-Collect Surge Boosting Regional Hub Needs

Click-and-collect appeals to shoppers who want cost-free pickup and instant returns, pushing retailers to mesh store networks with agile regional warehouses. Fnac Darty generates more than half its online revenue through omnichannel paths, driving demand for hubs placed within the same-day reach of its 1,000 stores. La Poste channels USD 1 billion into proximity platforms that replenish 19,555 Chronopost points overnight, shrinking last-mile costs while sustaining next-day service levels. Carrefour plans USD 11 billion in gross-merchandise value (GMV) via e-commerce by 2026 and requires nodes near hypermarkets to sync online orders with store pickup lanes. These strategies intensify the need for mid-sized, high-throughput facilities around metropolitan rings in the France e-commerce warehouse market.

AI-Driven Inventory Analytics Improving Facility ROI

Logistics providers now deploy artificial intelligence (AI) to squeeze more throughput from each square foot. ID Logistics' ASTRID robot photographs and reconciles 5,000 pallets per hour, eliminating manual stock counts and freeing labor for higher-value tasks. GEODIS earmarks technology spending under its Ambition 2027 plan to fuse predictive analytics with autonomous mobile robots, expecting paybacks through lower picking errors and better space utilization. As AI platforms move from pilot to portfolio scale, mid-tier warehouses gain the confidence to automate, accelerating the shift toward data-driven operations across the France e-commerce warehouse market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent urban noise and traffic-emission zoning compliance costs | −0.7% | Paris and other major cities | Short term (≤ 2 years) |

| Shortage of robotics-skilled labor delaying automation roll-outs | −0.5% | Nationwide | Medium term (2-4 years) |

| Volatile electricity tariffs inflating operating expenses | −0.4% | National; biggest hit to automated sites | Short term (≤ 2 years) |

| EU cybersecurity mandates raising WMS upgrade outlays | −0.3% | All automated facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Urban Noise and Traffic-Emission Zoning Compliance Costs

Municipalities now classify dark stores as warehouses, letting officials curb operating hours and impose delivery curfews, especially in Paris, where 60 quick-commerce sites risk closure for zoning breaches. Operators must invest in soundproof docks, electric vans, and real-time traffic management to retain urban footprints, inflating cost bases that already face thin e-commerce margins. Court rulings reinforce city authority, signaling that compliance spending will remain a near-term burden until vehicle electrification and micro-hub models mature.

Shortage of Robotics-Skilled Labor Delaying Automation Roll-Outs

ID Logistics plans to hire 1,000 IT and mechatronics specialists, highlighting a national scarcity that slows commissioning of automated systems. Training capacity at institutes like CRET-LOG lags market demand, stretching payback periods for robotics projects and tilting the advantage to multinationals that can import talent. Smaller firms therefore postpone upgrades or outsource to 3PLs, reinforcing consolidation trends in the France e-commerce warehouse market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Fulfillment Centers Anchor Capacity While Micro-Formats Surge

Fulfillment centers captured 51.43% of the France e-commerce warehouse market size in 2025, thanks to deep-lane storage and multi-SKU picking that serve national order peaks. Amazon’s 180,000 m² Augny site illustrates the scale of 4,000 staff and 25 km of conveyors keep lead times stable across Alsace, Lorraine, and neighboring countries[3]L’Alsace, “La démesure du dépôt Amazon qui livre l’Alsace,” lalsace.fr. These megasites prioritize automation to offset wage inflation, embedding goods-to-person shuttles and automated sorters that push dock-to-dock cycles below 30 minutes. Operators also retrofit mezzanines into legacy shells, focusing on cubic optimization to avoid greenfield barriers near Paris.

Dark stores and micro-fulfillment centers, though only 4% of floor space today, are the fastest-growing sub-category at 10.26% CAGR through 2031. Quick-commerce players exploit 1,000-3,000 m² facilities inside ring roads to promise 15-minute grocery drops. Land-use pushback is steering the next wave toward converted parking garages and rail depots, with Prologis piloting urban-hub concepts in Orleans that mix parcel lockers, EV charging, and bicycle docks. Cold-chain variants emerge as on-demand meal solutions expand, opening a premium pocket inside the France e-commerce warehouse market for temperature-specific micro sites.

By Service Type: Storage Dominates, Yet Picking and Packing Leads Growth

Storage services accounted for 45.16% of France e-commerce warehouse market share in 2025, reflecting the enduring need to hold safety stock amid supply-chain volatility. Large retailers secure long-term leases on multi-client campuses, tying up racked capacity ahead of holiday peaks. Value-added storage, such as tri-temperature chambers at STEF, commands premium rents by complying with food-safety protocols and energy-efficiency targets.

Picking and packing, expanding at 9.54% CAGR, gains traction as robotics slashes order-cycle times to under one hour. DISPEO’s Evreux site reaches 180 picks per person per hour with goods-to-person robots, extracting labor savings that more than offset capital outlays. Subscription boxes and influencer “drops” require kitting, labeling, and gift-wrap steps all bundled into integrated service contracts that lift warehouse yields. As same-day delivery proliferates, shippers favor operators that fuse storage, picking, personalization, and return handling under one roof, reinforcing convergence in the France e-commerce warehouse market.

By Automation Level: Semi-Automated Sites Rule, Full Automation Accelerates

Semi-automated facilities held 51.25% France e-commerce warehouse market share in 2025, balancing mechanical conveyors with human pickers for flexibility. Rising minimum wages spur broader adoption of robotic palletizers and automated guided vehicles (AGVs), yet many operators pause at semi-automation to manage upfront costs. Leasing models and robotics-as-a-service now lower entry barriers, allowing tier-two 3PLs to trial technology without capex spikes.

Fully automated sites, posting 9.39% CAGR, attract consumer-electronics and pharmaceutical clients that prize near-zero error rates. ID Logistics' ASTRID deployment highlights AI synergy, as image recognition validates inventory without Wi-Fi, cutting downtime in vast aisles. Energy volatility remains a headwind, but on-site solar and battery storage soften the impact, making full automation progressively viable across the France e-commerce warehouse market.

By End-User Industry: Apparel Dominates, Grocery Sets the Pace

Apparel and footwear controlled 25.28% of France e-commerce warehouse market size in 2025, as standardized SKUs and low ambient requirements simplify handling. Fashion brands leverage postponement strategies, holding undifferentiated stock centrally and customizing locally to cut markdowns, driving demand for facilities with value-added labeling and quality-control zones. Reverse logistics swells as returns exceed 30% in fast fashion, creating parallel flows that double facility complexity.

Grocery and FMCG, expanding at 11.65% CAGR, invest in tri-temperature depots to meet 30-minute delivery promises in dense cities. Carrefour positions micro-fulfillment pods near hypermarkets to align store replenishment with online baskets, while ID Logistics integrates ambient, chilled, and frozen docks at La Brede to consolidate food flows. Packaging waste regulations also spur closed-loop logistics, nudging operators to add cleaning and refurbishment zones.

Geography Analysis

Ile-de-France remains the nerve center of the France e-commerce warehouse market with 27.77% of the market size in 2025, but scarcity inflates rents and pushes developers toward creative vertical builds that integrate last-mile lockers on lower floors while stacking mezzanine pick modules above street level. Investors increasingly eye towns 100 kilometers south of Paris, where Orleans offers railroad interchanges and 30% lower land costs, yet still delivers parcels into the capital within two hours. Government brownfield grants accelerate conversions of former car plants in the outer ring, adding capacity without breaching greenbelt limits[4]Le Monde, “Logistique Urbaine,” lemonde.fr.

In Auvergne-Rhone-Alpes, which is expanding at a CAGR of 7.77%, Lyon is enhancing its logistics allure with coordinated upgrades to its airport, inland port, and highways. In a bid to promote sustainable practices, regional authorities are expediting permits for facilities that incorporate on-site renewable energy. This initiative dovetails with Renault Trucks' ambitious positive-energy logistics platform, set to create 500 jobs by 2028. Such strategic moves are drawing in shippers from the FMCG, pharmaceutical, and automotive sectors, all seeking multimodal solutions to manage costs and reduce carbon footprints.

Along France’s northeastern border, Grand Est leverages Germany-facing highways and a revitalized rail grid to capture consolidation flows. Amazon’s four-story Augny fulfillment center funnels 600,000 packages daily, demonstrating economies of scale unavailable in land-tight Paris. Regional planners extend fiber and renewable grids to appeal to data-rich, energy-intensive automation projects, further embedding Grand Est in cross-border supply chains.

Competitive Landscape

France’s e-commerce warehouse market shows moderate concentration: the top five integrators, La Poste, GEODIS, ID Logistics, GXO Logistics, and DHL, collectively control around 45% of active floor space, leaving room for niche specialists. La Poste leans on its USD 34.1 billion group revenue to retrofit depots with automated sorters and EV docks, cementing parcel dominance while bundling third-party logistics (3PL) contracts. GEODIS pursues bolt-on acquisitions under its Ambition 2027 strategy, expanding capacity and analytics talent to build a data-centric service stack.

Consolidation accelerates at the global tier. CEVA’s USD 22.3 billion revenue after absorbing Bollore Logistics adds 11.7 million m² worldwide, elevating its grip on automotive and temperature-controlled verticals. GXO, the world’s largest pure-play contract logistics firm, exploits scale to negotiate multiyear automation leases that smaller peers cannot match. Start-ups such as Exotec commercialize modular robot fleets, enabling mid-size 3PLs to leapfrog legacy conveyor systems with capex-light options.

Technological differentiation sharpens competition. Operators boasting AI-powered WMS and predictive analytics secure higher service premiums and stickier contracts. ID Logistics markets cycle-count robots as a compliance hedge against EU cybersecurity rules, while STEF’s hydrogen forklifts score decarbonization points with grocery majors. Price and service wars continue in the last-mile, yet long-haul consolidation and vertical specialization underpin overall margin resilience.

France E-Commerce Warehouse Industry Leaders

DHL Group

ID Logistics

GEODIS

GXO Logistics

La Poste Group (including Colissimo/Chronopost)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GXO Logistics expanded its e-commerce logistics footprint in France through a renewed partnership with Electro Depot. As part of this development, GXO is expanding its existing Fos-sur-Mer warehouse and launching a new distribution facility in Port-Saint-Louis-du-Rhone, strengthening its presence in southern France.

- May 2025: Barings sold a 27,622 m² core-plus logistics asset near Lyon to Fidelity International; the site remains leased to La Poste until 2029.

- April 2025: STEF deployed 48 hydrogen forklifts at its Athis-Mons cold-storage center under the Moving Green program, aiming for 100% low-carbon energy in buildings by 2025.

- March 2025: Amazon opened its four-level, 180,000 m² Augny fulfillment center employing 4,000 staff and 25 km of conveyors.

France E-Commerce Warehouse Market Report Scope

| Fulfilment Centres |

| Distribution Centres (DCs) |

| Cold-Chain Warehouses |

| Dark Stores / Micro-Fulfillment Centers |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, Etc.) |

| Storage |

| Picking and Packing |

| Value-Added Services and Others (Kitting, Labelling) |

| Manual |

| Semi-Automated |

| Automated |

| Apparel and Footwear |

| Consumer Electronics |

| Grocery and FMCG |

| Pharmaceuticals, Beauty and Wellness |

| Home Essentials and Furnishings |

| Others |

| Ile-de-France |

| Auvergne-Rhone-Alpes |

| Hauts-de-France |

| Provence-Alpes-Cote d’Azur |

| Grand Est |

| Nouvelle-Aquitaine |

| Occitanie |

| Others |

| By Warehouse Type | Fulfilment Centres |

| Distribution Centres (DCs) | |

| Cold-Chain Warehouses | |

| Dark Stores / Micro-Fulfillment Centers | |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, Etc.) | |

| By Service Type | Storage |

| Picking and Packing | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Automation Level | Manual |

| Semi-Automated | |

| Automated | |

| By End-User Industry | Apparel and Footwear |

| Consumer Electronics | |

| Grocery and FMCG | |

| Pharmaceuticals, Beauty and Wellness | |

| Home Essentials and Furnishings | |

| Others | |

| By French Region (Value) | Ile-de-France |

| Auvergne-Rhone-Alpes | |

| Hauts-de-France | |

| Provence-Alpes-Cote d’Azur | |

| Grand Est | |

| Nouvelle-Aquitaine | |

| Occitanie | |

| Others |

Key Questions Answered in the Report

What is the forecast value of the France e-commerce warehouse market by 2031?

The market is projected to reach USD 1.74 billion by 2031, reflecting a 5.06% CAGR from 2026-2031.

Which warehouse type currently holds the largest share in France?

Fulfillment centers lead with 51.43% share because they handle the bulk of traditional online order processing.

Which French region is expected to grow fastest in warehouse demand?

Auvergne-Rhône-Alpes is set to advance at 7.77% CAGR, buoyed by multimodal upgrades around Lyon.

How fast is the fully automated warehouse segment expanding?

Fully automated sites are forecast to grow at 9.39% CAGR thanks to maturing robotics and AI-driven ROI.

Why are brownfield site conversions important for French e-commerce logistics?

Urban land scarcity and supportive subsidies make redeveloping disused industrial plots the quickest path to add capacity near consumers.

What role does sustainability play in new warehouse investments?

Operators increasingly integrate EV charging, rooftop solar, and hydrogen equipment to meet tenant carbon targets and future regulations.

Page last updated on: