Saudi Arabia Cloud Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

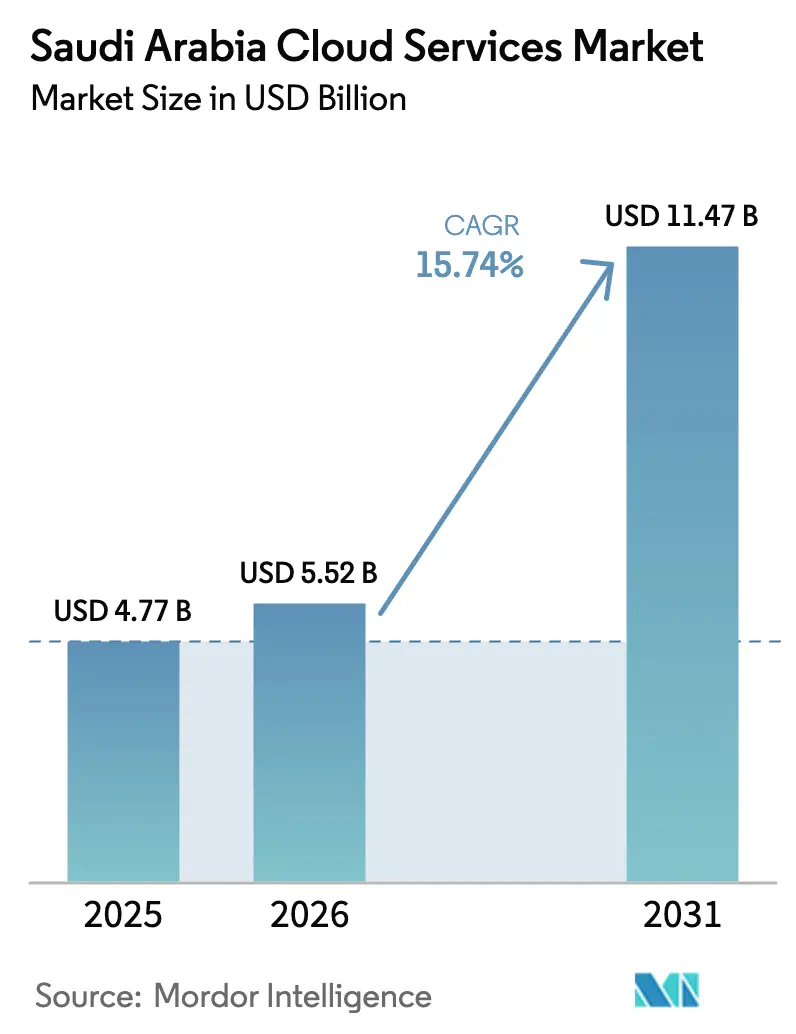

| Base Year Market Size (2025) | USD 4.77 Billion |

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 11.47 Billion |

| Growth Rate (2026 - 2031) | 15.74% CAGR |

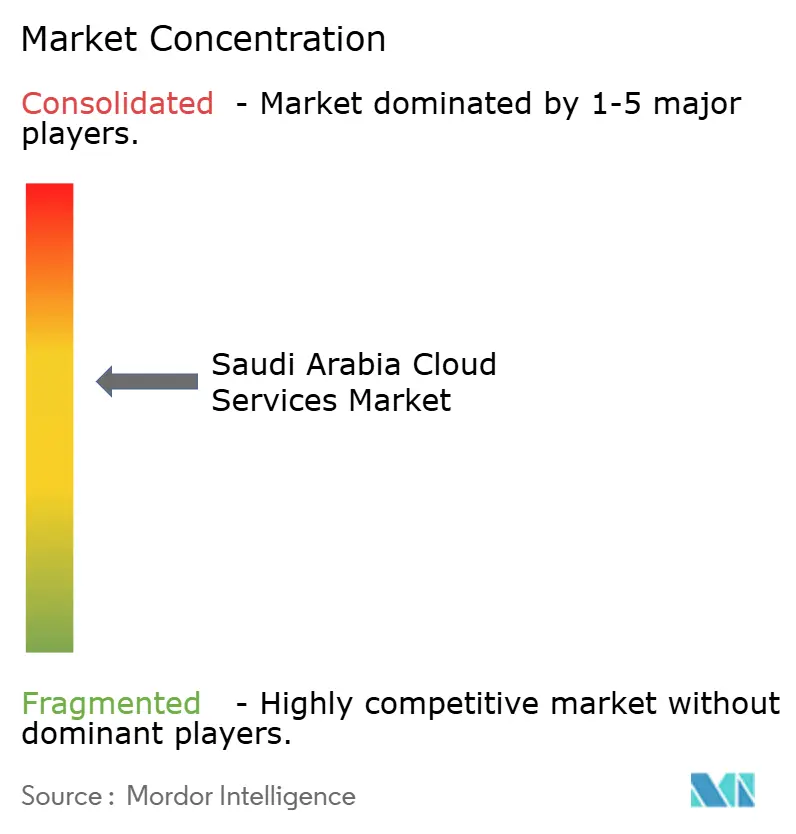

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Cloud Services Market Analysis by Mordor Intelligence

The Saudi Arabia cloud services market size was valued at USD 4.77 billion in 2025 and estimated to grow from USD 5.52 billion in 2026 to reach USD 11.47 billion by 2031, at a CAGR of 15.74% during the forecast period (2026-2031). Heightened digital-first mandates under Vision 2030, the Communications and Information Technology Commission’s Cloud-First Policy, and accelerating hyperscaler capital expenditure have created a strong foundation for sustained expansion. Software-as-a-Service (SaaS) continues to resonate with enterprises that want rapid deployment and minimal infrastructure upkeep, while Platform-as-a-Service (PaaS) is scaling quickly as developers prioritize modern application frameworks. Robust foreign direct investment totaling more than USD 21 billion in data center campuses keeps pricing competitive and latency low, widening adoption across regulated industries. Growing artificial-intelligence workloads, evidenced by large-scale NVIDIA GPU purchases and sovereign chip alliances, are catalyzing demand for GPU-rich cloud instances. Finally, rising edge-cloud deployments in NEOM and Riyadh enable gaming, streaming, and industrial IoT use cases to run close to end users for improved performance and compliance.

Key Report Takeaways

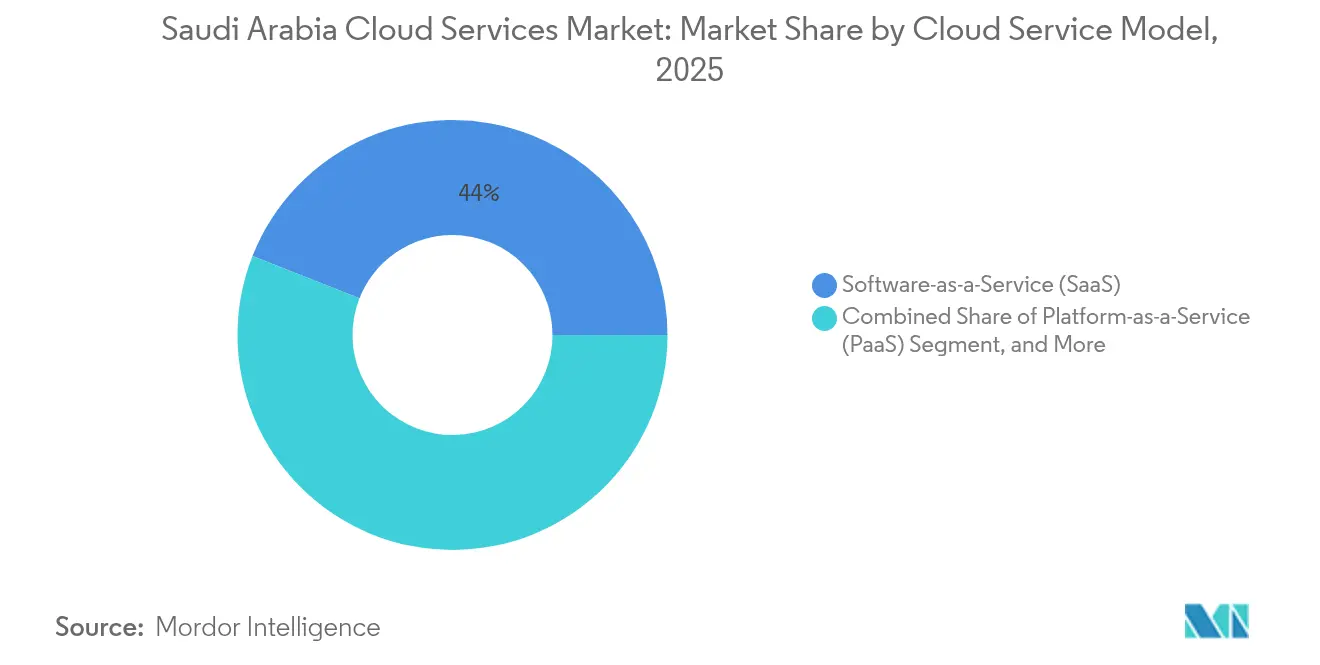

- By cloud service model, Software-as-a-Service led with 44.02% revenue share of the Saudi Arabia cloud services market in 2025; Platform-as-a-Service is projected to expand at a 16.64% CAGR through 2031.

- By deployment type, public cloud accounted for 65.72% of the Saudi Arabia cloud services market share in 2025, while hybrid cloud adoption is advancing at a 16.41% CAGR to 2031.

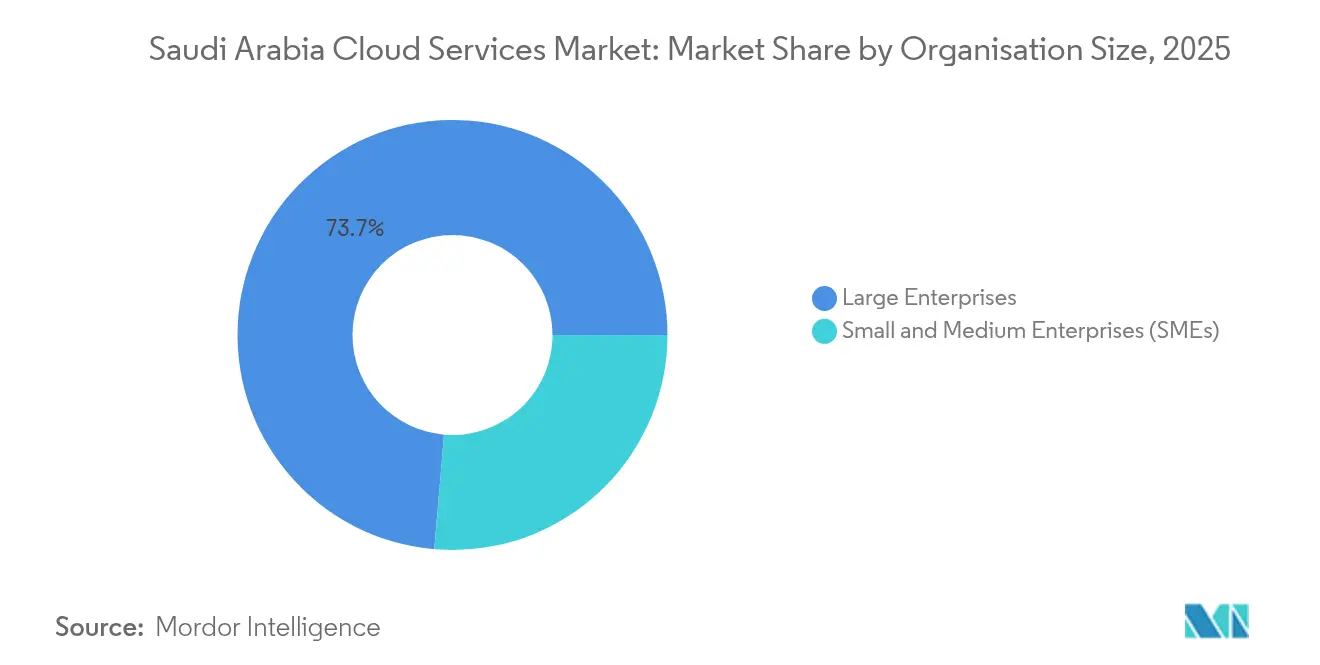

- By organisation size, large enterprises captured 73.65% of the 2025 spending of the Saudi Arabia cloud services market; SMEs are forecast to grow the fastest at 16.18% CAGR, due to Monsha’at programs.

- By end-user industry, Banking, Financial Services, and Insurance (BFSI) held a 27.06% share of the Saudi Arabia cloud services market in 2025; healthcare applications are set to record a 16.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Cloud Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-2030 digital-first mandates | +2.8% | Global | Medium term (2-4 years) |

| Cloud-First Policy (CITC) | +2.1% | Global | Short term (≤ 2 years) |

| Cost-optimization amid oil diversification | +1.9% | Global | Long term (≥ 4 years) |

| Hyperscaler DC investments (AWS, Azure, GCP) | +3.2% | Riyadh Province, Eastern Province | Medium term (2-4 years) |

| Gen-AI and GPU workload momentum | +2.4% | Riyadh Province, NEOM | Short term (≤ 2 years) |

| Edge cloud for gaming and streaming | +1.1% | NEOM, Riyadh Province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision-2030 Digital-First Mandates Drive Systematic Cloud Migration

Vision 2030 obliges government entities to prioritize cloud procurement, triggering consistent demand that spills into private-sector decision making. The Digital Government Authority’s Emerging Technology Adoption Readiness Index delivers assessment tools that streamline migration planning, while a USD 24.8 billion national digital-infrastructure program has driven 99% internet penetration and broad 5G coverage. Eighty-five percent of surveyed public-sector leaders now earmark budgets for cloud-enabled emerging technologies, and 45% actively evaluate AI-driven workloads. [1]KPMG, “Unlocking Government’s Technology Future,” kpmg.com National cloud infrastructure coordinated by the Saudi Data and Artificial Intelligence Authority joins more than 200 government systems, reinforcing secure data interchange standards that private firms subsequently mirror.

Hyperscaler Data Center Investments Create Infrastructure Foundation

Aggregated commitments from AWS, Microsoft, and Oracle surpass USD 21 billion, adding multiple availability zones by 2026. [2]Capacity Media, “What Is Driving Saudi Arabia’s $21bn Data Centre Investment Surge?,” capacitymedia.com AWS alone will invest USD 5.3 billion to deploy three zones accompanied by two innovation centers targeting 30,000 local trainees, 4,000 of whom are women. Oracle opened its second Riyadh region after outlaying USD 1.5 billion to offer more than 100 cloud services under strict data residency rules. Project MGX, a USD 30 billion Microsoft-Temasek-BlackRock alliance, plans an AI-centric campus in Riyadh to serve quantum and generative-AI workloads. These facilities reduce network latency, introduce next-generation accelerators, and intensify price competition, broadening adoption among cost-sensitive sectors such as education and retail.

Gen-AI Workload Momentum Drives GPU Infrastructure Demand

HUMAIN procured 18,000 NVIDIA GB300 chips and may order hundreds of thousands more to back a 500-megawatt compute roadmap that completes in early 2026. Groq secured USD 1.5 billion to deploy the region’s largest inference cluster, and AMD joined HUMAIN in a USD 10 billion five-year collaboration for accelerator supply. Saudi Aramco’s Dammam 7 supercomputer showcases industrial use of AI models for seismic data, while SDAIA aims to train 20,000 AI professionals by 2030. Demand for GPU-rich cloud instances, therefore, outpaces generic compute growth.

Cost-Optimization Imperatives Accelerate Cloud Migration

Non-oil activities composed 49.9% of GDP growth in 2024, heightening the focus on operational efficiency that cloud billing models address through pay-per-use pricing. Dell found that 90% of Saudi organizations accelerated digital transformation, exceeding the global 80% average, partly to curb capital outlays. SMEs gain particular relief from up-front infrastructure costs, accessing hyperscaler platforms via Monsha’at programs and benefiting from a 72% surge in venture funding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise skill deficit and expat reliance | -1.8% | Global, concentrated in technical roles | Medium term (2-4 years) |

| Vendor lock-in concerns | -1.2% | Large enterprises, government entities | Long term (≥ 4 years) |

| Legacy migration complexity | -1.5% | Oil and Gas, BFSI sectors | Medium term (2-4 years) |

| Data-center water/energy sustainability risk | -0.9% | Riyadh Province, Eastern Province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Skill Deficit Constrains Cloud Adoption Velocity

Rapid scaling of digital projects outstrips local talent supply, forcing reliance on expatriate professionals and elevating costs. Fifty-six percent of Saudi tech leaders identify skills shortages as the top barrier to AI deployment. Government programs such as One Million Arab Coders and SDAIA’s Elevate aim to upscale 25,000 women, while AWS pledges to train 30,000 citizens. Nevertheless, workforce development timelines keep the skills gap material for the medium term.

Legacy Migration Complexity Creates Implementation Barriers

Mission-critical workloads in oil, gas, and BFSI run on decades-old platforms that require phased re-engineering. A University of Hail case study cut server footprints by 50% only after a comprehensive redesign. Saudi Aramco phases data ingestion to safeguard drilling operations. The Saudi Central Bank highlights stringent security assessments before approving cloud migrations, extending timelines, and constraining near-term cloud velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cloud Service Model: Platform Services Accelerate Application Modernization

SaaS commanded 44.02% of 2025 revenue as enterprises embraced turnkey software to bypass legacy hardware management. PaaS adoption, projected at a 16.64% CAGR, aligns with developer demand for integrated toolchains and container orchestration that facilitate rapid releases. The Saudi Arabia cloud services market size allocated to PaaS is therefore positioned to outpace other models through 2031. IaaS persists among large firms that need granular control over compute resources, especially for security-sensitive oil-and-gas applications. Function-as-a-Service gains traction within startups seeking operational agility.

From 2019-2024, PaaS shifted from exploratory pilots to mainstream deployments. Saudi Aramco pilots industrial Large Language Models via managed PaaS offerings to avoid infrastructure overhead. Regulatory clarity from CITC’s Cloud Computing Regulatory Framework standardizes compliance, further reinforcing PaaS uptake.

By Deployment Type: Hybrid Strategies Balance Sovereignty and Cost

Public cloud captured 65.72% of the Saudi Arabia cloud services market share in 2025, leveraging economies of scale and on-demand scalability. Hybrid deployments are forecast to rise at a 16.41% CAGR as enterprises combine on-premise controls with off-premise elasticity. The Saudi Arabia cloud services market size aligned to hybrid solutions is expected to rise sharply as compliance frameworks mandate local data residency.

Financial institutions illustrate the pattern: STCPay runs Temenos on private infrastructure while connecting to public services for overflow capacity. Edarat Group’s IBM Cloud Satellite deployment in three domestic sites meets sovereignty requirements while offering multi-cloud provisioning.

By Organisation Size: SMEs Propel Future Expansion

Large enterprises controlled 73.65% of 2025 revenue due to established IT budgets and multi-site rollouts. However, SMEs will grow the fastest at 16.18% CAGR, attracted by low entry costs and supportive financing. Monsha’at programs lifted SME counts to 1.3 million and injected greater venture backing, driving wider cloud adoption.

Cloud offers SMEs enterprise-grade capabilities without capital burdens, facilitating rapid international scaling. Fintech start-ups rose 14.7-fold since 2018, with 147 regulated entities securing SAR 1.5 billion in investments that fund cloud-native platforms. Mobile-commerce research confirms leadership commitment and perceived benefits as crucial adoption triggers.

By End-User Industry: Healthcare Shows Rapid Uptake

BFSI led with 27.06% share in 2025, spurred by Saudi Central Bank sandbox programs and blockchain-based interbank platforms. Healthcare exhibits the highest CAGR at 16.88% as the government raised the health budget to USD 68.2 billion in 2023 and targets a USD 66.6 billion GDP contribution from digital health by 2030. The Saudi Arabia cloud services market size attributable to healthcare workloads is primed for strong upside.

Oil, Gas, and Utilities maintain large cloud budgets for predictive maintenance and seismic analytics. Manufacturing and construction leverage robotics; Samsung C&T’s SAR 1.3 billion automation project at NEOM cut manual labor by 80%. Retail and e-commerce enjoyed a 57% jump in April 2024 sales to SAR 23.27 billion, driving cloud needs for peak-season elasticity.

Geography Analysis

Riyadh Province houses the densest cluster of hyperscaler zones, including Oracle’s second region and AWS’s forthcoming sites. LEAP 2025 announcements added USD 14.85 billion to local tech commitments, underscoring persistent demand from government ministries and conglomerates. IBM’s USD 200 million Software Lab employs 70% Saudi nationals to support AI R&D, and ServiceNow plans data-center launches by 2026 for localized support.

Eastern Province, the energy capital, leverages Saudi Aramco’s Dammam 7 supercomputer and Groq’s inference cluster to run industry-specific analytics. The location also benefits petrochemical and logistics operators, and Invest Saudi incentives promote data-center investments.

Makkah and Western corridors tap Saudi Telecom Company’s Jeddah mega-centers that improve latency for trade hubs and pilgrims. NEOM in the northwest leads edge-cloud innovation via a USD 5 billion DataVolt partnership for a 1.5-gigawatt net-zero campus powered by renewables and liquid cooling. These developments expand geographic resiliency for the Saudi Arabia cloud services market.

Competitive Landscape

Market concentration is moderate as U.S. and Chinese hyperscalers vie for share. AWS retains leadership with a USD 5.3 billion region and expansive workforce skilling, while Microsoft positions an AI-oriented campus under Project MGX. Oracle strengthens its local value proposition through multi-cloud compliance offerings. Huawei and Alibaba, operating via the Saudi Cloud Computing Company, promote data sovereignty at competitive price points. [4]Rest of World, “How China Is Gaining Ground in the Middle East Cloud Computing Race,” restofworld.org

Local incumbents, Saudi Telecom Company and Solutions by stc, leverage regulatory rapport but face price pressure from hyperscalers. Solutions by stc maintains sovereign hosting zones in three cities and partners with IBM and VMware to deliver hybrid solutions. Niche players such as OmniOps raised SAR 30 million to create energy-efficient GPU farms, capturing sustainability-minded customers.

Geopolitical dynamics shape vendor selection as U.S. chip contracts exceeding USD 20 billion compete with Chinese alternatives, and CITC security rules favor providers with documented compliance architectures.

Saudi Arabia Cloud Services Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Alibaba Cloud (Alibaba Group Holding Ltd.)

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DataVolt signed with MODON to build a Riyadh facility, expanding capital-region capacity.

- February 2025: NEOM partnered with DataVolt on a USD 5 billion net-zero 1.5 GW AI center, the region’s largest sustainable deployment.

- February 2025: Groq obtained a USD 1.5 billion Saudi commitment for an AI inference cluster.

- February 2025: ServiceNow disclosed plans for 2026 Saudi data centers, adding localized SaaS support.

- February 2025: IBM expanded its Riyadh Software Lab, employing over 70% Saudis to accelerate AI development.

- December 2024: NEOM and Samsung C&T invested SAR 1.3 billion in construction robotics for 80% labor savings.

Saudi Arabia Cloud Services Market Report Scope

Cloud services are a broad category of on-demand services supplied to businesses and users through the Internet. These services are intended to enable simple, low-cost access to applications and resources that do not require internal infrastructure or hardware. Cloud computing vendors and service providers oversee all aspects of cloud services. A business does not need to host apps on its in-house servers as they are made available to clients from the providers' servers.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The scope of the study includes deployment and end-users. In addition, the study provides cloud service adoption trends and crucial vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem.

The saudi arabia cloud services market is segmented by deployment (public cloud [software-as-a-service, platform-as-a-service, infrastructure-as-a-service], private cloud), end-user industry (oil, gas & utilities, government & defense, healthcare, financial services, manufacturing & construction). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Function-as-a-Service (FaaS) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Oil, Gas and Utilities |

| Government and Defense |

| BFSI |

| Healthcare |

| Manufacturing and Construction |

| Retail and E-commerce |

| IT and Telecommunications |

| Education |

| Other End-User Industries |

| Riyadh Province |

| Eastern Province |

| Makkah Province |

| Madinah Province |

| Qassim Province |

| Rest of Saudi Arabia |

| By Cloud Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| Function-as-a-Service (FaaS) | |

| By Deployment Type | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Organisation Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-User Industry | Oil, Gas and Utilities |

| Government and Defense | |

| BFSI | |

| Healthcare | |

| Manufacturing and Construction | |

| Retail and E-commerce | |

| IT and Telecommunications | |

| Education | |

| Other End-User Industries | |

| By Province | Riyadh Province |

| Eastern Province | |

| Makkah Province | |

| Madinah Province | |

| Qassim Province | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How large is the Saudi Arabia cloud services market in 2026?

The market is valued at USD 5.52 billion in 2026 and is projected to reach USD 11.47 billion by 2031.

Which cloud service model leads spending in Saudi Arabia?

Software-as-a-Service leads with 44.02% revenue share in 2025, driven by ease of deployment.

What growth rate is expected for hybrid cloud adoption?

Hybrid deployments are forecast to expand at a 16.41% CAGR between 2026-2031 as firms balance sovereignty and cost.

Which end-user vertical is growing the fastest?

Healthcare workloads are set to grow at 16.88% CAGR through 2031 due to digital-health initiatives.

How are hyperscalers investing in Saudi Arabia?

AWS, Microsoft, and Oracle have collectively committed more than USD 21 billion for new regions and AI-centric campuses.

What is the outlook for SME cloud adoption?

SMEs will post a 16.18% CAGR as Monsha’at programs and venture funding lower entry barriers to advanced cloud services.

Page last updated on: