ASEAN Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

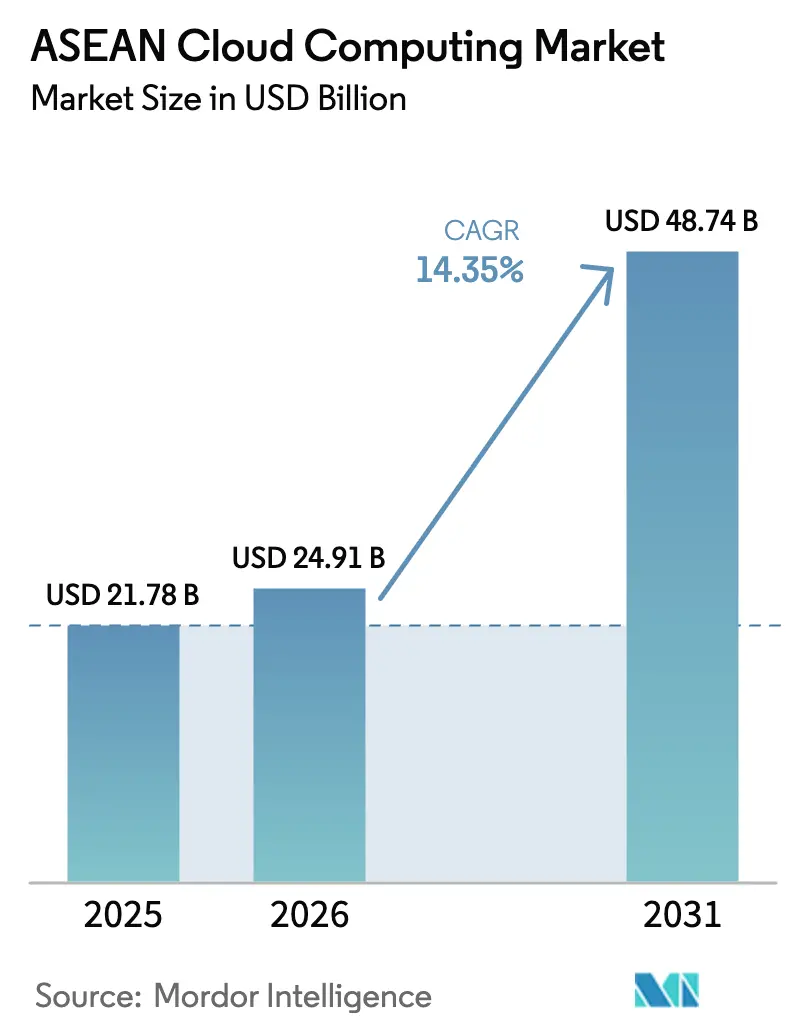

| Base Year Market Size (2025) | USD 21.78 Billion |

| Market Size (2026) | USD 24.91 Billion |

| Market Size (2031) | USD 48.74 Billion |

| Growth Rate (2026 - 2031) | 14.35% CAGR |

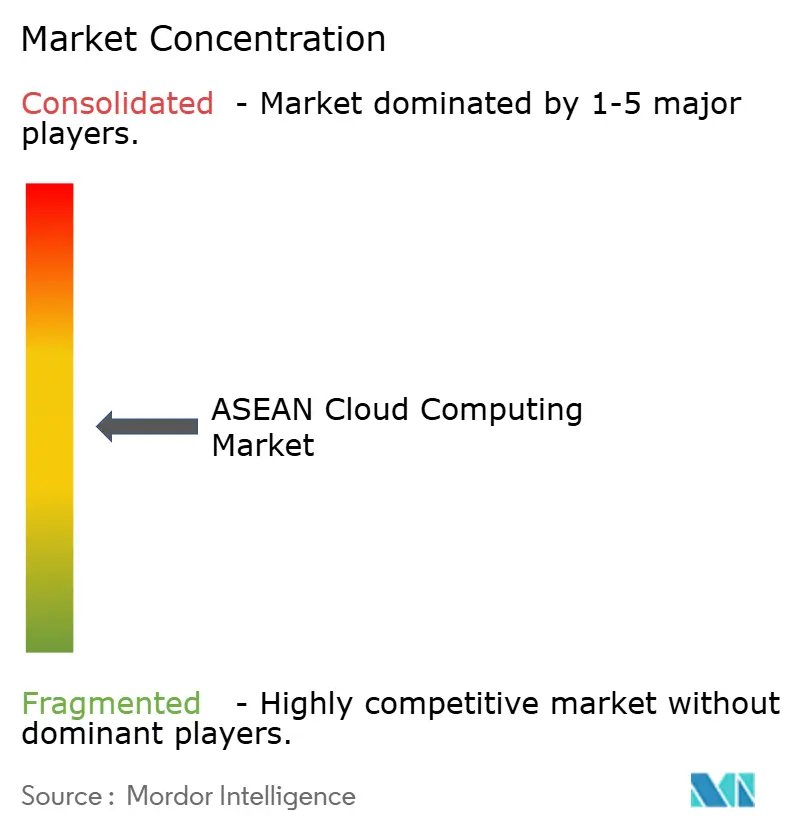

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Cloud Computing Market Analysis by Mordor Intelligence

The ASEAN Cloud Computing Market size was valued at USD 21.78 billion in 2025 and estimated to grow from USD 24.91 billion in 2026 to reach USD 48.74 billion by 2031, at a CAGR of 14.35% during the forecast period (2026-2031). Singapore anchors regional demand, Vietnam registers the fastest growth, and hyperscale investments exceeding USD 25 billion in 2024-2025 have strengthened the overall capacity pipeline. Government digital-economy master plans continue to mandate cloud migration across public agencies, while enterprise modernization pushes multi-cloud and hybrid strategies. Chinese hyperscalers have added significant price competition and localized capacity, accelerating infrastructure build-out across Indonesia, Malaysia, and Thailand. The ASEAN cloud computing market benefits further from 5G-enabled edge deployments, renewable-energy data-center initiatives, and rising demand for scalable IT among SMEs.

Key Report Takeaways

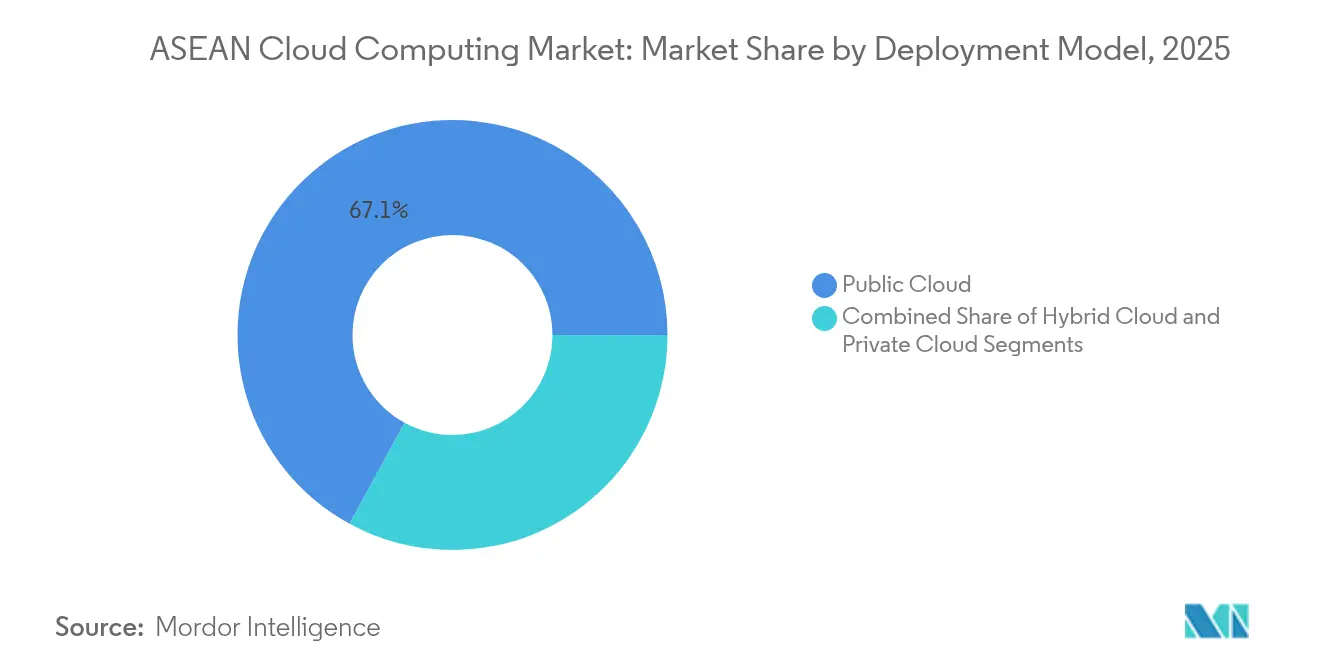

- By deployment model, Public Cloud led with 67.05% revenue share in 2025; Hybrid Cloud is forecast to expand at a 15.85% CAGR to 2031.

- By service model, Software as a Service held 55.65% of the ASEAN cloud computing market share in 2025, while Platform as a Service records the fastest projected CAGR at 16.3% through 2031.

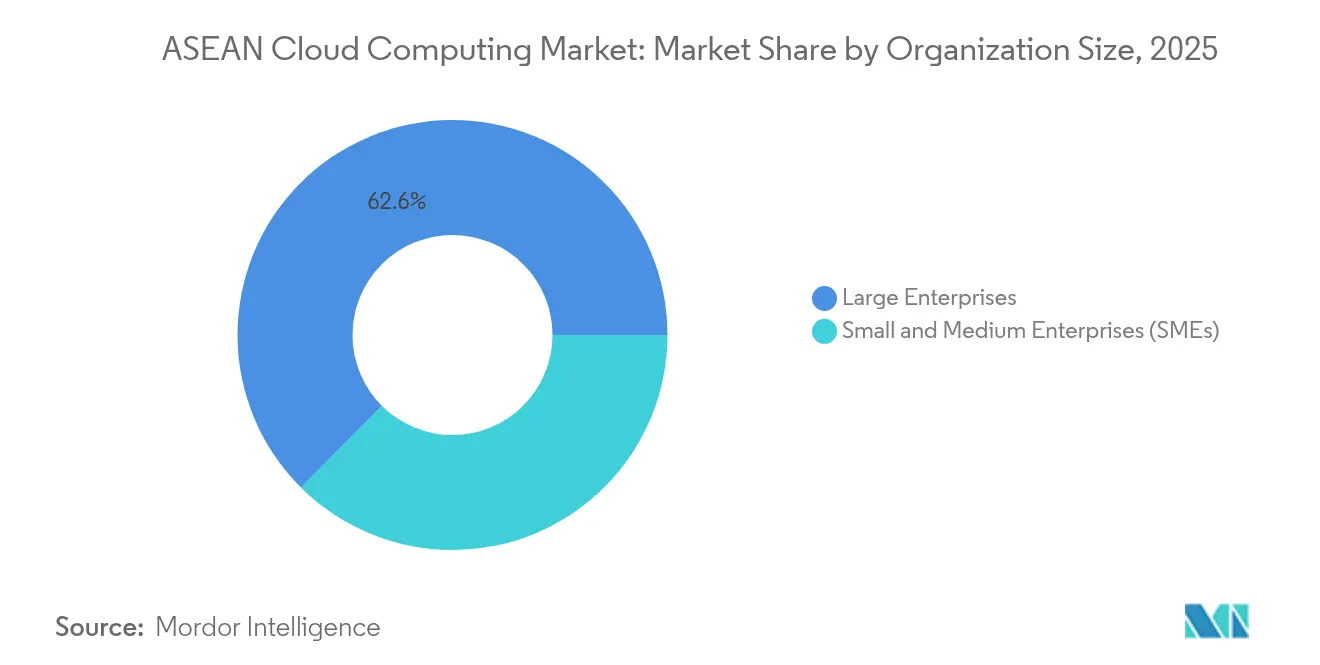

- By organization size, Large Enterprises accounted for 62.55% of the ASEAN cloud computing market size in 2025; Small and Medium Enterprises are set to advance at a 16.65% CAGR between 2026-2031.

- By end-user industry, Telecom and IT captured 28.35% revenue share in 2025; Healthcare is growing the quickest at 16.7% CAGR to 2031.

- By country, Singapore dominated with 36.10% of the ASEAN cloud computing market in 2025, whereas Vietnam is projected to grow at a 16.5% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G roll-outs enabling edge-cloud convergence | +2.1% | ASEAN-wide, strongest in Singapore, Thailand, Malaysia | Medium term (2-4 years) |

| Surge in ASEAN hyperscale data-center investments by Chinese providers | +2.8% | Indonesia, Malaysia, Thailand, Vietnam | Short term (≤ 2 years) |

| Government digital-economy masterplans boosting cloud adoption | +3.2% | Vietnam, Malaysia, Thailand, Philippines | Medium term (2-4 years) |

| Rising enterprise demand for scalable IT infrastructure | +2.4% | Singapore, Malaysia, Indonesia | Short term (≤ 2 years) |

| Cloud-native fintech growth in Indonesia and Vietnam | +1.9% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Sustainability incentives for renewable-powered cloud facilities | +1.6% | Singapore, Malaysia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G roll-outs enabling edge-cloud convergence

Nationwide 5G licenses in Cambodia and dense network upgrades in Thailand are enabling millisecond-latency applications that depend on proximate cloud nodes. [1]US-ASEAN Business Council, “Cambodia's Digital Transformation: 5G Rollout and Strengthened Cybersecurity Partnerships,” usasean.org Utilities such as Thailand’s Metropolitan Electricity Authority have already tied 5G grids to cloud analytics for predictive outage management. The synergy between edge nodes and public clouds improves service resilience and widens the addressable base for Internet-of-Things (IoT) workloads. Regional telcos now co-locate mini-data centers inside 5G base stations to minimize backhaul congestion. This convergence is expected to deepen hybrid adoption as enterprises partition latency-sensitive traffic to edge nodes while scaling the remainder on central hyperscale regions.

Surge in ASEAN hyperscale data-center investments by Chinese providers

Tencent allocated USD 500 million for Indonesian builds and formed deeper partnerships with local e-commerce leaders, delivering cost-competitive alternatives to North American platforms. Alibaba Cloud’s collaborative AI programs have also widened service breadth across Malaysia and Thailand. The influx of Chinese capacity favors regulated industries that prioritize local data residency, thereby pressuring incumbent vendors on price and latency. Short-haul cross-border interconnects between Chinese-backed facilities in Johor and Singapore have begun to offer sub-2 ms latency for multi-region replication. This investment wave materially boosts the ASEAN cloud computing market’s overall supply, lowering entry barriers for SMEs and start-ups.

Government digital-economy masterplans boosting cloud adoption

Vietnam’s 2030 mandate for 100% cloud utilization by state agencies has triggered synchronized migration roadmaps and budget allocations. Malaysia’s National Cloud Policy lines up fiscal incentives and sovereign-data principles that assure investors of market stability. Regional coordination under the ASEAN Digital Economy Framework aims to lift digital GDP by USD 2 trillion by 2030. Such clarity drives predictable procurement cycles for hyperscalers while de-risking private-sector migrations. Public-sector showcases are, in turn, accelerating enterprise confidence, especially among late-adopting verticals like education and utilities.

Rising enterprise demand for scalable IT infrastructure

Manufacturers across ASEAN expect USD 1.2 trillion of incremental output by embedding AI and cloud into production lines. In finance, insurers like Singlife have shifted core databases to cloud services to gain real-time analytics and cost elasticity. Multi-cloud procurement that pairs domestic regions with offshore backups mitigates vendor lock-in while meeting sovereignty demands. Managed-service partners now bundle container orchestration and site-reliability tooling, simplifying migration for legacy workloads. These developments collectively enlarge the ASEAN cloud computing market’s enterprise revenue pool and sustain double-digit growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data residency and sovereignty regulations | -1.8% | Vietnam, Malaysia, Indonesia, Thailand | Short term (≤ 2 years) |

| Shortage of cloud-skilled workforce in Tier-2 markets | -1.4% | Philippines, Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Cross-border connectivity and latency challenges | -0.9% | Regional; affecting smaller markets | Medium term (2-4 years) |

| High total cost of private and hybrid deployments for SMEs | -1.1% | Region-wide; concentrated in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data residency and sovereignty regulations

Malaysia’s 2025 Cross-Border Transfer Guidelines oblige firms to run Transfer Impact Assessments and prove the equivalence of foreign privacy standards. [2]Skrine, “Cross Border Personal Data Transfer Guidelines Launched,” skrine.com Vietnam’s July 2025 Data Law classifies “core data” and enforces domestic processing for sensitive sets. Such rules fragment infrastructure planning, forcing providers to duplicate facilities, raise capital costs, and adapt service catalogs per jurisdiction. Enterprises face legal complexity and higher total cost of ownership when architecting cross-region disaster recovery. Although compliance consultancies can bridge knowledge gaps, divergent national rules remain a notable drag on ASEAN cloud computing market growth during the near term.

Shortage of cloud-skilled workforce in Tier-2 markets

Indonesia employs nearly 1 million ICT workers, yet it still lacks specialists in DevOps and SRE roles critical for cloud operations. Thailand’s share of vocational enrollment sits at 35%, producing limited graduates ready for advanced cloud certifications. Attrition rates of 20-40% among certified engineers inflate salary benchmarks and delay enterprise migrations. Providers counterbalance by launching academies; Oracle alone plans to train 10,000 Singapore learners in 2025. However, until the talent gap narrows, implementation velocity outside primary metros will remain constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Cloud Gains Momentum

Public Cloud retained a 67.05% share of the ASEAN cloud computing market in 2025, backed by elastic pricing and abundant regional availability zones. Hybrid Cloud is forecast to post a 15.85% CAGR, generating the largest incremental addition to the ASEAN cloud computing market size between 2026-2031. Telecom operators such as AIS are blending local sovereignty with global services by launching domestically owned hyperscale platforms. Private Cloud installations continue among regulated banks and hospitals but are expected to cede share as security postures mature.

Hybrid growth springs from multi-cloud governance tooling, container portability, and maturing zero-trust frameworks. Enterprises now segment latency-critical analytics to local nodes while routing burst workloads to public zones, optimizing cost and compliance simultaneously. The approach unlocks new addressable opportunities for orchestration vendors and managed-service providers that can bridge hybrid estates across ASEAN’s diverse data-regulation landscape.

By Service Model: Platform Services Accelerate Innovation

Software as a Service contributed 55.65% revenue in 2025 and remains the market’s most mature delivery mode. Platform as a Service, however, is on track for a 16.3% CAGR, reflecting rising developer demand for serverless runtimes and integrated DevSecOps pipelines. The PaaS surge enlarges the ASEAN cloud computing market size for developer-centric tooling, with VNPT targeting USD 11.3 billion cloud-related revenue on the back of platform services.

Micro-services, AI model hosting, and IoT event streams require managed middleware that abstracts infrastructure yet preserves flexibility, positioning PaaS as the essential layer for rapid product cycles. SaaS uptake remains strong among HR, CRM, and ERP workloads, especially for mid-market firms seeking turnkey solutions. IaaS growth continues but at a tempered pace as abstraction layers climb the value chain.

By Organization Size: SME Digitalization Drives Growth

Large Enterprises held 62.55% of the ASEAN cloud computing market share in 2025, given their complex integration needs and sizable IT budgets. Yet SMEs will expand the pie quickest at 16.65% CAGR as governments subsidize onboarding costs and provide skills vouchers. Bundled SaaS suites with pre-configured compliance templates simplify adoption, while pay-as-you-go billing eases entry barriers.

Cloud marketplaces now highlight industry-specific solutions for retail, F&B, and professional services, reflecting SMEs’ preference for outcome-based buying rather than infrastructure tinkering. Such democratization spreads ASEAN cloud computing market adoption beyond capital cities into secondary provinces where digital commerce is emerging rapidly.

By End-user Industry: Healthcare Transformation Accelerates

Telecom and IT accounted for 28.35% of 2025 revenue, leveraging cloud for network functions, streaming, and over-the-top media. Healthcare, posting a 16.7% CAGR, benefits from telemedicine roll-outs, AI diagnostics, and electronic medical record mandates. Manufacturing’s Industry 4.0 push, BFSI’s real-time payment systems, and government e-services likewise sustain multi-vertical traction.

Providers now bundle HIPAA-aligned architectures, FHIR APIs, and data-anonymization toolkits to fast-track healthcare deployments, de-risking compliance and attracting venture capital into digital-health start-ups. Concurrently, telecom operators monetize edge clouds to host medical imaging inference engines near hospitals, underscoring cross-industry synergies.

Geography Analysis

Singapore commanded 36.10% of the ASEAN cloud computing market in 2025, supported by USD 9 billion AWS and USD 5 billion Google expansions that deepen the island’s multi-availability-zone density. Facebook’s 150 MW facility complements hyperscale footprints, although land scarcity pushes new builds into nearby Johor, Malaysia. Singapore’s Green Data Center Roadmap incentivizes liquid cooling and renewable procurement, enabling growth without breaching carbon caps.

Vietnam exhibits the highest trajectory with 16.5% CAGR, driven by the 2030 mandate for universal public-sector cloud adoption. Market liberalization now permits 100% foreign equity in data-center ventures. Domestic champions like Viettel are racing hyperscalers to roll out Tier III+ facilities, ensuring compliance pathways for critical manufacturing and e-government workloads.

Malaysia leverages its Johor corridor to relieve Singapore’s capacity crunch while rolling out a National Cloud Policy that balances sovereignty with economic targets. Indonesia remains the region’s largest single-country addressable base; Chinese cloud providers and local telcos co-finance new regions to localize gaming, fintech, and retail workloads. Thailand, meanwhile, aligns its smart-grid and industrial automation agendas with domestic cloud plants, supported by USD 1.8 billion in approved hyperscale projects.

Competitive Landscape

Competition is intensifying as hyperscalers jostle for capacity lead times, sovereign-cloud concessions, and sector-specific certifications. AWS, Microsoft, and Google collectively invested more than USD 20 billion across ASEAN since 2024, focusing on carbon-neutral builds and AI accelerators. Oracle deviates by pairing distributed-cloud offerings with local telcos, evidenced by its USD 30 billion multi-year contract and the first Thai-owned hyperscale cloud. [4]Network World, “Oracle inks $30 billion cloud deal…,” networkworld.com

Chinese entrants amplify price competition and diversify service stacks. Tencent’s third Indonesian region, Alibaba Cloud’s AI partner program, and Huawei Cloud’s APAC AI scaling plan collectively lower infrastructure costs and speed market entry for start-ups. Their local joint ventures help navigate data rules and provide multilingual support teams.

Regional telcos and data-center specialists are carving sovereign niches by pairing brownfield fiber assets with new cloud regions. AIS’s domestic platform, Viettel’s Hanoi mega-site, and Philippine carriers’ edge zones all underscore a trend toward national champions. Overall, the top five providers control roughly 55-60% of regional IaaS+PaaS spending, indicating a moderately consolidated yet contestable landscape.

ASEAN Cloud Computing Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC (Alphabet Inc.)

Alibaba Cloud (Alibaba Group Holding Limited)

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oracle secured a cloud contract expected to generate over USD 30 billion annually from fiscal 2028, significantly expanding its Asia-Pacific footprint.

- June 2025: Vietnam approved a national program mandating that 100% state agencies use the cloud by 2030.

- May 2025: Malaysia’s Data Protection Department issued Cross-Border Transfer Guidelines, influencing deployment design.

- April 2025: Tencent Cloud launched a new Osaka region, broadening redundancy options for ASEAN customers.

- March 2025: Microsoft announced plans for a Malaysian cloud region to support national digital goals.

- February 2025: Tencent Cloud unveiled its first Middle East region in Saudi Arabia, widening intercontinental replication paths.

- November 2024: GoTo Group, Tencent Cloud, and Alibaba Cloud committed USD 500 million for Indonesia’s third data center and talent training.

ASEAN Cloud Computing Market Report Scope

Cloud computing offers a vast range of computing services over the Internet. These services include servers, storage, databases, networking, software, analytics, and intelligence. Key advantages of cloud computing are accelerated innovation, flexible resource allocation, and economies of scale. Customers generally pay only for the services they use. This approach cuts operational costs, boosts infrastructure efficiency, and enables scaling to meet changing business demands.

The ASEAN cloud computing market is segmented by type (public cloud [IaaS, PaaS, SaaS], private cloud, and hybrid cloud), organization size (SMEs and large enterprises), end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, others [utilities, media & entertainment etc.]), and country (Singapore, Thailand, Malaysia, Indonesia, Vietnam, Philippine, Rest of ASEAN). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) |

| Software as a Service (SaaS) |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Utilities |

| Other End-user Industries |

| Singapore |

| Thailand |

| Malaysia |

| Indonesia |

| Vietnam |

| Philippines |

| Others |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) | |

| Software as a Service (SaaS) | |

| By Organization Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Industry | Manufacturing |

| Education | |

| Retail | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Utilities | |

| Other End-user Industries | |

| By Country | Singapore |

| Thailand | |

| Malaysia | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Others |

Key Questions Answered in the Report

What is the current size of the ASEAN cloud computing market?

The market reached USD 24.91 billion in 2026.

How fast is the ASEAN cloud computing market expected to grow?

It is forecast to expand at a 14.35% CAGR, hitting USD 48.74 billion by 2031 during the forecast period (2026-2031).

Which deployment model is growing the fastest?

Hybrid Cloud is projected to grow at a 15.85% CAGR through 2031.

Why is Vietnam considered the fastest-growing market?

Vietnam’s mandate for 100% public-sector cloud use and liberalized foreign ownership underpin a 16.5% CAGR.

What sector offers the strongest upside for providers?

Healthcare, with a 16.7% CAGR, leads due to telemedicine and AI diagnostics.

How significant are data-sovereignty rules for cloud strategy?

They can reduce regional CAGR by 1.8% and compel providers to localize data centers, influencing architecture and cost.

Page last updated on: