Cloud Integration Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

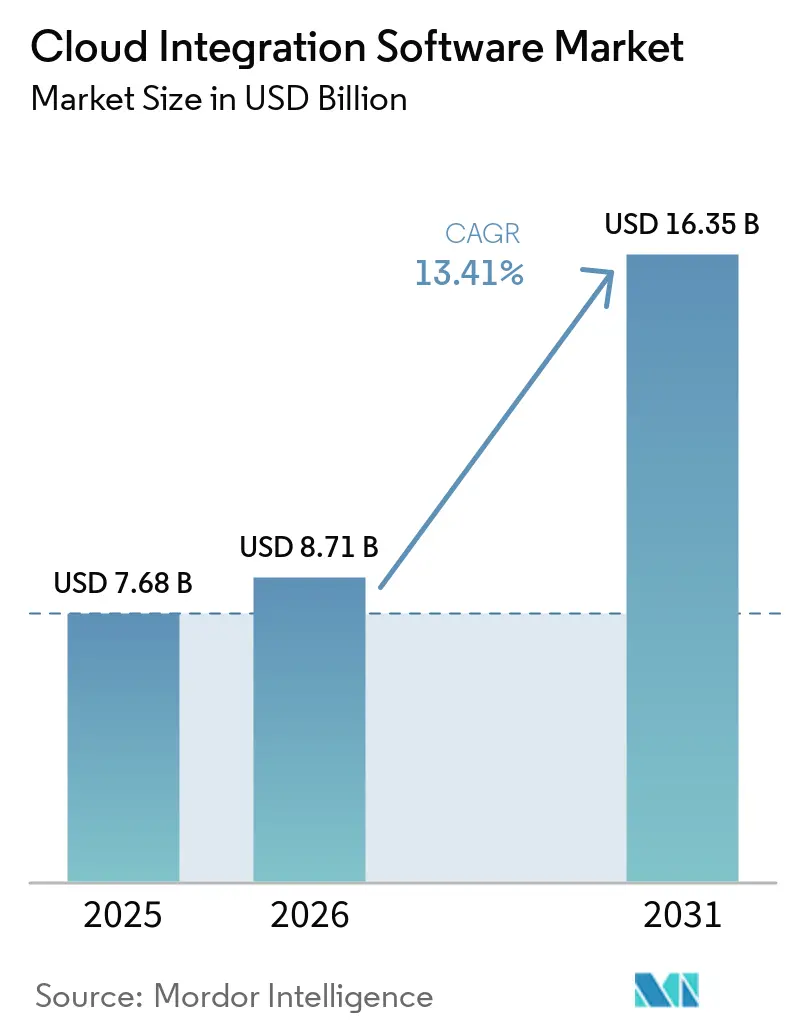

| Market Size (2026) | USD 8.71 Billion |

| Market Size (2031) | USD 16.35 Billion |

| Growth Rate (2026 - 2031) | 13.41% CAGR |

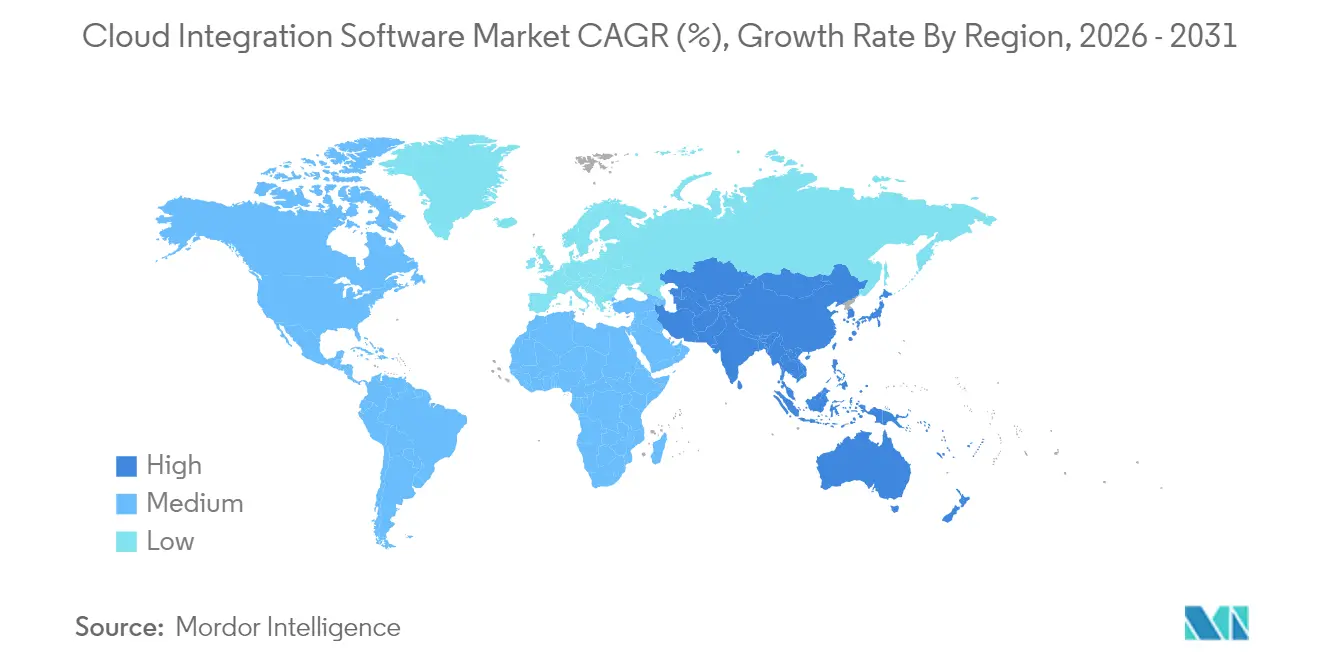

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Integration Software Market Analysis by Mordor Intelligence

The cloud integration software market size was valued at USD 7.68 billion in 2025 and estimated to grow from USD 8.71 billion in 2026 to reach USD 16.35 billion by 2031, at a CAGR of 13.41% during the forecast period (2026-2031). Most enterprises now distribute workloads across at least two hyperscalers to contain vendor lock-in while matching compute profiles to use-case needs. Growth is amplified by sprawling SaaS portfolios that must exchange data in real time, rising adoption of event-driven analytics engines, and factory modernisation initiatives that link edge sensors with cloud AI platforms. Uptake is further helped by low-code tooling that reduces time-to-value, plus vendor consolidation that bundles API management, data pipelines, and governance in a single contract. Headwinds such as cross-border data controls and hyperscaler egress fees are pushing providers toward hybrid deployment models that process sensitive records locally while still supporting global collaboration[1]ISACA, “Data Sovereignty: Compliance Risk in a Cloud World,” isaca.org.

Key Report Takeaways

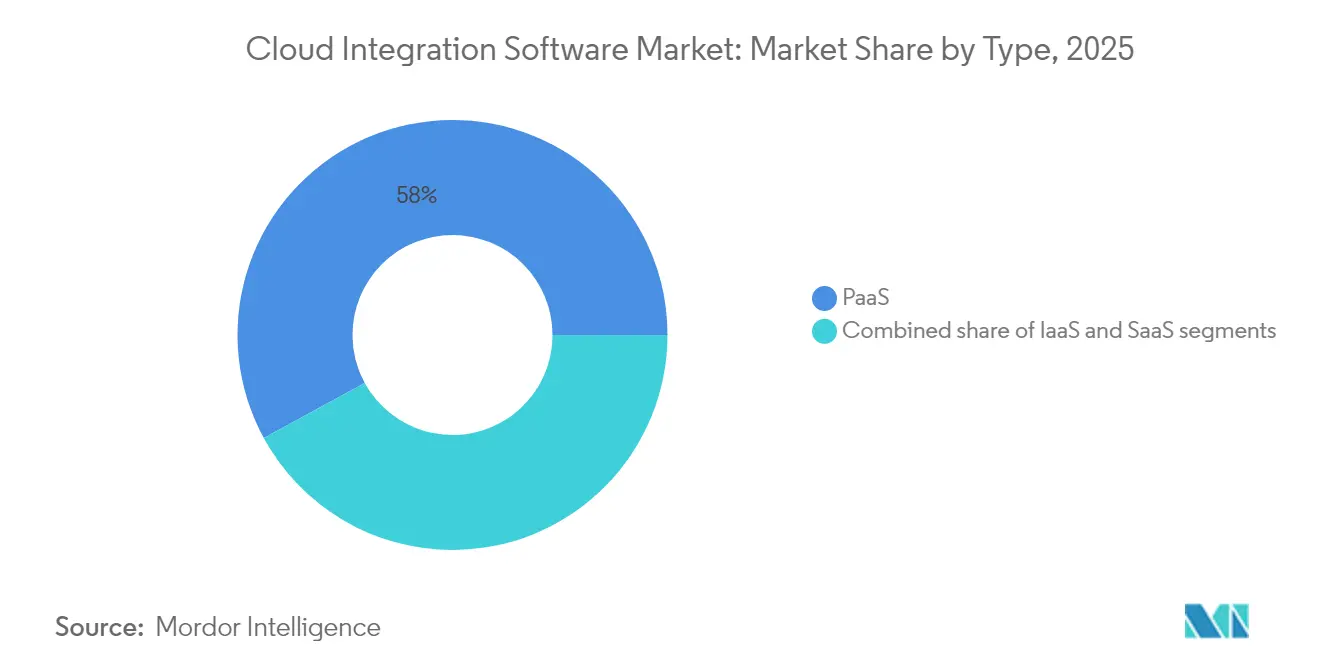

- By platform type, Platform-as-a-Service held 57.95% of cloud integration software market share in 2025; Software-as-a-Service integration platforms are forecast to expand at a 15.12% CAGR through 2031.

- By integration type, Application Integration captured 36.45% revenue share in 2025, while API Management is set for the fastest 14.02% CAGR through 2031.

- By enterprise size, large enterprises accounted for 70.88% share of the cloud integration software market size in 2025, whereas small and medium enterprises post the highest 14.89% CAGR to 2031.

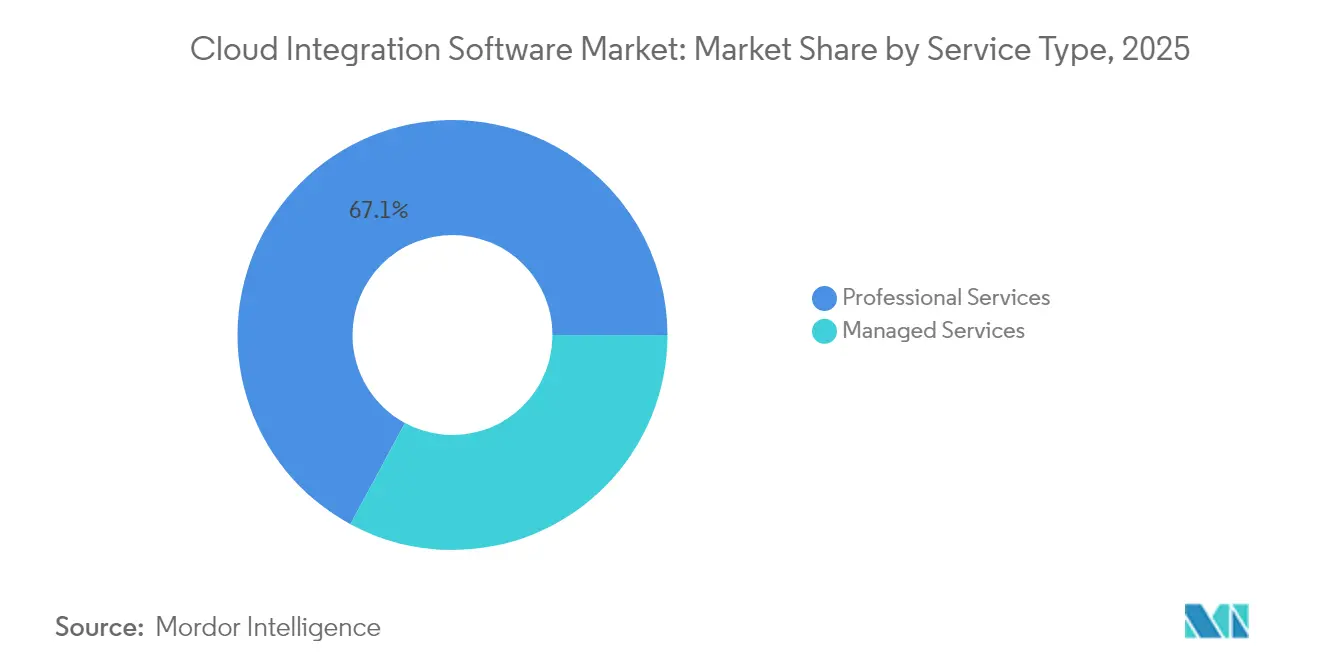

- By service type, Professional Services represented 67.12% share in 2025; Managed Services will grow at a 14.45% CAGR through 2031.

- By end-user industry, BFSI led with 22.34% revenue share in 2025; manufacturing is projected to advance at a 13.72% CAGR through 2031.

- By geography, North America maintained 36.02% share of the cloud integration software market size in 2025, while Asia-Pacific records the quickest 14.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Integration Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of multi-cloud adoption | +3.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| SaaS application sprawl requiring unified integration | +2.8% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Need for real-time data analytics and API-led connectivity | +2.5% | APAC core, North America and Europe | Medium term (2-4 years) |

| Event-driven architectures in microservices | +2.1% | Global, concentrated in tech hubs | Long term (≥ 4 years) |

| Edge-to-cloud orchestration for Industry 4.0 | +1.8% | Manufacturing regions: Germany, China, Japan | Long term (≥ 4 years) |

| Monetisation of marketplace connectors (iPaaS) | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Multi-Cloud Adoption

Enterprises treat multi-cloud as a competitive lever rather than an insurance policy, matching GPU-dense nodes to AI training while housing regulated data in sovereign regions[2]Microsoft, “Design Patterns for Multi-Cloud Architectures,” microsoft.com. Hyperscalers respond with cross-cloud database and networking services that trim latency and erase egress fees, spurring demand for control planes that abstract policy enforcement across providers. Unified governance hastens partner onboarding because encryption and logging remain consistent no matter where workloads land.

SaaS Application Sprawl Requiring Unified Integration

With the average enterprise now running more than 360 SaaS apps, point-to-point links crack under scale, fragmenting data and harming compliance. Modern iPaaS bundles pre-built connectors, schema mapping, and version control so teams can sync records instantly without scripting. Vendors further add API marketplaces that let customers sell curated connectors, turning integration from back-office cost into incremental revenue.

Need for Real-Time Data Analytics and API-Led Connectivity

Streaming analytics shifts integration from nightly batch runs to millisecond event processing at the network edge, where sensors feed AI inference and push results to cloud dashboards. API management layers add metering and product-style SLAs so firms can expose data to partners safely, encouraging monetisation and wider ecosystem reach.

Event-Driven Architectures in Microservices

Microservice estates migrate from synchronous REST calls toward event buses that buffer traffic during partial outages, improving resilience while lowering coupling mdpi.com. Integration platforms now ship Kafka and Pulsar connectors out of the box, letting developers build routing logic visually and auto-scale capacity with container orchestrators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and compliance complexity | -2.1% | EU, China, emerging markets with strict regulations | Short term (≤ 2 years) |

| Legacy on-prem integration complexity | -1.8% | Global, particularly in traditional industries | Medium term (2-4 years) |

| Rising hyperscaler egress charges | -1.2% | Global, affecting multi-cloud strategies | Short term (≤ 2 years) |

| Scarcity of cloud-native integration talent | -0.9% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Compliance Complexity

Fragmented privacy laws force teams to build region-specific pipelines that keep regulated data resident while still enabling global analytics. Vendors answer with sovereign cloud zones and policy-based routing, but compliance audits prolong rollouts and inflate operating costs.

Legacy On-Premises Integration Complexity

Mainframe and proprietary middleware remain vital in banking, healthcare, and government, yet expose limited API endpoints. Toolkits that bridge COBOL, JMS, or FTP into modern REST or event streams lower risk during phased migrations but demand scarce skillsets[3]IBM, “IBM Expands Consulting Capabilities with AST Acquisition,” ibm.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: SaaS Platforms Drive Next-Generation Integration

Platform-as-a-Service kept 57.95% share in 2025 because large enterprises need advanced customisation. Yet SaaS integration will grow 15.12% annually, thanks to instant scaling, built-in observability, and subscription pricing that slashes CapEx. Vendors weave AI-based data mapping and anomaly detection into their SaaS layers, letting citizen developers build flows without code while security teams remain in control.

For regulated sectors, Infrastructure-as-a-Service integration maintains relevance by anchoring workloads on dedicated hosts under strict audit. These deployments often rely on Kubernetes operators that enforce policy templates and replicate secrets across clusters.

By Integration: API Management Accelerates Microservices Adoption

Application Integration dominated revenue at 36.45% in 2025, underpinning ERP and CRM linkages. API Management, however, will post a 14.02% CAGR as firms monetise digital assets and adopt microservices. Gateways now ship with self-service developer portals, quota enforcement, and schema introspection, shrinking partner onboarding windows from months to days.

EDI modernisation also gains steam: manufacturers replace batch flat-file exchanges with real-time event streams that improve inventory turns and reduce stock-outs.

By Enterprise Size: SMEs Embrace Cloud-Native Solutions

Large enterprises captured 70.88% of 2025 spending by virtue of complex estates that span multiple clouds. Yet SMEs lead growth at 14.89% CAGR because low-code SaaS platforms remove infrastructure burdens and bill per connector rather than per server. Managed-service wrappers further entice resource-constrained firms by bundling monitoring, patching, and 24x7 support into a single monthly fee.

By Service Type: Managed Services Transform Delivery Models

Professional Services remained 67.12% of 2025 revenue because custom connector development and change management are still essential for global rollouts. Managed Services will grow 14.45% annually as vendors offer outcome-based contracts that guarantee throughput and latency while using AI to auto-remediate failures.

By End-User Industry: Manufacturing Drives Digital Transformation

BFSI commanded 22.34% revenue share in 2025 because real-time fraud screening requires low-latency data fusion across channels oracle.com. Manufacturing is on track for 13.72% CAGR as Industry 4.0 deployments connect plant-floor robots with cloud analytics to optimise yield and schedule predictive maintenance.

Geography Analysis

North America held 36.02% market share in 2025, buoyed by deep cloud expertise, permissive data-flow regimes, and proximity to vendor headquarters that grants early access to bleeding-edge features. Enterprises here adopt AI-driven integration observability that correlates API calls, message queues, and data pipelines under one pane of glass.

Asia-Pacific is forecast for the fastest 14.25% CAGR through 2031. Sovereign cloud programs require hybrid platforms able to enforce data-residency while still syncing R and D workloads globally. Rapid 5G deployment and IoT proliferation in China, Japan, and South Korea generate telemetry bursts that must be cleansed at the edge before archive to central data lakes.

Europe keeps sizable share due to strict privacy mandates that emphasise audit logs, consent workflows, and immutable data lineage. The upcoming Digital Operational Resilience Act will push financial institutions to adopt event-streaming architectures that survive single-point failures.

Competitive Landscape

The five leading vendors—Salesforce (MuleSoft), Oracle, Informatica, SAP, and Boomi—jointly command 57.7% of revenue, signalling moderate concentration. Incumbents differentiate via AI-assisted mapping, unified governance, and breadth of pre-built connectors. Disruptors like SnapLogic and Workato focus on citizen developers, embedding generative AI helpers that auto-generate pipelines from natural-language prompts.

Strategic consolidation accelerates: Salesforce’s USD 8 billion Informatica deal merges API-led connectivity with enterprise data governance, while IBM’s acquisition of integration specialists deepens public-sector reach. Vendors now invest in lightweight runtimes for edge deployment and embedded cost-optimisation dashboards that advise on instance right-sizing to curb cloud-spend inflation.

Cloud Integration Software Industry Leaders

Microsoft Corporation

Oracle Corporation

Informatica Corporation

SAP SE

TIBCO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce completed its USD 8 billion acquisition of Informatica, creating the industry’s most comprehensive data and application integration platform that combines MuleSoft’s API-led connectivity with Informatica’s enterprise data management capabilities to support autonomous AI agents.

- April 2025: Oracle announced partnerships with Google Cloud and OpenAI, enabling seamless workload deployment across cloud platforms without data transfer charges while providing Oracle Database services directly within Google Cloud data centers to support AI model training and deployment.

- March 2025: Oracle integrated NVIDIA AI Enterprise software platform across Oracle Cloud Infrastructure, providing access to over 160 AI tools and NIM microservices while ensuring compliance with local regulations for sovereign cloud deployments.

- February 2025: Salesforce and Google Cloud expanded their partnership to deliver autonomous AI agents that collaborate across Salesforce Customer 360 and Google Workspace applications, enabling bi-directional data usage between Google BigQuery and Salesforce without data duplication.

- January 2025: IBM acquired Applications Software Technology to enhance Oracle Cloud expertise for public sector clients, following the company’s strategy of acquiring specialised consulting capabilities to support digital transformation initiatives.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the cloud integration software market comprises any licensed or subscription-based platforms that enable data, application, API, process, and B2B/EDI flows to move seamlessly between public, private, or hybrid cloud workloads and on-premise systems. The scope spans pre-packaged integration platform-as-a-service (iPaaS), cloud data integration suites, and low-code middleware that deliver transformation, mapping, monitoring, and governance functions through a managed runtime.

Scope exclusions include tools sold solely for one-way backup/sync, bespoke professional service code, and pure on-premise ESB appliances that are not included.

Segmentation Overview

- By Type

- PaaS

- IaaS

- SaaS

- By Integration

- Application Integration

- Data Integration

- API Management

- Process Integration and Orchestration

- B2B/EDI Integration

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Service Type

- Professional Services

- Managed Services

- By End-user Industry

- BFSI

- IT and Telecom

- Retail and E-commerce

- Education

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Insights were refined through interviews and surveys with CIOs, integration architects, cloud procurement heads, and managed service providers across North America, Europe, and Asia-Pacific. These dialogues clarified average seat counts, API call bursts, licensing shifts toward event-based pricing, and barriers linked to data residency, letting us verify assumptions arising from secondary data.

Desk Research

Our analysts opened with structured desk work that mapped the universe of cloud deployments and integration touchpoints. Public sources such as US Bureau of Labor Statistics ICT spend tables, Eurostat cloud adoption surveys, Gartner open data portals, OECD ICT price indices, and industry associations like Cloud Native Computing Foundation provided baseline volume and price signals. Company 10-Ks, S-1s, and earnings calls clarified vendor billings, while patent analytics from Questel and shipment traces from Volza indicated emerging architecture choices. This collection offered the groundwork; it is illustrative rather than exhaustive, as many additional feeds informed validation.

Market-Sizing & Forecasting

A top-down construct begins with enterprise cloud workload counts and regional SaaS spending, which are then aligned to integration penetration ratios and blended average selling prices. Supplier roll-ups, channel checks, and sampled invoice reviews serve as selective bottom-up cross-checks that anchor totals. Key variables tracked include: 1) number of SaaS apps per enterprise, 2) multi-cloud workload share, 3) annual iPaaS subscription price bands, 4) average monthly API call volumes, and 5) cloud data egress fees. Multivariate regression on these drivers, followed by scenario analysis for macro shocks, generates the 2025-2030 curve. Data gaps in smaller geographies are bridged by proxy metrics such as internet bandwidth per capita and developer population.

Data Validation & Update Cycle

Outputs undergo variance checks against third-party benchmarks and historical series; anomalies trigger analyst escalation before sign-off. Mordor refreshes every 12 months, with interim revisions when material M&A or regulatory changes surface, and a final pre-publication sweep ensures clients receive the latest view.

Why Mordor's Cloud Integration Software Baseline Commands Reliability

Estimates published by research firms often diverge because each chooses unique market boundaries, cost assumptions, and refresh timing. Buyers deserve clarity on these gap drivers.

Key differences arise when some studies fold integration consulting revenue into software, cap calculations to a single region, or apply uniform price points that ignore consumption-based tiers. Mordor's model reports software-only revenue, applies geography-specific ASPs, and draws on a yearly refresh cycle; these guardrails reduce inflation or understatement.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.68 B (2025) | Mordor Intelligence | - |

| USD 3.66 B (2023) | Global Consultancy A | narrower geographic scope and excludes API management modules |

| USD 10.47 B (2024) | Industry Portal B | bundles integration services and uses list pricing without usage tier adjustments |

In sum, by aligning a clearly defined scope with mixed-method data capture and an annual refresh cadence, Mordor Intelligence offers decision-makers a balanced, transparent baseline they can replicate and stress test with confidence.

Key Questions Answered in the Report

What fuels the 13.41% CAGR expected for cloud integration software?

Enterprises need to unify data across multi-cloud environments, manage fast-growing SaaS portfolios, and support real-time analytics at the network edge, driving sustained double-digit growth.

Which deployment model grows the fastest?

SaaS-based integration platforms expand at a 15.12% CAGR because they offer turnkey scaling, low-code tooling, and subscription pricing that aligns with operating budgets.

How do data-sovereignty laws influence integration strategy?

Firms adopt hybrid models that keep sensitive data inside national borders while syncing anonymised insights globally, increasing demand for policy-driven routing and sovereign cloud zones.

Which region shows the highest growth potential through 2031?

Asia-Pacific leads with a projected 14.25% CAGR, boosted by sovereign cloud programs, 5G rollout, and industrial IoT investments.

Why are managed services gaining popularity?

Outcome-based managed contracts shift monitoring and remediation to providers, reduce downtime, and let enterprises focus on innovation rather than infrastructure upkeep.

Page last updated on: