Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

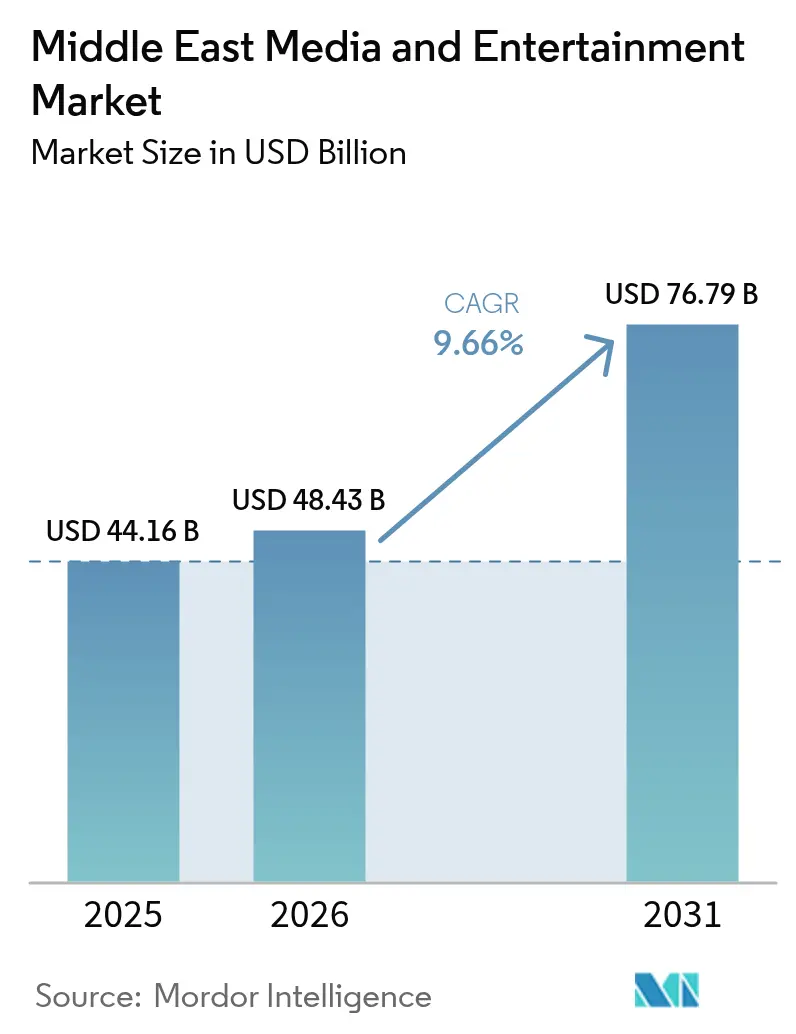

| Base Year Market Size (2025) | USD 44.16 Billion |

| Market Size (2026) | USD 48.43 Billion |

| Market Size (2031) | USD 76.79 Billion |

| Growth Rate (2026 - 2031) | 9.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Media And Entertainment Market Analysis by Mordor Intelligence

The Middle East Media And Entertainment Market size is projected to be USD 44.16 billion in 2025, USD 48.43 billion in 2026, and reach USD 76.79 billion by 2031, growing at a CAGR of 9.66% from 2026 to 2031.

This rapid trajectory springs from Vision 2030-driven economic diversification, region-wide 5G and fiber roll-outs, and an audience skewed toward digitally native youth. Saudi Arabia anchors demand through large-scale state investment, while the United Arab Emirates (UAE) races ahead by commercializing advanced connectivity and a pro-innovation regulatory climate. Online video, gaming, and immersive formats gain momentum as smartphone ubiquity, cloud infrastructure, and metaverse programs converge. Strategic partnerships between regional broadcasters and global streamers are reshaping competitive rules, and flexible monetization mixes are becoming essential to offset currency-linked advertising volatility.

Key Report Takeaways

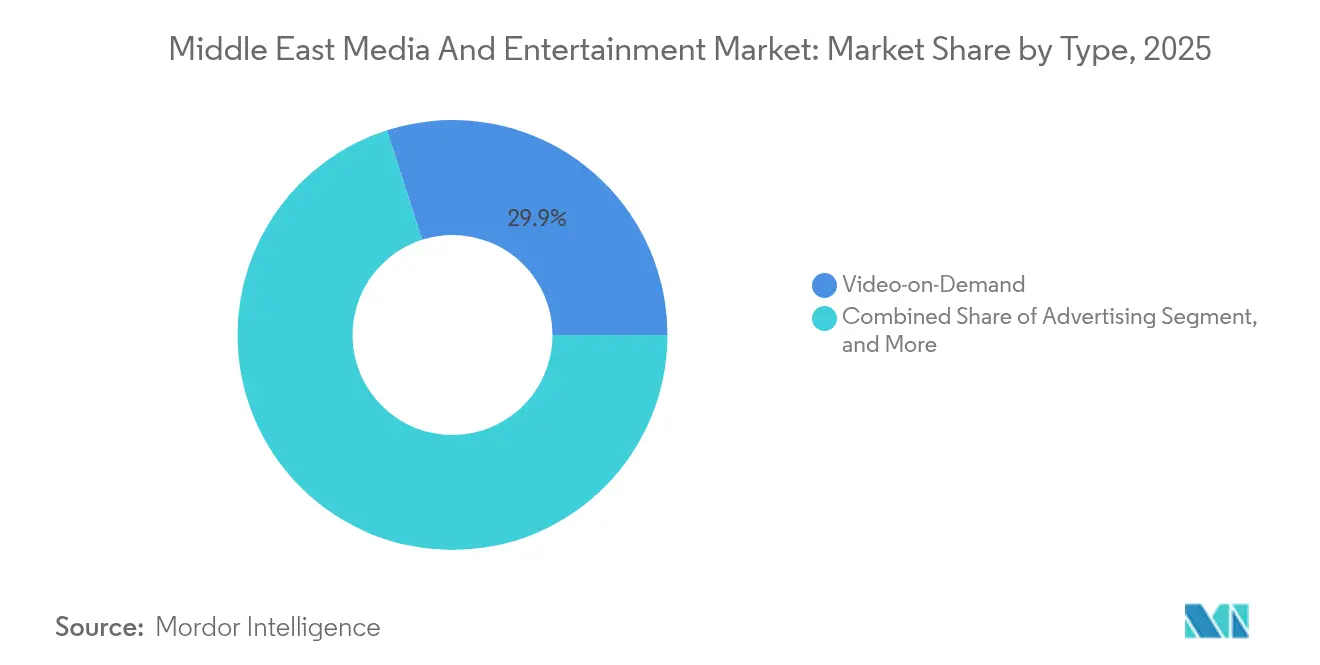

- By type, video-on-demand led with 29.93% revenue share of the Middle East media and entertainment market in 2025; advertising is projected to log the fastest 11.05% CAGR through 2031.

- By platform, online/digital captured 59.62% of the Middle East media and entertainment market share in 2025, while hybrid approaches are advancing at a 10.65% CAGR through 2031.

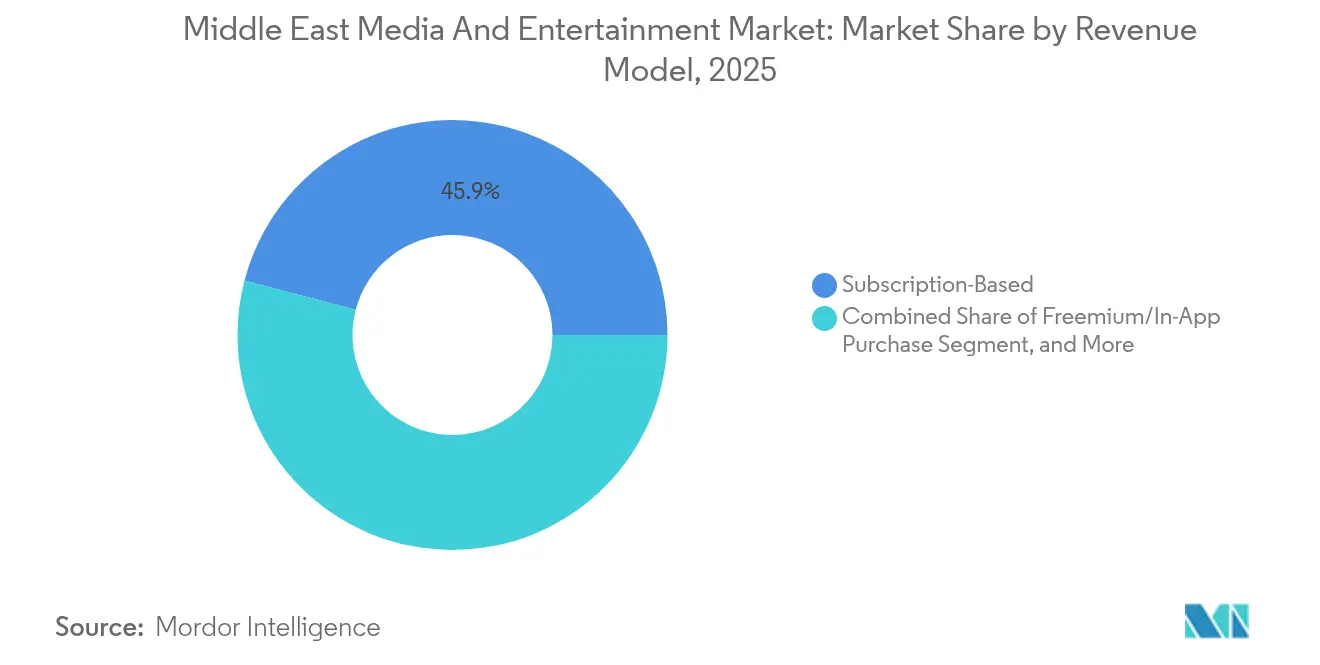

- By revenue model, subscriptions accounted for 45.92% of the Middle East media and entertainment market size in 2025; freemium and in-app purchase models are expected to grow at an 10.96% CAGR to 2031.

- By age group, millennials held a 35.62% share of the Middle East media and entertainment market in 2025, but Generation Z is growing fastest at an 11.19% CAGR through 2031.

- By device, smartphones commanded 44.88% share of the Middle East media and entertainment market in 2025, whereas VR/AR headsets should escalate at an 11.49% CAGR during the forecast.

- By geography, Saudi Arabia dominated with a 39.22% share of the Middle East media and entertainment market in 2025; the UAE registers the highest 11.08% CAGR toward 2031.

- The Public Investment Fund, MBC Group, and beIN MEDIA GROUP jointly held an estimated 41% revenue share in 2024 amid rising state-backed consolidation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Media And Entertainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated rollout of 5G networks and fibre broadband | +2.1% | Saudi Arabia, UAE, Qatar core with spillover to Kuwait, Bahrain | Medium term (2-4 years) |

| Booming smartphone and smart-TV penetration enabling OTT growth | +1.8% | Regional with strongest impact in Saudi Arabia, UAE | Short term (≤ 2 years) |

| Government-funded mega-events boosting content demand | +1.4% | Saudi Arabia (Vision 2030), UAE (Expo legacy), Qatar (World Cup legacy) | Long term (≥ 4 years) |

| Rapid rise of esports and in-app micro-transactions | +1.2% | Saudi Arabia, UAE leading with expansion across GCC | Medium term (2-4 years) |

| Arabic-language original production incentives | +1.0% | Saudi Arabia, UAE primary with regional content distribution | Long term (≥ 4 years) |

| Growing diaspora demand for Middle-East content on global platforms | +0.9% | Global reach with concentration in North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Rollout of 5G Networks and Fiber Broadband

Telecommunications incumbents continue to blanket major cities with 5G coverage, furnishing latency below 10 milliseconds and enabling 4K streaming, cloud gaming, and real-time augmented-reality services. Saudi Telecom Company allocated more than USD 2.4 billion to 5G and fiber upgrades in 2024, underscoring its pivot from voice carrier to digital-service orchestrator. UAE operators have already surpassed 95% fiber-to-the-home penetration in core emirates, creating a competitive scramble to monetize bandwidth with premium OTT bundles and interactive advertising inventory.

Booming Smartphone and Smart-TV Penetration Enabling OTT Growth

Regional smartphone penetration crossed 90% in 2024, and smart-TV connections doubled in Saudi homes over the past three years. This device base encourages consumers to bypass legacy satellite boxes in favor of direct-to-consumer apps, lifting paid subscription loyalty while widening addressable audiences for targeted programmatic ads. As internet connection speeds climb, average viewing hours on mobile screens have overtaken linear television among audiences below 35.

Government-Funded Mega-Events Boosting Content Demand

Fiscal stimulus targeting film, music, and live-event ecosystems continues to catalyze the Middle East media and entertainment market. Saudi Arabia’s USD 233 million film-sector financing program opened long-term credit lines for local productions, accelerating studio build-outs and job creation. [1]Melanie Goodfellow, “Saudi Arabia Launches USD 233 Million Film Financing Program,” Deadline, deadline.com Legacy from Expo 2020 Dubai and the Qatar World Cup sustains tourism-linked content pipelines, nurturing event coverage, documentaries, and commercial tie-ins that keep the global spotlight on the region.

Rapid Rise of Esports and In-App Micro-Transactions

Gaming revenues rose from USD 2.2 billion in 2024 toward a projected USD 4.7 billion by 2033 in Saudi Arabia alone, pushing publishers and platforms to replicate flexible monetization models across music and video verticals. [2]Kwalee, “2024 Guide to the Fast-Growing MENA Games Market,” kwalee.com Government-run accelerators such as the “Game Changers” program are seeding developer talent, while stadium-scale esports tournaments generate ancillary ad and sponsorship sales far beyond ticket revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High levels of piracy and illicit streaming sites | -1.6% | Regional with highest impact in Saudi Arabia, Egypt | Short term (≤ 2 years) |

| Fragmented regulatory and censorship regimes across countries | -1.2% | Pan-regional with varying intensity by jurisdiction | Long term (≥ 4 years) |

| Talent shortage in advanced VFX/game development | -0.8% | Saudi Arabia, UAE primary with regional spillover | Medium term (2-4 years) |

| Currency-linked ad-spend volatility due to oil price swings | -0.7% | GCC countries with oil-dependent economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Levels of Piracy and Illicit Streaming Sites

The 2024 takedown of Cima4U, an illegal portal with 30 million monthly visits, underscored the revenue leakage jeopardizing premium platforms. Despite improved enforcement, 23% of regional users still access pirate IPTV boxes, and account sharing hits 35% in Saudi Arabia, diluting subscription value and deterring premium advertisers who demand verified reach metrics.

Fragmented Regulatory and Censorship Regimes Across Countries

Content creators juggle eight separate broadcast-media statutes across Gulf states alone, inflating legal vetting costs. The UAE’s Decree-Law 55 of 2023 anchors local values, mandating edits to material deemed contrary to Islamic principles or social harmony, with fines reaching AED 1 million. [3]UAE Government, “Media Regulation,” u.ae This patchwork complicates the scaling of pan-Arab content libraries and strains release schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Video-on-Demand Dominates Amid Advertising Acceleration

The segment generated USD 13.22 billion in 2025, amounting to 29.93% of the Middle East media and entertainment market. Advertising, worth USD 7.24 billion, is expected to expand at an 11.05% CAGR as programmatic tools mature. Premium series, live sports replays, and diversified genres keep subscription renewal high, aided by improved measurement that helps brands allocate budgets confidently. The Middle East media and entertainment market size for advertising-supported formats could therefore outpace transactional video once real-time bidding and audience graphs reach scale. Regional music streaming consolidations—such as Anghami’s union with OSN+—point to synergistic cross-sell prospects, while video-game revenues ride mobile penetration and national esports leagues.

Content localization remains central; incentive funds underwrite Arabic scripts, and dubbing contests ensure regional dialect authenticity. Publishers see e-books gain traction as educational ministries digitize curricula, though monetization relies on micropayments rather than outright downloads. Meanwhile, internet access services furnish the substrate for all categories; yet price competition and regulatory fee caps constrain their growth contribution relative to higher-margin content verticals.

By Platform: Digital Leadership with Hybrid Momentum

Online and app-based environments contributed 59.62% of the total 2025 revenue, affirming the primacy of direct-to-consumer delivery in the Middle East media and entertainment market. Fast-growing hybrid models merging linear channels with on-demand libraries now track a 10.65% CAGR, a pace that reflects consumer appetite for choice without sacrificing live communal viewing. MBC’s bundling of Netflix inside the MBCNOW TV box illustrates how incumbents protect linear ad pools while upselling global catalogs. Traditional satellite still serves rural homes and older viewers, positioning hybrid set-tops as a soft migration path instead of abrupt cord-cutting.

For advertisers, platform diversity complicates reach but opens granular targeting. Cross-screen campaigns integrate linear ratings, OTT impressions, and social video engagements to maximize frequency without redundancy. As data-privacy codes tighten, first-party data from hybrid login environments strengthens value propositions, giving operators leverage over pure-play digital rivals lacking broadcast networks.

By Revenue Model: Subscription Strength Meets Freemium Disruption

Subscriptions held a 45.92% share in 2025, buoyed by household pay-TV upgrades and binge-worthy drama launches. Yet the freemium and in-app purchase segment is on track to eclipse USD 15.62 billion by 2031, its 10.96% CAGR reflecting gaming influence on wider entertainment habits. The Middle East media and entertainment market size for freemium pathways gains from low entry barriers, allowing mass sampling before micro-transaction conversion. Pay-per-view remains limited to marquee boxing cards and regional football tournaments, but dynamic pricing pilots hint at broader adoption once payment infrastructure matures. Ad-supported video climbs steadily as CPM yields rise alongside audience verification improvements.

Currency swings prompt platforms to experiment with multi-tier pricing denominated in local currencies while reporting consolidated earnings in USD, insulating revenue against petro-linked fluctuations. Bundling music, video, and cloud gaming inside single subscriptions improves average revenue per user and lengthens churn cycles, a trend accentuated after Warner Bros Discovery’s USD 57 million stake in OSN Streaming.

By End-User Age Group: Millennials Rule but Generation Z Surges

Millennials captured 35.62% revenue share in 2025 thanks to established purchasing power. Generation Z, however, accelerates with an 11.19% CAGR, fueling product decisions that prioritize mobile-first interactivity and creator-led content. Social-video challenges, esports tournaments, and influencer shopping streams resonate strongly, reshaping the Middle East media and entertainment market’s programming grid. Generation X and baby boomers still prefer long-form series and linear news, encouraging hybrid scheduling that alternates bingeable box-sets with appointment viewing. Platforms now segment marketing communication by life stage rather than merely chronological age, tailoring payment plans, parental controls, and cross-device synchronization features to each cohort.

Youth councils and ministries of culture invest in skills programs that mesh content creation with heritage preservation, fostering pipelines of Arabic-language animators and podcasters. This deliberate capacity building reduces external dependency and ensures region-specific narratives remain authentic and relatable.

By Device: Smartphones Lead While Immersive Gear Gains

Smartphones contributed 44.88% of 2025 consumption value, cementing their role as the principal screen for the Middle East media and entertainment market. VR/AR headsets, projected to climb at an 11.49% CAGR, benefit from Dubai’s metaverse blueprint, which targets USD 4 billion economic output and 42,000 jobs by 2030. Smart-TV shipments rise as vendors embed OSN, Shahid, and Netflix apps natively, simplifying sign-ups. Gaming consoles hold niche prestige among affluent youth, anchoring premium AAA releases and local esports leagues. Tablets serve education ministries pushing e-learning, whereas laptops keep their foothold among professionals and university students seeking higher-resolution productivity and video quality.

Government duty exemptions on VR equipment and grants to AR startups lower ownership hurdles, allowing museums, universities, and retail venues to pilot immersive storytelling. Device convergence also accelerates; foldable screens and 5G tethering blur lines between phone and tablet, while smart TVs double as console replacements through cloud gaming services.

Geography Analysis

Saudi Arabia retained 39.22% of the Middle East media and entertainment market in 2025, advancing from bold Vision 2030 allocations and the region’s largest youth demographic. Sector revenue reached SAR 17.4 billion (USD 4.6 billion) in the same year, with digital formats expanding at a 26% CAGR over five years. Public Investment Fund backing of MBC Group and landmark projects such as NEOM’s XR studios anchor the kingdom as both a production and distribution powerhouse. Gaming potential of USD 13.3 billion by 2030 and 39,000 projected jobs extend diversification beyond oil dependence.

The UAE is the fastest-growing sub-market, recording an 11.08% CAGR to 2031 on the strength of a fully articulated regulatory framework and its long-standing role as regional headquarters for multinationals. Dubai’s Metaverse Strategy alone aims for a USD 4 billion GDP impact, luring content tech firms and fostering a creative-class workforce. Warner Bros Discovery’s minority investment in OSN and Etisalat’s deployment of ultra-capacity 5G emphasize international confidence.

Qatar, Kuwait, and Bahrain ride post-mega-event tourism and cross-border content exchanges, with Qatar’s esports segment alone valued at USD 125.7 million in 2024. Joint marketing initiatives across the GCC nurture premium ad packages appealing to pan-regional brands. Rest-of-Middle-East territories exhibit heterogeneous regulatory landscapes yet offer upside in localized streaming catalogs adapted to linguistic and cultural nuance.

Competitive Landscape

The Middle East media and entertainment market remains moderately consolidated as state funds, legacy broadcasters, and tech-native entrants vie for scale. MBC Group, beIN MEDIA GROUP, and OSN collectively commanded around 41% revenue share in 2024, while Netflix, StarzPlay, and Shahid accelerate subscriber gains through localized originals. Public Investment Fund’s USD 2 billion acquisition of a 54% stake in MBC in November 2024 epitomizes sovereign intent to build national creative champions. Global entities increasingly prefer joint ventures instead of green-field expansion; Netflix’s July 2025 bundle with MBC NOW offers integrated billing, marketing, and set-top hardware.

Content is emerging as the decisive differentiator. Anghami’s merger with OSN+ couples music discovery with premium drama streaming, demonstrating ecosystem bundling as an antidote to churn. Korean giant CJ ENM opened its first Middle East subsidiary in Riyadh in July 2025 to co-produce Arabic-language adaptations of K-formats, exemplifying cross-cultural IP exchange. Smaller disruptors focus on esports broadcasting, children’s FAST channels, and vertical niches such as Islamic-compliant entertainment.

Capital inflows from sovereign funds lower financing costs for large-scale productions, but they also raise competitive entry barriers for pure start-ups. Meanwhile, rising expectations on cultural alignment, data residency, and compliance oblige foreign platforms to ally with local partners possessing regulatory know-how.

Middle East Media And Entertainment Industry Leaders

Middle East Broadcasting Center FZ-LLC (MBC Group)

Orbit Showtime Network FZ-LLC

beIN MEDIA GROUP LLC

Abu Dhabi Media Company PJSC

Arab Media Group LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Netflix partnered with MBC Group to roll out a bundled streaming offer via the MBCNOW Android TV box in Saudi Arabia.

- July 2025: CJ ENM formed a wholly owned subsidiary in Saudi Arabia to expand production and distribution footprints.

- July 2025: Manga Productions launched the Saudi Dialects Dubbing Contest to encourage authentic linguistic representation.

- July 2025: MBC’s Shahid platform secured children’s animation from TwelveP Animation, broadening family content.

- July 2025: Warner Bros Discovery and Etisalat introduced a kids’ FAST channel, enriching ad-supported offerings across the UAE.

- March 2025: Warner Bros Discovery invested USD 57 million for a minority stake in OSN Streaming.

- March 2025: Disney deepened its content pact with beIN Media Group, expanding beyond sports rights.

Middle East Media And Entertainment Market Report Scope

In order to entertain and inform audiences, media and entertainment are industries that encompass a range of activities relating to the creation, production, distribution, and consumption of content. It includes a vast range of media such as television, film, music, radio, newspaper, video games, live performances, and digital media. The media industry consists of the production and dissemination of news, information, or entertainment.

The market study emphasizes the trends impacting the media and entertainment industry across the major countries of the Middle Eastern region. The study highlights the key market parameters, underlying growth influencers, and major vendors operating in the industry. The study also tracks the impact of COVID-19 on the region's overall media and entertainment industry.

The Middle East media and entertainment market is segmented by type (digital music (music downloads and music streaming), video games, video-on-demand (SvoD and TVoD, video downloads), e-publishing, advertising (digital advertising, newspaper, magazine, television, radio, and outdoor advertising), and internet access) and country (Saudi Arabia, United Arab Emirates, Qatar, and the Rest of Middle East). Market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Type

| Digital Music | Music Downloads |

| Music Streaming | |

| Video Games | |

| Video-on-Demand | Subscription VoD (SVoD) |

| Transaction VoD (TVoD) | |

| Electronic Sell-Through/Downloads | |

| E-Publishing | |

| Advertising | Digital Advertising |

| Newspaper | |

| Magazine | |

| Television | |

| Radio | |

| Outdoor Advertising | |

| Internet Access Services |

By Platform

| Online/Digital |

| Traditional/Linear |

| Hybrid (Omnichannel) |

By Revenue Model

| Subscription-Based |

| Advertising-Supported |

| Pay-Per-View/Transactional |

| Freemium/In-App Purchase |

By End-User Age Group

| Generation Z (≤24) |

| Millennials (25-40) |

| Generation X (41-56) |

| Baby Boomers (57+) |

By Device

| Smartphones |

| Smart TVs and Connected TV Devices |

| PCs and Laptops |

| Tablets |

| Gaming Consoles |

| VR/AR Headsets |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Rest of Middle East |

| By Type | Digital Music | Music Downloads |

| Music Streaming | ||

| Video Games | ||

| Video-on-Demand | Subscription VoD (SVoD) | |

| Transaction VoD (TVoD) | ||

| Electronic Sell-Through/Downloads | ||

| E-Publishing | ||

| Advertising | Digital Advertising | |

| Newspaper | ||

| Magazine | ||

| Television | ||

| Radio | ||

| Outdoor Advertising | ||

| Internet Access Services | ||

| By Platform | Online/Digital | |

| Traditional/Linear | ||

| Hybrid (Omnichannel) | ||

| By Revenue Model | Subscription-Based | |

| Advertising-Supported | ||

| Pay-Per-View/Transactional | ||

| Freemium/In-App Purchase | ||

| By End-User Age Group | Generation Z (≤24) | |

| Millennials (25-40) | ||

| Generation X (41-56) | ||

| Baby Boomers (57+) | ||

| By Device | Smartphones | |

| Smart TVs and Connected TV Devices | ||

| PCs and Laptops | ||

| Tablets | ||

| Gaming Consoles | ||

| VR/AR Headsets | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

How large is the Middle East media and entertainment market in 2026?

The market is valued at USD 48.43 billion in 2026 and is on course for USD 76.79 billion by 2031.

Which segment is expanding fastest through 2031?

Advertising, propelled by programmatic technology and audience targeting, is forecast to grow at an 11.05% CAGR.

Why is Generation Z critical for future revenue?

Generation Z is set to post the highest 11.19% CAGR, favoring mobile-first, interactive formats that redefine content strategies.

Which country contributes most revenue today?

Saudi Arabia leads with 39.22% share, underpinned by Vision 2030 investments and a large youth population.

What device category is gaining momentum beyond smartphones?

VR/AR headsets are projected to rise at an 11.49% CAGR, bolstered by Dubai’s USD 4 billion metaverse ambition.

How are platforms countering piracy threats?

Operators are tightening DRM, launching affordable ad-supported tiers, and partnering with regulators to block illicit IPTV feeds.

Page last updated on: