Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

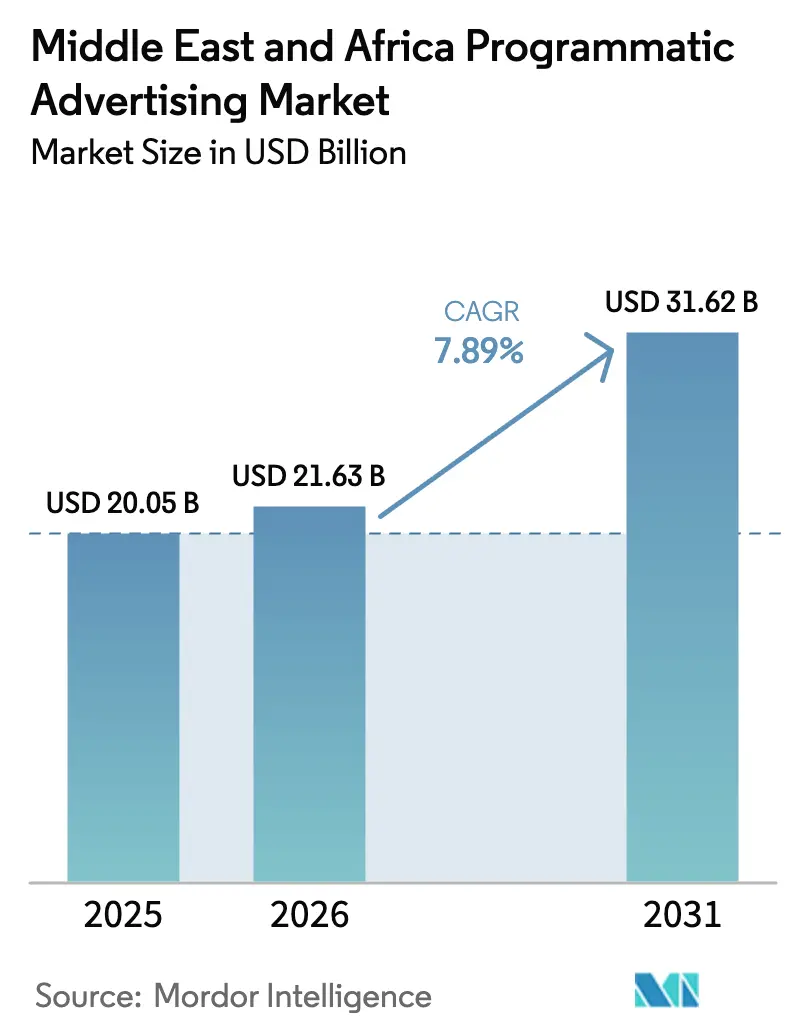

| Base Year Market Size (2025) | USD 20.05 Billion |

| Market Size (2026) | USD 21.63 Billion |

| Market Size (2031) | USD 31.62 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

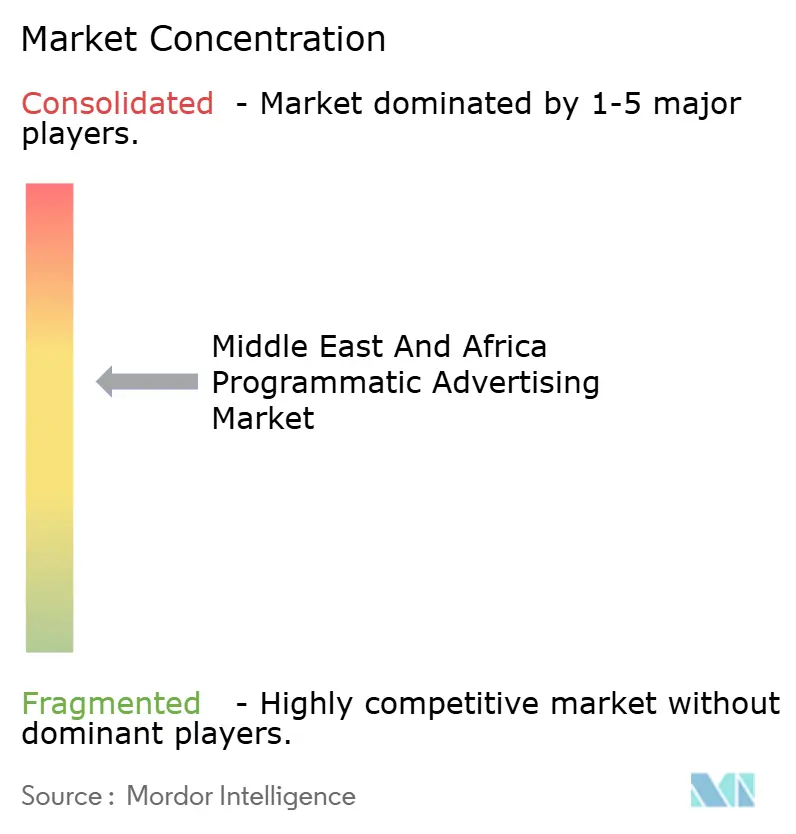

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Programmatic Advertising Market Analysis by Mordor Intelligence

The Middle East and Africa programmatic advertising market size is expected to grow from USD 20.05 billion in 2025 to USD 21.63 billion in 2026 and is forecast to reach USD 31.62 billion by 2031 at 7.89% CAGR over 2026-2031. Robust digital payment growth, sovereign AI programs, and telco-led identity graphs are widening the addressable audience pools while easing compliance with new privacy laws. [1]Jurgita Rudzyte, “MTN Reimagines Mobile Advertising,” Novatiq, novatiq.com Rapid e-commerce expansion has lifted first-party data volumes, enabling advertisers to shift budgets from broad targeting toward deterministic buys that improve return on ad spend. Mobile-first consumer behavior in GCC states, coupled with a decisive pivot to CTV inventory by regional broadcasters, is intensifying demand for cross-screen measurement solutions. At the same time, patchy connectivity outside Tier-1 African cities and uneven brand-safety adoption temper near-term growth prospects.

Key Report Takeaways

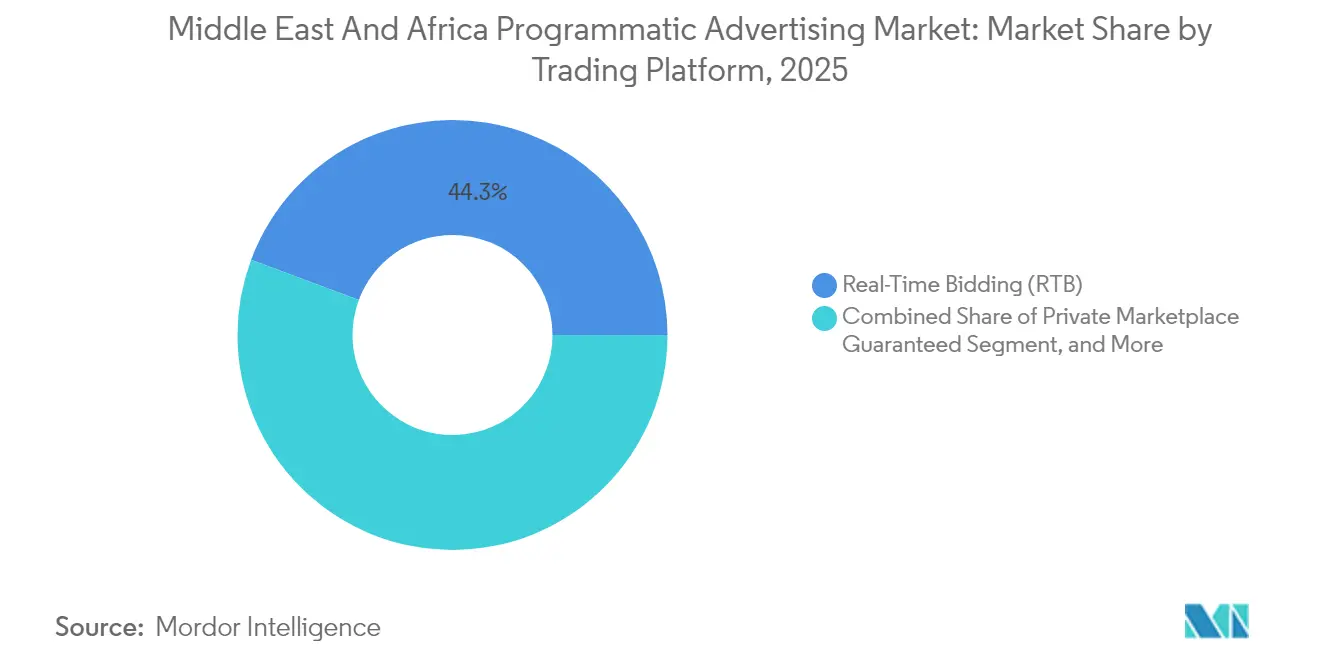

- By trading platform, Real-Time Bidding led with 44.30% of Middle East and Africa programmatic advertising market share in 2025, while Automated Guaranteed is projected to expand at a 10.34% CAGR through 2031.

- By advertising media, Digital Display captured 54.30% of revenue in 2025; Mobile Display is set to advance at a 8.88% CAGR to 2031.

- By ad format, Display Banner accounted for 34.40% of the Middle East and Africa programmatic advertising market size in 2025, whereas CTV/OTT is growing at a 13.98% CAGR.

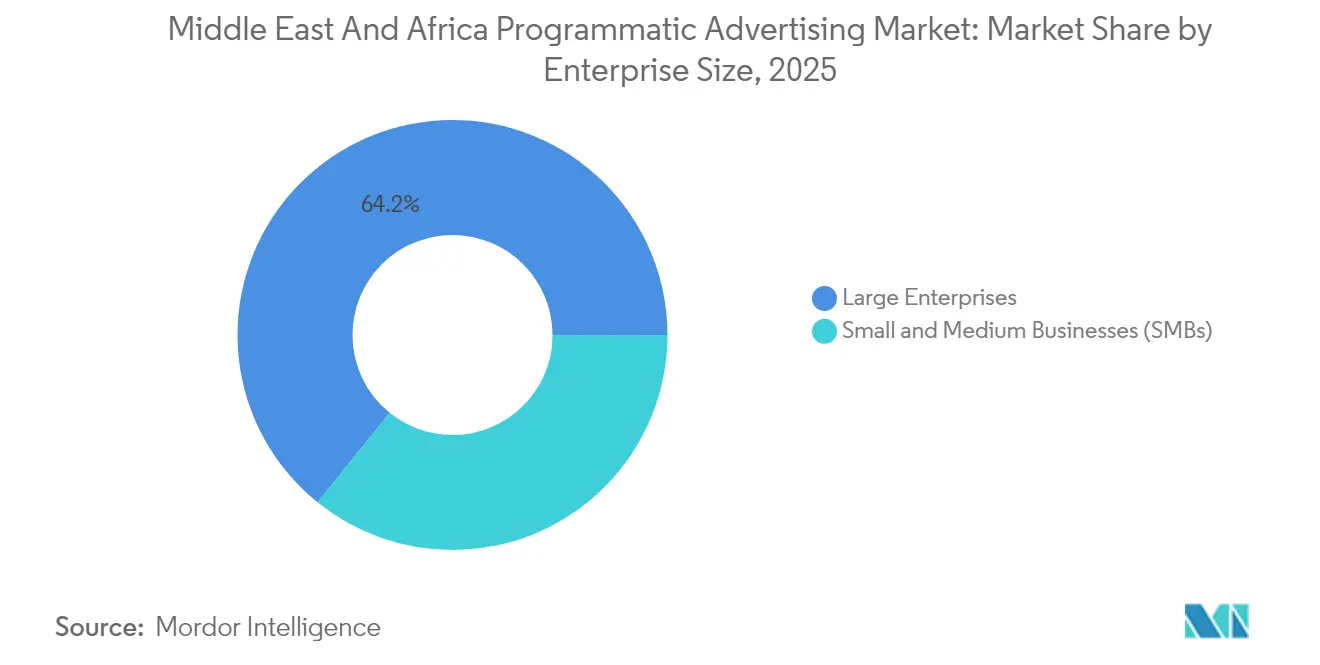

- By enterprise size, large enterprises held 64.20% of spending in 2025; SMBs are pacing growth at 8.96% CAGR.

- By industry vertical, retail and e-commerce led with 19.70% share in 2025, while healthcare and pharma is projected to grow at a 9.84% CAGR.

- By geography, the Middle East commanded 59.40% share in 2025; Africa is the fastest-growing region with a 9.12% CAGR forecast.

- Google, Amazon Ads, and Xaxis collectively accounted for 52% of spend in 2024, underscoring the market’s moderate concentration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Programmatic Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of Mobile-First Consumers in GCC States | +2.1% | UAE, Saudi Arabia, Qatar, Kuwait | Medium term (2-4 years) |

| Growing Adoption of CTV/OTT Advertising Inventory by MENA Broadcasters | +1.8% | Middle East core, spill-over to North Africa | Medium term (2-4 years) |

| Cross-border E-commerce Surge Boosting First-Party Data Use in UAE & KSA | +1.5% | UAE, Saudi Arabia, regional expansion | Short term (≤ 2 years) |

| Telco-led Identity Graph Initiatives in Africa | +1.2% | Sub-Saharan Africa, Nigeria, South Africa | Long term (≥ 4 years) |

| Programmatic DOOH Roll-outs Around FIFA & Expo Events in MEA | +1.0% | Qatar, UAE, Saudi Arabia, Egypt | Short term (≤ 2 years) |

| AI Integration and Automation in Advertising Operations | +0.9% | Global, with early adoption in GCC states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion of Mobile-First Consumers in GCC States

Mobile-first usage now defines consumer engagement, with 70% of UAE shoppers leveraging AI assistants, a 44% jump since 2024. Users spend 3.5 hours daily on social platforms, and 67% of TikTok viewers feel motivated to make in-app purchases. Advertisers gain granular audience signals that refine bid strategies across the Middle East and Africa programmatic advertising market. Retailers are prioritizing AI budgets to shorten the path to purchase and reduce cart abandonment. The UAE e-commerce market is projected to surpass AED 48.8 billion (USD 13.3 billion) by 2028, reinforcing the scale needed for advanced programmatic stacks. [2]Somshankar Bandyopadhyay, “E-commerce Market in the UAE Is Expected to Surpass Dh48.8 Billion by 2028,” Khaleej Times, khaleejtimes.com Mobile-centric DSPs such as InMobi are positioning for a USD 1 billion IPO to capitalize on this uptick.

Growing Adoption of CTV/OTT Advertising Inventory by MENA Broadcasters

Sixty-five percent of UAE residents stream content daily, accelerating migration of brand budgets toward addressable TV formats. Noon’s IPL streams show how shoppable overlays fuse entertainment with impulse purchases. ArabyAds’ alliance with LG Ad Solutions broadens supply while maintaining viewability standards. Dentsu’s curated CTV marketplace posted an 18% lift in attention scores and reduced fraud by 60% compared with open exchanges. Netflix and Yahoo expanded programmatic sales, and Amazon Ads struck a Roku pact reaching 80% of global CTV homes, pulling incremental demand into the Middle East and Africa programmatic advertising market.

Cross-Border E-commerce Surge Boosting First-Party Data Use in UAE and KSA

Digital payment volumes have risen 658% since 2020, fueling richer consented data sets for deterministic targeting. Saudi Arabia has recorded a 180% jump in weekly online shopping, while cash-on-delivery reliance fell to 20%, signaling higher trust in digital payments. New regulations such as UAE’s Federal Decree Law No. 45 of 2021 are forcing marketers to pivot toward secured data flows. Retail media partnerships including GoWit-Mumzworld enable brands to activate 3.5 million shopper IDs via self-service dashboards. Amazon’s South Africa launch validates untapped market headroom, further enlarging the Middle East and Africa programmatic advertising market.

Telco-Led Identity Graph Initiatives in Africa

MTN Ads now delivers deterministic matches across 19 markets without third-party cookies. GroupM and Accenture Song’s certification by Utiq shows global agencies are embracing telco IDs. Vodacom’s partnership with Google on generative AI and Orange’s African-language models highlight how carriers move beyond connectivity toward data enablement. As mobile subscriber penetration heads to 50% by 2030, identity graphs promise scale and privacy alignment for the Middle East and Africa programmatic advertising industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Third-Party Cookie Alternatives on Local Publishers | -1.4% | Regional publishers across MEA | Short term (≤ 2 years) |

| Patchy 4G/5G Coverage Outside Tier-1 African Cities | -1.1% | Sub-Saharan Africa, rural areas | Long term (≥ 4 years) |

| Low Brand-safety Tool Penetration Elevating Fraud Risk | -0.8% | Africa core, emerging Middle East markets | Medium term (2-4 years) |

| Fragmented Data-privacy Regulations Across MEA States | -0.6% | Pan-MEA, with varying compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Third-Party Cookie Alternatives on Local Publishers

Thirty percent of marketers remain ill-prepared for cookie deprecation, leading to over-reliance on contextual targeting. Local publishers often lack the capital to build first-party data tools, creating a two-speed ecosystem where global platforms win disproportionate budgets. Partnerships such as ArabyAds-Lotame aim to close the gap, yet uptake is uneven. Fragmented data-privacy frameworks add compliance overhead that smaller publishers struggle to manage. The imbalance restricts supply diversity within the Middle East and Africa programmatic advertising market and could dampen CPM growth for regional inventory.

Patchy 4G/5G Coverage Outside Tier-1 African Cities

South Africa enjoys 97.5% broadband coverage, yet many African regions face inconsistent speeds that impair high-bandwidth ad formats. Video and rich-media ads struggle to load, forcing advertisers to exclude rural cohorts or settle for lower engagement. Gaming revenues reached USD 1.8 billion in 2024, but further acceleration needs reliable networks. Starlink expansion offers a remedy, though high user fees and local ownership rules limit near-term scale. The constraint particularly hits programmatic DOOH and location-based campaigns that rely on real-time data pings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trading Platform: Shift Toward Quality-Guaranteed Inventory

Real-Time Bidding contributed USD 8.88 billion, equating to 44.30% of the Middle East and Africa programmatic advertising market size in 2025. Advertisers favor RTB for auction efficiency and reach across fragmented publisher pools. Yet fraud concerns have heightened the appeal of Automated Guaranteed deals that lock premium slots at predictable CPMs. Automated Guaranteed is set for 10.34% CAGR, reflecting rising brand-safety expectations and the integration of supply-path optimization protocols. The Trade Desk’s 25% revenue rise and Sincera acquisition demonstrate the pivot toward analytics that surface trustworthy paths and reduce hidden fees. PubMatic reports 55% of impressions now travel through optimized routes, underscoring a marketwide push for transparency.

Private Marketplace Guaranteed offers curated high-viewability contexts for auto, BFSI, and luxury brands. Unreserved Fixed-Rate deals remain relevant for performance marketers chasing cost control. Consolidation reshapes platform choices, as Outbrain’s USD 1 billion Teads takeover broadens native and video bundles. Advertisers therefore weigh scale versus exclusivity in determining optimal trading mixes across the Middle East and Africa programmatic advertising market.

By Advertising Media: Mobile Display Outpacing Desktop

Digital Display retained 54.30% share led by omnichannel campaigns that repurpose creative across screens. Mobile Display is forecast to post 8.88% CAGR, propelled by smartphone adoption and green media innovations that cut emissions by 39% while boosting click-throughs by 10%. Telco data integrations deepen contextual accuracy, particularly in cookie-light environments. As the Middle East and Africa programmatic advertising market matures, brands align mobile budgets with AI-driven commerce journeys, meeting consumers in-app where purchase intent peaks. Desktop display remains vital for B2B and long-form content, yet its share continues to edge down as hybrid work pushes more user time into mobile ecosystems.

Media buyers increasingly demand cross-device frequency capping and unified measurement. Magnite’s 23% CTV revenue rise signals demand for single-platform execution that blends CTV and mobile video. Media cost inflation has also nudged marketers toward supply-path pruning, elevating SSPs that guarantee viewable inventory at sustainable CPMs. The result is a more disciplined allocation of display budgets across the Middle East and Africa programmatic advertising market.

By Ad Format: CTV/OTT Accelerating Attention Economics

Display Banner generated USD 6.9 billion yet faces pressure from banner blindness. CTV/OTT posted the highest growth trajectory at 13.98% CAGR, reflecting full-screen engagement and fraud-mitigation tools inherent to server-side ad insertion. The move toward attention-based currencies gains momentum as contextual ad formats in Arabic achieved 3.5 times standard attention metrics. Online Video and Social Media deliver mid-funnel engagement, while Audio rides the regional podcast boom. DOOH scales through event-based installations like FIFA legacies, leveraging VIOOH’s SSP integration with BackLite Media.

CTV investment accelerates as platforms prioritize audience expansion. Magnite’s support for Netflix’s inaugural programmatic rollout affirms the premium of cinematic environments on brand recall. In turn, buyers channel incremental budgets toward CTV inventory that complements linear TV’s declining reach. The evolution underscores how user attention, not device, now anchors media planning across the Middle East and Africa programmatic advertising market.

By Enterprise Size: SMB On-Ramp to Self-Serve Buying

Large enterprises dominated with 64.20% spend due to proprietary data lakes and cross-market omnichannel orchestration. However, SMB adoption is projected to climb 8.96% CAGR as user-friendly dashboards remove execution hurdles. Intuit SMB MediaLabs and PubMatic partnership exemplify privacy-protective solutions tailored for smaller budgets. Self-service retail media exchanges such as GoWit elevate niche brands by opening direct access to high-intent shoppers in categories like mother-and-child retail. The Middle East and Africa programmatic advertising market size for SMB spend is forecast to surpass USD 3.25 billion by 2031, reflecting democratization.

Meanwhile, large enterprises refine incrementality measurement through AI algorithms that attribute offline lift to online exposure. Sustained investment in data clean rooms ensures compliance with emergent privacy statutes across MEA jurisdictions. Consequently, scale players keep command of premium supply and audience intelligence, even as SMB penetration broadens the purchaser base.

By Industry Vertical: Healthcare and Pharma Emerges as Growth Catalyst

Retail and e-commerce maintained 19.70% share in 2025, buoyed by retail media networks and same-day fulfillment options. Healthcare and pharma is slated for 9.84% CAGR as telemedicine, wearable devices, and AI symptom-checkers generate context-rich data streams. Strict regulatory oversight necessitates privacy-centric solutions, positioning programmatic channels that can honor consent frameworks. BFSI exploits deterministic IDs to enrich cross-sell models, while automotive brands lean on location-based formats to drive dealership visits.

Amazon’s retail media revenue is projected to exceed USD 60 billion in 2025, demonstrating the synergy between commerce data and ad monetization. Criteo’s alliance with MobileFuse deepens Commerce Audience targeting, hinting at future vertical-specific segmentation within the Middle East and Africa programmatic advertising market.

Geography Analysis

The Middle East delivered 59.40% of revenue, supported by visionary policies such as Saudi Vision 2030 that mandate digital diversification. UAE and Saudi Arabia benefit from near-universal smartphone adoption and advanced fintech rails. Cloud alliances including the USD 1 billion-plus AWS-e& agreement enhance real-time bidding throughput and low-latency ad serving across the Middle East and Africa programmatic advertising market. Qatar leverages World Cup infrastructure to expand DOOH networks, while Israel’s start-up scene injects AI algorithms into bidding engines. Meta’s Arabic language AI roll-out strengthens cultural resonance of creative assets.

Africa shows the fastest growth at 9.12% CAGR. South Africa anchors development with 124 million mobile connections and strong banking rails. Nigeria’s USD 300 million gaming revenue signals monetizable digital leisure segments. Kenya’s mobile-money innovation expands addressable payment cohorts, while Egypt’s youth bulge accelerates social media adoption. MTN Ads and Orange AI language projects equip marketers with localized identifiers. Airtel-SpaceX Starlink collaboration aims to bridge rural coverage gaps, improving inventory quality in lagging regions.

Cross-border trade corridors deepen first-party data troves. Amazon’s launch in South Africa pushes logistics benchmarks that competitors must meet. Ecobank-Google Cloud partnership advances financial inclusion, broadening digital wallet usage that supports conversion tracking. The geographic mix reveals a two-pronged opportunity: the Middle East focuses on optimization, while Africa concentrates on infrastructure build-out that will power the next wave of growth in the Middle East and Africa programmatic advertising market.

Competitive Landscape

Global ad tech leaders maintain scale advantages, yet regional specialists inject competitive tension. Google holds 31% share through YouTube reach and integrated DV360 stack. Amazon Ads follows at 12% by linking retail insights with DSP bidding. Xaxis captures 9% via agency embedded trading desks that negotiate curated supply. InMobi owns 7% through mobile-first positioning and telco alliances. The Middle East and Africa programmatic advertising market therefore exhibits moderate concentration, encouraging innovation around identity, measurement, and creative formats.

Strategic acquisitions shape value-chain integration. Outbrain’s Teads purchase creates a scaled open-internet video platform, while T-Mobile’s Vistar Media deal positions the carrier to own DOOH supply. Publicis’ Lotame buy seeks end-to-end data management, signaling that agency groups want proprietary identity scaffolding. Chinese cloud vendors like Huawei and Alibaba undercut AWS pricing, edging into the ad-tech hosting layer. As privacy mandates tighten, players able to deliver authenticated audiences without compromising compliance will strengthen their foothold.

Emerging disruptors include telco advertising arms such as MTN Ads, which leverages deterministic IDs, and retail media platforms like GoWit that monetize shopper intent at the point of sale. Technology differentiation is the decisive advantage. Platforms investing in generative AI for creative iteration and in clean rooms for safe data collaboration will out-maneuver legacy stacks. Consequently, the Middle East and Africa programmatic advertising industry stands at an inflection point where ownership of first-party signals and algorithmic efficiency set the competitive bar.

Middle East And Africa Programmatic Advertising Industry Leaders

Tonic International

Mars Media Group

Executive Digital

Boopin

Xaxis (GroupM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ecobank Group and Google Cloud partnered to modernize digital banking infrastructure across 35 African markets.

- June 2025: Netflix and Yahoo formed a programmatic sales alliance to widen premium inventory access.

- June 2025: Amazon Ads and Roku struck a global pact covering 80% of connected-TV households.

- May 2025: Airtel Africa agreed with SpaceX to deliver Starlink broadband.

Middle East And Africa Programmatic Advertising Market Report Scope

Programmatic Advertising is the utilization of software to buy digital advertising. This automation makes transactions efficient and more effective, streamlining the process and consolidating your digital advertising efforts in one technology platform.

The Middle East and Africa Programmatic Advertisement Market is segmented By Trading Platform (Real-Time Bidding, Private Marketplace Guaranteed, Automated Guaranteed, and Unreserved Fixed-rate), By Advertising Media (Digital Display and Mobile Display), and By Enterprise size (SMBs and Large Enterprises). The scope of the study tracks the impact of covid-19 on the studied market.

By Trading Platform

| Real-Time Bidding (RTB) |

| Private Marketplace Guaranteed |

| Automated Guaranteed |

| Unreserved Fixed-rate |

By Advertising Media

| Digital Display |

| Mobile Display |

By Ad Format

| Display Banner |

| Online Video |

| Social Media |

| CTV / OTT |

| Audio (Streaming and Podcast) |

| Digital-Out-of-Home (DOOH) |

| Others |

By Enterprise Size

| Small and Medium Businesses (SMBs) |

| Large Enterprises |

By Industry Vertical

| Retail and E-commerce |

| BFSI |

| Automotive |

| Media and Entertainment |

| Healthcare and Pharma |

| Travel and Hospitality |

| Telecom and IT |

| Others |

| By Trading Platform | Real-Time Bidding (RTB) |

| Private Marketplace Guaranteed | |

| Automated Guaranteed | |

| Unreserved Fixed-rate | |

| By Advertising Media | Digital Display |

| Mobile Display | |

| By Ad Format | Display Banner |

| Online Video | |

| Social Media | |

| CTV / OTT | |

| Audio (Streaming and Podcast) | |

| Digital-Out-of-Home (DOOH) | |

| Others | |

| By Enterprise Size | Small and Medium Businesses (SMBs) |

| Large Enterprises | |

| By Industry Vertical | Retail and E-commerce |

| BFSI | |

| Automotive | |

| Media and Entertainment | |

| Healthcare and Pharma | |

| Travel and Hospitality | |

| Telecom and IT | |

| Others |

Key Questions Answered in the Report

What is the current value of the Middle East and Africa programmatic advertising market?

The market stands at USD 21.63 billion in 2026 and is forecast to reach USD 31.62 billion by 2031 at a 7.89% CAGR.

Which trading platform segment is expanding the fastest?

Automated Guaranteed is projected to grow at 10.34% CAGR between 2026 and 2031, reflecting higher demand for premium, fraud-controlled inventory.

How large is the CTV/OTT opportunity in the region?

CTV/OTT advertising is the fastest-growing ad format with a 13.98% CAGR, benefiting from 65% daily streaming penetration in the UAE.

Why are telcos important to identity resolution in Africa?

Operators like MTN provide deterministic IDs across 19 markets, giving advertisers cookieless targeting paths in low-publisher-data environments.

What restrains growth outside major African cities?

Patchy 4G/5G coverage limits high-bandwidth formats, reducing campaign reach in rural areas and slowing adoption of advanced programmatic tools.

How concentrated is the competitive landscape?

The top five players hold about 60% share, indicating moderate concentration that still leaves room for regional specialists and new entrants to scale.

Page last updated on: