Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

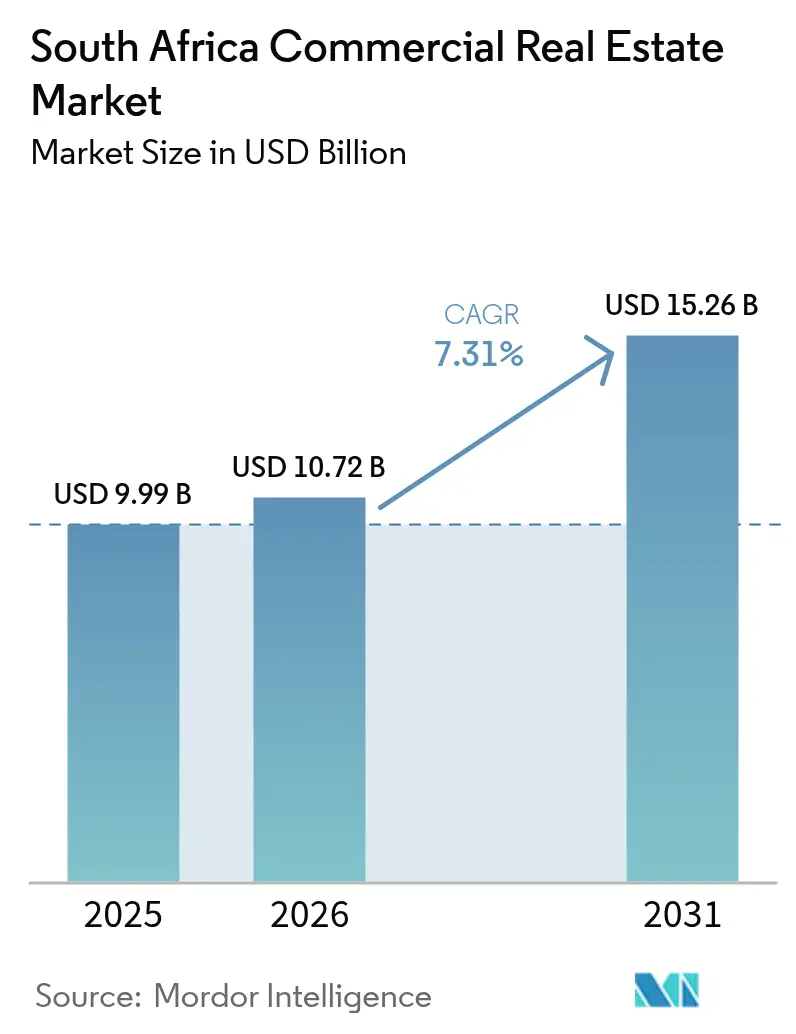

| Base Year Market Size (2025) | USD 9.99 Billion |

| Market Size (2026) | USD 10.72 Billion |

| Market Size (2031) | USD 15.26 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

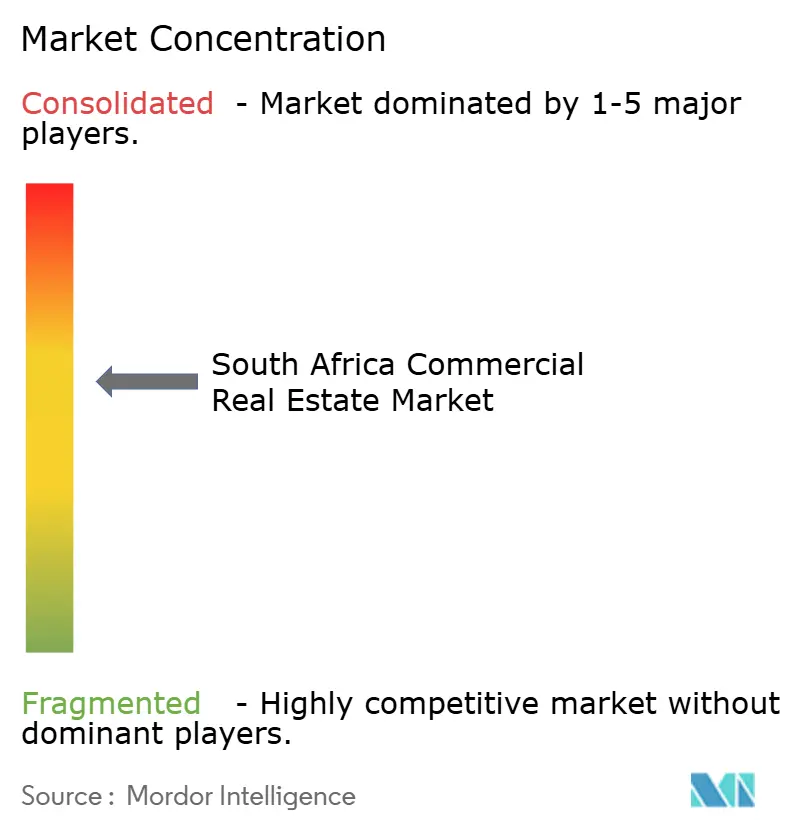

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Commercial Real Estate Market Analysis by Mordor Intelligence

South Africa Commercial Real Estate Market size in 2026 is estimated at USD 10.72 billion, growing from 2025 value of USD 9.99 billion with 2031 projections showing USD 15.26 billion, growing at 7.31% CAGR over 2026-2031. Developers are pivoting toward hybrid facilities that combine warehousing with server capacity as e-commerce and cloud computing converge, while flexible-office providers capture space vacated by traditional tenants adapting to hybrid work. Energy-efficiency mandates and carbon-pricing rules are pushing landlords to retrofit assets, which improves tenant retention and translates into lower operating expenditure amid persistent power-supply instability. As a result, capital flows continue to target certified green assets, even as elevated interest rates keep overall transaction volumes below pre-2020 peaks.

Key Report Takeaways

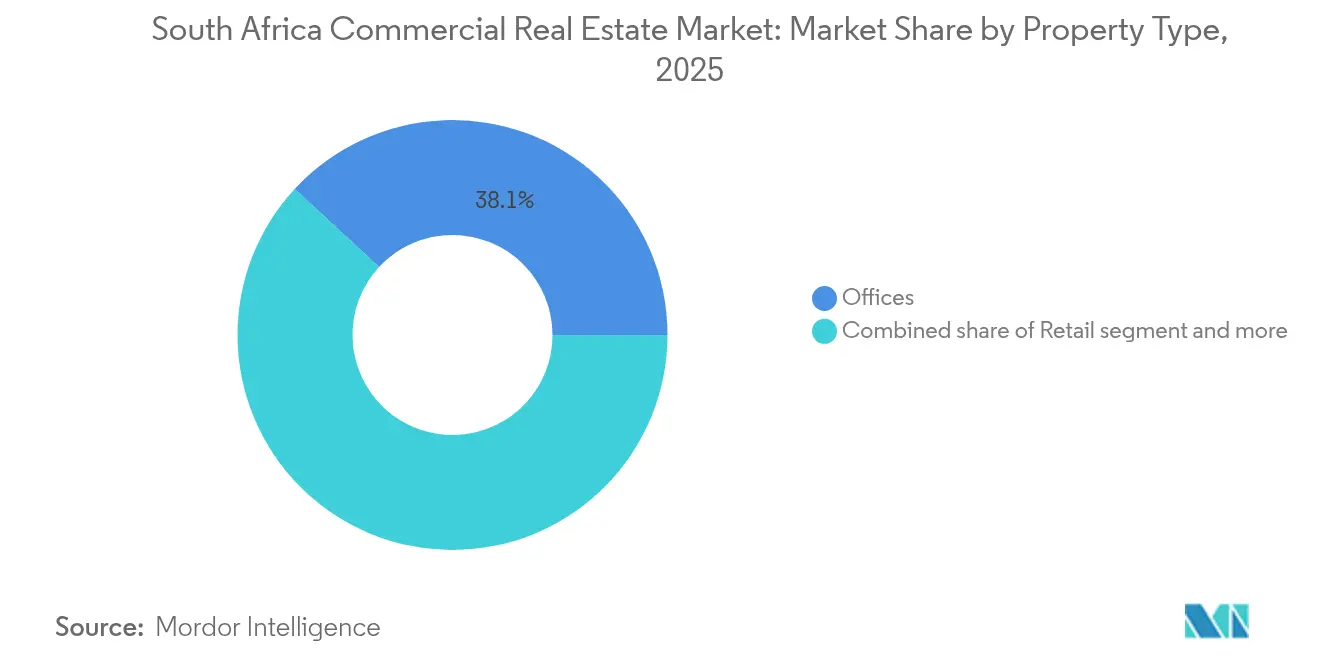

- By property type, the office segment led with 38.12% revenue share in 2025; logistics is forecast to expand at a 9.47% CAGR through 2031.

- By business model, the rental segment held 72.86% of the South Africa commercial real estate market share in 2025, while the sales segment records the highest projected CAGR at 8.37% through 2031.

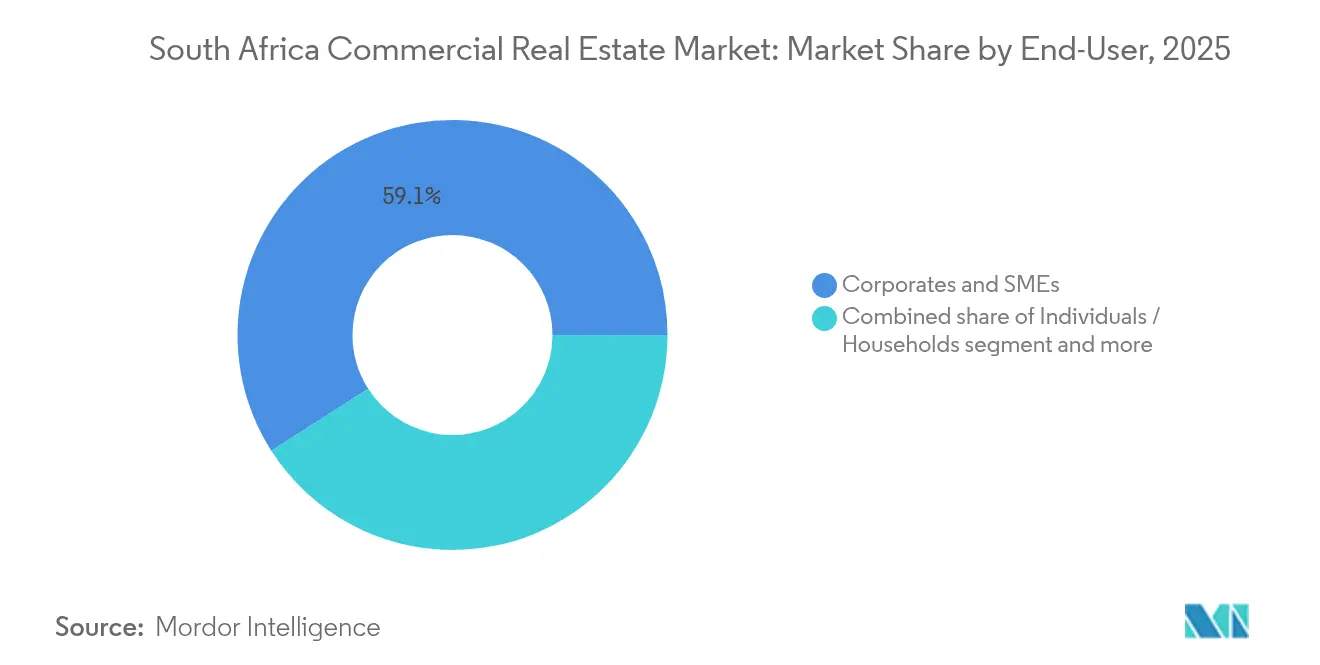

- By end-user, corporates and SMEs accounted for 59.05% of demand in 2025, and individual households are advancing at a 9.05% CAGR to 2031.

- By geography, Johannesburg commanded 35.32% of 2025 revenue, whereas the Rest of South Africa segment is set to grow at a 8.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization & Population Growth | +1.8% | National (Gauteng, Western Cape, KwaZulu-Natal) | Long term (≥ 4 years) |

| Growing FDI in Infrastructure | +1.5% | Johannesburg, Cape Town | Medium term (2–4 years) |

| Rising Demand from Data-Centers & Last-Mile Logistics | +1.4% | Johannesburg, Cape Town, secondary cities | Medium term (2–4 years) |

| Expansion of Shared Workspaces & Hybrid Offices | +1.2% | Major urban centers | Short term (≤ 2 years) |

| Green-Building Incentives & Energy-Efficiency Mandates | +0.9% | National | Medium term (2–4 years) |

| REIT Tax Reforms Stimulating Investment | +0.8% | JSE-listed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization & Population Growth

Rapid migration toward Gauteng, the Western Cape, and KwaZulu-Natal keeps occupational demand resilient across offices, light-industrial parks, and convenience retail. Government spatial-planning programs, accompanied by USD 25.89 million earmarked for land acquisition, aim to unlock mixed-use nodes that knit commercial space with affordable housing. These initiatives improve urban land governance and shorten project lead times, which encourages developers to start schemes outside traditional cores. Over the long term, consistent population inflows underpin the South Africa commercial real estate market by broadening the tenant base and lowering absorption risk for new projects.

Growing FDI in Infrastructure

A pipeline of USD 24.72 billion in new infrastructure projects, including USD 5.28 billion in private commitments, is accelerating construction of ports, rail links, and digital corridors. A streamlined approval regime under Infrastructure South Africa has already moved 34 strategic projects, worth USD 15.61 billion, into execution, which directly lifts demand for site offices, warehousing, and accommodation. High-profile technology deployments—such as Google’s USD 1.39 billion cloud region and Equinix’s data-center build—signal confidence in the South Africa commercial real estate market, especially for grade-A campuses that can guarantee redundant power. Medium-term spillovers include stronger rental growth in adjacent micro-markets as multinational suppliers co-locate to leverage clustering benefits[1]Kgosientsho Ramokgopa, “Infrastructure South Africa Strategic Project Pipeline 2025,” Department of Public Works and Infrastructure, dpwi.gov.za.

Rising Demand from Data-Centers & Last-Mile Logistics

Africa’s internet economy, forecast at USD 180 billion in 2025, is catalyzing a dual requirement for warehousing near consumption hubs and edge facilities that handle low-latency workloads. Johannesburg alone will add more than 40,000 digital jobs by 2030 on the back of Google’s investment, spurring the construction of cross-docked sheds with expandable power envelopes. Logistics assets in the South Africa commercial real estate market now trade at cap-rate premiums to offices because occupiers sign longer leases to secure tailored fit-outs. Medium-term growth will also emerge in secondary cities as e-commerce platforms chase faster delivery windows, widening the geographic footprint of institutional-grade stock[2]Google LLC, “Form 8-K: Launch of Johannesburg Cloud Region,” U.S. Securities and Exchange Commission, sec.gov.

Expansion of Shared Workspaces & Hybrid Offices

The Remote Work Visitor Visa, open to foreigners earning at least USD 36,165 annually, is drawing digital nomads to Cape Town and Johannesburg. Occupiers are consequently renegotiating lease terms in favor of shorter cycles and higher service intensity, which propels coworking penetration beyond pre-pandemic highs. One-bed apartment rents in Cape Town climbed 28% in 2024 as flexible-office operators absorbed converted residential stock to satisfy hot-desk demand. This structural shift trims long-term space requirements for corporates yet increases take-up of plug-and-play suites that command premium yields. Short-term upside, therefore, persists for landlords that retrofit secondary buildings into adaptable, tech-enabled environments[3]Aaron Motsoaledi, “Remote Work Visa Regulations (Gazette No. 49676),” Department of Home Affairs, dha.gov.za.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-Supply Instability & Infrastructure Deficits | -2.1% | National | Medium term (2–4 years) |

| Economic Uncertainty & Unemployment | -1.6% | National | Short term (≤ 2 years) |

| Regulatory Complexity & Land-Tenure Issues | -1.2% | National | Medium term (2–4 years) |

| Climate Risk & Insurance-Cost Escalation | -0.8% | Coastal areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Power-Supply Instability & Infrastructure Deficits

Rolling outages translate into unbudgeted fuel outlays. Stage 6 load-shedding lifted diesel spend for a leading REIT to USD 28,417 per day from USD 9,474 at Stage 2. Retail-linked landlords suffer doubly as generator costs coincide with subdued consumer traffic, compressing net-operating income. The government has allocated USD 12.18 billion for energy assets, yet capacity additions will not materially ease the strain before 2027. In the interim, occupiers gravitate toward buildings with solar arrays and storage, prompting brownfield retrofits but also raising entry barriers for fringe players lacking access to low-cost funding.

Economic Uncertainty & Unemployment

GDP growth remains below 2%, which tempers new-build demand and delays speculative starts. Construction value-added fell to USD 6.11 billion in 2023 from USD 8.33 billion in 2017 as governance gaps and policy ambiguity extended tender cycles. Although the real-estate sector still posted a 3.5% uptick in 2024, credit costs weigh on small-business expansion that traditionally absorbs secondary office inventory. The coalition government’s uneven reform pace erodes confidence, pushing some landlords to prioritize defensive capex over expansionary projects while they await clearer fiscal signals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Drives Digital Economy Growth

Logistics assets captured 9.47% CAGR through 2031, outstripping the office segment’s entrenched 38.12% share. This acceleration elevates logistics’ contribution within the South Africa commercial real estate market, especially around data-center clusters where dual-use footprints are emerging. Developers are layering high-density racks above conventional warehousing bays, creating blended facilities that serve both packet traffic and parcel flow. Landlords report pre-let ratios above 70% on such schemes because occupiers value integrated security and power resiliency. Conversely, traditional retail faces churn as anchor grocers evaluate smaller formats, reducing expansion pipelines and nudging owners to explore mixed-use repositioning.

Momentum in certified green projects is strongest in offices where corporate ESG targets drive leasing. Over 2 million sq m of certified space enjoys vacancy rates 350 basis points below the national office average, a metric that continues to support re-rating of prime CBD towers. While hospitality and industrial parks benefit from special-economic-zone incentives, their combined slice of the South Africa commercial real estate market remains modest, though capital appreciation prospects rise near new transport corridors.

By Business Model: Rental Dominance Amid Sales Recovery

Rental income accounted for 72.86% of the South Africa commercial real estate market in 2025 as REIT structures favor predictable cash flows. Embedded escalations averaging 6% mitigate inflation exposure, but higher generator expenses compress distributable earnings, prompting issuers to offer scrip options to preserve liquidity. At the same time, the sales model is reviving with 8.37% CAGR, buoyed by foreign buyers hunting yield pick-up against developed-market compression. Direct deals are clustering around Cape Town’s Atlantic seaboard and Johannesburg’s northern nodes, where infrastructure upgrades link projects to the ring-road network.

The South Africa commercial real estate market size for strata-titled offices and small-bulk warehouses is expanding as owner-occupiers hedge against rent volatility and as remote-work visa holders diversify portfolios. Discounted loan-to-value ratios and flexible mortgage products launched by local banks further lower entry thresholds, pointing toward sustained momentum in secondary sales into 2026.

By End-User: Corporate Demand Meets Individual Investment Growth

Corporates and SMEs held 59.05% of space in 2025, underscoring Johannesburg’s role as the continent’s decision-making center. Yet adoption of hybrid rosters has already trimmed average space per employee by 18%, compelling landlords to invest in amenity-rich environments that preserve footfall. The South Africa commercial real estate market share attributed to individuals is rising fastest, supported by fractional ownership platforms and investment apps that convert large properties into tradeable digital units. Visa-enabled remote workers add long-stay demand for turn-key apartments bundled with coworking access, which further diversifies revenue streams for mixed-use developers.

Government bodies and parastatals within the “Others” bracket sign longer leases that underpin debt service for public-private-partnership assets, though budget volatility can elongate payment cycles. Going forward, new infrastructure concessions are likely to incorporate inflation-linked clauses that protect rental cash flows and stabilize valuations.

Geography Analysis

Johannesburg dominates the South Africa commercial real estate market with a 35.32% revenue share, anchored by Africa’s deepest capital pool and a maturing technology ecosystem. Google’s USD 1.39 billion cloud launch is projected to inject USD 2.1 billion into provincial GDP and create over 40,000 jobs, reinforcing office and logistics take-up along the N1 corridor. The approved extension of the Gautrain will funnel USD 2.56 billion into construction, historically lifting property values near stations by an extra 3% annually. Nevertheless, load-shedding remains acute, forcing developers to integrate on-site solar and battery systems that add 12-15% to project capex.

Cape Town and Durban offer complementary profiles. Cape Town appeals to remote professionals, evident in one-bedroom rent jumps and rising absorption of small-format offices configured for shared use. Durban leverages port upgrades and industrial land banks to attract light-manufacturing tenants, though KwaZulu-Natal’s slower economic recovery moderates speculative building. Port Elizabeth (Gqeberha) anchors automotive export flows and is slated for logistics-park expansion once berth-deepening is finalized.

The Rest of South Africa segment is on track for a 8.90% CAGR through 2031. Government plans to channel USD 20.83 billion into state-enterprise road, bridge, and port projects are opening corridors in Mpumalanga, Limpopo, and the Northern Cape. Spatial-planning reforms streamline land-release processes, enabling private capital to package commercial nodes around service hubs. Institutional investors are already pre-committing to anchor retail and medical facilities in these greenfield districts, betting on first-mover advantages as household formation accelerates.

Competitive Landscape

The market remains moderately fragmented, with the five largest landlords controlling roughly 45% of institutionally traded stock. Load-shedding has become the principal cost differentiator: Attacq’s diesel spend escalated to USD 28,417 per day at Stage 6, prompting a pivot toward solar plus storage retrofits that cut annual carbon footprints and attract sustainability-linked debt. Redefine Properties and Oasis Crescent both opted for scrip dividends to preserve cash, while Vukile pursued offshore diversification via its USD 79 million Portuguese purchase.

Digital infrastructure represents a strategic frontier. REITs partnering with hyperscalers to develop edge campuses lock in long-dated triple-net leases that enhance income visibility. Simultaneously, green-building accreditation is an increasingly critical tenant requirement, with more than 2 million sq m already certified nationwide. Regulatory uncertainty around the Expropriation Act 2024 and looming executive-liability clauses in carbon legislation elevate compliance costs, skewing competitive advantages toward firms with in-house legal and ESG expertise.

White-space opportunities include last-mile hubs in secondary metros, mixed-use precincts tied to rail expansions, and solar-ready rooftop portfolios that can feed excess generation into municipal grids. Investors able to structure deals around these themes stand to outperform as the South Africa commercial real estate market pivots toward resilience and sustainability.

South Africa Commercial Real Estate Industry Leaders

Growthpoint Properties

Redefine Properties

Fortress REIT

Attacq Ltd

Liberty Two Degrees

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: President Cyril Ramaphosa confirmed an infrastructure plan worth USD 52.22 billion, including USD 20.83 billion for state-owned-enterprise transport upgrades, setting the stage for a new wave of commercial schemes.

- April 2025: Vukile Property Fund purchased Forum Madeira shopping center in Portugal for USD 79 million, signaling continued outbound diversification.

- March 2025: Google inaugurated a USD 1.39 billion cloud region in Johannesburg, projected to add USD 2.1 billion to national GDP by 2030.

- March 2025: Gautrain extension to Soweto and Cosmo City received final approval, unlocking USD 2.56 billion in construction value and catalyzing transit-oriented development.

South Africa Commercial Real Estate Market Report Scope

Commercial real estate (CRE) is only used for business-related activities or to offer a workspace, as opposed to being utilized as a residence, which would fall under the residential real estate market. Most frequently, renters lease commercial real estate to conduct businesses that generate cash. A complete background analysis of the South African commercial real estate market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The South African commercial real estate market is segmented by type (office, retail, industrial and logistics, and hospitality) and key cities (Johannesburg, Cape Town, Durban, Port Elizabeth, and Other Key Cities). The report offers market sizes and forecasts for all the above segments in value (USD).

By Property Type

| Offices |

| Retail |

| Logistics |

| Others (industrial real estate, hospitality real estate, etc.) |

By Business Model

| Sales |

| Rental |

By End-user

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Geography

| Johannesburg |

| Cape Town |

| Durban |

| Port Elizabeth / Gqeberha |

| Rest of South Africa |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (industrial real estate, hospitality real estate, etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Geography | Johannesburg |

| Cape Town | |

| Durban | |

| Port Elizabeth / Gqeberha | |

| Rest of South Africa |

Key Questions Answered in the Report

What is the current value of the South Africa commercial real estate market?

The South Africa commercial real estate market size is USD 10.72 billion in 2026.

How fast will South African logistics property grow?

Logistics assets are projected to record a 9.47% CAGR through 2031 as e-commerce and data-center demand converge.

Which city holds the largest share of commercial real estate in South Africa?

Johannesburg leads with 35.32% market share thanks to its status as Africa’s financial and technology hub.

How are power outages affecting commercial landlords?

Stage 6 load-shedding can raise diesel costs to USD 28,417 per day, pressuring net operating income and encouraging solar retrofits.

Page last updated on: