India Mid-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

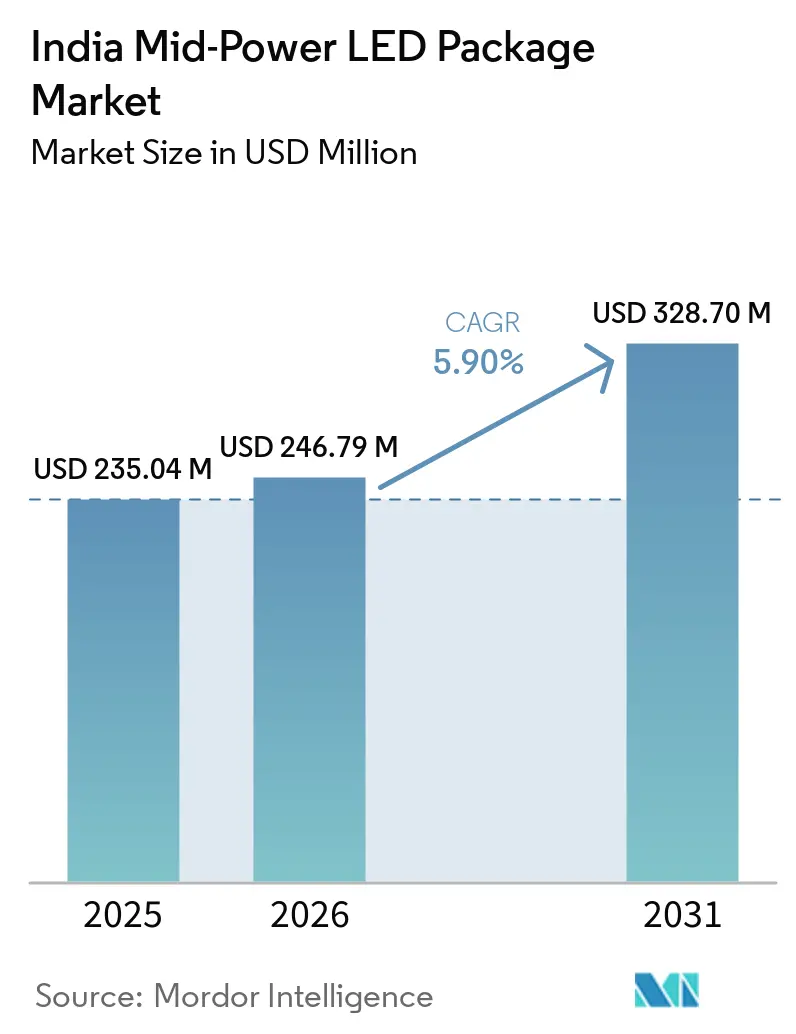

| Base Year Market Size (2025) | USD 235.04 Million |

| Market Size (2026) | USD 246.79 Million |

| Market Size (2031) | USD 328.70 Million |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Mid-Power LED Package Market Analysis by Mordor Intelligence

The India mid-power LED package market size is expected to increase from USD 235.04 million in 2025 to USD 246.79 million in 2026 and reach USD 328.70 million by 2031, growing at a CAGR of 5.9% over 2026-2031. Demand is anchored by municipal street-lighting upgrades that now stipulate ≥110 lumens-per-watt efficacy, the government’s Production Linked Incentive (PLI) scheme that is steering INR 10,478 crore (USD 1.26 billion) into localized LED component lines, and the rapid build-out of contract electronics hubs in Noida, Bengaluru, and Chennai. Tighter Bureau of Indian Standards (BIS) specifications published between late 2025 and early 2026 are accelerating the retirement of non-compliant lamp inventories, while indigenous smartphone and display assemblers shifting to in-house backlighting arrays are shortening supply chains. Price volatility in rare-earth phosphors and an inverted GST structure that taxes LED components at 18% and finished luminaires at 12% temper margin expansion, yet overall capital commitments suggest a durable multi-year runway for the India mid-power LED package market. The absence of a single dominant vendor further widens opportunities for contract manufacturers that can combine BIS-certified efficacy with aggressive unit economics.

Key Report Takeaways

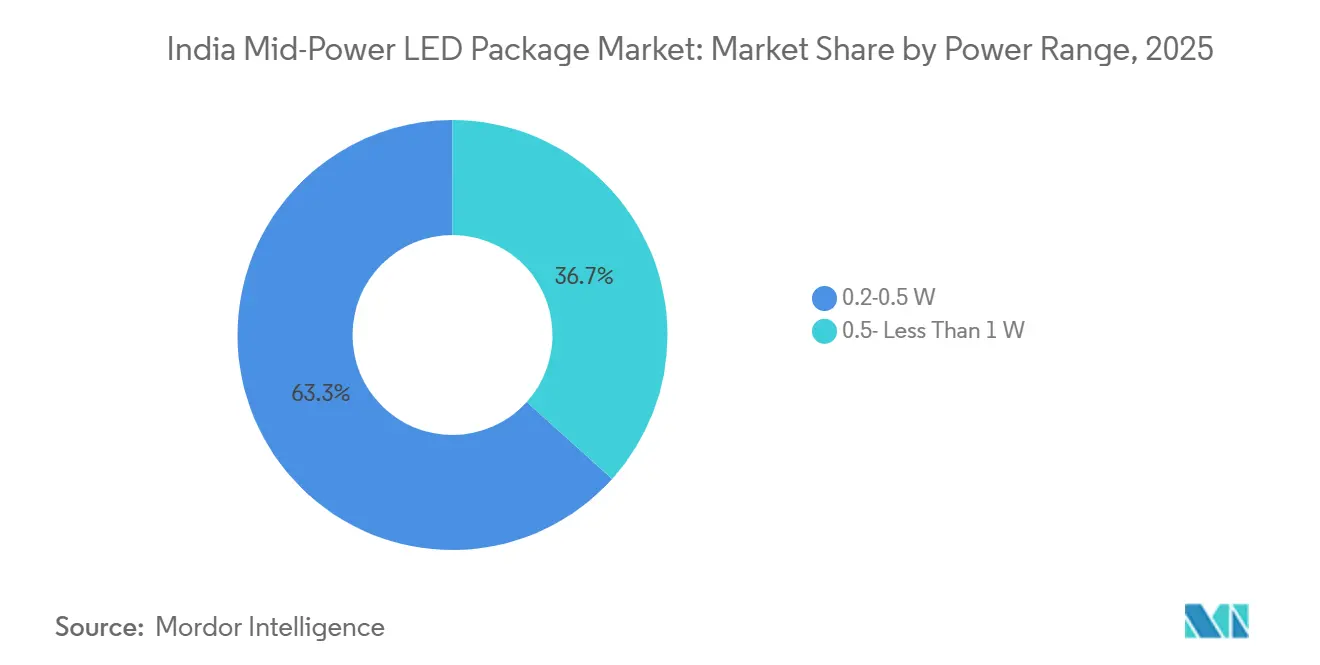

- By power range, the 0.5 W-to Less Than 1 W sub-segment commanded 63.33% of the India mid-power LED package market share in 2025 and is forecast to expand at a 6.78% CAGR through 2031.

- By package architecture, surface-mount devices held 74.28% revenue share in 2025, while chip-scale packages are projected to register the fastest growth at a 6.93% CAGR during 2026-2031.

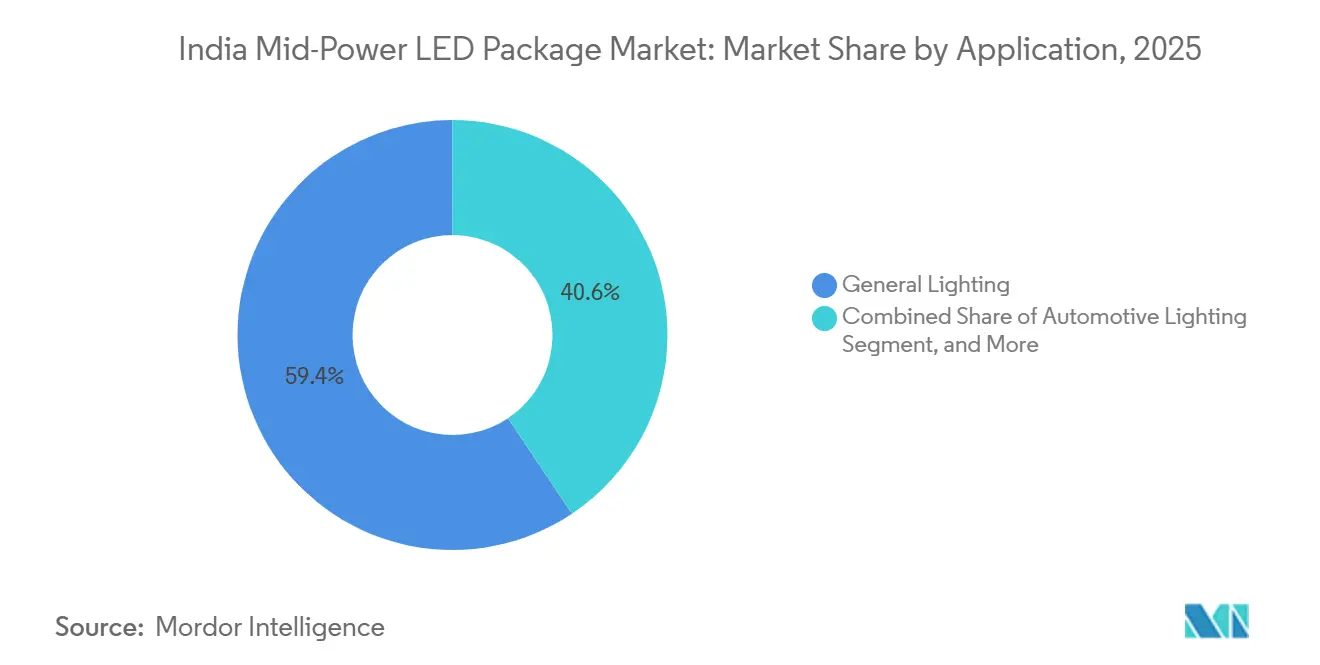

- By application, general lighting led with a 59.38% share of the India mid-power LED package market in 2025, whereas automotive lighting is advancing at a 6.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Mid-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mainstream LED Adoption in Street-Lighting Tenders | +1.8% | National, early uptake in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Rising Luminous-Efficacy Mandates by BIS | +1.2% | National | Short term (≤ 2 years) |

| Rapid Expansion of Indian Contract Electronics Manufacturing | +1.0% | Noida, Bengaluru, Chennai clusters | Medium term (2-4 years) |

| Indigenous Smartphone Assembly Shifting to Mid-Power LEDs | +0.7% | Noida, Tamil Nadu hubs | Medium term (2-4 years) |

| Government’s PLI Scheme for LED Components | +0.6% | National | Long term (≥ 4 years) |

| Micro-Retailers Embracing Smart-Lighting Retrofits | +0.4% | Urban and semi-urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream LED Adoption in Street-Lighting Tenders

Municipal corporations embedded minimum efficacy and color-rendering thresholds into more than 90% of street-lighting tenders issued since 2025, effectively disqualifying high-pressure sodium fixtures and pushing procurement toward 0.5 W-to-1 W mid-power packages that deliver 120-140 lumens per watt. Energy Efficiency Services Limited (EESL) is accelerating replacement cycles through central co-financing. This move guarantees multi-year order visibility. Vendors that showcase BIS compliance and boast surge-protection ratings exceeding 4 kilovolts are consistently landing the largest lots. This trend is prompting local encapsulation lines to expand their operations.

Rising Luminous-Efficacy Mandates By BIS

The BIS suite, IS 10322:2026, IS 16102:2026, and IS 16103:2025, has raised efficacy floors from 100 lumens per watt to 110-120 lumens for the most prevalent wattage classes.[1]Bureau of Indian Standards. "Standards Portal." Accessed April 6, 2026. Major players, equipped with in-house photometric labs, have swiftly rolled out upgraded product lines. In contrast, smaller assemblers grapple with certification delays that can stretch up to 6 months. This mandatory shift renders slower-moving SKUs obsolete, prompting a surge in restocking in India's mid-power LED package market.

Rapid Expansion of Indian Contract Electronics Manufacturing

Dixon Technologies, Samsung, and Tata Electronics collectively announced more than INR 3,500 crore (USD 420 million) in 2025-2026 capex for display and smartphone assembly lines that integrate mid-power LED backlighting arrays.[2]Business Standard Staff, “Dixon to Invest INR 1,100 Cr in Display Modules,” business-standard.com Localization shortens lead times from 10-12 weeks to less than 4 weeks and reduces landed cost volatility tied to freight rates, adding a full percentage point to market growth as domestic sourcing displaces Southeast Asian imports.

Indigenous Smartphone Assembly Shifting to Mid-Power LEDs

The shift toward indigenous smartphone assembly and the use of domestically sourced mid-power LED strips brings clear cost and policy advantages, but it also introduces several constraints. Mid-power LEDs, while economical, typically offer lower brightness efficiency, thermal performance, and long-term stability compared to higher-end alternatives, which can limit display quality, especially in premium devices. Additionally, the domestic supply chain for such components is still maturing, with fewer vendors, potential quality inconsistencies, and limited access to advanced technologies, creating risks as production scales up. Although manufacturers benefit from avoiding the inverted GST on imports, the cost advantage is partly policy-driven and may not fully offset the lack of global-scale efficiencies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatility in Phosphor Supply Prices | -1.3% | Global, acute in India | Short term (≤ 2 years) |

| Low Switching-Cost Toward COB Imports from China | -0.9% | Cost-sensitive general lighting | Medium term (2-4 years) |

| Thermal-Management Issues in High-Ambient Zones | -0.5% | Northern and central India | Long term (≥ 4 years) |

| Persistent GST-Rate Uncertainty on LED Inputs | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility In Phosphor Supply Prices

China’s April 2026 export controls on yttrium compounds drove European yttrium-oxide spot prices from USD 8 per kg to USD 126 per kg within six weeks, compressing operating margins by up to 200 basis points for Indian package makers reliant on imported red and yellow phosphors.[3]China Tungsten Industry News Center, “China’s Yttrium Export Controls,” ctiw.cn Although forward contracts and partial substitution with gadolinium-based blends temper the shock, persistent geopolitical risk subtracts 1.3 percentage points from market expansion.

Low Switching-Cost Toward COB Imports from China

Chip-on-board (COB) modules delivering equivalent lumen output at 10-15% lower landed cost remain a credible substitute in high-bay and downlight luminaires. Minimal retooling is required, and the GST inversion further incentivizes importing semi-finished COB assemblies rather than discrete mid-power LEDs. The drag on discrete package demand is estimated at 0.9 percentage points.[4]Directorate General of Foreign Trade, “Import Tariff Circular No. 48/2025,” dgft.gov.in

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: 0.5 W-To- Less Than 1 W Packages Consolidate Leadership

The 0.5 W-to-Less Than 1 W band captured 63.33% of India's mid-power LED package market share in 2025. Government street-lighting programs and automotive adaptive headlamps specify this wattage to balance efficacy with thermal headroom, and demand is reinforced by Lumax Industries’ INR 1,759 crore (USD 211 million) LED-heavy order book. Outdoor ambient temperatures exceeding 40 °C in much of India elevate junction-temperature risk, making the lower current density of 0.5 W to 1 W dice indispensable for 50,000-hour lumen maintenance targets.

Segment growth also benefits from PLI-funded localization of phosphor coating and wire-bonding lines, which trim bill-of-materials costs by nearly 8% versus imported equivalents, sustaining a 6.78% CAGR through 2031. The Indian mid-power LED package market size for this power range is projected to move in lockstep with the ramp-up of municipal tenders that collectively cover more than 3 million luminaire points over the forecast horizon.

By Package Architecture: SMD Dominance Meets CSP Momentum

Surface-mount devices accounted for 74.28% of India's mid-power LED package market revenue in 2025, enabled by entrenched 2835 and 3030 footprints that integrate seamlessly with legacy pick-and-place lines. Crompton Greaves’ Q3 FY26 lighting revenue uptick underscores the mass-market pull for these standardized packages. However, chip-scale packages (CSPs) are forecast to outpace all other form factors with a 6.93% CAGR to 2031.

CSPs eliminate wire bonds and encapsulant overmold, reducing package height to below 0.5 mm and delivering thermal resistances under 4 K/W. Automotive matrix headlamps and mini-LED displays require such profiles, and Nichia’s 2025 cross-license deal with ams OSRAM relaxes IP bottlenecks, enabling faster vendor qualification. The India mid-power LED package market for CSPs is also poised to benefit from Dixon Technologies’ June 2026 display-module plant, which will consume domestically sourced wafer-level phosphor-coated dies.

By Application: Automotive Lighting Gains Speed on Regulatory Tailwinds

General illumination held 59.38% of 2025 revenue, buoyed by residential bulb swaps and public-sector street upgrades. Price elasticity remains high, but retrofits bundled into energy-savings contracts mitigate acquisition cost hurdles. Meanwhile, automotive lighting is projected to be the fastest-growing application at a 6.86% CAGR through 2031.

Daytime running lamp mandates and premium segment adoption of adaptive beam lighting underscore the need for mid-power matrix arrays that deliver high luminance without the thermal penalties of high-power dice. Lumax Industries already sources more than 60% of its LED inputs from domestic package lines, a pivot that corrals procurement risk and shrinks design-to-SOP lead times. The India mid-power LED package market for automotive applications will also capture incremental demand as two-wheeler OEMs migrate from halogen to LED headlamps.

Geography Analysis

Noida’s electronics corridor drives domestic consumption as Dixon Technologies, Samsung, and allied EMS vendors ramp SMT lines. Bengaluru and Chennai comprise the automotive center of gravity, with Lumax Industries and Stanley Electric joint ventures specifying locally assembled CSP arrays for adaptive headlamps. These southern hubs hold disproportionately large design-in pipelines for 2027 vehicle programs.

Western states, such as Maharashtra and Gujarat, benefit from stronger fiscal headroom and early adoption of performance-based street-lighting contracts, resulting in municipal tender sizes that average larger luminaires per lot than the national mean. The India mid-power LED package market in these states is growing steadily as smart-pole pilots kick off in Pune, Nagpur, and Ahmedabad. Northern and central regions contend with high summer temperatures that accelerate lumen depreciation, prompting select municipalities to specify metal-core PCBs, which in turn favor higher-wattage dice over lower-wattage alternatives.

Export volumes remain modest, though PLI incentives are slated to halve capex payback periods for new phosphor coating and bin-sorting lines, positioning Indian vendors for selective penetration of South Asian and African retrofit programs. Government targets under the Electronics Components and Semiconductors Manufacturing Scheme propose domestic phosphor production, a milestone that could further diversify geographic revenue streams.

Competitive Landscape

The mid-power LED package market in India is moderately fragmented. The top five suppliers command a significant portion of the market, while over 55 assemblers vie for the remainder. Global companies like Nichia, Seoul Semiconductor, Lumileds, and ams OSRAM capitalize on their brand reputation and consistent high-bin quality to secure positions in the automotive and premium consumer segments. Meanwhile, domestic players such as Havells, Surya Roshni, Bajaj Electricals, Crompton Greaves, and Dixon Technologies adeptly align their pricing with specifications in government tenders and urgent EMS demands.

Havells has set aside funds for capacity enhancements through 2027. This includes wafer-level phosphor dispensing technology, enabling them to adjust output in response to commodity price fluctuations. Surya Roshni, with a zero-debt status and cash reserves, is poised to seize opportunistic supply deals during phosphor price surges. The IP landscape is evolving with cross-licensing agreements. For instance, the 2025 pact between Nichia and ams OSRAM mitigates litigation risks, while Everlight Electronics' 2026 lawsuit against Seoul Semiconductor over flip-chip patents underscores the ongoing enforcement dynamics.

Contract manufacturers are increasingly wielding power in the market. For example, Dixon Technologies' joint venture with Longcheer has secured substantial demand for smartphone backlighting. This scale empowers Dixon to negotiate die pricing on par with global standards. Standalone package assemblers face margin pressures due to accumulated input tax credit from GST inversion. In contrast, vertically integrated firms leverage surplus credits by directing them into downstream luminaires, a strategy that smaller players find challenging to emulate.

India Mid-Power LED Package Industry Leaders

-

Nichia Corporation

-

Seoul Semiconductor Co. Ltd.

-

Lumileds Holding B.V.

-

Osram Opto Semiconductors GmbH

-

Everlight Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Everlight Electronics sued Seoul Semiconductor for infringement of flip-chip patent US 7,554,126, escalating patent enforcement dynamics in advanced mid-power architectures.

- March 2026: Dixon Technologies gained approval under the Electronics Components and Semiconductors Manufacturing Scheme for an INR 1,100 crore (USD 132 million) display-module facility in Noida, with trial runs slated for Jun 2026.

- March 2026: Dixon Technologies and Longcheer Technology formed a 74:26 joint venture for smartphone and AI-PC assembly, capitalized at INR 10 crore (USD 1.2 million).

- January 2026: Crompton Greaves introduced 70 W and 80 W Dynaray LED lamps delivering 120 lumens-per-watt efficacy and BIS 2026 compliance.

India Mid-Power LED Package Market Report Scope

The India Mid-Power LED Package Market Report is Segmented by Power Range (0.2-0.5 W and 0.5- Less Than 1 W), Package Architecture (SMD including 2835, 3014, 3030, Others, and CSP), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

| 0.2-0.5 W |

| 0.5- Less Than 1 W |

| SMD (Surface Mount Device) | 2835 |

| 3014 | |

| 3030 | |

| Others (3528, 3020, 5050, etc.) | |

| CSP (Chip Scale Package) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| By Power Range | 0.2-0.5 W | |

| 0.5- Less Than 1 W | ||

| By Package Architecture | SMD (Surface Mount Device) | 2835 |

| 3014 | ||

| 3030 | ||

| Others (3528, 3020, 5050, etc.) | ||

| CSP (Chip Scale Package) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

Key Questions Answered in the Report

How large will India’s mid-power LED package market be by 2031?

It is projected to reach USD 328.70 million by 2031, reflecting a 5.9% CAGR from 2026-2031.

Which power range leads domestic demand?

Packages rated 0.5 W-to-1 W hold more than 63% share and enjoy a 6.78% CAGR outlook.

What is driving the fastest growth in application terms?

Automotive lighting is expanding at a 6.86% CAGR, driven by daytime running lamp mandates and the adoption of adaptive beams.

How do BIS 2026 standards affect suppliers?

The updated standards lift minimum efficacy to 110-120 lumens per watt, forcing suppliers to upgrade phosphor blends and high-bin chips.

Why is phosphor price volatility a concern?

China’s export controls on yttrium drove a 1,500% spike in 2026, slicing 150-200 basis points off gross margins for Indian package makers.

Are contract manufacturers reshaping competition?

Yes, ventures such as Dixon-Longcheer leverage PLI incentives to secure in-house LED backlighting demand, tightening local supply chains.

Page last updated on: