Microneedling Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

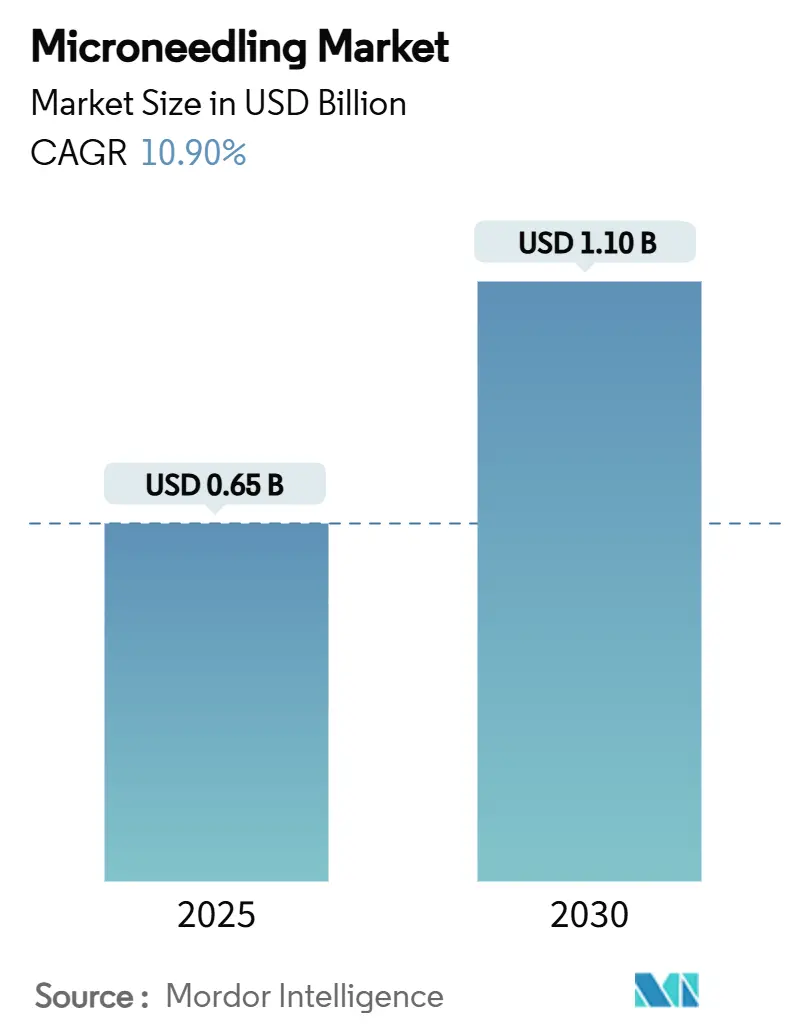

| Market Size (2025) | USD 0.65 Billion |

| Market Size (2030) | USD 1.10 Billion |

| Growth Rate (2025 - 2030) | 10.90% CAGR |

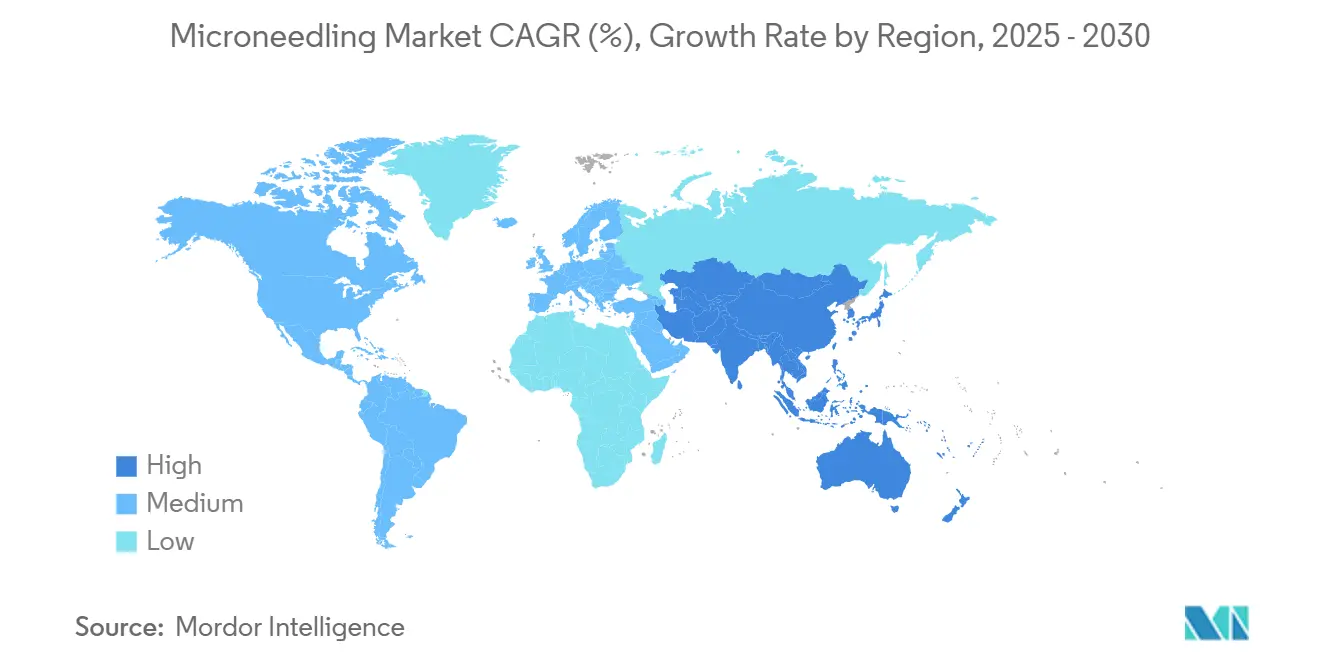

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

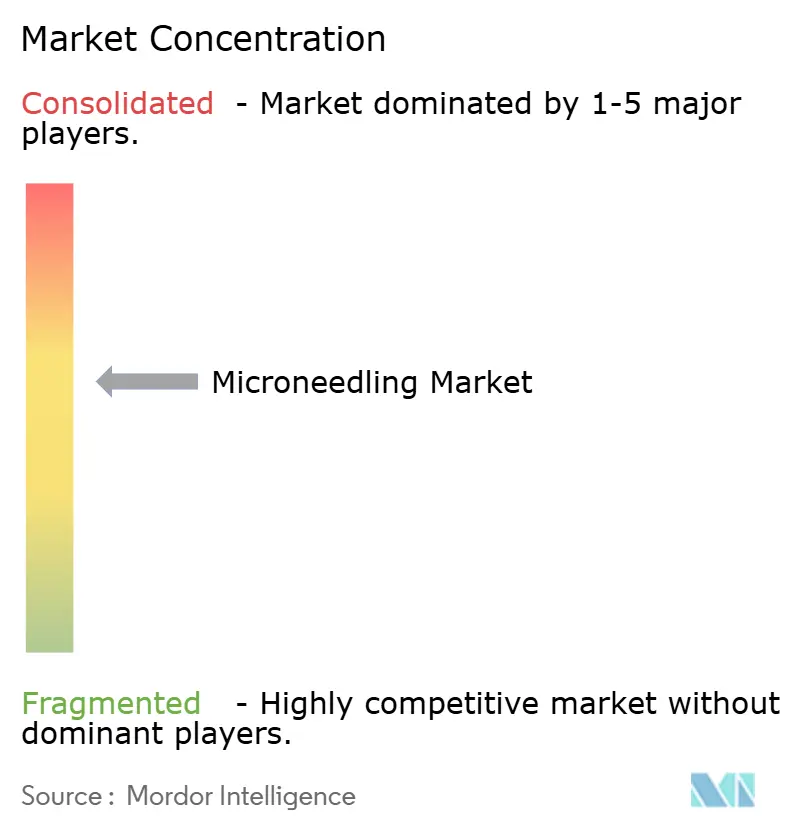

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microneedling Market Analysis by Mordor Intelligence

The microneedling market size stood at USD 0.65 billion in 2025 and is forecast to reach USD 1.1 billion by 2030, advancing at a 10.9% CAGR. This performance is powered by the convergence of radiofrequency (RF) integration, clear-cut regulatory guidance in major economies and a steady patient shift toward minimally invasive options that avoid surgical downtime. Automated pens remain the workhorse of the microneedling market, yet premium RF platforms are scaling quickly as practitioners prioritize predictable tissue contraction and deeper collagen remodeling. Demand is reinforced by a rising clinical consensus that microneedling complements, rather than substitutes, fractional lasers, especially for darker skin phototypes where laser-associated dyspigmentation risk persists. Parallel growth in platelet-rich plasma (PRP) and exosome add-ons raises procedure value, while at-home devices spur consumer awareness and funnel new patients into clinics.

Key Report Takeaways

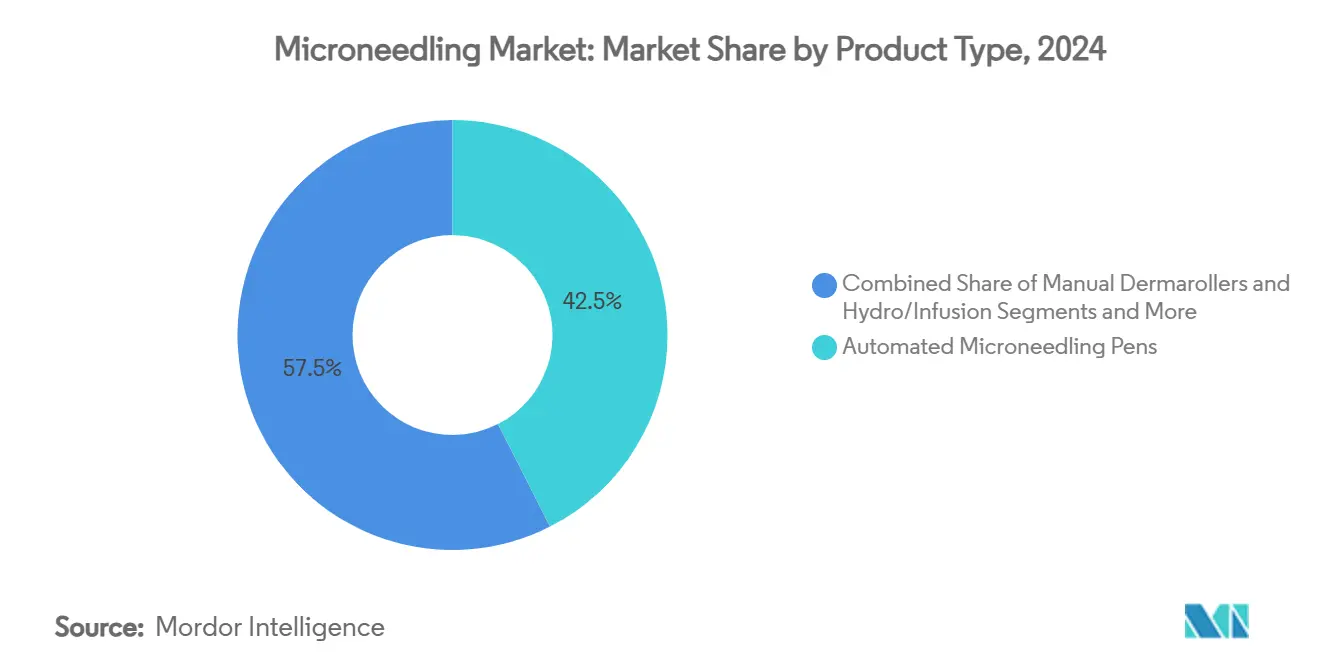

- By product type, automated pens held 42.5% of the microneedling market share in 2024. RF microneedling systems are projected to expand at a 13.8% CAGR through 2030.

- By application, skin rejuvenation commanded 38.2% of the microneedling market size in 2024. Alopecia and hair restoration are expected to post the fastest 16.2% CAGR between 2025-2030.

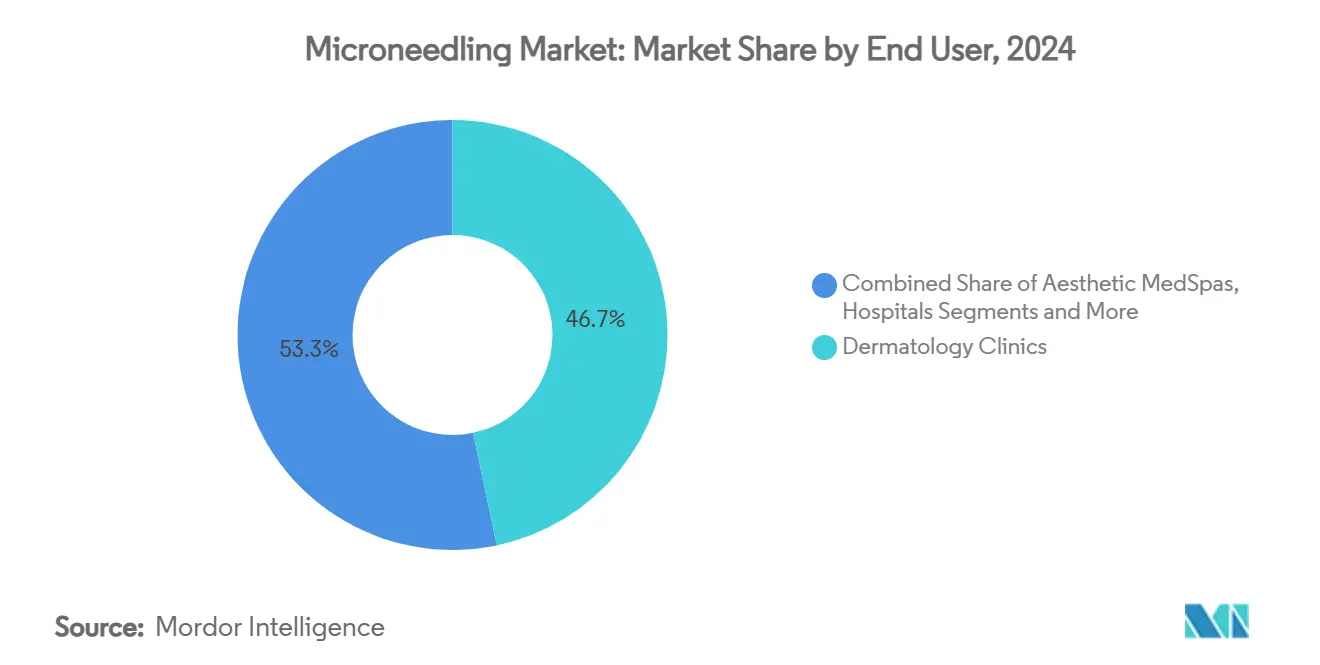

- By end user, dermatology clinics led with 46.7% revenue share in 2024, while the home-use segment is set to climb at a 14.9% CAGR through 2030.

- By geography, North America retained a 34.9% share of the microneedling market in 2024, and Asia Pacific is forecast to grow the quickest at an 11.5% CAGR to 2030.

Global Microneedling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Minimally-Invasive Aesthetic Procedures | +2.80% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Rising Prevalence Of Acne Scars & Photo-Aging | +1.90% | Global, particularly Asia Pacific & Latin America | Long term (≥ 4 years) |

| Rapid Device Innovation (Automated & RF Systems) | +2.10% | North America & EU leading, APAC adoption | Short term (≤ 2 years) |

| Expansion Of Aesthetic Clinics In Emerging Markets | +1.70% | APAC core, spill-over to MEA & Latin America | Medium term (2-4 years) |

| Surge In FDA-Cleared At-Home Microneedling Pens | +1.20% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Exosome-Enhanced Protocols Boosting Treatment Prices | +0.80% | North America & EU premium markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Minimally Invasive Aesthetic Procedures

Global procedure volumes confirm a structural tilt toward treatments that bridge topical skincare and surgery. Microneedling addresses this gap by tightening lax skin after weight-loss drug use, smoothing wrinkles, and amplifying adjunct therapies such as PRP. Patients value its low downtime, while practitioners benefit from the technology’s adaptability across face, neck and scalp indications. FDA clearances for soft-tissue contraction have further legitimized the modality.[1]U.S. Food & Drug Administration, “Regulatory Considerations for Microneedling Products,” fda.gov Clinics now routinely bundle microneedling with cosmeceutical actives, elevating revenue per session and driving repeat attendance. The convergence of pharmaceutical weight-management trends with aesthetic medicine therefore sustains a robust demand runway for the microneedling market.

Rising Prevalence of Acne Scars & Photo-Aging

Roughly 95% of acne-affected patients develop some degree of scarring, and lasers often pose dyspigmentation risks on darker skin tones. Fractional RF microneedling has demonstrated two-grade scar improvements in 80.6% of subjects while maintaining safety across all Fitzpatrick types. The mechanism of selective electrothermolysis triggers neocollagenesis yet preserves the epidermis, reducing recovery time. Photo-aging, compounded by longer life expectancy and UV exposure, enlarges the candidate pool. Pairing microneedling with growth-factor serums or peptides accelerates visible results and decreases the number of visits, reinforcing patient satisfaction and clinic throughput. These advantages translate into sustained volume growth for the microneedling market.

Rapid Device Innovation (Automated & RF Systems)

Regulators endorsed the category’s clinical potential when the FDA cleared the Morpheus8 applicator for tissue contraction in 2024. Automated pens eliminate operator-dependent depth variability, boosting outcome consistency and safety. Contemporary systems now include impedance-based real-time energy modulation and AI-guided protocols, allowing practitioners to customize settings by tissue thickness. Dissolving microneedle patches made of hyaluronic acid or PLGA broaden horizons beyond aesthetics toward drug and vaccine delivery.[2]MDPI, “Recent Advances in Microneedling-Assisted Cosmetic Applications,” mdpi.com These R&D pipelines inject sustained momentum into the microneedling market, particularly as clinics upgrade legacy pens to premium RF platforms.

Expansion of Aesthetic Clinics in Emerging Markets

Rapid clinic rollouts across Asia Pacific mirror rising disposable incomes and cultural acceptance of cosmetic enhancement. Accelerated approvals for innovative devices ease market entry in China, while medical tourism hubs in Thailand and the GCC markets fuel cross-border patient flow. Clinics in these economies often adopt RF systems early to differentiate services, shortening the adoption curve. Manufacturers support expansion with structured training programs that mitigate adverse-event risks and strengthen brand loyalty. The result is a widening geographic footprint for the microneedling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-Event Risk & Stringent Regulatory Hurdles | -1.80% | Global, particularly EU & North America | Long term (≥ 4 years) |

| High Capital & Procedure Costs For Providers | -1.40% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Competition From Non-Ablative Fractional Lasers | -1.10% | North America & EU mature markets | Medium term (2-4 years) |

| Proliferation Of Counterfeit Dermarollers Online | -0.90% | Global, with concentration in APAC & online marketplaces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Risk & Stringent Regulatory Hurdles

Once treated as simple dermal rollers, powered microneedling platforms are now Class II medical devices under the FDA’s 510(k) pathway.[3]U.S. Food & Drug Administration, “Regulatory Considerations for Microneedling Products,” fda.gov Requirements cover penetration depth, sterility, and biocompatibility testing. Several U.S. states further restrict estheticians from using powered pens without medical supervision, trimming the total addressable market. Counterfeit devices exacerbate complication rates, prompting heightened enforcement and consequently higher compliance costs for legitimate manufacturers. Fragmented classifications across global agencies prolong launch timelines and inflate R&D budgets, cooling the growth velocity of the microneedling market.

High Capital & Procedure Costs for Providers

Top-tier RF consoles often exceed USD 50,000, a steep outlay for single-site practices. Annual maintenance contracts and consumables add ongoing expense, nudging practitioners toward lower-cost dermarollers despite their limitations. Rising patient price sensitivity, especially where treatments are paid out-of-pocket, intensifies fee compression. The rapid spread of consumer-grade pens magnifies pricing tension as clients compare clinic quotes with at-home alternatives. Unless providers amortize devices through high procedure volumes, payback periods stretch, restraining equipment refresh cycles and tempering the expansion pace of the microneedling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RF Platforms Outpace While Pens Dominate

RF systems delivered the fastest 13.8% CAGR from 2025-2030, riding on superior clinical outcomes, durable collagen remodeling and a premium fee profile. Automated pens retained 42.5% of the microneedling market share in 2024, meeting everyday needs for acne scars, pores and stretch marks at manageable capital cost. Manual dermarollers have retreated to entry-level or consumer channels due to inconsistent depth control. Hydro-infusion pens carve small but lucrative niches by pairing serum delivery with needling in one pass. Dissolving microneedle patches, already mainstream in transdermal vaccination studies, hint at a disruptive leap that could double the broader microneedling market size for drug delivery within the decade.

RF consoles also sustain high consumable pull-through via single-use needle cartridges, elevating lifetime revenue streams for manufacturers. Energy-based platforms increasingly integrate impedance feedback and software-guided protocols, raising barriers to entry and reinforcing switching costs for clinics. Meanwhile, automated pen vendors pivot to cordless, lithium-powered designs that improve ergonomics and procedure speed. This cross-tier product evolution keeps the microneedling market vibrant and segmented across diverse capital-budget profiles.

By Application: Hair Restoration Becomes a Core Growth Engine

Skin rejuvenation commanded 38.2% of the microneedling market size in 2024, reflecting universal demand for wrinkle reduction and skin-texture refinement. Evidence that needling improves topical absorption has elevated the modality in hyperpigmentation and melasma protocols for darker phototypes. The alopecia segment is now the fastest-moving at 16.2% CAGR; electric microneedles enhance minoxidil uptake and stimulate follicular stem cells, driving 100% responder rates in moderate-to-severe androgenetic alopecia trials. Scars remain a steady revenue pillar: fractional RF needles outperform non-ablative lasers for ice-pick and rolling variants, particularly on sebaceous skin.

Stretch-mark and cellulite treatments leverage combined RF and mechanical needling to thicken dermal matrix and smooth dimpling, though adoption is still niche. Outside aesthetics, pharmaceutical researchers test dissolving patches for insulin, vaccines and pain therapy, potentially multiplying addressable volume by tapping large chronic-disease pools. If commercialization succeeds, transdermal medicine could outgrow cosmetic use, recasting the long-term ceiling for the microneedling market.

By End User: Consumer Uptake Accelerates Democratization

Dermatology and plastic-surgery clinics accounted for 46.7% of 2024 revenue, twice the share of medical-spa chains that emphasize ambiance over medical oversight. Yet home-use devices are scaling fastest at a 14.9% CAGR as consumers seek privacy, convenience, and lower price points. Consumer-grade pens must comply with stringent over-the-counter limits; one leading brand paused U.S. sales pending FDA reclassification, underscoring regulatory complexity. Despite hurdles, the direct-to-consumer channel widens awareness and often funnels patients into professional offices for more aggressive RF sessions. Hospitals and wound-care centers represent a small but expanding cohort, applying needling for scar contracture and drug infusion. As end-user diversity broadens, training, consumable logistics, and after-sales support become pivotal competitive levers across the microneedling market.

Geography Analysis

North America’s leadership in the microneedling market stems from clear regulatory expectations, widespread practitioner expertise, and consumer readiness to invest in elective procedures. FDA guidance on powered devices sets safety benchmarks that build patient trust. New product approvals—such as a micro-coring platform cleared in Canada—underscore continuous innovation across the region, where total aesthetic device revenue is set to surpass USD 7 billion by 2030. The GLP-1-driven body-contouring surge funnels clients seeking adjunct facial tightening, pushing demand for RF microneedling services.

Asia Pacific is adding patients even faster. Device approvals via accelerated pathways and cost-competitive treatment packages encourage cross-border travel from mature to emerging economies inside the region. Highly digital consumer behavior speeds word-of-mouth diffusion, while younger demographics adopt preventive skincare earlier, enlarging lifetime values per patient. Clinics frequently bundle microneedling, energy-based tightening, and topical K-Beauty actives in a single session, raising ticket size and supporting double-digit revenue growth in the microneedling market.

Europe provides a stable base. Harmonized rules under the EU Medical Device Regulation extend review times, but once they are cleared, devices benefit from continent-wide marketability. Practitioners emphasize combination protocols that meet strict post-treatment downtime expectations, making depth-controlled RF needles attractive. In the Middle East and Africa, Gulf Cooperation Council states are investing in JCI-accredited hospitals and luxury medical spas, enabling high-yield segments such as radiofrequency microneedling for scarring acne among younger populations. Latin America, led by Brazil and Mexico, is catalyzed by a cultural affinity for cosmetic enhancement; nonetheless, currency volatility and import tariffs can delay equipment upgrades.

Competitive Landscape

The microneedling market remains moderately fragmented, yet consolidation momentum is evident as manufacturers chase scale and broader portfolios. Mergers between RF-centric and laser-centric companies create combined offerings spanning facial, body, and drug-delivery use cases. Private-equity interest has intensified, with recent acquisitions designed to optimize distribution footprints and accelerate R&D pipelines. Firms that excel typically cope with proprietary technology with strong clinical education programs, safeguarding consistent results that build practitioner confidence.

Product differentiation is now anchored in software, cartridge design, and treatment versatility. Flagship RF consoles integrate impedance feedback loops and AI-driven setting libraries that auto-adjust pulse width to tissue impedance, enhancing safety. Cartridge-as-a-service models lock clinics into exclusive consumables, generating recurring revenue and discouraging brand switching. Meanwhile, automated pen makers focus on ergonomic improvements, cordless powertrains, and antimicrobial needle coatings. These innovations raise entry barriers and fortify brand equity across the microneedling market.

Capital allocation strategies vary. Well-capitalized leaders post high gross margins and funnel 10-14% of sales into R&D, funding next-generation systems that cross the aesthetics-therapeutics boundary. Smaller firms often adopt an OEM approach, rebranding white-label pens while investing heavily in social media outreach. Regulatory compliance costs are increasing, tilting advantage toward players with global quality-management infrastructures. Overall, top five suppliers jointly control less than 45% of global revenue, indicating room for further consolidation to unlock scale benefits and streamline regulatory navigation.

Microneedling Industry Leaders

DermapenWorld

Crown Aesthetics (SkinPen)

Cynosure

Cutera

Candela Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cutera completed a debt-reduction program totaling USD 400 million and secured USD 65 million of new capital to support pipeline launches and global expansion.

- November 2024: Lumenis France signed a distribution accord with X-Derma to widen access to its aesthetic technology suite across metropolitan clinics.

- August 2024: Candela received FDA clearance for the Matrix Pro RF microneedling applicator to treat facial wrinkles, with 94% of clinical-trial participants noting visible improvement.

- January 2024: Consumer-brand Dr. Pen voluntarily halted U.S. sales while pursuing FDA reclassification for its at-home devices, demonstrating the regulatory hurdles facing DTC models.

Global Microneedling Market Report Scope

| Manual Dermarollers |

| Automated Microneedling Pens |

| RF Microneedling Systems |

| Hydro / Infusion Microneedling Devices |

| Dissolving Microneedle Patches |

| Skin Rejuvenation & Anti-aging |

| Acne & Surgical Scar Revision |

| Hyperpigmentation & Melasma |

| Alopecia / Hair Restoration |

| Stretch Marks & Cellulite |

| Transdermal Drug / Vaccine Delivery |

| Dermatology & Plastic Surgery Clinics |

| Aesthetic MedSpas |

| Hospitals |

| Home-use Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Manual Dermarollers | |

| Automated Microneedling Pens | ||

| RF Microneedling Systems | ||

| Hydro / Infusion Microneedling Devices | ||

| Dissolving Microneedle Patches | ||

| By Application | Skin Rejuvenation & Anti-aging | |

| Acne & Surgical Scar Revision | ||

| Hyperpigmentation & Melasma | ||

| Alopecia / Hair Restoration | ||

| Stretch Marks & Cellulite | ||

| Transdermal Drug / Vaccine Delivery | ||

| By End User | Dermatology & Plastic Surgery Clinics | |

| Aesthetic MedSpas | ||

| Hospitals | ||

| Home-use Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current microneedling market size?

The microneedling market size was valued at USD 0.65 billion in 2025.

How fast is the microneedling market expected to grow?

From 2025 to 2030 the market is projected to record a 10.9% CAGR, reaching USD 1.1 billion by the end of the forecast period.

Which product segment leads the microneedling market?

Automated pens hold the largest 42.5% revenue share, thanks to versatility across acne, scar and rejuvenation treatments.

What is driving the rapid uptake of RF microneedling systems?

RF platforms deliver deeper collagen remodeling, precise energy control and have secured expanded FDA indications for soft-tissue contraction, pushing them to a 13.8% CAGR trajectory.

Why is Asia Pacific the fastest-growing region?

A rising middle class, favorable regulatory pathways for new devices and cultural affinity for aesthetic enhancements underpin the region’s 11.5% CAGR outlook.

Are at-home microneedling devices regulated?

Yes. Consumer-grade devices must satisfy FDA rules on needle length, sterility and labeling; several brands paused sales while pursuing reclassification to achieve compliance.

Page last updated on: