Microneedle Drug Delivery Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

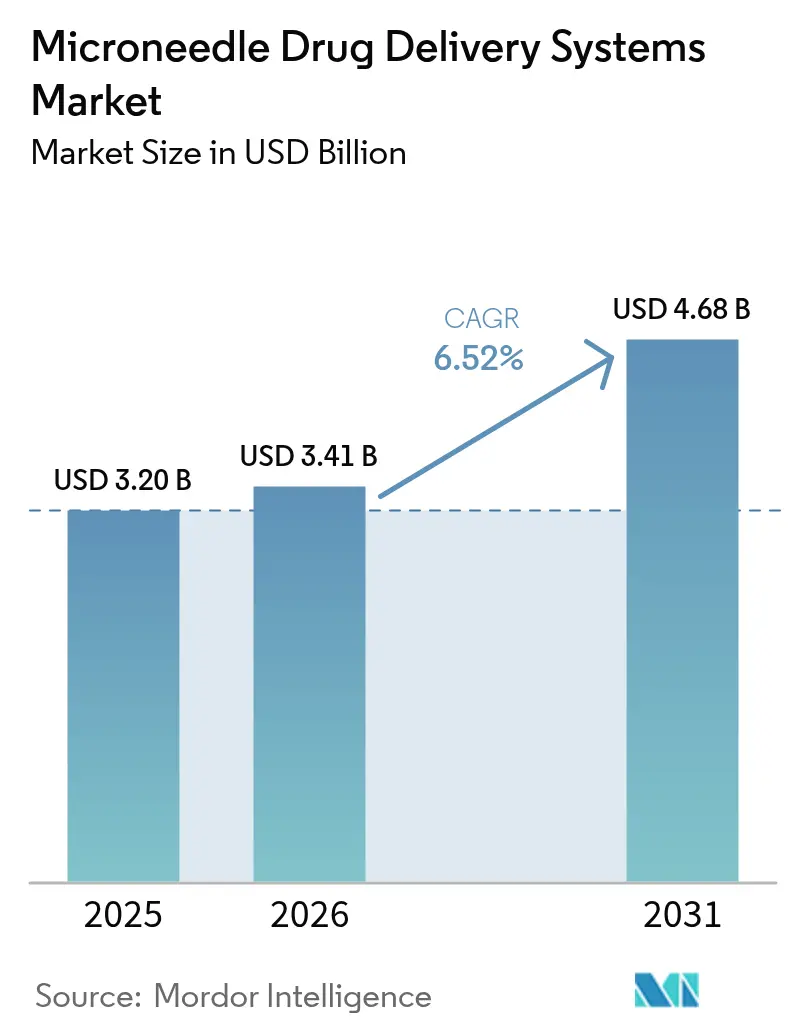

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.68 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

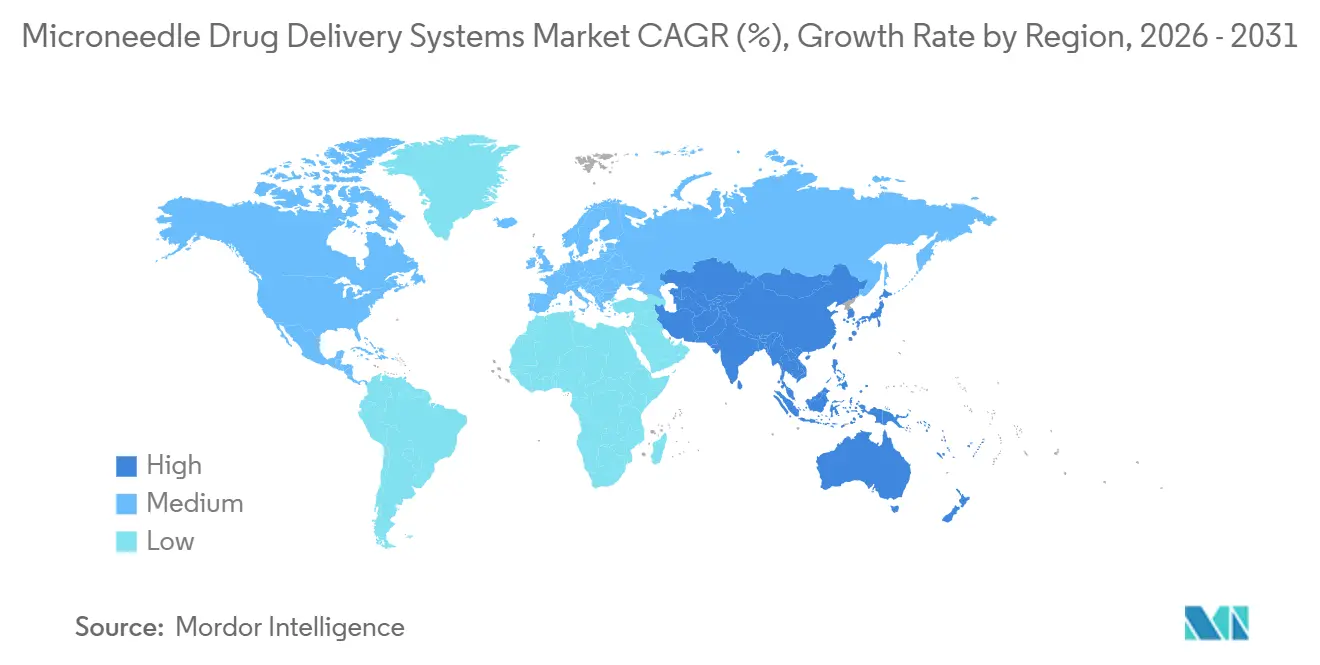

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microneedle Drug Delivery Systems Market Analysis by Mordor Intelligence

The microneedle drug delivery systems market size is projected to expand from USD 3.20 billion in 2025 and USD 3.41 billion in 2026 to USD 4.68 billion by 2031, registering a CAGR of 6.52% between 2026 to 2031. Solid growth reflects a strategic pivot toward dissolving and biodegradable designs that avoid sharps waste and support cold-chain independence. Peptide therapeutics are a key pull factor: Daewoong Pharmaceutical’s semaglutide patch achieved more than 80% relative bioavailability in 2024 Phase II trials, demonstrating clinical parity with subcutaneous injection. At the same time, defense and space-medicine agencies are running field pilots with ultra-compact patches that function outside hospital supply chains. Manufacturing capacity is scaling, led by Chinese roll-to-roll lines that push unit costs below USD 0.12, while MEMS-etched silicon arrays set new performance benchmarks in insertion reliability. Collectively, these shifts reposition the microneedle drug-delivery systems market as a mainstream platform for vaccination, diabetes care, and emergent biologics rather than a niche device category.

Key Report Takeaways

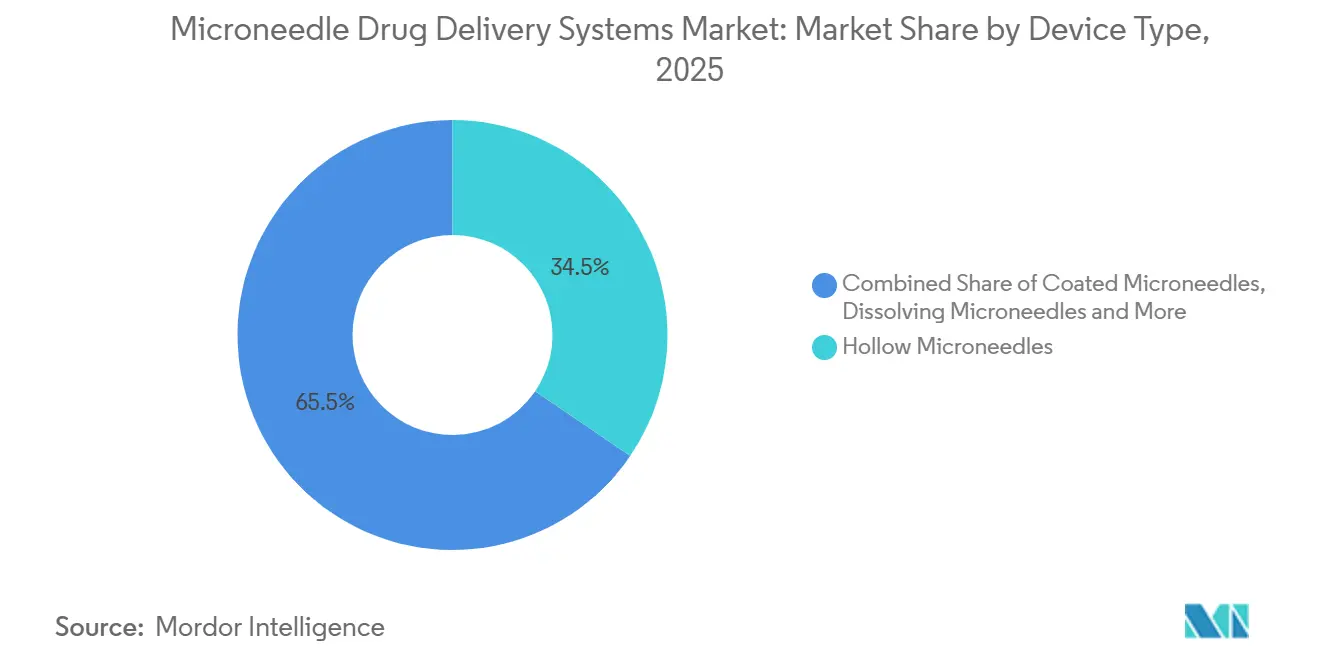

- By device type, hollow microneedles led with 34.55% of microneedle drug delivery systems market share in 2025, while dissolving variants are advancing at a 9.85% CAGR through 2031.

- By material, polymers held 45.53% share of the microneedle drug delivery systems market size in 2025 and silicon is projected to grow at 9.75% between 2026-2031.

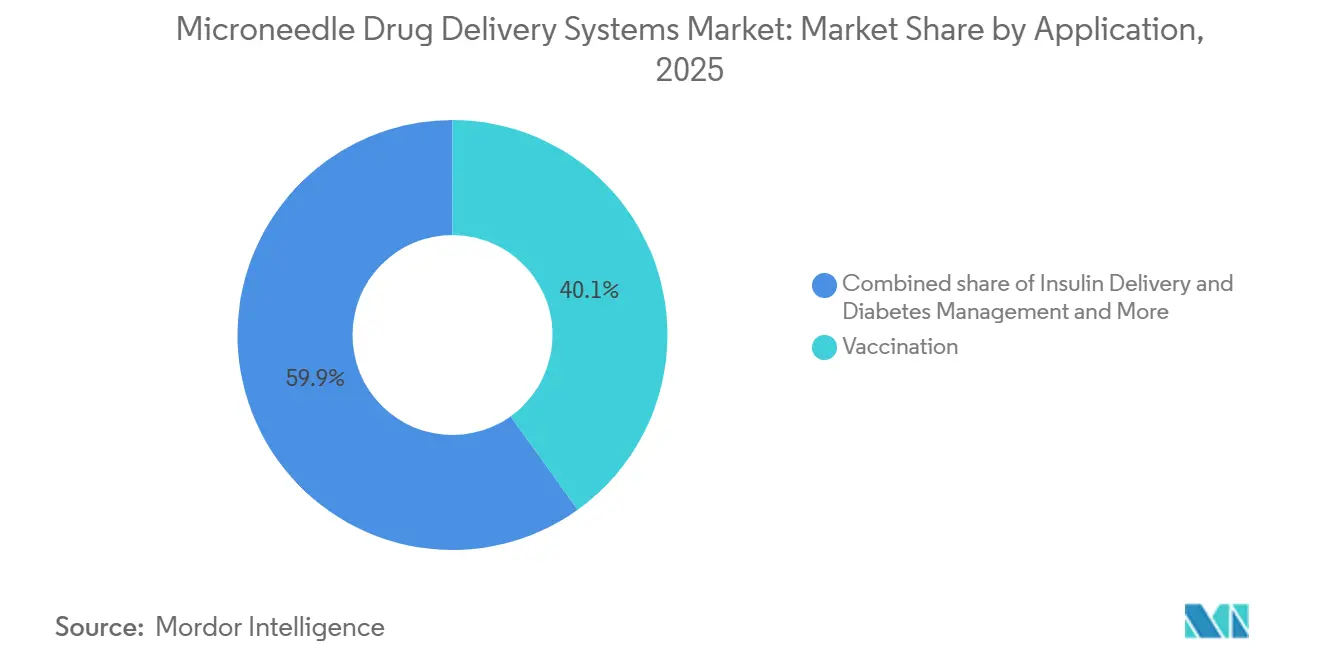

- By application, vaccination accounted for 40.15% of 2025 revenue yet insulin delivery is forecast to post the fastest 10.82% CAGR to 2031.

- By end user, hospitals and clinics contributed 44.52% of 2025 sales, whereas home-care settings will expand at a 10.12% CAGR over 2026-2031.

- By geography, North America retained 42.55% revenue share in 2025 and Asia-Pacific is set to register the highest 9.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microneedle Drug Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases requiring painless self-administration | +1.8% | Global, highest intensity in North America and Europe | Medium term (2-4 years) |

| Advantages over conventional injections improving patient compliance | +1.5% | Global, strong in home-care settings across developed markets | Short term (≤ 2 years) |

| Growing vaccination initiatives adopting patch-based delivery | +1.3% | APAC core, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Technological advances in dissolving / biodegradable microneedles | +1.2% | North America and APAC (Japan, South Korea, China) | Long term (≥ 4 years) |

| Regulatory incentives to curb needle-stick injuries and sharps waste | +0.9% | North America, EU, spillover to MEA and Latin America | Short term (≤ 2 years) |

| Defense and space-medicine demand for ultra-compact, shelf-stable delivery | +0.6% | North America, select EU defense ministries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Painless Self-Administration

Diabetes affected 537 million adults in 2025 and is projected to reach 643 million by 2030, yet needle phobia continues to suppress adherence to injectable insulin. Microneedle patches remove visible needles and deliver basal doses aligned with weekly regimens, improving time-in-range outcomes by 23% in real-world studies[1]Lisa Valeritas et al., “V-Go Real-World Study,” Diabetes Technology & Therapeutics, liebertpub.com . Oncology trials now exploit dissolving arrays for intratumoral checkpoint inhibitors, achieving drug concentrations 40-fold higher than intravenous delivery with minimal systemic toxicity. Reimbursement parity for insulin patches in the United States and Germany removes a historic commercial obstacle. Collectively, these factors elevate microneedle patches from optional convenience to clinically mandated tools in chronic-disease pathways.

Advantages Over Conventional Injections Improving Patient Compliance

Needle phobia afflicts up to 30% of adults and 63% of children, directly limiting vaccine coverage. Microneedles penetrate only 50-900 µm into dermal tissue, avoiding nerve-rich layers and virtually eliminating pain. A 2024 randomized trial showed 89% of participants preferred the influenza patch over intramuscular injection, with pediatric acceptance rising to 91%. Gavi’s 2025-2030 strategy lists 11 vaccines for microneedle reformulation to close immunization gaps. Community health‐worker programs in rural India raised measles-rubella coverage from 78% to 97% using self-applicable patches. These findings confirm that painless delivery directly translates into higher population-level adherence.

Growing Vaccination Initiatives Adopting Patch-Based Delivery

The WHO-CEPI VIPS Alliance elevated microneedle patches to Tier 1 priority in 2024, citing cold-chain independence as essential for epidemic response. Vaxxas’ measles-rubella patch remained stable at 40 °C for 12 months and delivered non-inferior immunogenicity in Phase II trials. Sanofi’s quadrivalent influenza patch reached 92% seroconversion in interim Phase III data versus 88% for standard intramuscular vaccine. FDA draft guidance in 2025 enables a streamlined 510(k) route for vaccine patches that show bioequivalence, cutting review times to 12-18 months. Together, these developments reposition patches as the preferred modality for both mass immunization and rapid outbreak control.

Technological Advances in Dissolving / Biodegradable Microneedles

Polyvinylpyrrolidone, PLGA, and carboxymethyl cellulose formulations dissolve within minutes, eliminating sharps disposal and enabling ambient storage. MIT’s 3D-printed pillar-guided arrays achieved 95% dose uniformity across 1,000 needles, surpassing regulatory thresholds. Daewoong’s CLOPAM semaglutide patch matched injection bioavailability while dissolving in 15 minutes. Hydrogel-forming needles deliver zero-order insulin release for 48 hours, maintaining euglycemia without hypoglycemia in animal models. Silicon needles etched via MEMS processes insert with 98% success across diverse skin types. The cumulative effect is a broadened design toolkit that supports higher payloads, longer wear times, and tighter dose control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited drug-loading capacity per patch | -1.1% | Global, constraining high-dose biologics in North America and EU | Medium term (2-4 years) |

| Stringent and fragmented regulatory pathways | -0.8% | Global, most acute in EU and emerging markets | Short term (≤ 2 years) |

| Skin-microbiome variability impacting dose reproducibility | -0.6% | Global, larger variance in tropical regions | Long term (≥ 4 years) |

| Scarcity of GMP roll-to-roll fabrication equipment inflating CAPEX | -0.5% | North America, EU, APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Drug-Loading Capacity Per Patch

Typical dissolving arrays hold 0.5-2 mg of active drug per cm², far below the 50-200 mg required for monoclonal antibodies. Delivering a 100 mg dose would demand a 50 cm² patch, an impractical footprint for patients. Hollow designs can deliver liquids but reintroduce sharps disposal and cold-chain burdens. Cyclodextrin complexation quadrupled insulin payloads to 4.8 mg per array in a 2025 proof-of-concept, yet scale-up remains years away. Until such breakthroughs mature, the microneedle drug-delivery systems market will cede high-dose biologics to autoinjectors.

Stringent and Fragmented Regulatory Pathways

Combination-product status requires dual evaluations. Zosano’s migraine patch spent 14 additional months in review before receiving a Complete Response Letter in 2024 that cited human-factors deficits. Europe’s MDR now mandates clinical evidence for all combination devices, disallowing literature-based routes that once accelerated low-risk submissions. India classifies microneedle patches as new drugs, obliging domestic Phase III studies despite foreign approvals. Sequential launches inflate go-to-market costs and slow global revenue capture, dampening near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Dissolving Variants Reshape Competitive Dynamics

Dissolving microneedles are forecast to grow 9.85% annually, outpacing the microneedle drug delivery systems market by 3.3 percentage points and eroding the 34.55% 2025 revenue share once held by hollow designs. Sharps-free disposal and ambient stability resonate with home-care users and vaccine agencies. Hydrogel-forming arrays enter pivotal trials for long-acting hormones, while coated and solid variants slip toward commoditization as Asian contract manufacturers undercut prices.

Hollow microneedles remain essential for real-time insulin titration, yet OSHA’s mandate to review needle-free options clouds their long-term outlook. Additive manufacturing widens design space; pillar-guided arrays hit 95% dose uniformity, signaling a shift toward high-precision geometries. Market leaders now split portfolios: premium dissolving formats for chronic therapies and cost-optimized hollow kits for acute care.

By Material: Silicon Gains Ground Despite Polymer Dominance

Polymers commanded 45.53% of the microneedle drug-delivery systems market size in 2025, yet silicon is poised for the fastest 9.75% CAGR through 2031. Deep-reactive-ion-etched silicon reaches aspect ratios above 10:1 and insertion success of 98%.

Polymer arrays keep majority share through cost advantages—USD 0.08-0.15 per unit versus USD 0.40-0.70 for silicon—and their GRAS status speeds vaccine approvals. Metals retreat as dissolving polymers displace them for safety. Carbohydrate needles grow in pediatric vaccines, leveraging biodegradable sugars. Silicon’s optical transparency also halves batch-rejection rates via machine-vision inspection, aligning with quality initiatives in high-value biologics.

By Application: Insulin Delivery Outpaces Vaccination Growth

Vaccination held 40.15% of 2025 revenue, yet insulin management will advance at a 10.82% CAGR, the strongest among all uses. Continuous glucose monitoring integration turns patches into closed-loop systems that raise time-in-range metrics by 23%.

Pain management, dermatology, and oncology follow with steady gains. Lidocaine patches shorten outpatient procedures, while cosmetic hyaluronic-acid patches sell through over-the-counter channels in Japan and South Korea. Intratumoral microneedles for checkpoint inhibitors register 40-fold tumor drug concentration improvements in early trials. Segment diversification spreads risk and widens the addressable microneedle drug-delivery systems market.

By End User: Home-Care Settings Drive Structural Shift

Hospitals and clinics generated 44.52% of 2025 sales but face share erosion as payers shift chronic management to patients’ homes. Home-care venues are forecast to post a 10.12% CAGR, the fastest across end users.

Medicare Part D coverage for insulin patches began in 2025, lowering copays and spurring adoption in the United States. Community programs in India achieved 97% measles-rubella coverage when distributing self-applied patches. Hospitals retain dominance in oncology where initial dosing requires observation, but even these clinics use patches for maintenance therapy, compressing chair time and freeing infusion capacity.

Geography Analysis

North America retained 42.55% microneedle drug-delivery systems market share in 2025 on the strength of an established 510(k) route and USD 18 million in DoD contracts. FDA guidance issued in 2025 further streamlined vaccine-patch approvals. Canada leverages its agile licensing pathway to host Phase II studies, and Mexico’s fledgling market is held back by limited public procurement. Regionally, diabetes and dermatology lead uptake thanks to robust reimbursement and high out-of-pocket willingness.

Asia-Pacific is forecast to grow at 9.72%, the fastest regional CAGR, fueled by China’s low-cost roll-to-roll output, Japan’s revised legislation that accelerates cosmetic-device approvals[2]PMDA, “Revised Pharmaceutical Affairs Legislation,” pmda.go.jp, and South Korea’s K-beauty exports. India channels public funds toward cold-chain-free vaccines for remote districts. Australia and South Korea target premium diabetes and oncology patches. Diverse national priorities produce a mosaic of growth levers yet converge on a single theme: cost-efficient manufacturing married to rising consumer expectations.

Europe grows more slowly due to fragmented reimbursement. Germany’s statutory insurer began covering dissolving insulin patches in 2025, but France and Spain await local cost-effectiveness studies. The UK’s NICE endorsed influenza patches but NHS rollout lags budget cycles. GCC nations adopt premium microneedle products, while South Africa pilots measles-rubella patches in rural clinics. Brazil leads South America after ANVISA cleared an insulin patch in 2024. Across territories, absence of harmonized device–drug rules forces stepwise launches, diluting speed to market.

Competitive Landscape

The microneedle drug-delivery systems market is moderately fragmented. The top five players, Becton Dickinson, Corium International, Terumo, Nitto Denko, and Vaxxas, control a sizeable slice of 2025 revenue, yet startup pipelines swell on academic IP. Asian contract manufacturers drive price competition by supplying polymer arrays at USD 0.08-0.12 per unit, forcing incumbents to differentiate on regulatory track record and hospital relationships.

Vaxxas differentiates through a spring-loaded applicator that assures penetration consistency, proven in measles-rubella Phase II trials. Micron Biomedical’s USD 33 million Series B funded a 50,000 ft² GMP plant in Georgia, providing scale parity with larger device firms. Patent filings for microneedle technologies rose 42% year-over-year in 2025 with hydrogel and MEMS silicon the fastest-growing categories[3]USPTO Analytics, “2025 Microneedle Patent Trends,” uspto.gov.

Large pharma is increasingly partnering rather than building in-house expertise: Corium licensed its platform to a top-10 drug maker for a diabetes patch in 2024. Asian cosmetics brands exploit regulatory gray zones to market hyaluronic-acid patches as wellness devices, gaining early consumer mindshare. Consolidation is likely as incumbents acquire innovative startups to secure IP and as contract manufacturers move up the value chain into branded offerings.

Microneedle Drug Delivery Systems Industry Leaders

Becton, Dickinson and Company

Corium International, Inc.

Terumo Corporation

Nitto Denko Corporation

Vaxxas Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Daewoong Pharmaceutical reported its semaglutide microneedle patch exceeded 80% relative bioavailability in a human pharmacokinetic study.

- April 2025: ARPA-H unveiled a home-use intradermal microneedle device developed under its SBIR program to accelerate patient-centric drug delivery.

Global Microneedle Drug Delivery Systems Market Report Scope

As per the scope of this report, a microneedle drug delivery system is a transdermal drug delivery system used to administer drugs and vaccines in a non-invasive, painless manner. Microneedles create temporary, micron-sized pores on the skin through which drugs and vaccines are delivered.

The microneedle drug-delivery systems market segmentation is based on device type, material, application, end-user, and geography. By device type, the market includes solid microneedles, hollow microneedles, coated microneedles, dissolving microneedles, and hydrogel-forming microneedles. By material, it is segmented into silicon, metals (stainless steel, titanium), polymers (PVP, PLA, PLGA, etc.), carbohydrates and sugars, and other materials (ceramics and composites). By application, the market covers vaccination, insulin delivery and diabetes management, pain management/local anesthesia, dermatology and cosmetics, oncology and immuno-oncology, and other applications. By end-user, the segmentation includes hospitals and clinics, pharmaceutical and biotech companies, academic and research institutes, and home care and self-administration settings. By geography, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the value (in USD) for the above segments.

| Solid Microneedles |

| Hollow Microneedles |

| Coated Microneedles |

| Dissolving Microneedles |

| Hydrogel-Forming Microneedles |

| Silicon |

| Metals (Stainless Steel, Titanium) |

| Polymers (PVP, PLA, PLGA, etc.) |

| Carbohydrates & Sugars |

| Other Material (Ceramics & Composites) |

| Vaccination |

| Insulin Delivery & Diabetes Management |

| Pain Management / Local Anesthesia |

| Dermatology & Cosmetics |

| Oncology & Immuno-Oncology |

| Other Applications |

| Hospitals & Clinics |

| Pharmaceutical & Biotech Companies |

| Academic & Research Institutes |

| Homecare & Self-Administration Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Solid Microneedles | |

| Hollow Microneedles | ||

| Coated Microneedles | ||

| Dissolving Microneedles | ||

| Hydrogel-Forming Microneedles | ||

| By Material | Silicon | |

| Metals (Stainless Steel, Titanium) | ||

| Polymers (PVP, PLA, PLGA, etc.) | ||

| Carbohydrates & Sugars | ||

| Other Material (Ceramics & Composites) | ||

| By Application | Vaccination | |

| Insulin Delivery & Diabetes Management | ||

| Pain Management / Local Anesthesia | ||

| Dermatology & Cosmetics | ||

| Oncology & Immuno-Oncology | ||

| Other Applications | ||

| By End-user | Hospitals & Clinics | |

| Pharmaceutical & Biotech Companies | ||

| Academic & Research Institutes | ||

| Homecare & Self-Administration Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the microneedle drug-delivery systems market be by 2031?

The microneedle drug-delivery systems market size is projected to reach USD 4.68 billion by 2031.

Which segment is expanding the fastest?

Insulin delivery applications are expected to post the strongest 10.82% CAGR between 2026-2031 thanks to closed-loop patch systems.

Why are dissolving microneedles gaining share?

They remove sharps waste, enable cold-chain-free transport, and match injection bioavailability for peptides such as semaglutide.

What limits broader adoption in high-dose biologics?

Dissolving patches currently hold only up to 2 mg of drug per cm², well below antibody dose requirements.

Which region offers the highest growth potential?

Asia-Pacific is forecast to record a 9.72% CAGR through 2031, underpinned by China's manufacturing scale and Japan's regulatory reforms.

How are regulators supporting the technology?

FDA draft guidance in 2025 enables an expedited 510(k) pathway for vaccine patches that demonstrate bioequivalence, shortening U.S. review times to 12-18 months.

Page last updated on: