Global Microtomes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

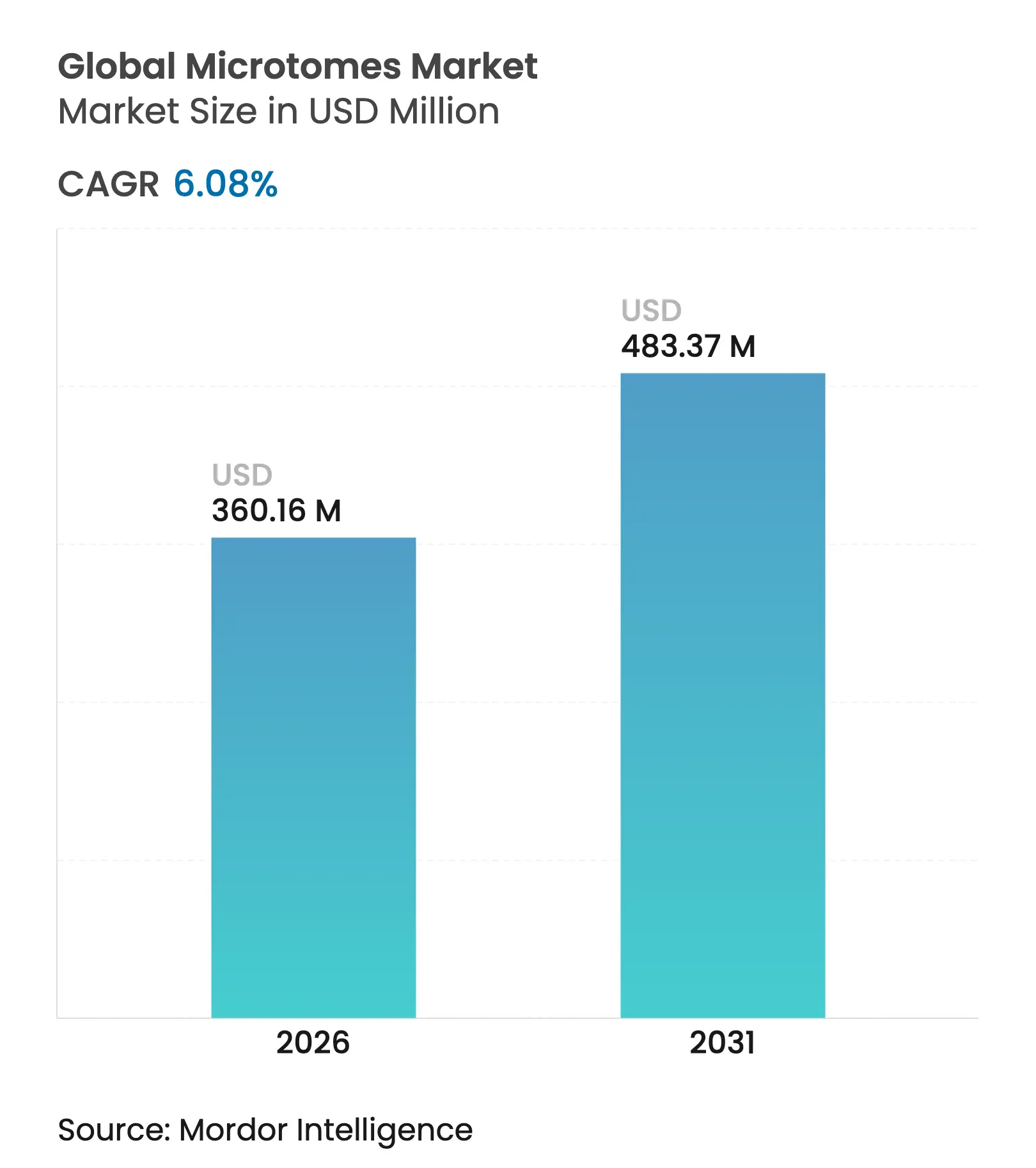

| Market Size (2026) | USD 360.16 Million |

| Market Size (2031) | USD 483.37 Million |

| Growth Rate (2026 - 2031) | 6.08 % CAGR |

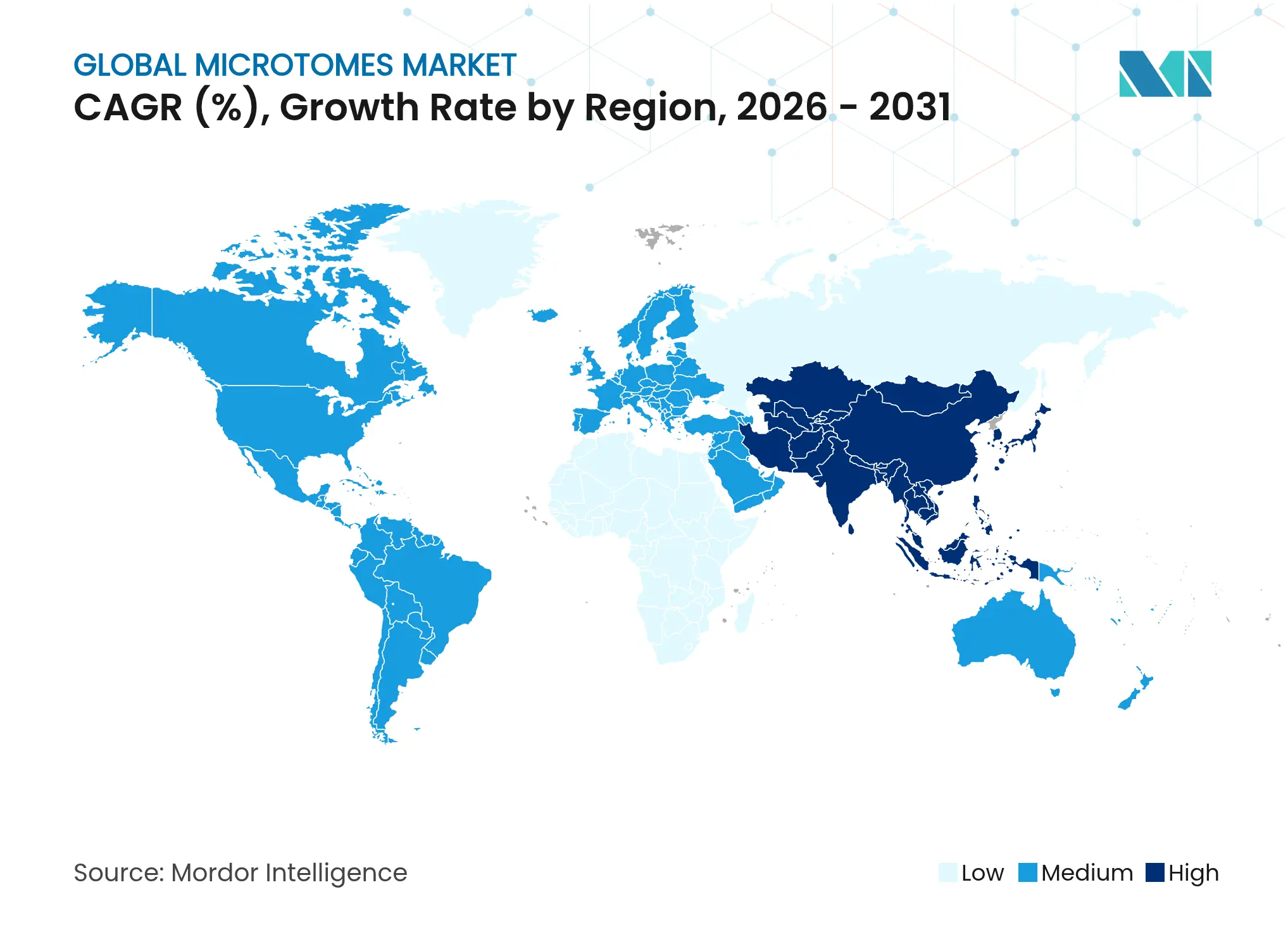

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Global Microtomes Market Analysis by Mordor Intelligence

The microtomes market size is expected to grow from USD 339.52 million in 2025 to USD 360.16 million in 2026 and is forecast to reach USD 483.37 million by 2031 at 6.08% CAGR over 2026-2031. Rising global cancer incidence, accelerating digital pathology projects, and ongoing laboratory infrastructure investments in emerging economies are the chief growth engines. Automated sectioning systems are gaining traction as health systems confront staffing shortages and the need for throughput gains. Regional dynamics remain uneven: North America retains scale advantages, yet Asia-Pacific laboratories are adopting new instruments fastest as governments prioritize self-reliance in medical technology. On the competitive front, suppliers are bundling precision sectioners with whole-slide imaging software, while also investing in local blade production to shield customers from geopolitical supply risks.

Key Report Takeaways

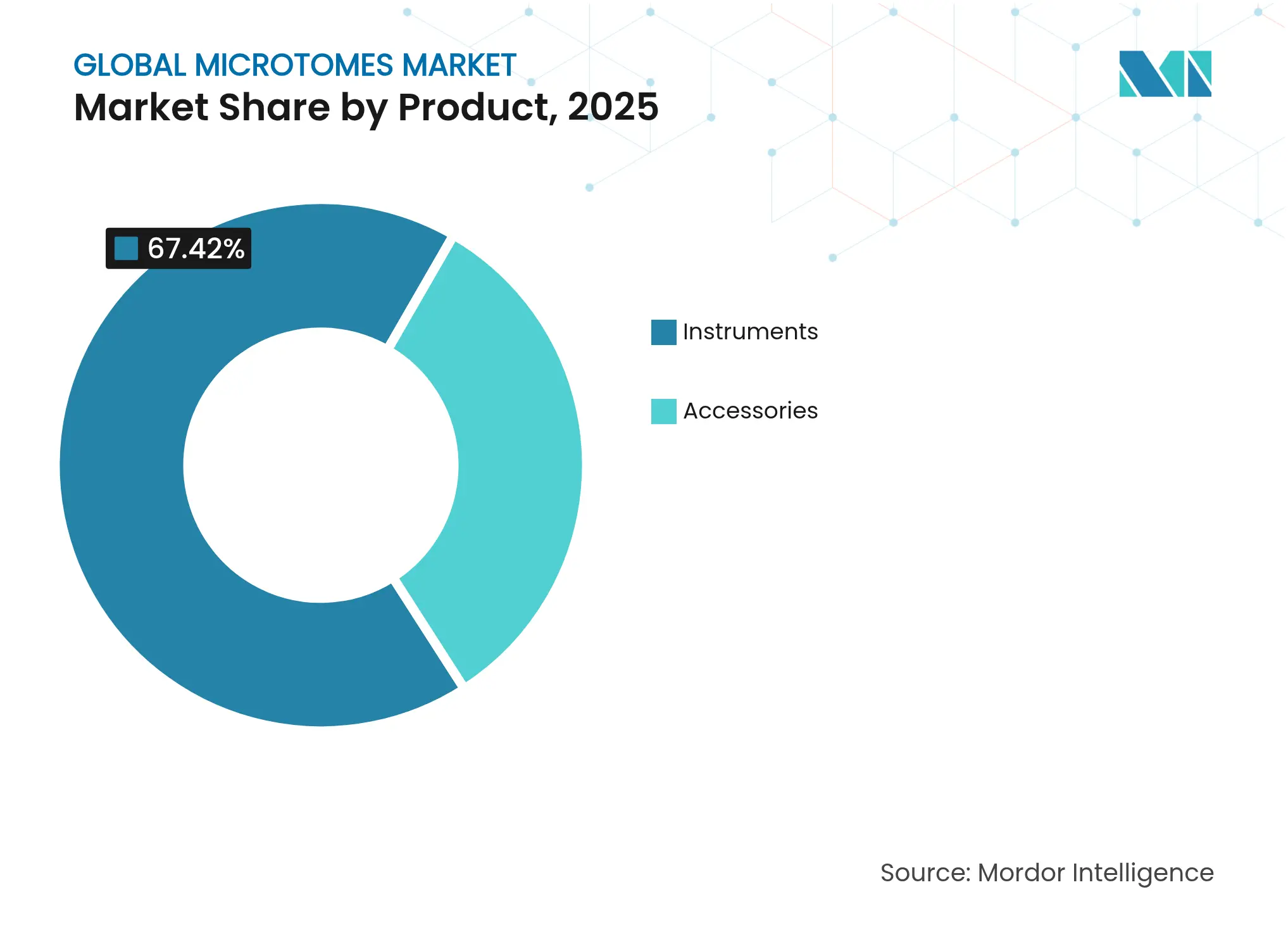

- By product, instruments led with 67.42% revenue share in 2025; accessories are projected to expand at a 6.73% CAGR to 2031.

- By technology, manual systems accounted for 52.56% of microtomes market share in 2025, whereas fully automated platforms are advancing at a 7.22% CAGR through 2031.

- By application, disease diagnostics held 64.22% of the microtomes market size in 2025; digital pathology is the fastest-growing use case at 7.3% CAGR to 2031.

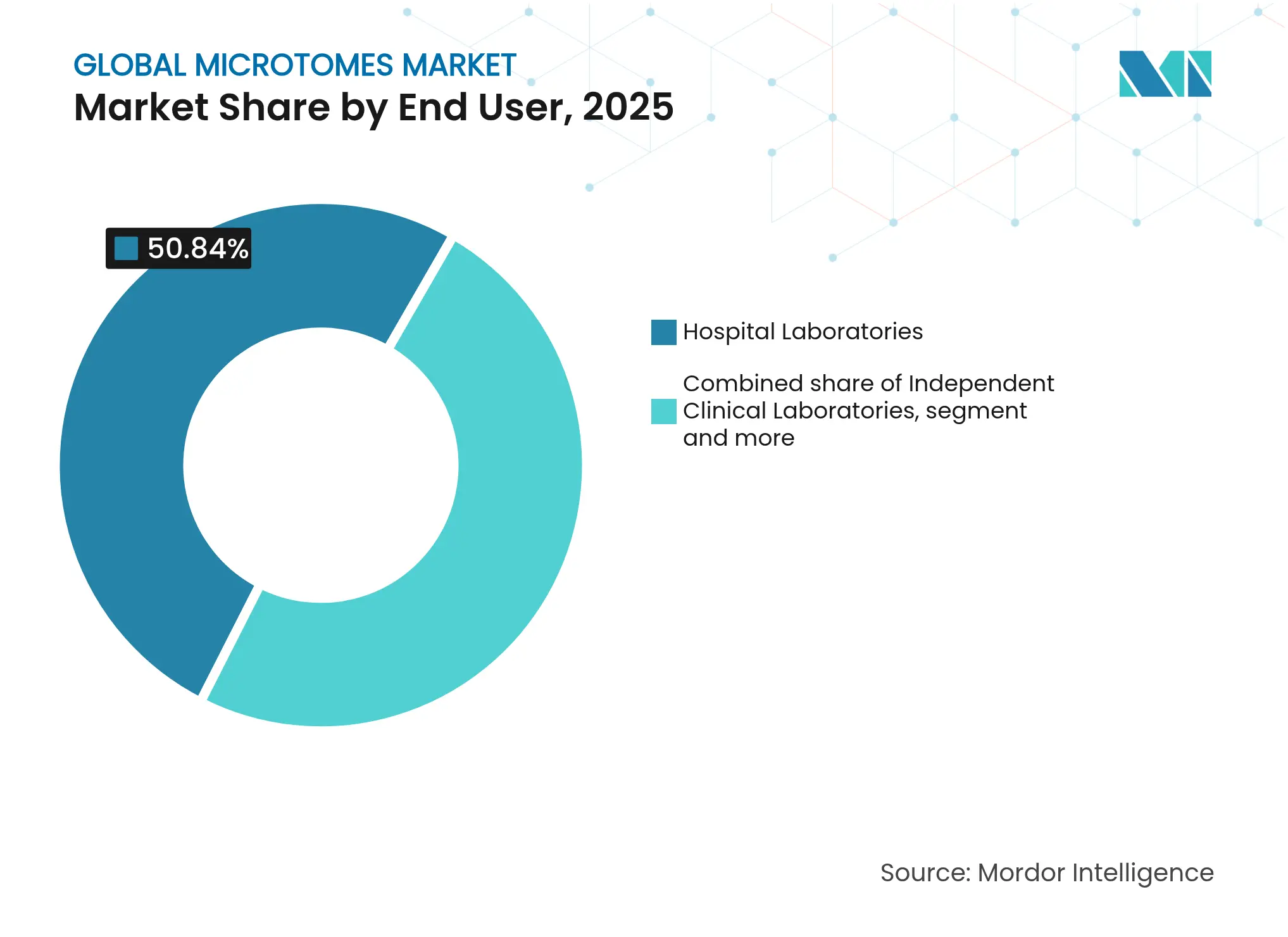

- By end user, hospital laboratories commanded 50.84% share of the microtomes market size in 2025, while pharmaceutical and biotechnology companies are increasing spending at a 7.03% CAGR.

- By geography, North America dominated with 42.18% share in 2025; Asia-Pacific is set to register a 7.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microtomes Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising global cancer burden Rising global cancer burden | +1.8% | Global, with highest impact in aging populations of North America and Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, with highest impact in aging populations of North America and Europe | Impact Timeline:Long term (≥ 4 years) |

Digital pathology adoption Digital pathology adoption | +1.2% | North America & EU leading, APAC rapid adoption | Medium term (2-4 years) | |||

Advances in automated microtomy Advances in automated microtomy | +0.9% | Global, concentrated in developed markets initially | Medium term (2-4 years) | |||

Histopathology lab expansion in APAC Histopathology lab expansion in APAC | +1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) | |||

Demand for 3-D tissue & spatial-omics sectioning Demand for 3-D tissue & spatial-omics sectioning | +0.7% | North America & EU research institutions | Short term (≤ 2 years) | |||

Microtome use in material-science & battery R&D Microtome use in material-science & battery R&D | +0.3% | Global, concentrated in technology hubs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Global Cancer Burden

New oncologic cases are projected to climb 75% by 2050 versus 2022, intensifying demand for precise sectioning equipment that supports advanced biomarker testing. Prostate cancer studies that employ multiplex immunohistochemistry have reported sensitivities above 99%, a performance that hinges on uniform tissue slices. Whole-mount techniques are also expanding because they improve tumor volume estimation and link imaging to pathology, further raising microtome utilization.

Digital Pathology Adoption

The United States Food and Drug Administration has cleared several whole-slide imaging systems for primary diagnosis, signaling regulatory confidence in digital workflows. Vendors such as Leica Biosystems and Indica Labs are integrating slide scanners with AI software, which in turn demands thin, scratch-free sections from modern automated microtomes. Laboratories pursuing full digital conversion report that image-based decisions now influence nearly 70% of therapeutic choices, placing sectioning quality at the center of diagnostic integrity.

Advances in Automated Microtomy

Systems like the Leica UC Enuity bring automated knife and sample alignment that produces repeatable sub-micron cuts while reducing operator skill requirements. Nanopolished blade edges have been shown to lower tissue trauma and support faster downstream staining. Automation directly counters staffing gaps; the American Society for Clinical Pathology registered an 18% vacancy rate in core labs in 2024.

Histopathology Lab Expansion in APAC

China’s medical-equipment sector has grown 15% per year, a rate well above global averages, buoyed by policies that foster domestic production and larger oncology screening programs.[1]Tong Wu, “China Medical Device Growth Outlook,” Dove Press, dovepress.com Pandemic-era supply shocks pushed regional labs to adopt automated microtomes that preserve quality despite limited staffing. India, Indonesia, and Vietnam show similar trajectories as they fast-track cancer screening and digital records, positioning the microtomes market for sustained demand across the region.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of skilled histotechnologists Shortage of skilled histotechnologists | -1.4% | Global, particularly acute in developed markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, particularly acute in developed markets | Impact Timeline:Long term (≥ 4 years) |

High cost of advanced systems High cost of advanced systems | -0.8% | Emerging markets primarily, budget-constrained institutions | Medium term (2-4 years) | |||

Supply-chain risk for precision blades Supply-chain risk for precision blades | -0.6% | Global, concentrated in regions dependent on single suppliers | Short term (≤ 2 years) | |||

Substitution by laser micro-dissection systems Substitution by laser micro-dissection systems | -0.4% | North America & EU research institutions primarily | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Skilled Histotechnologists

Worldwide there are only 14 pathologists per million population, with Africa averaging fewer than 3, limiting throughput in many laboratories.[2]Clare Verrill, “Global Pathologist Shortages,” The Pathologist, thepathologist.com In the United Kingdom, just 3% of pathology departments report full staffing, forcing facilities to lower certification standards and accept longer turnaround times. While automation eases daily workloads, complex cases still need expert oversight, constraining the microtomes market when professionals are unavailable.

High Cost of Advanced Systems

Premium automated microtomes can require capital outlays that smaller clinics cannot absorb, especially as supply-chain expenses have risen to as much as 20% of device revenue for manufacturers.[3]NRI Digital, “Medical Device Supply-Chain Cost Trends,” medicaltechnology.nridigital.com Leasing models and pay-per-use agreements are emerging but remain uncommon in lower-income regions. Consequently, some institutions delay upgrades, slowing penetration even as total-cost-of-ownership studies show labor savings often recoup initial spend within three years.

Segment Analysis

By Product: Instruments Lead Despite Accessories Growth Acceleration

Instruments held 67.42% of microtomes market share in 2025, underlining their prevalence in clinical histology. Rotary systems dominate routine cases, while laser and vibrating variants meet specialist demands for thicker neuroscience slices or ultra-thin research cuts. Accessories, notably disposable blades and specimen holders, are growing at a 6.73% CAGR as laboratories look for consistent performance and lower injury risk. Innovations in nanopolished steel and diamond coatings explain much of this accessories acceleration. Many regional suppliers are localizing blade manufacturing to counter shipping bottlenecks and steady the microtomes market.

Early adoption of accessories with RFID-enabled tracking also supports traceability mandates in regulated settings. Although accessories account for a smaller revenue base today, their high replacement frequency means recurring sales that buttress supplier margins. As automation rises, consumable-smart microtomes that alert technicians to blade-life parameters are being piloted, a development expected to lock in accessory demand through proprietary ecosystems.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Manual Systems Dominate While Automation Accelerates

Manual platforms captured 52.56% of microtomes market share in 2025 because they cost less and give experienced technicians tactile feedback that remains useful for atypical specimens. However, fully automated models are expanding at 7.22% CAGR as hospitals adopt lean staffing models. Automated devices, integrating stepper-motor drives and onboard diagnostics, consistently yield slices under 4 µm, a quality threshold recommended for digital scanning.

Semi-automated units provide a bridge solution, offering motorized trimming yet retaining manual advance for delicate tissues, thereby accommodating budget-sensitive buyers. As cloud-based laboratory information systems mature, vendors are bundling predictive-maintenance dashboards, enabling labs to schedule servicing around workload peaks. This connectivity is forecast to keep the microtomes market on its automation trajectory without fully displacing legacy equipment in low-volume settings.

By End User: Hospitals Lead While Pharma Companies Accelerate

Hospital laboratories represented 50.84% of the microtomes market size in 2025 due to their direct role in patient care. Nonetheless, pharmaceutical and biotechnology firms are the fastest-expanding customers, with 7.03% CAGR linked to surging biomarker and companion-diagnostic pipelines. Contract research organizations that service these firms increasingly specify automated microtomes to guarantee reproducible GLP-compliant sections across multicenter trials.

Independent clinical labs also hold a sizable share as they absorb overflow testing from community hospitals. Their growth prospects hinge on adopting automation to offset wage inflation and to meet same-day reporting contracts. Academic centers and government institutes continue to push the boundaries of microtome functionality by sectioning composite materials and battery electrodes, widening the scope of the microtomes market beyond life sciences.

Note: Segment shares of all individual segments available upon report purchase

By Application: Disease Diagnostics Dominates While Digital Pathology Surges

Disease diagnostics accounted for 64.22% of the microtomes market size in 2025, reflecting the indispensable role of sectioning in cancer workflows. Oncology specimens, particularly breast and prostate tissues, depend on high-integrity slices for multiplex staining that guides therapy selection. Elsewhere, 3-D omics technologies are emerging, prompting demand for instruments capable of controlled serial sectioning at micron-level intervals.

Digital pathology, rising at 7.3% CAGR, relies on consistent section flatness and uniform thickness to avoid scan artifacts. Laboratories moving to remote sign-out models stipulate automated sectioners that cut, track, and transmit QC data directly into slide scanners, creating a virtuous cycle that reinforces purchasing of high-end systems. Pre-clinical drug safety teams also leverage automated microtomes to process large animal cohorts, underscoring the equipment’s relevance beyond core pathology.

Geography Analysis

North America led with 42.18% revenue in 2025, propelled by large cancer-screening volumes, high per-capita health spending, and early uptake of digital pathology. Federal reimbursement schemes support capital investment, and domestic blade manufacturing mitigates shipping delays. Europe exhibits steady but slower growth; its aging population and universal coverage sustain demand, yet shortages of histotechnologists limit daily throughput in several countries.

Asia-Pacific is advancing at a 7.7% CAGR as China, India, and Southeast Asia expand pathology networks to detect non-communicable diseases earlier. Government incentives for local medical-device production are fostering regional players, particularly in precision blades, thereby lowering total cost of ownership and broadening the buyer base. Japan and South Korea contribute incremental gains through high-end research applications such as spatial-omics, while Australia functions as a regional referral hub for complex oncologic diagnostics.

Latin America and the Middle East–Africa are still nascent but present upside as private hospital chains invest in modern laboratories. Political instability and currency volatility can slow procurement, yet multilateral cancer-control programs are gradually improving funding visibility. Suppliers who offer modular upgrades and financing plans are well-positioned to capture early adopters in these frontier markets, further diversifying the global microtomes market.

Competitive Landscape

Market Concentration

Competition is moderate, with major players prompting a steady pace of incremental innovation rather than price wars. Leica Biosystems has extended its suite through an AI partnership that marries Aperio scanners to HALO AP analytics, creating an end-to-end pathway from sectioning to diagnosis. Thermo Fisher Scientific is investing USD 2 billion in U.S. production to strengthen domestic supply for blades and consumables. Sakura Finetek continues to refine its Tissue-Tek line with ergonomic designs that reduce repetitive-strain injuries.

Emerging manufacturers are exploiting niches such as cryogenic sectioning for regenerative medicine, while start-ups pursue smart microtomes that adjust cutting force in real time via machine-vision feedback. Supply-chain resilience has become a differentiator; firms are dual-sourcing tungsten and diamond raw materials to reduce lead times. Meanwhile, service models are shifting toward multi-year uptime guarantees bolstered by IoT sensors that forecast part failures weeks in advance.

White-space opportunities include non-biological applications in semiconductor cross-sectioning and lithium-ion battery research, fields that demand ultra-clean slicing within inert environments. Vendors able to transfer histology know-how to these segments can open new revenue pools without cannibalizing core medical demand, strengthening the long-term outlook for the microtomes market.

Global Microtomes Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The European Society of Pathology issued digital-workflow guidelines emphasizing microtome calibration as critical for producing homogeneous sections ready for whole-slide imaging.

- March 2024: Leica Microsystems unveiled the UC Enuity ultramicrotome featuring automated knife alignment and modular upgrades to aid both novice and expert users.

- October 2023: Leica Microsystems opened a USD 60 million manufacturing complex in Singapore, expanding capacity for advanced microtome production.

- January 2023: A Journal of Biological Engineering study documented increased adoption of vibrating microtomes for tissue-slice assays, citing superior preservation of cellular architecture.

Table of Contents for Global Microtomes Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising global cancer burden

- 4.2.2Digital pathology adoption

- 4.2.3Advances in automated microtomy

- 4.2.4Histopathology lab expansion in APAC

- 4.2.5Demand for 3-D tissue & spatial-omics sectioning

- 4.2.6Microtome use in material-science & battery R&D

- 4.3Market Restraints

- 4.3.1Shortage of skilled histotechnologists

- 4.3.2High cost of advanced systems

- 4.3.3Supply-chain risk for precision blades

- 4.3.4Substitution by laser micro-dissection systems

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product

- 5.1.1Instruments

- 5.1.1.1Rotary Microtomes

- 5.1.1.2Vibrating Microtomes

- 5.1.1.3Laser Microtomes

- 5.1.1.4Sliding/Sledge Microtomes

- 5.1.1.5Other Instruments

- 5.1.2Accessories

- 5.2By Technology

- 5.2.1Manual Microtomes

- 5.2.2Semi-automated Microtomes

- 5.2.3Fully Automated Microtomes

- 5.3By Application

- 5.3.1Disease Diagnostics – Histopathology

- 5.3.2Digital Pathology & Whole-Slide Imaging

- 5.3.3Drug Discovery & Pre-clinical Testing

- 5.3.4Others

- 5.4By End User

- 5.4.1Hospital Laboratories

- 5.4.2Independent Clinical Laboratories

- 5.4.3Pharmaceutical & Biotechnology Companies

- 5.4.4Contract Research Organisations (CROs)

- 5.4.5Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Thermo Fisher Scientific Inc.

- 6.3.2Leica Biosystems Nussloch GmbH (Danaher Corporation)

- 6.3.3Sakura Finetek

- 6.3.4SLEE medical GmbH

- 6.3.5MEDITE Medical GmbH

- 6.3.6Histo-Line Laboratories

- 6.3.7Amos Scientific Pty Ltd

- 6.3.8Boeckeler Instruments Inc.

- 6.3.9Diapath SpA

- 6.3.10Cardinal Health

- 6.3.11Epredia (PHC Holdings)

- 6.3.12Bright Instrument Co. Ltd

- 6.3.13Erma Inc.

- 6.3.14microTec Laborgeräte GmbH

- 6.3.15Especialidades Médicas MYR, S.L.

- 6.3.16Jinhua Yidi Medical Appliance Co.,Ltd.

- 6.3.17Zhejiang Jinhua kedi Instrumental Equipment Co. Ltd (JINHUA KEDI)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Microtomes Market Report Scope

As per the scope of the report, a microtome is a device used to cut thin sections of tissues for microscopic examination, and the process is known as microtomy. The cut tissue, usually of 2 to 10-micrometer thickness, is further processed for observation under a microscope. The microtomes market is segmented by product, technology, end user, and geography. The product segment is divided into instruments and accessories. The technology segment is further segmented into manual microtomes and automated microtomes. The end-user segment includes hospital laboratories, clinical laboratories, pharmaceutical and biotechnology companies, and other end-users. The geography segment is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.