Microsurgical Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

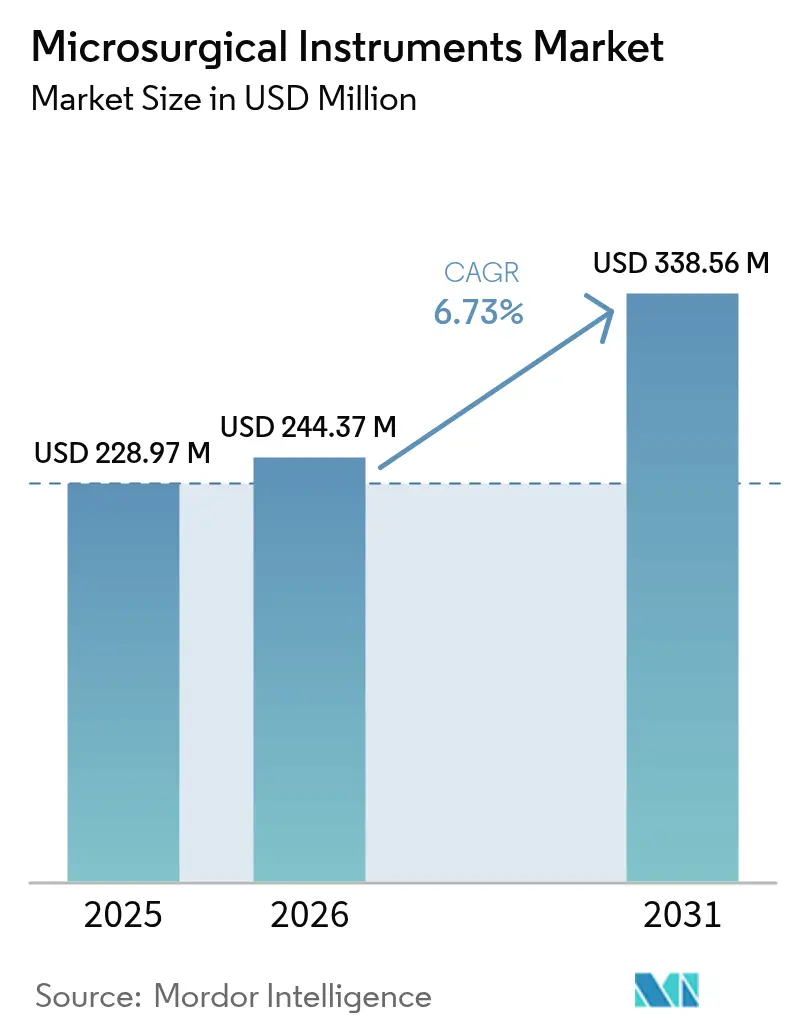

| Market Size (2026) | USD 244.37 Million |

| Market Size (2031) | USD 338.56 Million |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

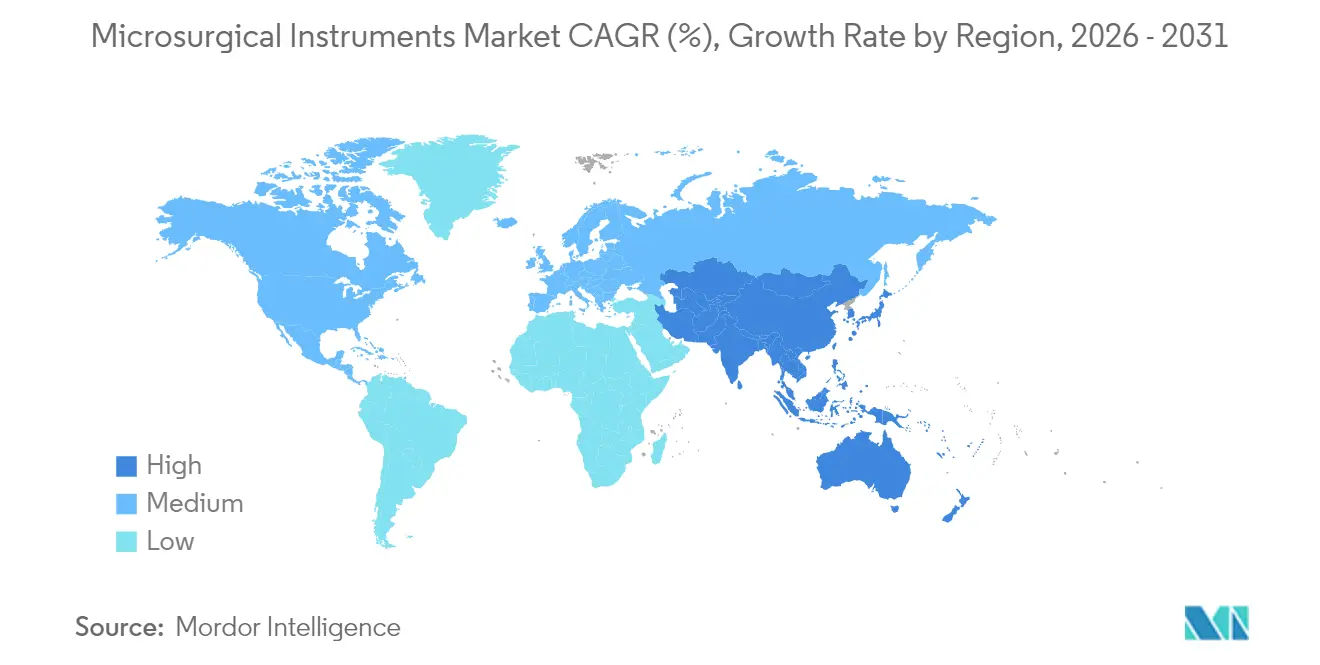

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microsurgical Instruments Market Analysis by Mordor Intelligence

The Microsurgical Instruments Market size was valued at USD 228.97 million in 2025 and is estimated to grow from USD 244.37 million in 2026 to reach USD 338.56 million by 2031, at a CAGR of 6.73% during the forecast period (2026-2031).

Escalating uptake of precision-based surgical techniques, rapid integration of 4K/3D digital microscopy, and rising volumes of chronic-disease-related interventions continue to expand demand for highly specialized instruments. Hospitals and teaching centers continue to refresh capital equipment fleets with AI-enabled operating microscopes, while ambulatory surgical centers lean on compact, workflow-oriented sets to migrate complex cases to outpatient settings. The competitive field shows purposeful R&D spending on ergonomic designs, bio-resorbable micro-suture materials, and voice-controlled visualization units to differentiate offerings. Manufacturers must, however, maneuver through stringent Class III approval pathways, making early engagement with regulators and risk-sharing partnerships with providers vital to sustaining innovation momentum.

Key Report Takeaways

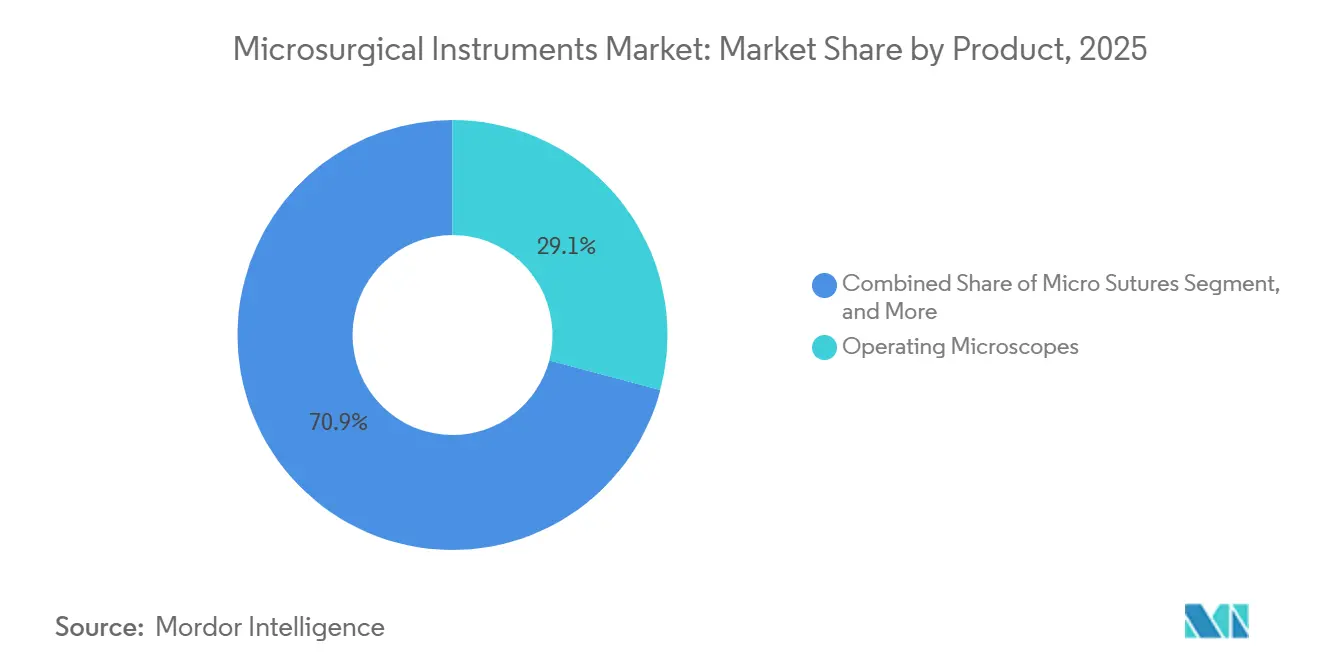

- By product category, Operating Microscopes led with 29.12% of microsurgical instruments market share in 2025; micro sutures are projected to expand at an 8.92% CAGR through 2031.

- By microsurgery type, ophthalmic procedures accounted for 30.05% of the microsurgical instruments market in 2025, while orthopedic microsurgery is poised to grow at a 9.88% CAGR through 2031.

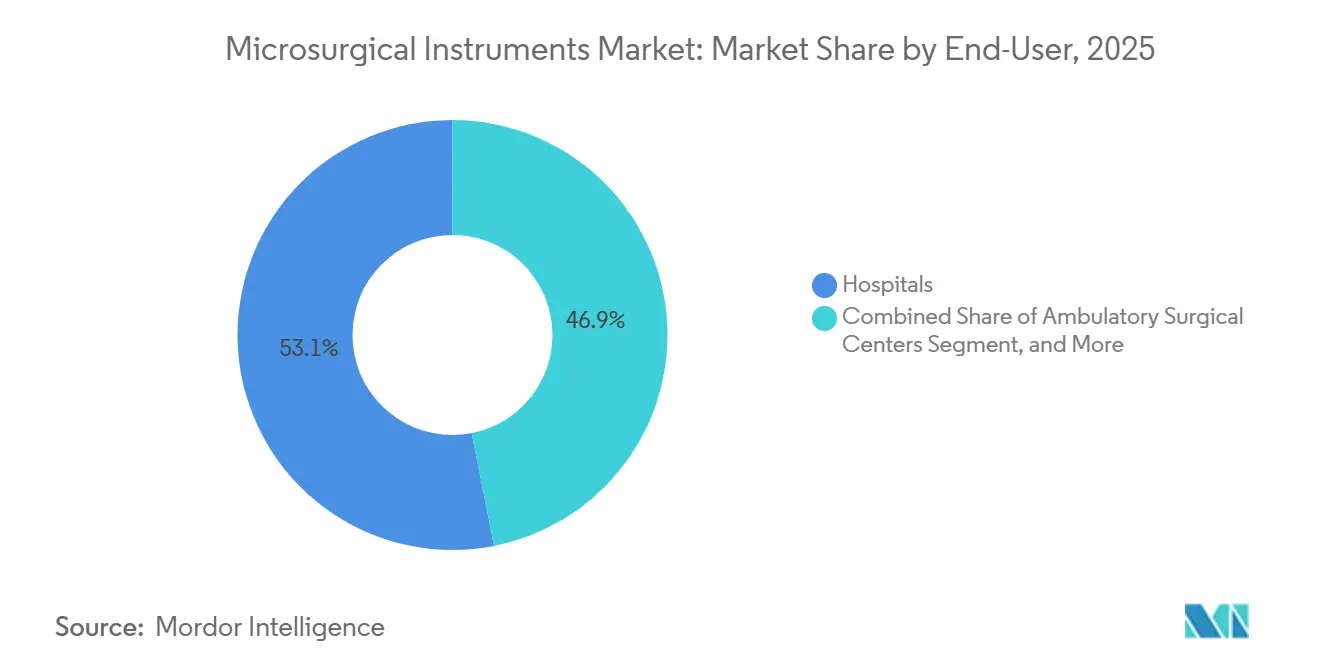

- By end user, hospitals accounted for 53.10% of revenue in 2025; ambulatory surgical centers posted the fastest growth at a 7.98% CAGR.

- By geography, North America accounted for 38.25% of revenue in 2025; Asia-Pacific is forecast to grow at a 9.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Microsurgical Instruments Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Microsurgery advantage over conventional surgery | +1.2% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Rising surgical volumes and chronic disease incidence | +1.5% | Global, concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Technological advances in digital microscopes and robotics | +1.8% | North America and European Union lead, Asia-Pacific catching up | Short term (≤ 2 years) |

| Growing demand for minimally invasive procedures | +1.3% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| 4K/3D OR integration accelerating micro-instrument upgrades | +0.9% | North America, Western Europe, select Asia-Pacific metros | Short term (≤ 2 years) |

| Emergence of bio-resorbable micro-sutures | +0.6% | North America and EU, limited penetration in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Microsurgery Advantage Over Conventional Surgery

Microsurgical procedures are increasingly being reimbursed at premium rates due to their superior outcomes in nerve repair and lymphatic reconstruction. In 2024, U.S. academic centers reported a 95% success rate for free-flap breast reconstruction, significantly surpassing the 78% success rate for pedicled flaps. However, a bottleneck persists in fellowship capacity, with only 180 accredited microsurgery training slots available in the U.S. in 2024. To address this limitation, equipment suppliers are investing in simulation modules to expedite skill acquisition and expand the pool of trained professionals. This increase in skilled practitioners is driving higher demand for essential tools such as microscopes, clamps, and sutures.

Rising Surgical Volumes and Chronic Disease Incidence

Population aging and the global diabetes burden underpin rising procedure counts, ensuring multi-year growth for the microsurgical instruments market. China’s health expenditure outlook of USD 33.4 trillion by 2060 signals large equipment pools across tertiary centers.[1]BMC Health Services Research, “Forecast of Total Health Expenditure on China’s Ageing Population,” biomedcentral.com Diabetic retinopathy drives a high baseline of retinal microsurgery, while coronary artery bypass and tumor resections require nerve-sparing precision that legacy tools cannot deliver. Governments in Asia allocate procurement budgets for ophthalmic and cardiovascular suites, creating attractive bulk-purchase opportunities. Western systems, although mature, still see growth from revision surgeries and longer life expectancy. Device makers respond by tailoring starter kits that bundle microscopes, forceps, and bio-resorbable sutures to lower adoption friction in mid-tier facilities.

Technological Advances in Digital Microscopes and Robotics

Next-generation visualization, force-feedback robotic arms, and AI-driven image recognition raise the performance ceiling for complex procedures, deepening penetration of the microsurgical instruments market. Intuitive Surgical’s da Vinci 5 force-feedback module cuts tissue stress by 43% while easing novice suturing skills acquisition. Hyperspectral imaging, able to reveal sub-surface vascularity, guides neurosurgeons around the eloquent cortex and reduces postoperative deficits. Vendors embed 4K sensors and cloud-linked analytics to auto-document key procedural steps, supporting audit trails and continuous learning loops. Early adopters in North America generate peer-reviewed datasets that accelerate broader reimbursement approvals. Supply chains integrate modular upgrades so existing systems can receive software enhancements without complete hardware replacement, controlling lifecycle costs for providers.

Growing Demand for Minimally Invasive Procedures

Patients and payers favor minimally invasive routes that reduce scarring, shorten stays, and lower infection risk, driving new-case volume in the microsurgical instruments market. Endoluminal robotic systems enter through natural orifices, eliminating large incisions and broadening indications previously considered too morbid.[3]Noah Medical, “2025 Predictions in Healthcare: The Rise of Endoluminal Robotics,” noahmed.com Academic centers deploy the Symani system for delicate flap reconstructions, demonstrating suture diameters of 40 µm now possible in outpatient theatres.[2]American Hospital Association, “3 Ways Robotic Surgery Is Changing Health Care This Year,” aha.org Virtuoso Surgical advanced needle-sized manipulators into the first-in-human bladder tumor removal, showcasing en bloc resection in anatomically confined spaces. These successes spark payer inclusion of additional CPT codes, encouraging equipment acquisitions at ASCs where procedure mix upgrades raise operating margins. Training programs adapt simulation modules to expand the pool of surgeons proficient in ultra-fine instrument handling.

Restraints Impact Analysis of Microsurgical Instruments Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of advanced microsurgical systems | −1.4% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Stringent device-approval pathways (Class III) | −0.8% | North America and EU | Short term (≤ 2 years) |

| Shortage of trained microsurgeons in emerging markets | −1.1% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Budget shift toward robotic platforms cannibalizing manual sets | −0.9% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Microsurgical Systems

Premium robotic microscopes command list prices exceeding USD 1 million, while maintenance contracts and sterile consumables can double ten-year ownership costs. Emerging-market hospitals divert limited capital toward essential imaging or ICU beds, leaving microsurgical upgrades on deferred wish lists. Smaller North American community facilities also weigh volume thresholds before committing to complete suites, opting instead for refurbished units that offer limited functionality. Vendors counteract sticker shock with pay-per-use leasing, profit-sharing models, and modular build-outs that start with core optics, then add robotic arms later. Government procurement grants tied to quality-of-care targets partially offset capex barriers, yet parity with lower-cost manual sets may take additional cycles.

Stringent Device-Approval Pathways (Class III)

The FDA’s PMA process demands rigorous clinical evidence, submission fees, and multi-year timelines that elongate return-on-investment horizons for microsurgical innovators. Similar hurdles appear in Europe’s MDR and Japan’s Pharmaceutical and Medical Device Act, causing “device lag” between first-in-class launches and global rollouts. Start-ups must allocate scarce funds to regulatory consultants and large-animal trials before human deployment, often prompting partnerships with larger strategics to support dossiers. While high standards safeguard patients, they slow iterative releases, meaning surgeons may rely on older models longer. Companies increasingly design clinical protocols with global harmonization in mind, streamlining evidence packages to satisfy multiple authorities concurrently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Microsurgical Instruments Market Segment Analysis

By Product:

Recurring Consumables Overtake Capital EquipmentIn 2025, operating microscopes contributed 29.12% of total revenue, reflecting a strong return on initial program investments. At the same time, micro sutures are projected to grow the fastest, with an anticipated CAGR of 8.92% through 2031. Driven by increasing demand for high-volume reconstructive and pediatric cases, the microsuture market is expected to grow by the end of the forecast period.

Consumable economics remain a critical factor; for example, a single free-flap reconstruction may require up to 15 units of premium sutures, each priced at USD 150. Meanwhile, micro forceps and scissors face significant commoditization pressures, with ISO-certified Chinese exports offering prices up to 60% lower than Western brands. Digital advancements are enhancing capabilities and extending the life cycles of microscopes. For instance, ZEISS’s MICOR 700 utilizes augmented-reality overlays to justify premium pricing. Manufacturers that effectively integrate hardware offerings with subscription-based consumables are well-positioned to secure consistent revenue streams in the evolving microsurgical instrument market.

By Microsurgery Type:

Orthopedics Becomes the New Growth EngineOphthalmic procedures dominated revenue, with a 30.05% microsurgical instruments market share in 2025, and accounted for USD 68.79 million of the microsurgical instruments market size during 2025. Continuous cataract case flow, coupled with complex retinal detachment repairs, anchors volume in mature economies and in fast-growing Asian ophthalmology chains. The procedural baseline makes eye surgery a bellwether for next-gen instrument acceptance; 3D heads-up displays migrated from retina suites into corneal transplant and glaucoma units within two years of launch.

Orthopedic microsurgery, advancing at a 9.88% CAGR, leverages high-resolution imaging and ultra-thin saw blades to perform ligament reconstructions with millimeter precision, reducing revision rates. Peripheral nerve transfers, once confined to academic centers, move into community hospitals as standardized kits arrive. Plastic & Reconstructive teams deploy super-microsurgical tools to revascularize free flaps with diameters as small as 0.8 mm, shortening ischemia time and driving adoption of automated coupler devices. ENT, neurological, and urological specialties are tapping similar advancements, each reinforcing supplier incentive to maintain robust multi-specialty support programs that expand total addressable revenue.

By End-User:

Ambulatory Surgical Centers Accelerate AdoptionHospitals captured 53.10% revenue in 2025, equating to USD 121.55 million of the microsurgical instruments market size in 2025, reflecting their role as referral hubs for high-acuity cases that demand multidisciplinary resources. Academic medical centers, which often act as early adopters, influence regional purchasing norms and set clinical benchmarks that ripple into surrounding community hospitals.

Yet Ambulatory Surgical Centers register the fastest expansion at 7.98% CAGR as minimally-invasive techniques enable complex cases such as shoulder arthroplasty and peripheral nerve decompressions to shift to outpatient pathways. Lower facility fees, same-day discharge, and streamlined staffing models create compelling economics for payers and patients alike. Specialty Clinics focus on high-volume aesthetics, ophthalmology, or fertility preservation and differentiate by offering concierge-level recovery packages that integrate microsurgical precision for superior cosmetic outcomes. Research institutes, while contributing modest revenue, punch above their weight in shaping technique evolution and validating prototypes that later achieve mainstream commercialization.

Geography Analysis

North America Microsurgical Instruments Market

North America generated 38.25% of 2025 revenue, supported by entrenched OR digitization and favorable reimbursement that covers high-ticket visualization platforms. Regional teaching alliances, such as Cleveland Clinic’s collaboration with optics manufacturers, pilot augmented-reality guidance that feeds directly into procurement pathways across affiliated hospitals. Site-of-service migration continues unabated; ASCs now execute more than 60% of rotator cuff repairs, ensuring replacement demand for compact microscopes and single-use suture cartridges. The microsurgical instruments market maintains pricing power here due to value-based contracting, where lower readmission rates secure bonus payments that offset premium device costs.

Europe Microsurgical Instruments Market

Europe remains the second-largest buyer pool, with strong adoption in Germany, France, and the Nordics. The region leans on rigorous surgeon credentialing and centralized tender frameworks that prioritize lifecycle cost, pushing vendors to extend warranty periods and offer predictive maintenance packages. EU MDR compliance expenses elevate barriers for new entrants, indirectly protecting incumbent share. Growth, however, is more tempered at mid-single-digit rates as austerity constraints linger in Southern Europe. That drag is partially offset by expanding private hospital networks in Poland and the Czech Republic, which often emulate German standards and thus purchase top-tier microscopes.

APAC Microsurgical Instruments Market

Asia-Pacific posts the highest CAGR at 9.14%, buoyed by rapid healthcare infrastructure expansion in China and India. Government initiatives such as China’s Healthy China 2030 blueprint and India’s Ayushman Bharat insurance scheme enlarge addressable patient pools. Chinese class-III medical zones grant tax incentives for local device assembly, enabling foreign brands to shorten lead times and capture provincial tenders. Rising middle-class expectations accelerate penetrative depth in cataract and refractive surgery, bolstering ophthalmic instrument imports. Local start-ups, often staffed by returnee engineers, collaborate with tertiary hospitals to co-develop cost-effective microscopes, injecting competitive pressure yet broadening overall adoption. Japan and South Korea, mature but aging societies, drive replacement sales as facilities swap first-generation digital scopes for robotics-ready variants, preserving regional unit shipment volume.

Competitive Landscape

Competition is moderate, with top suppliers controlling a meaningful but not overwhelming share, ensuring active jostling for hospital preference cards. Carl Zeiss Meditec fortifies its leadership with the launch of KINEVO 900 S, featuring depth-tracking autofocus and a surgeon-controlled robotic arm. This package binds optics, software, and disposables into a single recurring-revenue ecosystem. Olympus Corporation leverages its endoscopy dominance to upsell integrated hybrid suites that seamlessly allow microscopes to switch to flexible scopes for multi-quadrant ENT cases. Stryker pushes ergonomics, introducing lighter titanium micro-forceps that reduce surgeon thumb strain during multi-hour flap anastomoses, while bundling them with its 1688 4K platform for cohesive imaging.

M&A activity continues to reshape portfolios. Medtronic’s 2024 acquisition of Fortimedix added articulating micro-graspers and clip appliers that slot neatly into Medtronic’s robotic pipeline, creating a comprehensive offering from access to closure. Teleflex’s 2025 purchase of BIOTRONIK’s vascular intervention line injects drug-eluting balloon know-how that synergizes with its micro-catheter range, broadening cross-selling depth in complex bypass graft procedures. Strategic alliances also bloom; Leica Microsystems aligns with AR software firms to overlay perfusion maps atop live surgical fields, differentiating against pure hardware competitors.

Emerging challengers focus on niche pain points. Virtuoso Surgical’s needle-sized manipulators disrupt bladder oncology by delivering delicate traction within confined lumens, illustrating how micro-robotics can open previously untapped segments. Start-ups in Israel and Singapore prototype smart sutures with in-line impedance sensors that alert clinicians to early dehiscence, foreshadowing a future where consumables feed data into hospital EMRs. Medium-sized European firms are trialing eco-friendly sterilization trays to meet growing sustainability mandates. Collectively, these moves ensure the microsurgical instruments market remains dynamic, rewarding incumbents that rapidly iterate and punishing those who rely solely on installed base inertia.

Microsurgical Instruments Industry Leaders

Olympus Corporation

KLS Martin Group

Global Surgical Corporation

ZEISS International

Karl Kaps GmbH

- *Disclaimer: Major Players sorted in no particular order

Microsurgical Instruments Market Companies Covered in this Report

- Alcon

- B. Braun

- Baxter

- Beaver-Visitec International, Inc.

- Danaher

- Global Surgical

- HAAG-Streit

- Integra LifeSciences

- Johnson & Johnson Services, Inc. (Ethicon)

- Karl Kaps

- Karl Storz SE

- KLS Martin Group

- Danaher

- Medical Microinstruments SpA

- Medtronic

- MicroSure BV

- Microsurgery Instruments Inc.

- Olympus

- Scanlan International

- Stille

- Stryker

- Teleflex

- Virtuoso Surgical Inc.

- Carl Zeiss

Recent Industry Developments in Microsurgical Instruments Market

- February 2026: ZEISS Medical Technology won NMPA approval for its ARTEVO 750 and ARTEVO 850 ophthalmic microscopes in China, adding RGB illumination and workflow integration.

- January 2026: AROSurgical Instruments celebrated its 40-year anniversary, launching a credibility campaign focused on supply reliability.

- December 2025: Medical Microinstruments secured FDA 510(k) clearance for its NanoWrist scissors and forceps, expanding Symani’s indication set.

Microsurgical Instruments Market Report Scope and Research Methodology

Market Definition and Coverage

Our study views the microsurgical instruments market as revenue derived from precision hand-held tools, micro forceps, micro scissors, micro sutures, needle holders, vessel clamps, and allied accessories used under an operating microscope to perform sub-millimeter procedures in ophthalmology, neurology, plastic-reconstructive, ENT, and orthopedic settings. Devices whose primary purpose is optical visualization rather than tissue manipulation are considered complementary, not core, to this market and are treated separately within Mordor Intelligence's broader surgical equipment framework.

Scope exclusion: powered robotic workstations and stand-alone operating microscopes fall outside our sizing universe.

Segments Covered in This Report

- By Product

- Micro Sutures

- Micro Forceps

- Operating Microscopes

- Micro Scissors

- Micro Needle Holders

- Micro Vessel Clamps

- Other Instruments

- By Microsurgery Type

- Orthopedic

- Ophthalmic

- Plastic & Reconstructive

- ENT

- Neurological

- Gynecological & Urological

- Other Types

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed practicing microsurgeons, peri-operative nurses, and instrument distributors across North America, Europe, India, and Japan. These discussions clarified kit replacement rates, titanium versus stainless adoption, and average selling price progression, enabling us to sharpen preliminary desk findings and close data gaps before final triangulation.

Desk Research

We compiled foundational data from open sources such as the US FDA 510(k) database, Eurostat trade codes for HS-901890, Japanese PMDA approvals, and clinical-procedure registries from the American Academy of Ophthalmology and the International Society of Plastic Surgeons. Company 10-Ks, Medicare outpatient claims, and selective insights from paid platforms including D&B Hoovers and Dow Jones Factiva enriched competitive and pricing intelligence. Numerous additional public-domain articles and association white papers were also reviewed to confirm trends and volumetrics; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build starts with annual procedure counts (e.g., cataract, free-flap transfers), applies instrument-per-case coefficients and replacement cycles, and is balanced through selected bottom-up checks such as sampled OEM revenues and channel audits. Key variables in our model include ophthalmic surgery volumes, neurosurgical microscope case growth, average reusable set lifespan, titanium raw-material costs, regulatory approval cadence, and hospital capital-budget trends. Multivariate regression on these drivers generates the 2025-2030 forecast, with scenario analysis used where volatility around input costs is high.

Data Validation & Update Cycle

Outputs undergo variance scans against independent shipment data and customs codes. Senior reviewers challenge anomalies, and any material market event triggers interim refresh ahead of the annual update. A final analyst pass precedes delivery, ensuring clients receive the latest vetted view.

How Mordor Intelligence's Microsurgical Instruments Market Size Compares to Other Published Estimates

Published figures often diverge because firms choose dissimilar scopes, price bases, and refresh rhythms. We focus strictly on hand-held precision tools, report manufacturer revenue at ex-factory level, and refresh models each year, which keeps our baseline lean yet timely.

Key gap drivers include rivals bundling microscopes and robotic consoles into instrument revenue, using list prices rather than blended ASPs, or extrapolating unit sales from limited import datasets without procedure cross-checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 228.97 million (2025) | Mordor Intelligence | - |

| USD 2.65 billion (2024) | Global Consultancy A | Includes microscopes and robots; uses list prices |

| USD 2.20 billion (2024) | Trade Journal B | Aggregates all minimally-invasive kits; limited primary validation |

| USD 5.94 billion (2024) | Regional Consultancy C | Broad "microsurgery" scope spanning implants and disposables |

The comparison shows that once narrower scope, validated ASPs, and yearly refresh are applied, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current value of the microsurgical instruments market?

The market is valued at USD 244.37 million in 2026 and is set to rise to USD 338.56 million by 2031.

Which product segment leads revenue?

Operating Microscopes command the top spot with 29.12% microsurgical instruments market share in 2025.

Which region shows the fastest growth?

Asia-Pacific posts the highest forecast CAGR at 9.14% through 2031 due to large-scale healthcare investments and an expanding middle class.

Why are Ambulatory Surgical Centers important to future demand?

ASCs grow at 7.98% CAGR because minimally-invasive techniques allow complex cases to shift to cost-efficient outpatient settings, driving instrument purchases.

How do regulatory hurdles affect new product launches?

Class III approval pathways demand extensive clinical evidence, extending development timelines and increasing costs but ensuring patient safety.

Page last updated on: