Microplate Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

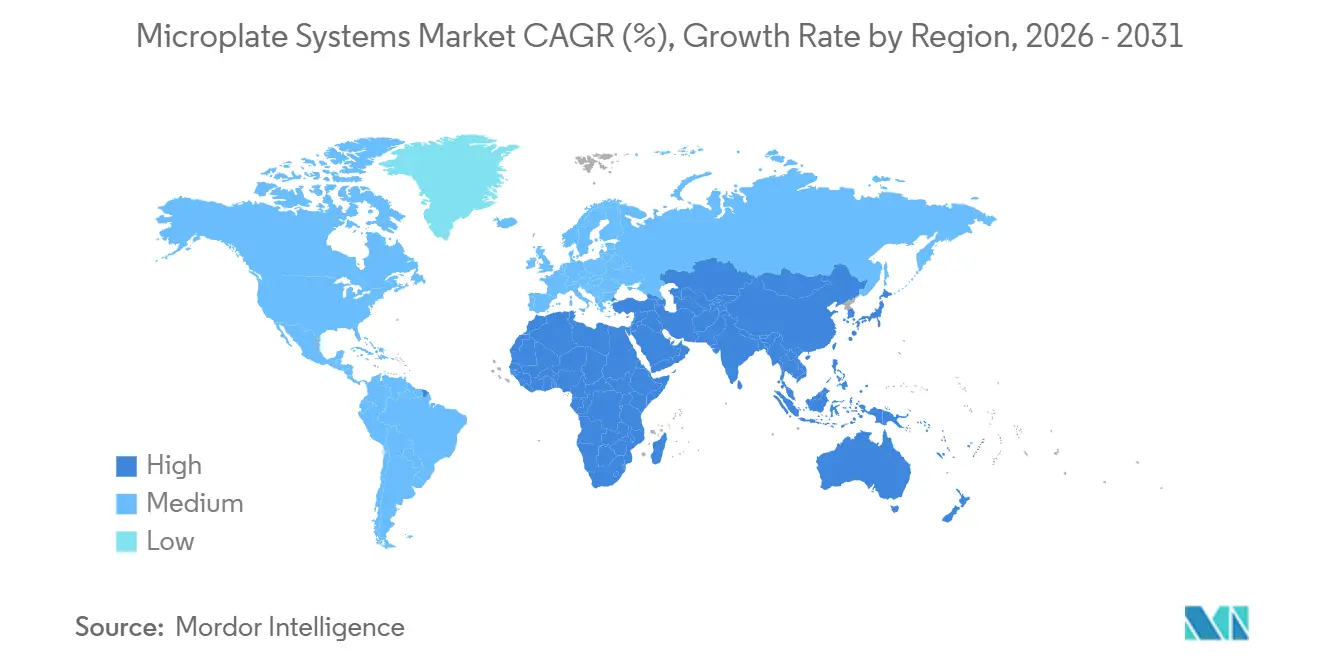

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microplate Systems Market Analysis by Mordor Intelligence

The Microplate Systems Market size is projected to expand from USD 1.21 billion in 2025 and USD 1.26 billion in 2026 to USD 1.59 billion by 2031, registering a CAGR of 4.73% between 2026 to 2031.

Sustained investment in high-throughput screening, demand for hybrid detection optics, and stronger public-sector funding underpin this steady climb. Laboratories are shifting from single-mode absorbance readers toward multi-mode platforms that integrate fluorescence, luminescence, and imaging, a pivot that compresses capital budgets while widening assay menus. Pharmaceutical companies favor these hybrid systems because they enable legacy ELISA workflows and next-generation phenotypic screens without hardware swaps, reducing validation overhead. Sovereign initiatives in precision medicine and the broader adoption of automated liquid handling are amplifying growth in Asia-Pacific, where sovereign funding is accelerating the installation of multi-mode readers. At the same time, sustainability mandates in the European Union and California push vendors to disclose energy-per-read metrics and offer take-back schemes for consumables, tilting procurement toward greener models.

Key Report Takeaways

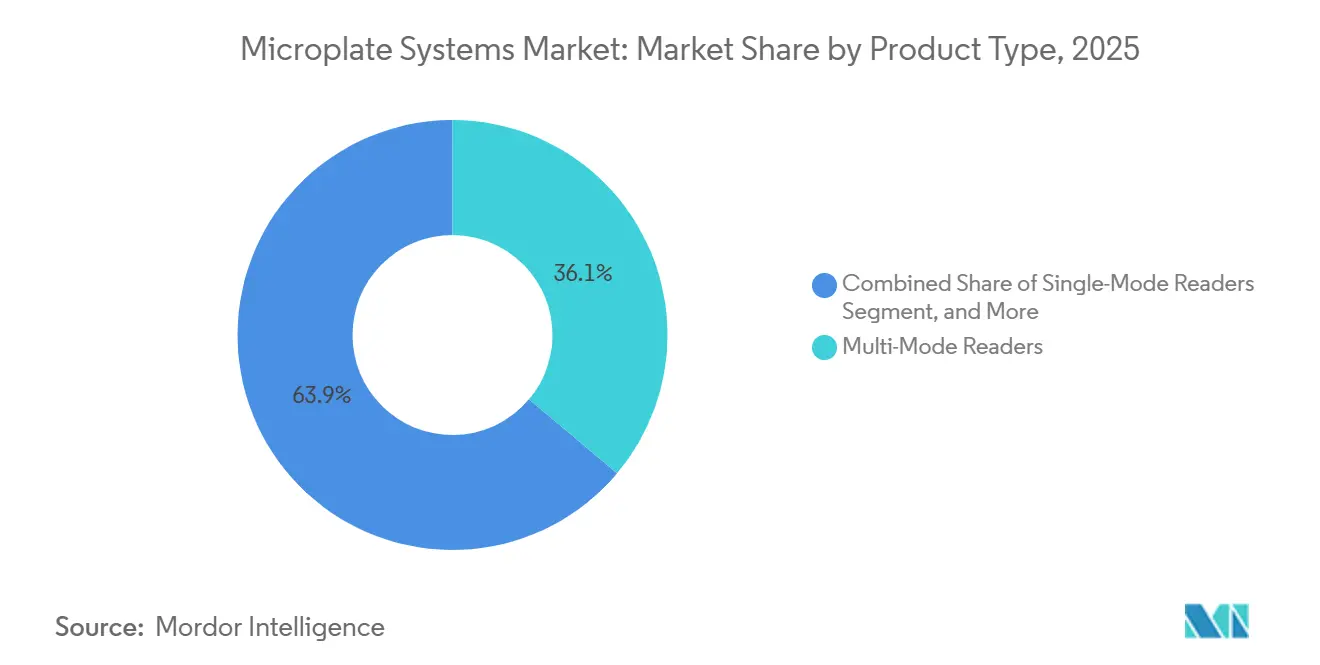

- By product type, multi-mode readers led with 36.12% of the microplate systems market share in 2025 and are advancing at a 6.06% CAGR through 2031.

- By application, drug discovery and high-throughput screening captured 47.09% of the microplate systems market size in 2025, while genomics and proteomics research is projected to expand at a 7.63% CAGR during 2026-2031.

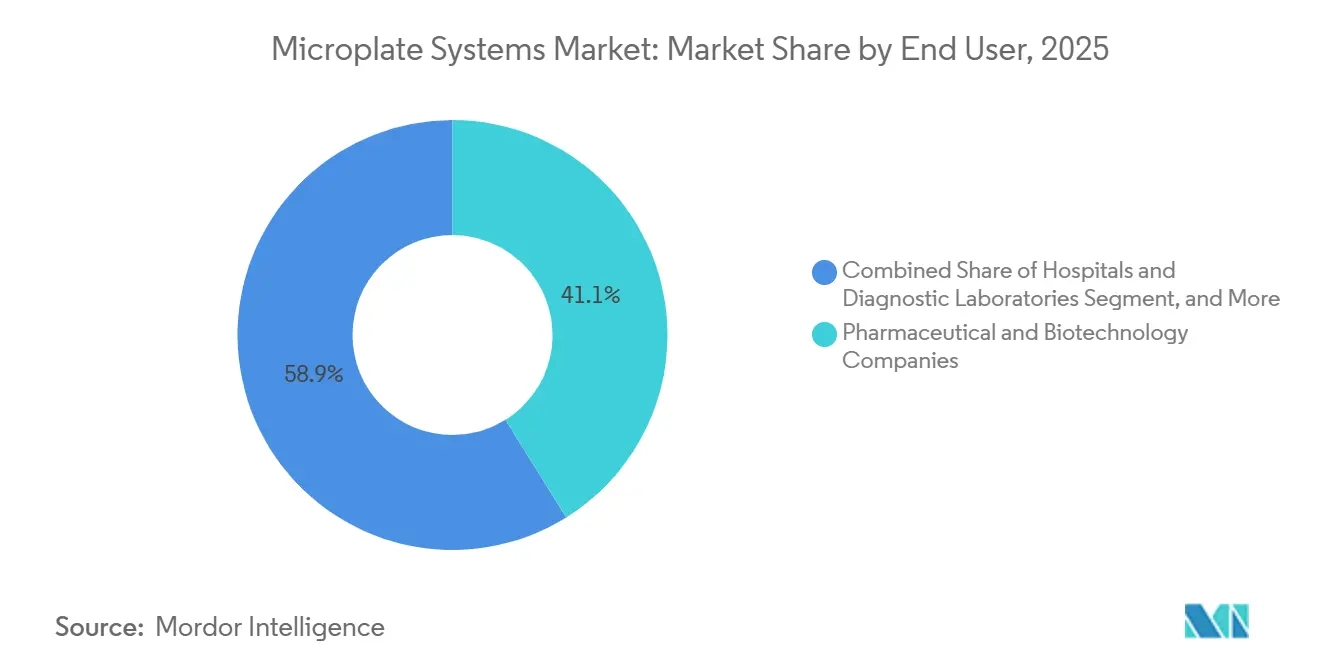

- By end user, pharmaceutical and biotechnology companies held 41.13% share of end-user spending in 2025; contract research and manufacturing organizations posted the fastest growth at 8.18% CAGR through 2031.

- By geography, North America commanded 38.29% 2025 sales, whereas Asia-Pacific is projected to post the strongest regional CAGR of 10.13% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microplate Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of High-Throughput Screening | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Automation & Multi-Mode Detection | +1.0% | Global, strongest in Asia-Pacific | Short term (≤2 years) |

| Expansion of Life-Sciences Research Funding | +0.8% | North America, Europe, China, India | Long term (≥4 years) |

| Technological Advances in Sensitivity & Throughput | +0.6% | Global | Medium term (2-4 years) |

| Emergence of AI-Integrated Real-Time Analytics | +0.7% | North America, Europe, early Asia-Pacific | Short term (≤2 years) |

| Sustainability Push for Energy-Efficient Instruments | +0.3% | European Union, California, Massachusetts | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of High-Throughput Screening in Drug Discovery

Pharmaceutical pipelines continue to migrate toward complex modalities such as antibody-drug conjugates and cell therapies that demand phenotypic assays screening tens of thousands of compounds per campaign.[1]Nature Methods, “Advances in High-Throughput Screening,” nature.com Modern high-throughput platforms now process more than 100,000 data points per day by integrating robotic plate handlers, tight environmental control, and hybrid optics that switch between fluorescence polarization and time-resolved luminescence without manual changeover. This consolidation lets a single reader displace multiple single-mode devices, freeing bench space and reducing validation overhead. Biopharma R&D spending rose above USD 145 billion in 2025, intensifying pressure to improve productivity. Automation answers that call by allowing chemists to interrogate larger libraries with fewer full-time employees. Oncology and immunology programs show the greatest uptake because they rely on multiplexed cytokine profiling and live-cell imaging across 384- and 1536-well formats.

Growing Demand for Automation & Multi-Mode Detection in Diagnostics

Clinical laboratories now link sample reception, centrifugation, aliquoting, and microplate immunoassays into a single conveyor workflow, cutting manual touchpoints by more than 70% and reducing turnaround time for routine panels from 4 hours to under 90 minutes.[2]Academic OUP, “Total Laboratory Automation,” academic.oup.com Multi-mode readers fit seamlessly because they switch among ELISA, chemiluminescence, and fluorescence assays without operator intervention. Molecular Devices embedded AI-driven quality-control algorithms in its SpectraMax iD5e and iD3s models, released in July 2025, lowering repeat runs by an estimated 15%. Hospitals that reach 98% instrument availability can defer capital replacement by up to two years, a vital cash-flow advantage for regional networks. Demand is strongest in Asia-Pacific, where universal health coverage programs and electronic health record mandates require machine-readable assay data. Compliance frameworks such as ISO 15189 now stress audit trails, prompting vendors to add HL7 and FHIR connectivity.

Expansion of Life-Sciences Research Funding

Multi-year grants for precision-medicine programs funnel capital into proteomics core facilities that depend on microplate readers for ELISA, Luminex bead arrays, and AlphaLISA proximity assays. Genome Canada committed CAD 52 million (USD 38 million) in 2024 to shared-equipment purchases.[3]Genome Canada, “Research Funding Announcements,” genomecanada.ca India’s biotechnology roadmap targets sector expansion to USD 300 billion by 2030, with 30% directed to research infrastructure. Public funding often mandates open-access data, favoring cloud-connected readers that auto-upload to FAIR-compliant repositories. China’s biotechnology investment exceeded USD 20 billion in 2024, with procurement concentrated in the biotech parks in Shenzhen, Shanghai, and Beijing. These inflows smooth demand cycles because grant-funded equipment purchases are insulated from quarterly budget swings in private industry.

Technological Advances in Sensitivity & Throughput

Hybrid filter-monochromator optics, next-generation photomultiplier tubes, and improved thermal management tighten detection limits and shorten read times. Tecan’s Spark Cyto integrates confocal imaging that quantifies 3D spheroid growth in real time, reducing assay development time for oncology drug screening. Agilent’s BioTek Cytation combines environmental control with brightfield imaging, shrinking the workstation footprint from 6 m² to under 3 m². Piezoelectric and acoustic dispensing reach sub-100 nL precision, enabling 1536- and 3456-well formats that save reagents. Laboratories investing in these advances report up to 40% faster run times and 20% lower per-sample consumable costs, enhancing the appeal of microplate systems to lean operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs of Advanced Systems | -0.9% | Global, pronounced in emerging markets | Short term (≤2 years) |

| Shortage of Skilled Technicians | -0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Semiconductor & Optical Component Volatility | -0.4% | Global | Short term (≤2 years) |

| Competition From Lab-On-Chip Microfluidics | -0.3% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Advanced Systems

Multi-mode readers with integrated incubators, robotic stackers, and AI modules range from USD 80,000 to USD 200,000, stretching budgets for academic cores and early-stage biotech firms. Annual service contracts add an additional 8-12% to the purchase price, covering photomultiplier replacement and software updates. Import duties in several middle-income nations inflate landed costs by up to 35%, delaying adoption. Leasing and reagent-rental models from PerkinElmer and Tecan convert capital outlay into operating expense, but multi-year minimums expose laboratories to penalty clauses if projects stall. Cost pressure sometimes steers buyers toward lower-spec single-mode devices that can become obsolete once research shifts to multiplexed assays.

Shortage of Skilled Technicians

Operating advanced microplate systems requires expertise in liquid-handling robotics and data-integrity protocols, skills that 41% of employers report as critically scarce. University curricula lag, so new hires often need six months of training on automation software such as Tecan FluentControl. Under-staffed labs leave USD 150,000 instruments idle up to 40% of the time, hurting return on investment. CROs now run internal academies to cross-train staff, but attrition remains high as pharma firms offer 30% salary premiums after two years’ experience. Vendors respond by embedding wizards that auto-suggest gain settings and flag protocol deviations, lowering the learning curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Mode Readers Drive Consolidation

Multi-mode readers accounted for 36.12% of 2025 revenue and are projected to grow at 6.06% through 2031, the fastest rate among product categories, as laboratories replace single-mode absorbance units with hybrid platforms that integrate filter wheels and monochromators in a single chassis. This segment’s expansion lifts the microplate systems market size because each unit commands premium pricing and pulls through ancillary software and service contracts. Single-mode readers survive in high-volume ELISA labs where cost per test rules, yet their share erodes as automated conveyor architectures need instruments that run chemiluminescence and fluorescence without downtime. Pipetting and dispensing systems gain relevance as 1536-well and 3456-well formats spread, but their uptake depends on precision at sub-microliter volumes.

Tecan’s Spark and Agilent’s Cytation illustrate the trend toward convergence, folding detection, environment control, and imaging into footprints under 3 m². BMG LABTECH’s VANTAstar and Molecular Devices’ iD5e embed AI quality control, cutting repeat runs by 15%. Pipettor vendors focus on acoustic or piezoelectric dispensing to achieve ≤1 nL precision, a must for ultra-high-density plates. Microplate washers remain essential for ELISA workflows but often sell bundled with readers, reflecting buyer preference for single-vendor support contracts. Handlers and incubators round out the ecosystem; open-source designs such as G-Bot lower entry costs but challenge incumbent profit pools.

By Application: Genomics and Proteomics Outpace Legacy Screening

Drug discovery and high-throughput screening accounted for 47.09% of revenue in 2025, underscoring demand for phenotypic assays in oncology programs. However, genomics and proteomics research is the fastest-growing application at 7.63% CAGR, boosted by national precision-medicine grants that require multiplexed biomarker quantification. This dynamic diversifies the microplate systems market; even if pharma R&D stalls, public-funded omics projects sustain unit orders. Clinical diagnostics provides a steady baseline, with hospital labs adopting total automation to absorb seasonal surges in sample volume.

Cell-based assays and toxicity testing are gaining momentum as regulatory encouragement of in vitro alternatives drives the need for kinetic reads over 72 hours in incubated multi-mode readers. Environmental and food-safety applications, though smaller, are moving toward stricter residue limits; ELISA screening on plates remains the cost-effective first filter before confirmatory mass spectrometry. Vendors tailor firmware to handle long kinetic runs and integrate with LIMS for traceability. Feature roadmaps now include flexible scheduling that interleaves fast endpoint assays with multi-day cell viability studies, maximizing reader utilization.

By End User: CROs and CMOs Accelerate Faster Than Pharma

Pharmaceutical and biotechnology firms accounted for 41.13% of spending in 2025, yet contract research and manufacturing organizations grew faster at 8.18% through 2031 as outsourcing intensified. CROs buy automation-ready stacks with SiLA 2 interfaces that meet audit and data-integrity mandates, driving the microplate systems market share across service providers. Hospitals and diagnostic laboratories install multi-mode readers to shrink assay menus onto fewer devices amid reimbursement pressure.

Academic and research institutes rely on multi-year capital cycles funded by national science agencies, smoothing demand volatility. They emphasize open-access scheduling and cloud repositories, rewarding vendors that bundle no-code assay builders. Regional suppliers like Shenzhen Mindray and Rayto Life Sciences penetrate price-sensitive hospital segments with systems priced 30-40% below Western peers and backed by 24-hour service networks. Sales strategies must therefore segment by value driver: uptime for CROs, flexibility for pharma, cost for hospitals, and openness for academia.

Geography Analysis

North America retained a 38.29% share in 2025, fueled by biotech clusters in Boston and San Francisco, which together raised more than USD 30 billion in venture funding in 2024. Large CROs such as Charles River and IQVIA operate fleets of more than 500 readers each, ensuring consistent replacement cycles. FDA’s predictable 510(k) and Computer Software Assurance frameworks lower regulatory risk, speeding adoption of AI-enabled models. Canada contributes via Genome Canada grants that direct funds to precision-medicine cores, while Mexico’s demand is nascent but growing as private labs in Mexico City shift from manual ELISA to semi-automatic platforms.

Asia-Pacific is the fastest-growing region, with a 10.13% CAGR to 2031, double the global pace. China’s state funding of above USD 20 billion in 2024 and India’s roadmap to a USD 300 billion biotechnology value by 2030 supply robust capital for laboratory infrastructure. NMPA’s accelerated approvals enable domestic firms like Mindray to capture hospital share through localized service. Japan’s aging demographics drive laboratory automation, though lengthy consensus procurement slows cycles. Australia and South Korea maintain steady demand tied to genomics and biosecurity projects at leading universities.

Europe’s market reflects the revised in vitro diagnostic regulation, which increases data and environmental reporting requirements. Germany, the United Kingdom, and France dominate demand, blending pharmaceutical giants with academic heavyweights such as Max Planck Institutes and the Francis Crick Institute. Sustainability rules push buyers toward ACT-labeled instruments and recyclable consumables. The Middle East and Africa, though smaller, grow as Gulf states build biotech hubs; King Abdullah University and Dubai’s Mohammed bin Rashid University both installed multi-mode readers in 2025. South America sees Brazil leading, but high tariffs and currency swings temper growth. Collectively, these dynamics shape a geographically diversified microplate systems market with region-specific catalysts.

Regulatory Landscape

Microplate systems span research-use-only and regulated diagnostic environments, so compliance requirements vary by intended use and software functionality. In the United States, FDA device controls apply when plate readers, washers, or bundled software are marketed for IVD use, while laboratory-developed tests are primarily overseen under CLIA following the September 2025 rescission of the 2024 LDT final rule. For manufacturers, the FDA Quality Management System Regulation (QMSR) took effect on February 2, 2026, aligning device quality requirements more closely with ISO 13485-style quality management expectations.

In Europe, instruments and software supplied for IVD workflows are influenced by IVDR transition rules, including the extended transitional periods under Regulation (EU) 2024/1860 and operational milestones such as the May 26, 2026, Notified Body application deadline for Class C devices under the extension framework. Labeling and data integrity expectations also tighten through standards used in laboratory practice and procurement, including EN ISO 18113-3:2024 for IVD instrument labeling and the continued emphasis on ISO 15189 in accredited clinical laboratories, which pushes vendors toward stronger audit trails, connectivity, and traceability features in instrument firmware and data systems.

Competitive Landscape

The top five vendors, Danaher (Molecular Devices), Agilent Technologies, Revvity, Tecan Group, and Bio-Rad Laboratories, command significant global revenue, pointing to moderate concentration. These incumbents lock in customers through installed-base ecosystems that bundle readers, washers, and software, thereby raising switching costs associated with assay revalidation and staff retraining. Competition pivots on software and cloud services; vendors offering FAIR-compliant auto-upload and no-code assay builders lower adoption hurdles for resource-constrained labs.

Disruptors emerge from open-source automation consortia like Advanced Cell Culture System, which publish hardware blueprints that labs assemble for under USD 10,000, eroding ancillary revenue streams. Regional champions such as Shenzhen Mindray, Rayto Life Sciences, and Shimadzu win share in Asia-Pacific by pairing CE-mark or NMPA-cleared devices with local-language interfaces and rapid on-site service. Technology roadmaps now highlight AI algorithms for real-time QC, confocal imaging for 3D spheroids, and SiLA 2 compatibility, features that command 15-20% premiums because they compress assay development cycles.

Strategic moves continue to reshape the field. Ingersoll Rand purchased Scinomix in January 2026, adding plate handlers that integrate via SiLA 2 and broadening its precision portfolio. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification unit in February 2025 further tightens its grip on upstream workflows that feed microplate assays. Agilent’s 2024 takeover of BIOVECTRA creates a captive customer base for its BioTek readers. Such vertical integrations intensify service bundling and could raise entry barriers for smaller hardware-only entrants.

Microplate Systems Industry Leaders

Bio-Rad Laboratories, Inc.

Agilent Technologies, Inc.

Danaher Corporation

Shenzhen Mindray Bio-Medical Electronics Co., Ltd

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest gap sits at the intersection of high-content imaging, multimode detection, and automation-ready software stacks. Product moves in 2026 support this convergence, such as Agilent introducing the BioTek Cytation 9 cell imaging multimode reader, which packages imaging and hybrid detection in one platform and helps laboratories consolidate separate instruments used across cell-based assays, toxicity testing, and phenotypic screening. This consolidation theme aligns with the report’s buying behavior indicators, where multi-mode readers lead product share and CROs value automation-ready systems that reduce assay revalidation and downtime.

A second opportunity area is compliance-grade digital workflow enablement for regulated and semi-regulated labs, where procurement increasingly links instruments to data integrity and connectivity requirements. Embedded audit trails and electronic records requirements, often framed through FDA 21 CFR Part 11 in the United States and IVDR-aligned quality and documentation expectations in Europe, create room for vendors that ship validated software modules, standardized APIs, and LIMS connectivity rather than standalone readers. Open-source and modular automation efforts also widen integration paths, including new tooling that translates experimental designs into acoustic liquid handling instructions (for example, the PickliPy framework released in July 2026), which increases the value of vendor-supported interoperability across readers, stackers, and dispensing systems.

Recent Industry Developments

- July 2026: Agilent launched an AI-driven analysis module for its xCELLigence RTCA eSight workflow to automate label-free imaging analysis. By reducing manual interpretation steps, this strengthens Agilent's software-led differentiation around reproducibility and throughput in cell-based assay environments that frequently interface with microplate-based screening workflows.

- June 2025: Mitsui Chemicals launched InnoCell cell culture microplates featuring high oxygen permeability. The product targets more demanding live-cell and functional assay formats, reinforcing the shift toward specialty plates that perform reliably in automated handling and longer kinetic runs.

- May 2024: Genome Canada committed CAD 52 million (USD 38 million) toward shared-equipment purchases for research programs. This type of core-facility funding supports broader access to plate-based assay infrastructure, sustaining procurement of readers, washers, and automation-compatible add-ons in publicly funded labs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the microplate systems market is defined as the revenue generated from laboratory instruments and related control software used to process microplates for assays, screening, and routine testing across life science and diagnostic workflows.

Scope exclusions: We exclude reagents, disposable microplates, and standalone liquid handlers that do not have an integrated plate-deck workflow.

Segmentation Overview

- By Product Type

- Single-Mode Readers

- Multi-Mode Readers

- Microplate Washers

- Pipetting & Dispensing Systems

- Handlers & Incubators

- By Application

- Drug Discovery & HTS

- Genomics & Proteomics Research

- Clinical Diagnostics

- Cell-based Assays & Toxicity Testing

- Environmental & Food Safety Testing

- By End User

- Pharmaceutical & Biotechnology Companies

- CROs & CMOs

- Hospitals & Diagnostic Laboratories

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear product boundary and a short list of measurable signals that explain demand for microplate instruments. Public sources help us anchor those signals, including US FDA databases for diagnostics context, US NIH and similar grant databases for research funding direction, OECD or World Bank indicators for macro health and R&D intensity, and USITC or UN Comtrade trade statistics for instrument shipment movements. We also review peer reviewed articles that discuss assay throughput, microplate formats (96 to 1536 well), and adoption of automation in labs.

Alongside these, we use company annual reports, investor decks, and press releases to track product launches, regional exposure, and any pricing commentary that can affect average selling prices. Where needed, we also reference paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records to cross-check the public picture. These desk sources are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm the practical scope of what buyers treat as a microplate system, and to sanity check unit volumes and price ranges by instrument type and lab setting. We speak with a mix of instrument suppliers, distributors, lab managers, and procurement or operations leads across APAC, EMEA, and the Americas, so assumptions can be adjusted for regional purchasing cycles and installation patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 42% |

| Mid tier: 41% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 21% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where lab instrument demand is reconstructed from a demand pool that reflects assay activity, lab automation intensity, and typical replacement cycles for plate-based workflows. Inputs that shape the model include the installed base replacement rhythm for plate readers and washers, the shift toward higher-density plate formats, capital equipment budget trends in pharma and academic labs, clinical testing volumes where plate workflows are common, and observed price bands for single-mode versus multi-mode systems.

After this, results are checked using selective bottom-up approximations, such as sampled unit shipments by region multiplied by realistic ASP ranges, followed by distributor channel checks to catch over-counting between bundled systems and standalone modules. Gaps are handled by using conservative adoption curves for emerging geographies and by applying narrower ASP ranges when interview feedback indicates discounting is heavier than what desk sources suggest. Forecasting uses scenario analysis supported by a light multivariate regression, where assay throughput drivers and lab budget indicators are stress tested so the final curve does not rely on one single assumption.

Data Validation & Update Cycle

Validation is done through stepwise triangulation, where our market totals are compared against independent signals like reported instrument revenue mixes, trade flows for relevant equipment categories, and regional lab spending direction. Outliers are reviewed, and when a variance cannot be explained by scope or timing, we re-check assumptions and reconnect with experts who can clarify whether a change came from pricing, delayed purchases, or a reporting shift.

Before sign-off, the model and key assumptions go through internal analyst reviews so calculation logic and year mapping are consistent across regions and product groupings. Reports are refreshed annually, and interim updates are made when material events occur, such as major pricing resets, regulatory shifts that alter lab testing volumes, or large supply disruptions. Right before delivery, a final pass is performed to make sure the latest available public data and interview learnings are reflected.

Mordor Intelligence's Microplate Systems Market Size Compared With Other Published Estimates

Different publishers often land on different market sizes because they do not always align on what counts as a microplate system, which year is treated as the base, and how prices are converted and normalized across regions. The gap also grows when one estimate is updated on a different schedule, since instrument ASPs and shipment timing can move within a year.

In this study, the refresh cadence and currency timing are kept consistent across regions, and ASP logic is revalidated using distributor checks before totals are finalized, which is a key reason the 2026 number lands where it does for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.26 B (2026) | |

| Trade Journal A | USD 1.02 B (2023) | Uses an earlier base year and does not clearly state exclusions for adjacent spend like consumables, which can shift what is captured as system revenue and how inflation is treated across the time series. |

| Global Consultancy B | USD 1.98 B (2025) | Applies a broader product boundary and a faster ASP growth path, which can lift the total when bundled automation modules are counted more widely and discounting is not adjusted by region. |

The table shows that most of the spread comes from timing and boundary choices, followed by how ASPs and currency are handled across regions. By tying the model to clear plate-workflow indicators and then pressure testing totals with channel feedback, the estimate stays traceable and repeatable even when public data is uneven.

Key Questions Answered in the Report

What CAGR is projected for microplate systems between 2026 and 2031?

The microplate systems market is forecast to grow at a 4.73% CAGR over 2026-2031.

Which product segment grows fastest?

Multi-mode readers are set to advance at 6.06% CAGR, leading product-level growth.

How large is the share of drug discovery applications?

Drug discovery and high-throughput screening accounted for 47.09% of 2025 revenue.

Why are CROs buying more readers?

CROs and CMOs expand at 8.18% CAGR as pharma outsources routine assays, valuing automation-ready readers with GxP compliance.

Which region posts the highest growth rate?

Asia-Pacific leads with 10.13% CAGR through 2031, powered by Chinese and Indian biotech investment.

Page last updated on: