Hernia Mesh Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.47 Billion |

| Market Size (2031) | USD 5.5 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

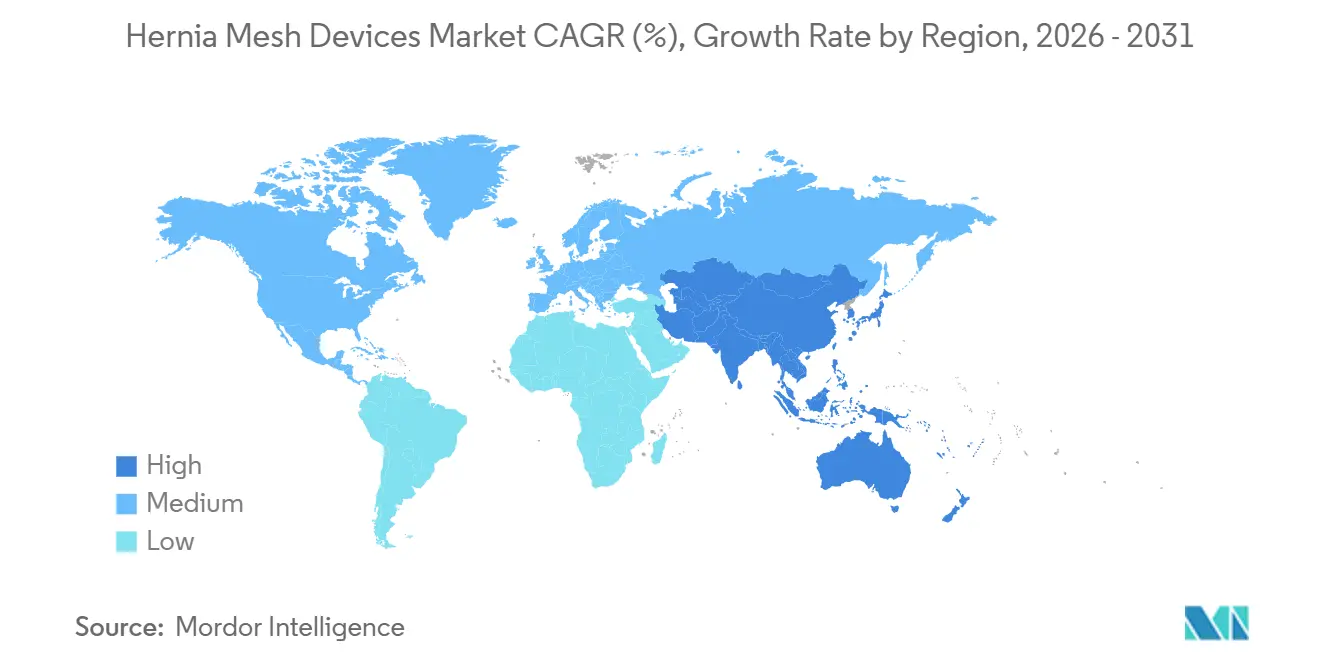

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

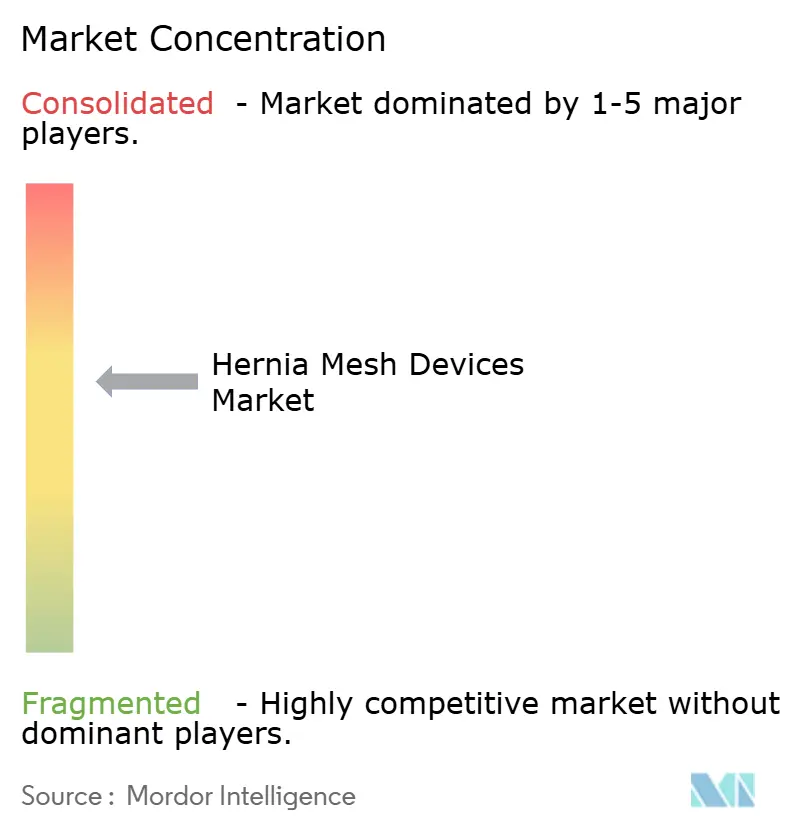

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hernia Mesh Devices Market Analysis by Mordor Intelligence

The hernia mesh devices market size reached USD 4.47 billion in 2026 and is expected to advance to USD 5.50 billion by 2031 at a 4.23% CAGR, reflecting measured growth that balances rising procedure volumes with persistent litigation headwinds. Obesity, population aging, and recurrent abdominal surgeries continue to maintain a steady demand. At the same time, the adoption of robotic repair, value-based procurement, and the introduction of premium biologic mesh products shape product strategies. Hospitals expand robotic fleets to limit conversion-to-open rates, and ambulatory centers leverage 40–60% cost savings to capture routine inguinal repairs. Manufacturers respond by refining lightweight composite meshes for trocar delivery, adding infection-resistant barriers for ventral cases, and accelerating the development of hybrid designs that strike a balance between tensile strength and resorption. Financial risk from more than USD 1 billion in 2024 legal settlements keeps pricing disciplined as buyers demand long-term safety records and indemnity clauses.

Key Report Takeaways

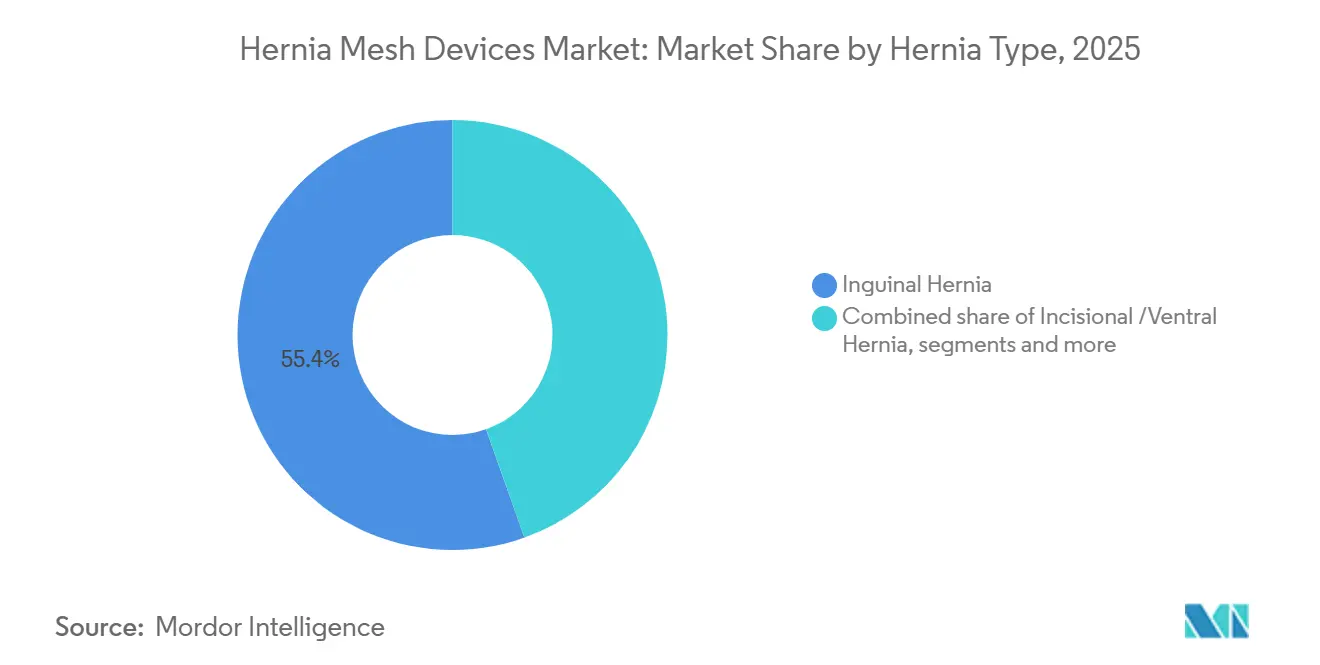

- By hernia type, inguinal repairs led with a 55.43% market share of hernia mesh devices in 2025, while ventral and incisional maintenance are projected to expand at a 6.54% CAGR through 2031.

- By mesh type, synthetic products accounted for 85.11% of the hernia mesh devices market size in 2025, whereas biologic alternatives are forecast to grow at a 6.42% CAGR through 2031.

- By mesh material, non-absorbable polymers held 78.43% share of the hernia mesh devices market size in 2025; fully absorbable poly-4-hydroxybutyrate platforms are expected to rise at 7.12% CAGR.

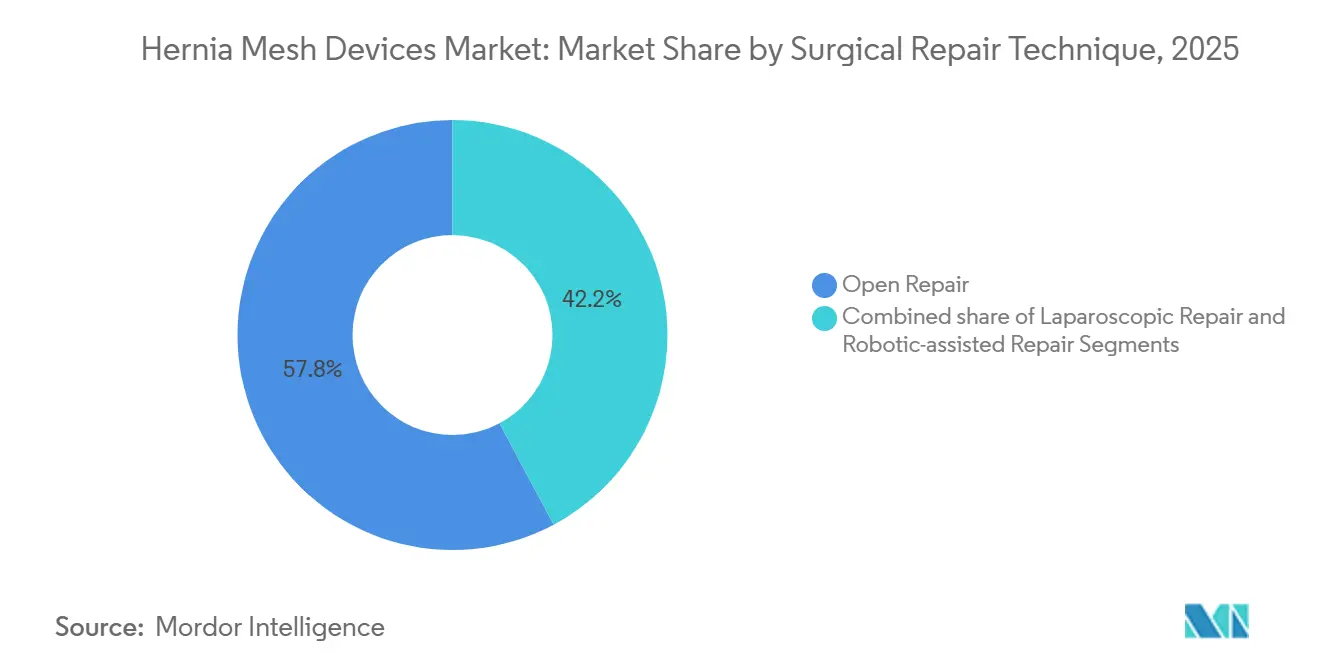

- By surgical technique, open repairs accounted for 57.86% of procedures in 2025, but robotic approaches are set to climb at a 6.98% CAGR through 2031.

- By end-user, hospitals captured a 48.65% revenue share in 2025, while ambulatory surgical centers are expected to post the quickest expansion at a 7.53% CAGR, driven by expanded CMS coverage.

- By geography, North America dominated with 41.35% of global revenue in 2025; Asia-Pacific is forecast to rise at a 5.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Hernia Mesh Devices Market*

| Driver | Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rising Surgical Hernia Incidence in Obese and Aging Populations | +1.2% | Global, with highest concentration in North America and Europe | Long term (≥ 4 years) |

| Shift Toward Minimally Invasive and Robotic Hernia Repairs | +0.9% | North America & Europe, expanding to Asia-Pacific tier-one cities | Medium term (2-4 years) |

| Product Innovations in Lightweight Composite and Barrier Meshes | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Adoption of Integratable Biosensors in Smart Mesh Prototypes | +0.3% | North America & Europe research hubs | Long term (≥ 4 years) |

| Uptake of Value-Based Procurement Contracts Favoring Low-Complication Meshes | +0.5% | North America, expanding to Europe | Short term (≤ 2 years) |

| Outsourcing of Custom 3D-Printed Meshes by Specialty Centers | +0.2% | North America & Europe academic medical centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Hernia Incidence in Obese and Aging Populations

Global obesity prevalence and a growing cohort aged 60 plus are raising procedure counts, particularly for ventral defects that are 2.42 times more common in obese patients than in normal-weight peers[1]. Meta-analysis data link obesity to a 1.27-fold higher inguinal recurrence, pressing surgeons to favor heavyweight polypropylene or reinforced composites in high-BMI cases. The World Health Organization projects that there will be 2.1 billion seniors by 2050, a demographic likely to present connective-tissue weakness and comorbidities that complicate mesh integration. Absorbable and hybrid meshes designed for impaired healing benefit from this trend, especially in complex ventral reconstructions that already exhibit a 6.54% CAGR within the Hernia mesh devices market. Post-bariatric patients and repeat laparotomy cases often result in larger, multi-territory defects, driving the consumption of premium barrier meshes that reduce infection risk while maintaining tensile support.

Shift Toward Minimally Invasive and Robotic Hernia Repairs

Robotic platforms have surpassed the adoption tipping point in U.S. hernia centers, with 54.9% of inguinal repairs utilizing robotic assistance during 2022–2023, compared to 45.1% using laparoscopic techniques, thereby reducing conversion rates to open surgery to 1.2%. Hospitals amortize da Vinci systems across multiple specialties, and surgeons typically reach proficiency after 16–20 robotic cases, which is half the number required for standard laparoscopy. Mesh design has followed suit, with low-profile products that roll through an 8 mm trocar and unfold without extra fixation; Gore’s SYNECOR hybrid mesh delivers 2.5 times the tensile strength of Bard Soft Mesh and remains pliable for robotic manipulation. Operative time still runs 15–20 minutes longer than laparoscopy, prompting suppliers to add self-gripping features that eliminate the need for sutures. Ambulatory centers, now eligible for robotic hernia reimbursement under the 2025 CMS ASC list, are expanding access and increasing demand for pre-sterilized mesh kits, which reduce turnaround times.

Product Innovations in Lightweight Composite and Barrier Meshes

Material science breakthroughs now decouple foreign-body burden from mechanical strength. Gore’s ENFORM fully absorbable mesh, unveiled in 2024, shows 25% greater tensile strength than BD’s Phasix and has reported zero infections in early cohorts, an advantage in contaminated fields where synthetic mesh once produced infection rates up to 15%. Academic data from July 2024 challenge the notion of aggressive weight reduction: lightweight synthetics displayed higher failure rates in ventral repairs than medium-weight alternatives, suggesting an integration trade-off[2]. Composite meshes strike a middle ground by incorporating a visceral barrier layer coupled to a parietal polypropylene scaffold, which cuts adhesions without compromising modulus. Phasix maintained double-digit growth in fiscal 2024 by serving surgeons who treat diabetics or immunosuppressed patients who require gradual resorption of implants. Yet, high price points—biologics run three to five times the cost of synthetics limit uptake in emerging markets and cost-sensitive ambulatory settings, steering buyers toward value-engineered hybrids, such as Gore’s SYNECOR.

Adoption of Integratable Biosensors in Smart Mesh Prototypes

Preclinical prototypes that embed strain and pH sensors tackle an unmet need for real-time complication detection. Early smart meshes wirelessly transmit intra-abdominal pressure and tissue pH, alerting clinicians to the presence of seroma or infection before symptoms arise. Technical obstacles remain: sensor coatings must resist enzymatic degradation for 90 days, power modules must avoid thermal injury, and Bluetooth-class signals must penetrate adipose tissue while meeting FCC absorption limits. No smart mesh has yet secured FDA clearance, leaving adoption confined to research centers that manage complex abdominal wall reconstructions. Long-term, these devices could help guide staged repairs and post-operative activity, but cost and regulatory ambiguity keep them a future-state driver rather than an immediate volume catalyst.

Restraints Impact Analysis of Hernia Mesh Devices Market*

| Restraint | Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Product Recalls and Litigation Over Chronic Pain & Adhesion Risks | -0.8% | Global, most acute in North America | Medium term (2-4 years) |

| High Per-Procedure Cost of Biologic and Biosynthetic Meshes | -0.6% | Global, limits Asia-Pacific and Latin America uptake | Short term (≤ 2 years) |

| Availability of Suture-Only Tissue Repairs for Small Defects | -0.3% | Global, particularly in Europe following EHS guidelines | Long term (≥ 4 years) |

| Slow Uptake in Emerging Markets Owing to Sterilization Infrastructure Gaps | -0.5% | Asia-Pacific tier-two cities, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Product Recalls and Litigation Over Chronic Pain & Adhesion Risks

More than USD 1 billion in 2024 settlements, including BD’s resolution of 38,000 lawsuits, underscore the financial stakes tied to chronic pain and adhesion claims. Ethicon’s Physiomesh remains burdened by 3,617 pending suits despite its 2016 withdrawal, while Getinge paid SEK 450 million to settle related actions in 2023. Hospitals now insist on indemnity clauses and 90-day complication tracking, forcing suppliers to restrain prices and emphasize long-term data, such as Gore’s 13-year BIO-A follow-up, which records a 6.2% recurrence rate. Litigation chills radical innovation, steering R&D toward predicate-line extensions rather than novel materials that could trigger extensive surveillance mandates.

High Per-Procedure Cost of Biologic and Biosynthetic Meshes

Biologic meshes cost USD 2,000–4,000, compared to USD 150–300 for polypropylene, resulting in negative margins under bundled payments and limiting adoption to contaminated or complex cases. TELA Bio’s OviTex, priced at the upper end, still logged 29% revenue growth in Q3 2024 by focusing on tertiary reconstructions. Ambulatory centers, which are expanding at a 7.53% CAGR, are defaulting to synthetics to remain profitable under Medicare’s average reimbursement of USD 3,500 for inguinal repair. Emerging markets feel the constraint more acutely; per-capita health spend below USD 500 pushes clinics toward low-cost polypropylene even when comorbidities warrant absorbable alternatives. Hybrid meshes like SYNECOR, which cost under half of leading biologics, aim to bridge the gap, yet still face price pushback outside well-funded systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hernia Mesh Devices Market Segment Analysis

By Hernia Type:

Ventral Repairs Outpace Inguinal Volume GrowthVentral and incisional repairs, propelled by obesity and repeat laparotomies, are forecast to outstrip inguinal growth at 6.54% CAGR through 2031. Inguinal repairs retained 55.43% of the Hernia mesh devices market share in 2025; however, their annual growth lags, as BMI shows an inverse association with groin defects, evidenced by an odds ratio of 0.60.

The hernia mesh devices market increasingly sees ventral cases exceeding 10 cm that require component separation and large composite meshes. Robotic uptake favors inguinal work—54.9% of groin repairs used robotics in 2022–2023—but complex ventral reconstructions still rely on open techniques paired with biologic scaffolds such as OviTex, which underpinned TELA Bio’s 29% sales jump. Post-bariatric cohorts and elderly women with femoral hernias sustain a varied but steady demand for mesh reinforcement across non-midline defects.

By Mesh Type:

Biologic Platforms Gain Share in Contaminated FieldsSynthetic meshes accounted for 85.11% of the revenue in 2025; however, biologics are expected to accelerate at a 6.42% CAGR as surgeons expand indications beyond frank contamination. In clean-contaminated ventral repairs, Phasix posted double-digit growth during fiscal 2024, demonstrating that a resorbable P4HB scaffold can capture a significant market share when infection risk is elevated.

The hernia mesh devices market size for hybrid designs such as SYNECOR is projected to widen as payers seek lower-priced alternatives with infection resistance. Ambulatory centers remain price sensitive, so biologic use stays below 5% of their volume, while hospitals apply them in up to 25% of complex abdominal wall cases. Lightweight synthetics face scrutiny after registry data showed higher failure in ventral repairs versus medium-weight constructs, reinforcing the need for balanced weight-to-strength ratios.

By Mesh Material:

Absorbable Polymers Challenge Polypropylene DominanceNon-absorbable polypropylene still accounts for 78.43% of revenue, but fully absorbable P4HB meshes will rise at 7.12% CAGR as chronic pain and foreign-body sensation concerns gain visibility. ENFORM’s 25% strength edge and zero infections in early use make it attractive for contaminated fields.

Partially absorbable blends promise lower inflammation but may compromise integration if too lightweight, as 2024 data revealed elevated ventral failure rates. The Hernia mesh devices market in emerging regions remains polypropylene-centric due to logistical gaps that limit biologic logistics; however, long-term hospitals may adopt absorbables as cold-chain infrastructure improves.

By Surgical Repair Technique:

Robotic Platforms Reshape Operative WorkflowsOpen repair maintained 57.86% of cases in 2025, but robotic procedures are on pace to expand at a 6.98% CAGR, the fastest growth rate in the Hernia mesh devices market. Robotic inguinal repairs reduce conversion-to-open rates to 1.2% and shorten learning curves, thereby incentivizing hospital capital outlays.

Laparoscopy still dominates in cost-conscious settings, while open methods remain indispensable for large ventral hernias that require component separation. Standardized robotic mesh kits with self-gripping surfaces reduce the 15–20 minute operative time penalty and support ambulatory workflows. Hospitals continue to refine protocol-driven instrument turnover to recover da Vinci leasing costs across multiple service lines.

By End-User:

Ambulatory Centers Capture Routine Inguinal VolumeHospitals retained 48.65% share in 2025, yet ambulatory surgical centers will post a 7.53% CAGR through 2031 as CMS expands the ASC-covered list. The Hernia mesh devices market size within ASCs favors lightweight synthetic meshes that fit bundled payments, while hospitals remain the primary users of biologics for contaminated or complex reconstructions.

Specialty tourism hubs in Thailand, Singapore, Brazil, and the United Arab Emirates deploy premium hybrids to attract international patients and differentiate service lines. Military facilities prioritize shelf life and cost, thus defaulting to polypropylene. Parallel demand curves emerge: hospitals drive premium adoption for complex cases, whereas ASCs fuel high-volume, cost-efficient synthetic sales.

Geography Analysis

North America Hernia Mesh Devices Market

North America accounted for 41.35% of 2025 revenue, driven by more than 1 million annual procedures, leading robotic penetration, and procurement models that reward low-complication meshes. The region’s insurers and hospitals insist on long-term performance data after BD’s USD 1 billion settlement, pushing suppliers toward meshes with decade-long track records. Robotic usage in inguinal repair surpassed 54% during 2022–2023, and ASC migration accelerates under CMS reimbursement, shifting routine volumes into lower-cost sites.

APAC Hernia Mesh Devices Market

The Asia-Pacific region is expected to log the fastest growth rate of 5.67% CAGR, as Chinese insurance reforms expand surgical coverage and Indian device liberalization increases import flows. However, sterilization gaps and cold-chain limits keep biologic uptake low outside tier-one cities; polypropylene dominates lower-income segments. Singapore and Thailand leverage premium meshes, such as SYNECOR, to attract medical tourists, while TELA Bio’s international expansion targets Australia and affluent clinics in Southeast Asia.

EMEA and South America Hernia Mesh Devices Market

Europe’s stringent Medical Device Regulation slows new product launches but cements quality expectations. EHS guidelines confine mesh use to tiny defects, tempering overall per-capita consumption. Litigation is less severe in Sweden than in the United States, but still notable; Getinge’s SEK 450 million settlement highlights the growing regional risk. The Middle East & Africa, as well as South America, offer nascent growth, with Gulf states investing in tertiary robotics and Brazil’s private network adding da Vinci systems. However, the public sectors remain budget-constrained and reliant on polypropylene.

Competitive Landscape

The hernia mesh devices market features moderate fragmentation. Global leaders, including Ethicon, Medtronic, Becton Dickinson, and W.L. Gore, hold strong positions, while specialty entrants such as TELA Bio carve out premium niches. Legal liabilities force large players to allocate hefty reserves: BD’s USD 1 billion outlay and Getinge’s SEK 450 million settlement exemplify the cost of post-market complications. Gore differentiates through material science, launching ENFORM and SYNECOR to pair strength with infection resistance at competitive price points.

White-space areas include custom 3D-printed meshes, smart sensor-embedded constructs, and value-engineered hybrids tailored for ASC economics. TELA Bio’s 29% revenue surge in Q3 2024 shows specialist momentum when clinical evidence and surgeon education align. Regulatory pathways grant incumbents an edge: FDA 510(k) linkage to legacy predicates shortens approval cycles, while Europe’s MDR imposes data burdens that smaller firms may struggle to finance. Competitive intensity will tighten as robotics amplifies demand for trocar-deployable meshes and as payers tie pricing to 90-day outcomes.

Hernia Mesh Devices Industry Leaders

Medtronic Plc

W. L. Gore & Associates, Inc.

Ethicon Inc. (Johnson & Johnson)

Becton, Dickinson and Company

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Hernia Mesh Devices Market Companies Covered in this Report

- AbbVie Inc. (LifeCell)

- Advanced Medical Solutions Group

- B. Braun

- Beckton Dickinson

- Cook Group

- Cousin Surgery SAS

- Dipromed

- Duomed Group

- Ethicon Inc. (Johnson & Johnson)

- Getinge AB (Atrium Medical)

- Herniamesh Srl

- Integra LifeSciences Holdings Corp.

- Medtronic

- Novus Scientific AB

- Poly-Med Inc.

- TELA Bio Inc.

- Via Surgical Ltd.

- W. L. Gore & Associates

Recent Industry Developments in Hernia Mesh Devices Market

- October 2025: TI Medical, a rapidly expanding Indian surgical device company, launched its innovative hernia repair mesh, HIPO. The event saw participation from India’s top laparoscopic and gastrointestinal surgeons, highlighting its significance in surgical advancements. This launch underscores TI Medical’s commitment to enhancing patient care with precision-engineered solutions.

- June 2025: TELA Bio, Inc. announced the European launch of its OviTex Inguinal Reinforced Tissue Matrix, designed for laparoscopic and robotic-assisted inguinal hernia repair. This follows the successful U.S. launch in 2024, where it generated over USD 1 million in sales in its first year. The product offers a natural alternative to synthetic mesh for hernia surgeries.

- April 2025: Becton, Dickinson and Company launched Phasix ST Umbilical Hernia Patch. This is the first fully absorbable hernia patch specifically designed for umbilical hernias. The new product aims to improve treatment options for patients with umbilical hernias.

Hernia Mesh Devices Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the hernia mesh devices market as the value of newly manufactured synthetic, biologic, or hybrid mesh implants supplied for surgical reinforcement of abdominal wall defects across all hernia types. The scope tracks factory-gate revenues, not procedural fees or ancillary fixation tools.

Scope Exclusions - One-line Note. Staples, tacks, glues, sutures, robotic arms, and other fixation accessories are excluded.

Segments Covered in This Report

- By Hernia Type

- Inguinal Hernia

- Incisional / Ventral Hernia

- Femoral Hernia

- Other Hernia Types

- By Mesh Type

- Synthetic Mesh

- Biologic Mesh

- Bio-Synthetic / Hybrid Mesh

- By Mesh Material

- Non-Absorbable (Polypropylene, ePTFE, Polyester)

- Partially-Absorbable (PP + PGA/PLA)

- Fully-Absorbable (P4HB, PGA)

- By Surgical Repair Technique

- Open Repair

- Laparoscopic Repair

- Robotic-Assisted Repair

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interview general surgeons, minimally invasive specialists, supply-chain managers at group purchasing organizations, and material scientists across North America, Europe, Asia-Pacific, and Latin America. Their inputs validate mesh utilization rates, biologic adoption hurdles, typical ASP discount ladders, and regional coding-reimbursement nuances, allowing us to close data gaps and fine-tune model assumptions.

Desk Research

Mordor analysts begin with open datasets such as the WHO Global Health Observatory, OECD Health Statistics, United States CDC National Inpatient Sample, and the European Hernia Society registry, which map procedure incidence and technique mix by country. Trade-body reports (Medical Device Manufacturers Association), peer-reviewed journals in Surgical Endoscopy, customs import records, and filings retrieved from D&B Hoovers and the FDA 510(k) database further clarify mesh volumes, material splits, and average selling prices (ASPs). These publicly available sources, alongside paid feeds from Dow Jones Factiva and Questel patent analytics, collectively anchor baseline demand and technology trends. The list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down procedure-pool model converts country-level hernia repair volumes into mesh unit demand using surveyed penetration ratios, which are then stress-tested against sampled manufacturer ASP × volume roll-ups from hospital channel checks. Key drivers include elective surgery backlog clearance, shift toward ambulatory centers, FDA biologic approvals, polypropylene price movements, and robotic-assisted repair share gains. Forecasts rely on a multivariate ARIMA that links mesh uptake to aging population growth, obesity prevalence, and disposable income trajectories, with scenario adjustments vetted by interviewed surgeons. Residual bottom-up gaps are bridged through selective supplier roll-ups.

Data Validation & Update Cycle

Outputs pass multi-step variance checks and peer review. Material deviations trigger re-contacts with sources. Reports refresh annually, and any recall, litigation, or reimbursement shock prompts an interim update before client delivery.

How Mordor Intelligence's Hernia Mesh Devices Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick different device mixes, pricing tiers, and refresh cadences.

Key gap drivers include whether fixation kits are bundled, how biologic meshes are weighted, the ASP progression method, and the frequency of exchange-rate resets. Mordor's disciplined scope, annual refresh, and dual-approach modeling mitigate these variables, yielding a balanced baseline for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.29 B (2025) | Mordor Intelligence | - |

| USD 5.58 B (2024) | Global Consultancy A | Bundles fixation devices and ventral patch systems, inflating total |

| USD 4.96 B (2024) | Industry Tracker B | Applies retail ASPs without channel discount adjustments |

| USD 2.29 B (2024) | Trade Journal C | Focuses mainly on biologic meshes sold in North America |

These contrasts show that, by selecting the right product universe and validating every assumption through field feedback, Mordor Intelligence delivers a transparent, reproducible baseline clients can rely on for strategic planning.

Key Questions Answered in the Report

What is the current global value of the Hernia mesh devices market?

The Hernia mesh devices market size reached USD 4.47 billion in 2026.

How fast will revenue grow for hernia mesh devices over the next five years?

Market revenue is projected to rise to USD 5.50 billion by 2031 at a 4.23% CAGR.

Which hernia type is expanding the quickest?

Ventral and incisional repairs are advancing at a 6.54% CAGR as obesity elevates midline defect risk.

Why are ambulatory surgical centers gaining share in hernia repair?

CMS reimbursement now covers laparoscopic and robotic inguinal repairs, and ASCs operate at 40-60% lower costs than hospital outpatient departments.

What material innovations are drawing surgeon interest?

Fully absorbable poly-4-hydroxybutyrate meshes such as ENFORM and Phasix combine infection resistance with durable strength.

How significant is litigation risk for mesh manufacturers?

More than USD 1 billion in settlements in 2024 demonstrates that chronic pain and adhesion claims remain a major financial constraint.

Page last updated on: