Mexico Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.37 Billion |

| Market Size (2026) | USD 5.54 Billion |

| Market Size (2031) | USD 6.49 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

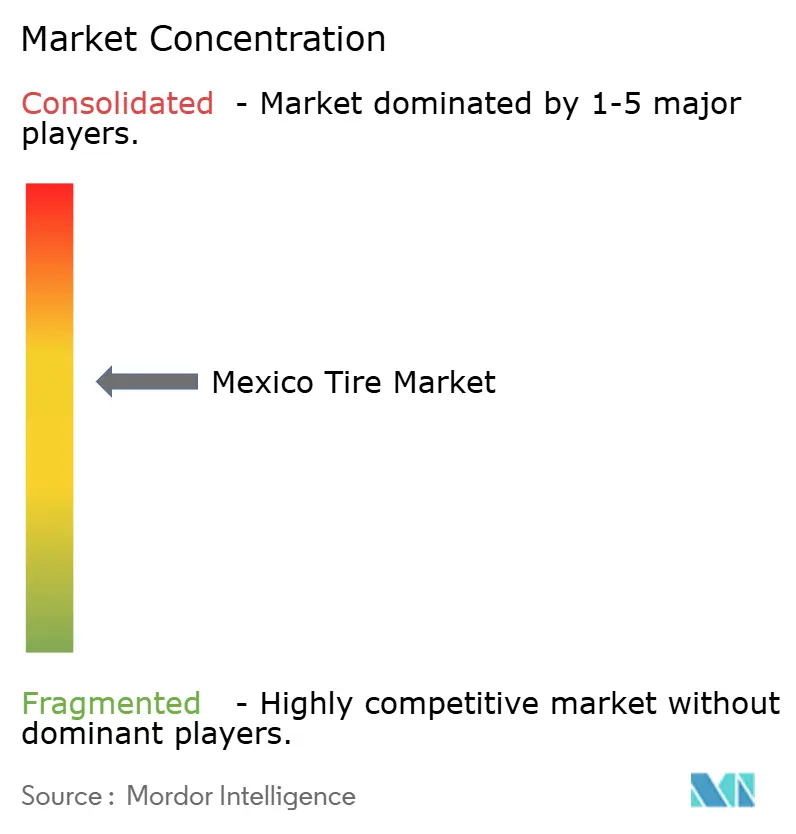

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Tire Market Analysis by Mordor Intelligence

The Mexican tire market size is expected to increase from USD 5.37 billion in 2025 to USD 5.54 billion in 2026 and is forecast to reach USD 6.49 billion by 2031, growing at a CAGR of 3.21% over 2026-2031. Near-shoring investments by global brands, supportive trade rules under USMCA, and anti-dumping duties on certain imports have strengthened local pricing power and encouraged capacity additions. Demand is further lifted by the expanding light-truck and SUV production base, which favors mid-size, high-load-index tires. On the downside, raw-material price swings and consumers’ inflation-driven delays in replacement purchases continue to temper volume growth. Still, growing interest in airless, EV-optimized, and circular-economy solutions is opening white-space opportunities for both incumbents and new entrants.

Key Report Takeaways

- By season, All-Season tires led with 67.12% of the Mexico tire market share in 2025; Summer tires are projected to expand at a 4.25% CAGR through 2031.

- By tire design, Radial tires held 89.15% of the Mexico tire market share in 2025, while Non-pneumatic/Airless formats are set to advance at a 6.17% CAGR to 2031.

- By vehicle type, Passenger Cars accounted for a 48.33% share of the Mexico tire market size in 2025, and Off-the-Road/Specialty tires are growing fastest at a 5.61% CAGR through 2031.

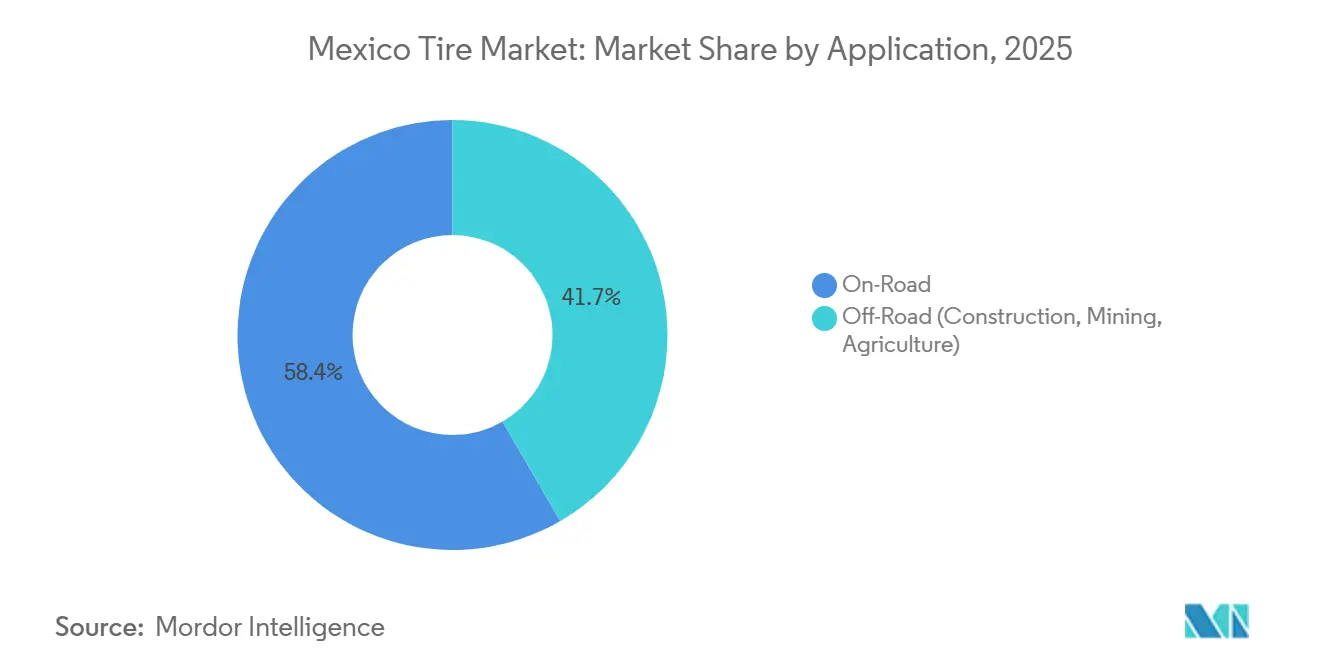

- By application, On-Road demand represented 58.35% share of the Mexico tire market size in 2025; Off-Road tires are forecast to post a 5.29% CAGR to 2031.

- By end user, the Aftermarket captured 75.16% share of the Mexico tire market size in 2025, whereas OEM deliveries are expected to expand at a 4.06% CAGR over the forecast horizon.

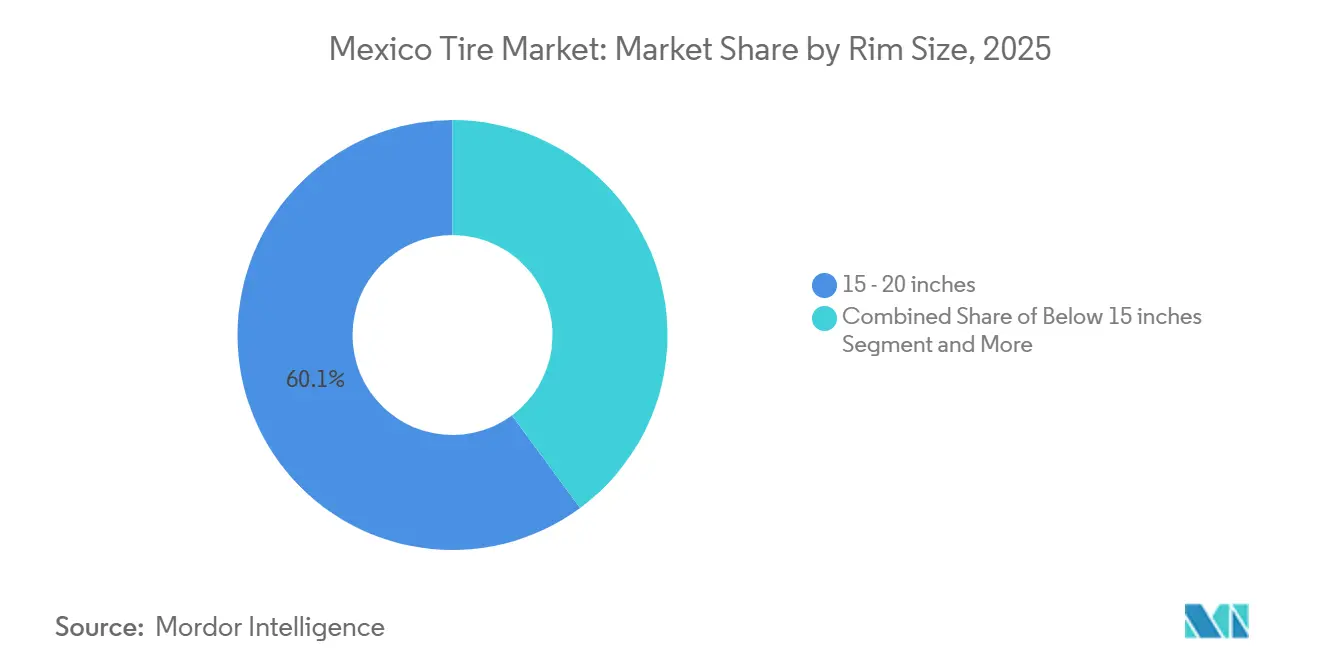

- By rim size, the 15-to-20-inch range commanded 60.12% share of the Mexico tire market size in 2025; Above-20-inch sizes are on track for a 6.55% CAGR through 2031.

- By propulsion, Internal-Combustion vehicles represented 83.14% share of the Mexican tire market size in 2025, yet Battery-Electric vehicle tires will surge at a 10.37% CAGR to 2031.

- By geography, Central Mexico accounted for 42.55% share of the Mexico tire market in 2024, while Northern Mexico is poised to expand at a 4.76% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Passenger-Vehicle Demand | +0.8% | National; strongest in Central and Northern Mexico | Medium term (2-4 years) |

| Near-shoring Boosts OEM Capacity | +0.7% | Northern and Central manufacturing corridors | Long term (≥ 4 years) |

| Anti-Dumping Stabilizes Domestic Pricing | +0.5% | Central clusters; Northern assembly plants | Medium term (2-4 years) |

| SUV and Light-Truck Output Rises | +0.4% | National; highest in border regions | Short term (≤ 2 years) |

| Fleet Digital Management Adoption | +0.2% | National; early uptake in Northern logistics lanes | Long term (≥ 4 years) |

| Guayule-Based Rubber Pilots | +0.1% | Northern arid zones; cross-border R&D sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Passenger-Vehicle Parc and Replacement Demand

An aging vehicle fleet underpins a steady aftermarket, as older cars cycle through tires more frequently than new models. Independent retailers dominate distribution, yet digital maintenance platforms are winning adopters among commercial fleets by reducing downtime and optimizing inventory. Macro-economic inflation has caused some motorists to defer purchases or trade down, but premiumization persists among safety-conscious buyers who view high-performance tires as a value rather than a luxury. Regulatory safety standards reinforce this perception by setting clear benchmarks for tread and labeling compliance, implicitly nudging consumers toward established brands. As connectivity features proliferate, predictive maintenance alerts encourage timely replacements, moderating the impact of price sensitivity.

Near-Shoring-Led OEM Capacity Expansion (Goodyear, Michelin, Pirelli)

Regional sourcing incentives are prompting global manufacturers to add local capacity, exemplified by Yokohama’s ongoing Saltillo greenfield project and other multinationals’ plant upgrades[1]"New Yokohama Tire Plant in Mexico Will Provide Additional Capacity to North America," Yokohama Tire Corporation, www.yokohamatire.com. These moves shorten supply chains for North American OEM contracts, improve just-in-time reliability, and strengthen bargaining positions with automakers that now prefer regionally compliant inputs. Local governments in Nuevo León and Coahuila actively court suppliers with streamlined permitting and workforce training programs, creating industrial clusters that feed into U.S. export corridors. As production scales, ancillary benefits arise for compounders, mold makers, and logistics firms, forming a self-reinforcing ecosystem that supports long-term market stability. The visibility into volume from locked-in OEM contracts also enables tire makers to pursue higher-margin specialty lines for the aftermarket.

Anti-Dumping Duties Stabilizing Domestic Pricing

Tariffs on selected Chinese tires have narrowed cost gaps, granting domestic and multinational producers a buffer to recoup higher raw-material expenses[2]"Mexico approves tariff hikes on imports from India, China, and other Asian countries," ET Online, economictimes.indiatimes.com . While some parallel-import circumvention persists, enforcement through customs inspections and stricter documentation has curbed extreme price undercutting in key urban markets. Suppliers now negotiate multi-year OEM deals without the constant threat of sudden, low-priced bids, enabling more predictable capacity planning. The duties also catalyze investments in local testing facilities to certify compliance, deepening technical capabilities within Mexico’s manufacturing base. Over time, consistent pricing should encourage more tier-two suppliers to commit capital to compound mixing and mold tooling, strengthening the entire value chain.

SUV and Light-Truck Output Boom Lifting Mid-Size Tire Demand

Mexico’s assembly plants have pivoted toward SUVs and light trucks, segments that require larger-diameter, higher-load-index tires. OEM specifications now prioritize compounds balancing rolling resistance and durability, an area where premium brands leverage proprietary materials science to defend pricing. This structural shift in the mix of structures filters downstream into replacement demand, since fleet and personal-use owners typically repurchase OEM-specified sizes. Smaller budget brands face a certification hurdle in meeting global automakers’ strict quality protocols, which in turn protects incumbent shares in the lucrative OEM channel. The performance-oriented consumer base in northern states further amplifies demand for sport-tuned all-terrain and summer compounds, nudging the overall product mix toward higher-value units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw Material Prices | -0.6% | National; manufacturing centers most exposed | Short term (≤ 2 years) |

| Compounder Shortage for EV Tires | -0.4% | Central EV manufacturing hubs | Medium term (2-4 years) |

| Inflow of Low-Priced Imports | -0.3% | Border regions; major distribution hubs | Medium term (2-4 years) |

| Inflation Postpones Replacements | -0.2% | National; consumer markets nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Synthetic-Rubber and Crude Prices

Input-cost fluctuations erode margins because tire makers cannot always raise prices instantly without risking share. Hedging mitigates some variability, yet sudden feedstock shortages or energy price spikes ripple throughout the cost structure. Small- to mid-size plants feel the squeeze most acutely, lacking the purchasing leverage of their global peers. Persistent swings undermine capital-investment planning, as project returns hinge on stable cost baselines. Until alternative rubber sources such as guayule reach scale, exposure to global commodity cycles remains an operational reality.

Tier-2 Compounder Shortage for EV-Specific Tires

Battery-electric vehicles demand high-silica, low-rolling-resistance compounds that few local mixers can supply at quality and volume. As BEV output accelerates, OEMs risk longer lead times and import dependency. Joint-development initiatives between global tire majors and local chemical firms are underway, but capacity ramp-ups require technical know-how, capital, and rigorous qualification testing. This bottleneck caps near-term volume potential for EV-optimized lines and slows the wider market’s transition toward lower-emission mobility solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Dominance, Summer Momentum

All-Season tires secured the largest Mexico tire market share at 67.12% in 2025, reflecting their ability to handle the country’s varied yet mostly temperate driving conditions. Fleet managers appreciate a single, versatile product that simplifies stocking and rotation decisions across mixed vehicle groups. Tire makers reinforce this preference by blending compounds that balance wet traction and tread life, which resonates with safety-minded consumers and commercial operators alike. Dealer networks also promote All-Season lines as the default choice, streamlining marketing messages for both premium and budget shoppers.

Summer tires, projected to grow at a 4.25% CAGR through 2031, are gaining followers among performance-oriented drivers who prioritize handling precision and shorter braking distances. Suppliers highlight sport-tuned road feel and stylish tread patterns in their advertising, appealing to owners of high-profile SUVs and pickups in Mexico’s hotter northern states. Retailers are beginning to allocate more shelf space to Summer SKUs, encouraged by steady inquiries from enthusiasts migrating up the value curve. Training programs for technicians now include best-practice guidelines on temperature-sensitive compounds, reinforcing confidence in proper fitment.

By Tire Design: Radial Supremacy, Airless Trials

Radial construction commanded 89.15% of the Mexican tire market share in 2025, a testament to decades of product refinement and widespread OEM endorsement. The layered steel-belt architecture delivers comfort, durability, and fuel efficiency that align with everyday driving needs across urban and rural routes. Manufacturers continue to tweak tread geometry and rubber chemistry to trim rolling resistance, positioning radial lines as low-maintenance choices for cost-conscious fleets. Service centers are fully equipped to handle radial repairs and balancing, cementing their status as the default aftermarket replacement.

Non-pneumatic or Airless tires are poised to expand at a 6.17% CAGR, driven by commercial operators eager to eliminate puncture-related downtime. Early adopters in construction, logistics, and municipal services cite predictable maintenance schedules and extended service intervals as compelling benefits. Pilot programs showcase the absence of pressure checks and the resilience of composite web structures under harsh site conditions. Training modules for equipment operators emphasize the simplicity of daily inspections, further lowering operational hurdles.

By Vehicle Type: Passenger Car Scale, Specialty Upside

Passenger Cars represented the largest slice of the Mexico tire market size at 48.33% in 2025, underscoring the centrality of light-vehicle ownership to national mobility. A broad installed base ensures steady replacement cycles, which in turn support stable plant utilization for mainstream rim diameters and tread patterns. Dealers maintain deep inventories of passenger-car tires, allowing same-day installation that reinforces consumer loyalty. Marketing campaigns from global brands focus on ride comfort and mileage warranties, attributes valued by daily commuters.

Off-the-Road and Specialty tires are expected to post the fastest growth at a 5.61% CAGR, reflecting momentum in mining, agriculture, and motorsport activities. Heavy equipment operators require robust sidewalls and unique tread geometries to navigate abrasive terrains, creating a premium niche for high-margin SKUs. Suppliers collaborate closely with machinery OEMs to fine-tune load ratings and compound recipes, ensuring product integrity under extreme loads. Training clinics for fleet technicians emphasize correct mounting procedures to maximize service life in remote sites.

By Application: On-Road Core, Off-Road Lift

On-Road usage commanded 58.35% of the Mexican tire market revenue in 2025, mirroring Mexico’s extensive highway network and high daily commuting volumes. Continuous pavement upgrades keep demand resilient for long-wear, low-noise tread designs aimed at passenger cars and light commercial fleets. Tire makers update sidewall aesthetics and labeling to meet evolving safety and eco-rating standards, reinforcing consumer trust. Wholesale distributors rely on predictable reorder cadences from urban retailers, allowing efficient inventory turns. This ingrained channel synergy helps stabilize margins even when raw-material costs fluctuate.

Off-Road applications are projected to rise at a 5.29% CAGR, buoyed by sustained capital spending in construction corridors and mineral extraction zones. Operators value puncture resistance and heat dissipation, prompting suppliers to develop thicker carcass layers and specialized cooling ribs. Dealer training now includes telematics integration, enabling real-time monitoring of temperature and tread depth for heavy machinery. Case studies from early adopters highlight lower unplanned stoppages, convincing risk-averse fleet managers to pilot next-generation designs.

By End User: Aftermarket Weight, OEM Momentum

The aftermarket captured 75.16% of 2025 shipments, reflecting the size and age of Mexico’s vehicle parc and the importance of independent retailers. Store owners cultivate neighborhood loyalty through installment financing and quick-service turnarounds, reinforcing a culture of proactive tire inspection. Manufacturers support this ecosystem with point-of-sale materials and warranty programs that simplify customer decision-making. Mobile fitting vans and online ordering platforms are emerging, broadening access beyond metropolitan hubs.

OEM sales are forecast to advance at a 4.06% CAGR, driven by localized auto assembly and stricter regional content criteria. Once a tire model is approved for a platform, it typically remains the factory fit for the vehicle’s life cycle, guaranteeing baseline volume for the supplier. Engineers collaborate early with automakers to meet ride-comfort targets and NVH requirements, fostering long-term technical partnerships. Promotional campaigns often emphasize the continuity between factory specifications and recommended replacement products, guiding owners back to the same brand.

By Rim Size: Mid-Range Foundation, Large-Diameter Appeal

The 15-to-20-inch category held the leading 60.12% Mexico tire market share in 2025, underpinned by its fitment across compact sedans, crossovers, and light trucks. Supply chains for this size band are fully optimized, ensuring steady availability at multiple price points. Styling updates from automakers occasionally shift consumer taste, yet functional considerations like ride comfort keep mid-range rims the default choice. Retailers carry extensive SKUs within this band to satisfy immediate walk-in demand, reinforcing its status as the sector’s commercial backbone. Brand messaging often focuses on value and dependability to cement loyalty in this mainstream tier.

Above-20-inch rims are expected to grow at a 6.55% CAGR, fueled by rising sales of luxury SUVs and visually commanding pickups that prioritize aesthetics and cornering stability. Designers showcase larger wheels in showroom displays, cementing consumer perception of premium status. Tire engineers respond with reinforced bead bundles and advanced sidewall compounds to support higher vehicle weights and lower aspect ratios. Dealer staff receive specialized training on mounting best practices to avoid rim damage, ensuring a seamless upgrade experience.

By Propulsion: ICE Backbone, BEV Surge

Internal combustion vehicles retained 83.14% of the 2025 unit demand, sustaining the core production mix for tire plants nationwide. Continuous incremental gains in rolling resistance and tread longevity keep these profiles competitive as fuel-economy norms tighten. Dealers maintain broad inventories to match the diverse array of existing models, ensuring quick replacement for everyday motorists. Educational outreach on rotation schedules and pressure checks reinforces good maintenance habits, safeguarding tread life.

Battery-electric vehicle tires are projected to grow at a 10.37% CAGR as charging infrastructure expands, and automakers launch new models. Engineers incorporate high-silica compounds and bead reinforcements to handle extra torque and curb weight, differentiating these lines from traditional products. Retail advisors highlight range-extending, low-rolling-resistance benefits when guiding early adopters through purchase decisions. Collaborative programs with charging-station operators create bundled maintenance packages that align service intervals with vehicle software alerts.

Geography Analysis

Central Mexico commanded 42.55% of the Mexico tire market share in 2025, supported by a mature cluster of assembly plants, component suppliers, and established logistics corridors linking industrial zones to key seaports. A dense aftermarket retail network centered around Mexico City and Guanajuato ensures ready access to consumers and fleets, reinforcing the region’s status as the commercial heartland of the sector[3]"An Overview of Mexico’s Major Industry Clusters," TACNA Services, tacna.net. Large multinationals leverage proximity to skilled labor and regulatory agencies to fast-track product certifications, further entrenching their operational foothold. While replacement cycles are stable, incremental growth now depends on premiumization and the roll-out of fleet-oriented digital services that can unlock hidden efficiencies for regional haulers and bus operators.

Northern Mexico is projected to record the fastest expansion at a 4.76% CAGR through 2031, propelled by near-shoring investments clustered in Nuevo León and Coahuila. New plants add capacity aimed at U.S. OEM programs, while regional governments partner with technical institutes to supply specialized labor. Cross-border freight corridors intensify tire wear on commercial fleets, stimulating demand for long-haul radials and retreads. The presence of well-organized industrial clusters accelerates knowledge transfer among suppliers, promoting the rapid adoption of advanced compounds and productivity practices. Moreover, mining operations in Sonora and Chihuahua require a steady pipeline of OTR products, creating additional pull for specialty lines.

South and Southeast Mexico remain comparatively small, yet infrastructure upgrades linking ports to inland manufacturing hubs are beginning to shift trade flows. Agricultural modernization programs drive selective uptake of tractor and harvester tires that must withstand harsh tropical conditions. Lower vehicle density tempers passenger-car replacement volumes, but rising tourism and inter-city bus traffic create pockets of opportunity for highway-grade commercial radials. Over time, enhanced road connectivity is expected to stimulate logistics activity, opening the door for broader aftermarket development and larger distribution footprints.

Competitive Landscape

Mexico’s tire market is moderately concentrated, with leading global brands capturing most OEM fitments and premium aftermarket share. Their scale advantage enables early adoption of smart-tire technologies, advanced materials, and sustainability initiatives such as closed-loop recycling partnerships. Local subsidiaries benefit from strong brand recognition, established dealer relationships, and access to proprietary R&D pipelines that deliver incremental performance gains crucial for modern vehicle platforms.

Cost-focused challengers from Asia and regional producers occupy the budget and mid-tier spaces, leveraging competitive labor and import pricing to win over price-sensitive replacement shoppers. Anti-dumping measures have narrowed but not eliminated their cost edge, prompting these firms to emphasize quick SKU rotation and aggressive promotions. Some are exploring local assembly partnerships to qualify for regional trade benefits and improve lead-time responsiveness.

Strategic white space centers on EV-specific compounds, airless architectures, and circular-economy solutions that align with tightening sustainability mandates. Brands investing early in local compounder capacity, telematics-enabled fleet services, and end-of-life collection frameworks are positioned to capture emerging profit pools as regulatory and customer expectations evolve. Industry observers note growing collaboration between tire makers, recyclers, and academic institutions to commercialize alternative rubber sources and accelerate eco-design certification pathways.

Mexico Tire Industry Leaders

-

Bridgestone de México S.A. de C.V.

-

Goodyear Tire & Rubber Company México

-

Michelin Mexicana S.A. de C.V.

-

Continental Tire de México S.A. de C.V.

-

Pirelli Neumáticos de México

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lummus Technology made a strategic investment in InnoVent Renewables, aiming to accelerate the rollout of its proprietary tire-recycling technology.

- June 2025: Sailun Group kicked off trial runs at its newly established plant in Mexico, gearing up for commercial production slated for later this year.

- June 2025: Aztema, a joint venture with 51% ownership by China's Sailun and 49% by Mexico's Tire Direct, began operations at its new tire manufacturing facility in Irapuato, Guanajuato. The plant, bolstered by a USD 400 million investment, aims to produce 6 million tires annually for both domestic and international markets.

Mexico Tire Market Report Scope

The Mexican Tire Market is analyzed based on season, tire design, vehicle type, application, end-user, rim size, propulsion, and geography.

By Season, the market is segmented into Summer, Winter, and All-Season. By Tire Design, the market is segmented into Radial, Bias, and Non-pneumatic. By Vehicle Type, the market is segmented into Passenger, Light Commercial, Heavy Commercial, Two-Wheelers, and Off-the-Road. By Application, the market is segmented into On-Road and Off-Road (OTR). By End User, the market is segmented into OEM and Aftermarket. By Rim Size, the market is segmented into below 15 inches, 15-20 inches, and above 20 inches. By Propulsion, the market is segmented into Internal Combustion Engine (ICE), Battery-Electric, Hybrid, and Others. By Geography, the market is segmented into Northern Mexico, Central Mexico, and South and Southeast Mexico.

Market forecasts are provided in terms of Value (USD) and Volume (Units).

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Two-Wheelers |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 - 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| Northern Mexico |

| Central Mexico |

| South and Southeast Mexico |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Two-Wheelers | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | Original Equipment Manufacturer (OEM) |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 - 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles | |

| By Geography | Northern Mexico |

| Central Mexico | |

| South and Southeast Mexico |

Key Questions Answered in the Report

How big is the Mexico tire market in 2026 and how fast is it growing?

The market is valued at USD 5.54 billion in 2026 and is projected to reach USD 6.49 billion by 2031, reflecting a 3.21% CAGR.

Which tire segment holds the largest share in Mexico?

All-Season tires account for 67.12% of 2025 sales, driven by their year-round versatility.

What is the fastest-growing tire design in Mexico?

Non-pneumatic/Airless tires are expected to expand at a 6.17% CAGR through 2031 as fleet operators seek puncture-free uptime.

Which region of Mexico shows the strongest growth prospects?

Northern Mexico leads with a forecasted 4.76% CAGR, supported by near-shoring investments and cross-border logistics demand.

Page last updated on: