Mexico Heavy-Duty Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

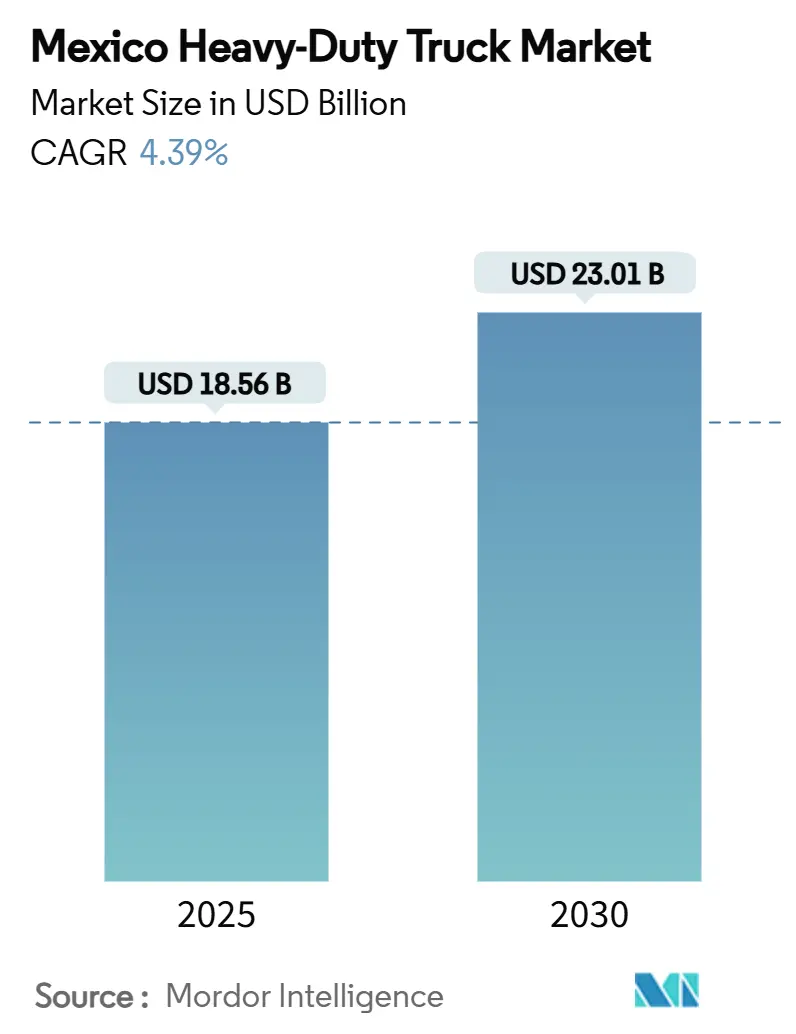

| Market Size (2025) | USD 18.56 Billion |

| Market Size (2030) | USD 23.01 Billion |

| Growth Rate (2025 - 2030) | 4.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Heavy-Duty Truck Market Analysis by Mordor Intelligence

The Mexico Heavy-Duty Truck Market sits at USD 18.56 billion in 2025 and is projected to reach USD 23.01 billion by 2030, delivering a 4.39% CAGR. Cross-border freight volumes have climbed 62.6% since 2017, underscoring how nearshoring is stretching long-haul capacity and pushing carriers to renew fleets with higher-payload tractors that conform to U.S. bridge-formula limits. Internal-combustion technology remains dominant, yet NOM-044 regulations, aligned with U.S. EPA 2010, are accelerating a 15.32% electric-truck CAGR as large shippers tighten sustainability mandates. Central-Bajío commands the largest regional share due to its dense automotive cluster, while Western Mexico is growing fastest on the back of Pacific-port expansions. Market concentration is high: Daimler, PACCAR, and Navistar collectively hold a 61% share, giving incumbents the scale to absorb compliance costs and bundle digital services that lock in customer loyalty.[1]“BTS Data Reveals Long-Term Trend Emerging in North American Freight Trucking,” Bureau of Transportation Statistics, bts.gov

Key Report Takeaways

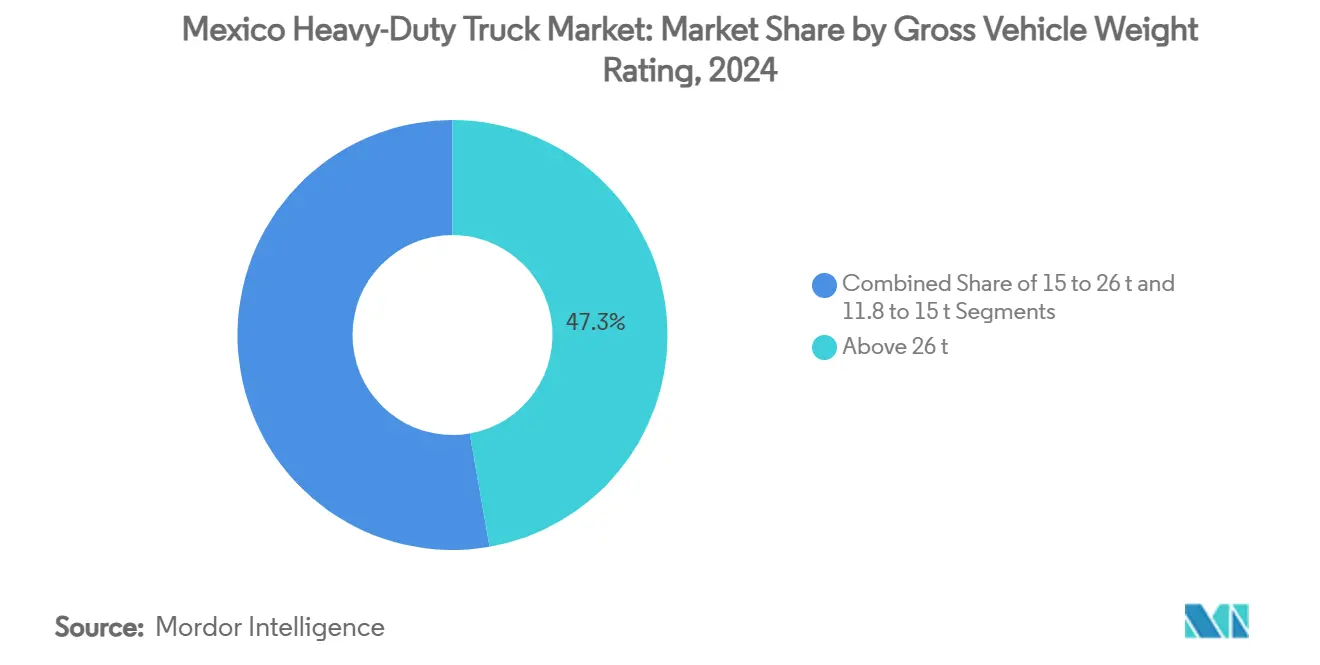

- By gross vehicle weight rating, the above-26-ton segment led with 47.25% of the Mexico Heavy-Duty Truck market share in 2024, and the 15-26 ton class is projected to advance at a 9.05% CAGR through 2030.

- By propulsion, internal-combustion engines controlled 92.49% of the Mexican heavy-duty Truck market size in 2024, while electric trucks are poised for a 15.32% CAGR to 2030.

- By axle configuration, 6×4 vehicles held 51.46% share of the Mexico Heavy-Duty Truck Market in 2024, whereas 4×2 trucks are set to expand at 7.38% CAGR by 2030.

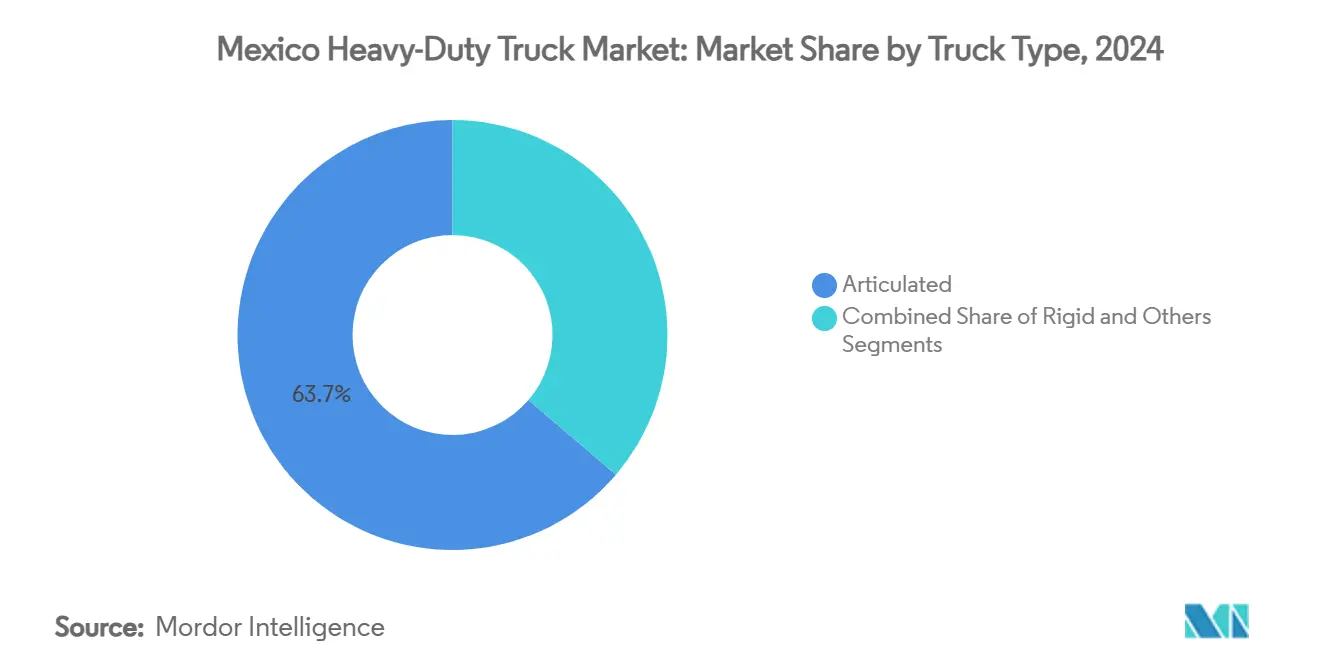

- By truck type, articulated models captured 63.74% of the Mexico Heavy-Duty Truck market share in 2024, and rigid trucks are expected to grow at 8.13% CAGR through 2030.

- By application, freight and logistics accounted for a 53.91% share of the Mexico Heavy-Duty Truck market size in 2024, but urban freight is forecast to post a 9.81% CAGR between 2025-2030.

- By region, Central-Bajío held 37.54% share of the Mexico Heavy-Duty Truck Market in 2024 while Western Mexico will register the strongest 8.11% CAGR to 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with Mexico being one of the contributors. Our global heavy duty trucks market size represents that cumulative total.

Mexico Heavy-Duty Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Freight Boom | +1.8% | Northern Mexico, Central-Bajío, Western Mexico | Medium term (2-4 years) |

| Manufacturing-Export Expansion | +1.2% | Central-Bajío, Western Mexico, Northern Mexico | Long term (≥ 4 years) |

| Infrastructure Megaproject Pipeline | +0.9% | Western Mexico, Gulf Coast, South, and Southeast | Long term (≥ 4 years) |

| Stricter NOM-044 Emissions Norms | +0.7% | Central-Bajío, Northern Mexico, Western Mexico | Short term (≤ 2 years) |

| Growing CNG Corridor Network | +0.5% | Northern Mexico, Gulf Coast, Central-Bajío | Medium term (2-4 years) |

| "Truck-as-a-Service" Fintech Platforms | +0.3% | Central-Bajío, Northern Mexico, Western Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nearshoring-led Cross-Border Freight Boom

Cross-border truck volumes have risen 62.6% since 2017, with the Laredo gateway alone processing 2.93 million tractor-trailers yearly, roughly 40% of all land freight between both nations. Foreign direct investment inflows and shifting sourcing away from Asia have entrenched Mexico as the preferred manufacturing back-office for U.S. clients. Consistent northbound demand enables carriers to deploy fully utilized above-26-ton assets, feeding sequential upgrades of fleets in the Mexico Heavy-Duty Truck Market. Nearshoring also drives predictable backhaul opportunities that support pricing discipline and improved asset-turn metrics. The structural nature of reshoring suggests durable volume tailwinds over the medium term.

Manufacturing-Export Expansion Lifting Domestic Demand

Heavy-duty truck output hit 195,789 units in 2024, 83% of which headed for U.S. dealerships, yet the domestic multiplier effect is meaningful as supply chains shuttle parts among Nuevo León, Guanajuato, and Jalisco. Employment in automotive and allied sectors tops 1 million, underpinning steady origin-destination lanes that sustain the Mexico Heavy-Duty Truck Market. OEM green-field investment, such as Volvo’s Monterrey plant set to start production in 2026, adds facility-to-port traffic and fresh demand for tractors built to U.S. specifications. Export orientation, therefore, safeguards local carrier utilisation even during domestic slowdowns, anchoring baseline freight volumes.

Federal Infrastructure Megaproject Pipeline

A USD7.5 billion investment from the Mexican government for the 303 km Interoceanic Corridor rail line requires sustained inbound cement, steel, and machinery flows for construction phases before pivoting to container drayage once operational[2]"Mexico: The High-Speed Railway Project That Challenges the Panama Canal", Webuild, webuildvalue.com. Port expansions at Manzanillo are slated to lift capacity to 10 million TEUs by 2030, necessitating dense trucking links for hinterland dispersal. Highway and energy corridors in the Gulf Coast and Southeast further extend lane density, broadening the geographic footprint of the Mexico Heavy-Duty Truck Market. Infrastructure outlays thus create a two-stage demand cycle: immediate construction haulage followed by recurring freight once assets go live.

Stricter NOM-044 Emission Norms Driving Fleet Renewal

All new heavy-duty vehicles must now meet filter-based standards equivalent to U.S. EPA 2010, imposing significant cuts in particulate and NOx outflow. Compliance elevates the total cost of ownership of legacy diesel units, prompting carriers to shorten replacement cycles. Average fleet age stands at 25 years, revealing sizeable pent-up replacement potential in the Mexico Heavy-Duty Truck Market. Engine leader Cummins reinforced local capacity to supply Euro VI-caliber powertrain kits, assuring carriers of parts availability. Early adopters also gain cross-border flexibility since their rigs mirror U.S. regulatory thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certified Heavy-Duty Driver Shortage | -1.1% | Northern Mexico, Central-Bajío, Western Mexico | Short term (≤ 2 years) |

| High Cost and Sparse Charging Facility | -0.8% | Central-Bajío, Western Mexico, Northern Mexico | Medium term (2-4 years) |

| Peso Volatility | -0.6% | Northern Mexico, Central-Bajío, Western Mexico | Short term (≤ 2 years) |

| Border Wait-Times | -0.4% | Northern Mexico, Western Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Heavy-Duty Drivers

Mexico is short 54,000 credentialed drivers; Nuevo León alone needs 20,000 more to satisfy nearshoring lanes. English-language rules for cross-border hauls disqualify many domestic operators, tightening capacity on high-yield U.S. routes. Carrier wage bills are climbing as fleets bid aggressively for licensed talent, which erodes margins in the Mexico Heavy-Duty Truck Market. Although accredited schools train roughly 105,000 recruits yearly, churn offsets much of that inflow. Labor shortages, therefore, curtail the speed at which carriers can scale asset counts even when freight demand is robust.

High Upfront Cost and Sparse Charging for E-Trucks

Only 8.2% of Mexico’s 39,257 charging points are public-access, offering little support for line-haul duty cycles. The total cost of ownership of battery rigs remains elevated relative to diesel due to high capex and limited resale markets. Government electrification road-maps exist, yet execution lags, slowing penetration beyond pilot fleets. Carriers therefore defer large orders until a credible charging corridor emerges; this stalls the 15.32% electric-truck CAGR potential implicit in regulatory targets. Infrastructure gaps will likely persist through the medium term, tempering rapid electrification within the Mexico Heavy-Duty Truck Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gross Vehicle Weight Rating: Heavy-Haul Dominance Drives Demand

The above-26-ton category represented 47.25% of 2024 revenue and remains the anchor of the Mexico Heavy-Duty Truck Market, largely because cross-border freight favors higher payload utilisation. The Mexico Heavy-Duty Truck market size for this band is forecast to grow alongside nearshoring corridors that demand 53-ft trailers and double-stack container assignments. Meanwhile, the 15-26 ton range will lead gains at 9.05% CAGR as e-commerce hubs in Guadalajara and Monterrey rely on mid-weight units that balance manoeuvrability with pallet capacity. Heavier vehicles also dovetail with U.S. axle-load regulations, simplifying bilateral fleet rotation.

The structural emphasis on export manufacturing necessitates reliable high-capacity tractors that can shuttle stamped parts, finished vehicles, and electronics directly to border crossings. Leasing products, including Daimler’s all-inclusive e360 programme, lower entry barriers for SMEs wishing to tap this segment. As a result, carriers favour extended wheel-base, high-horsepower builds that can withstand 1,200 km daily duty cycles. The Mexico Heavy-Duty Truck Market thus skews toward high-tonnage specifications even as lighter niches gain relevance in city logistics.

By Propulsion Type: ICE Dominance Faces Electric Disruption

Internal-combustion powertrains prevailed with 92.49% revenue in 2024, cementing diesel as the workhorse of the Mexico Heavy-Duty Truck Market. Even so, electric units are projected to clock a 15.32% CAGR, helped by tax incentives on zero-emission imports and the roll-out of fast-charge depots within industrial parks. The Mexico Heavy-Duty Truck market share of electric models remains modest at present, but is set to expand as OEMs align launch timelines with 2028 emissions caps.

CNG options offer a transitional pathway in regions where natural-gas pipeline density is improving, such as Tamaulipas and the Gulf Coast. Nevertheless, fleet operators cite range anxiety and payload penalties as deterrents to early electric adoption. Government-backed tender frameworks that pair vehicle purchase with depot-level chargers could unlock scale. Over the forecast period, drivetrain diversity will intensify, but diesel will still underpin most cross-border lanes that demand 1,600 km range per refuel.

By Axle Type: Configuration Flexibility Meets Operational Demands

In 2024, the 6×4 design captured 51.46% of unit shipments, offering traction suitable for mountainous routes linking the Bajío plateau with Pacific ports. The Mexico Heavy-Duty Truck market size for 4×2 rigs is expanding rapidly, supported by urban-freight niches where turning radius outweighs fifth-wheel capacity. Customised 6×2, 6×6, and 8×6 builds cater to mining operations in Sonora and infrastructure projects in Oaxaca, though volumes remain comparatively limited.

Fleet managers increasingly order modular axle layouts that can be retro-configured for seasonal contracts. Electronic lift-axle technology also boosts fuel economy by reducing rolling resistance on partial loads. Regulation harmonisation with the United States continues to influence Mexican specification trends, reinforcing demand for 6×4 and 6×2 tractors that align with U.S. bridge-formula limits.

By Truck Type: Articulated Leadership Reflects Long-Haul Focus

Articulated combinations delivered 63.74% sales in 2024, reflecting the Mexico Heavy-Duty Truck Market’s orientation toward long-haul, high-cube freight flows. Swappable trailer pools cut dwell time at yards along the Monterrey-Laredo super-corridor, amplifying asset productivity. Rigid trucks, however, are set for an 8.13% CAGR as last-mile networks proliferate within the Mexico City megaregion.

OEM investment remains geared toward conventional articulated frames to satisfy export demand; Volvo’s Monterrey plant will exclusively build Class-8 tractors calibrated for NAFTA-wide regulations. Rigid chassis gains come from construction fleets and municipal services that value integrated bodies for concrete mixing, refuse hauling, and tanker assignments. Expect incremental growth from specialty niches such as hydrogen-fuelled rigs servicing mountainous mining enclaves.

By Application: Freight-Logistics Dominance Amid Urban Growth

Freight and logistics represented 53.91% revenue in 2024, underscoring international supply-chain interdependence within the Mexico Heavy-Duty Truck Market. Automakers, electronics assemblers, and appliance brands rely on predictable just-in-time deliveries to U.S. assembly hubs. Urban freight will log a 9.81% CAGR as e-commerce penetration lifts parcel density across Tier-1 metros. The Mexico Heavy-Duty Truck market size for construction and mining remains steady, buoyed by megaprojects and commodity cycles.

Growth in refrigerated pharma distribution and petrochemical shuttle runs in the Gulf Coast region also widens the application mix. Carriers are integrating telematics to optimise city-centre drop-off windows and comply with congestion curfews. Consequently, specialised bodies, refrigerated, tanker, and tipper, will diversify fleet architecture beyond generic dry-van specs.

Geography Analysis

In 2024, Central-Bajío dominated the Mexican heavy-duty truck market with a commanding 37.54% share, solidifying its reputation as the nation's industrial nucleus. Its strategic location, nestled between the Pacific and Gulf ports and surrounded by dense OEM clusters, not only curtails empty miles but also ensures optimal tractor utilization. Carriers, capitalizing on tollway redundancies, guarantee timely border crossings, bolstering their ability to command premium contract rates.

Western Mexico is poised for an 8.11% CAGR, driven by upgrades at the Manzanillo port and foreign direct investments in the tech sector flooding into Jalisco. As exporters sidestep congestion at Gulf gateways, opting for swifter routes to Asia, the heavy-duty truck market in this corridor witnesses notable growth. Additionally, highway expansion projects along the Guadalajara–Colima route amplify the region's logistical allure.

While Northern Mexico serves as the primary hub for cross-border activities, its growth rate trails behind that of the Pacific coast. However, reforms in border processing and the introduction of pre-clearance programs are slashing truck idling times, enhancing fleet productivity. Meanwhile, burgeoning demand in the Gulf Coast and the South/Southeast regions, driven by LNG projects and tourism-focused rail lines, hint at a future diversification in the geographic revenue streams for the Mexican heavy-duty truck market.

Coverage of the heavy duty trucks market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe and Africa, alongside detailed country-level intelligence for United States and Saudi Arabia, each shaped by local operating conditions.

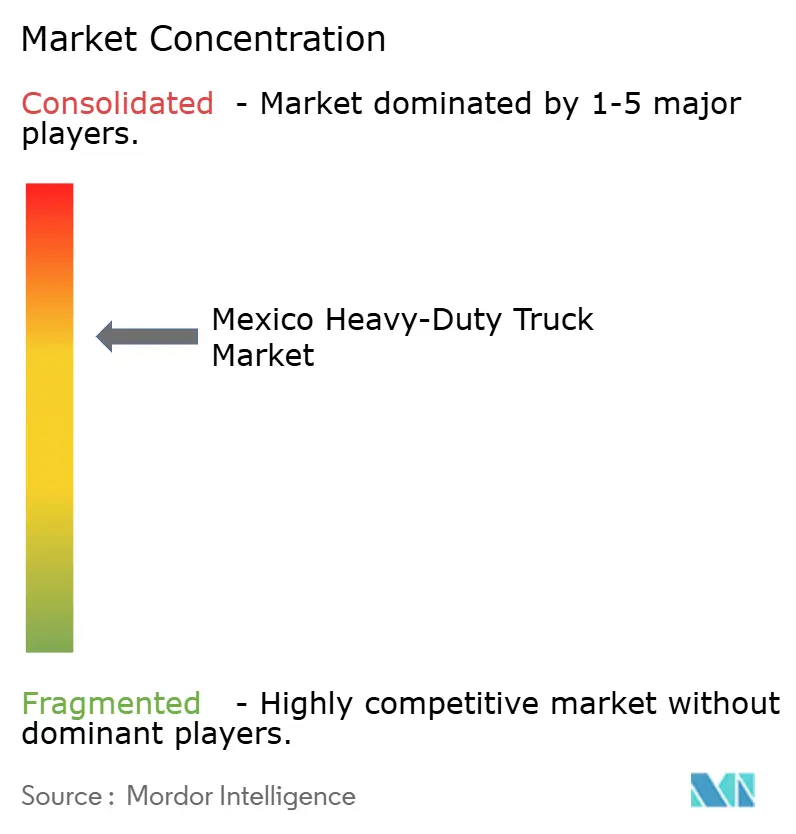

Competitive Landscape

The top three OEMs command a significant combined share, underscoring a high concentration. Scale advantages enable incumbents to amortize NOM-044 compliance costs across larger build volumes, thereby reinforcing their price leadership. Daimler’s digital-services bundle attaches AI-driven fuel-efficiency analytics and predictive maintenance to each truck sale, converting one-off hardware deals into annuity revenue streams.

Software-defined truck architectures are emerging; Daimler Truck and Volvo Group have formed a joint venture to co-develop common code platforms that enable over-the-air feature unlocks. Such moves raise switching costs for fleet operators who become embedded in proprietary ecosystems.

Challenger brands from China are building CKD plants to localise cost structures, while fintech start-ups finance working capital gaps among small carriers. The confluence of new capital models and lower-priced imports could erode incumbent share at the margin, yet entrenched after-sales networks and resale-value reputations still tilt buyer preference toward legacy OEMs within the Mexico Heavy-Duty Truck Market.

Mexico Heavy-Duty Truck Industry Leaders

-

Daimler Trucks AG

-

PACCAR Inc

-

Navistar International

-

Volvo Trucks

-

Mack Trucks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Volvo Group confirmed its USD 700 million heavy-duty truck plant in Monterrey will proceed, with series production slated for 2026.

- December 2024: Stellantis announced USD 1.6 billion upgrades to Toluca and Saltillo complexes, earmarked for electric-vehicle output.

- August 2024: Daimler Truck Mexico unveiled its e360 electric tractor alongside an upgraded Enlace Freightliner telematics suite.

Mexico Heavy-Duty Truck Market Report Scope

| 11.8 to 15 t |

| 15 to 26 t |

| Above 26 t |

| Internal-Combustion (ICE) | Diesel |

| Natural Gas (CNG/LNG) | |

| Electrified | Battery-Electric (BEV) |

| Hybrid and Plug-in Hybrid (HEV and PHEV) | |

| Fuel-Cell Electric (FCEV) |

| 4x2 |

| 6x4 |

| 6x2 |

| 6x6 |

| 8x6 |

| 8x8 |

| Others |

| Rigid |

| Articulated |

| Others |

| Construction and Mining |

| Freight and Logistics |

| Long Haul |

| Other |

| Northern Mexico |

| Central-Bajío |

| Western Mexico |

| Gulf Coast |

| South and Southeast |

| By Gross Vehicle Weight Rating | 11.8 to 15 t | |

| 15 to 26 t | ||

| Above 26 t | ||

| By Propulsion Type | Internal-Combustion (ICE) | Diesel |

| Natural Gas (CNG/LNG) | ||

| Electrified | Battery-Electric (BEV) | |

| Hybrid and Plug-in Hybrid (HEV and PHEV) | ||

| Fuel-Cell Electric (FCEV) | ||

| By Axle Type | 4x2 | |

| 6x4 | ||

| 6x2 | ||

| 6x6 | ||

| 8x6 | ||

| 8x8 | ||

| Others | ||

| By Truck Type | Rigid | |

| Articulated | ||

| Others | ||

| By Application | Construction and Mining | |

| Freight and Logistics | ||

| Long Haul | ||

| Other | ||

| By Region | Northern Mexico | |

| Central-Bajío | ||

| Western Mexico | ||

| Gulf Coast | ||

| South and Southeast | ||

Key Questions Answered in the Report

What is the current value of the Mexico Heavy-Duty Truck Market?

The market is worth USD 18.56 billion in 2025 and is projected to reach USD 23.01 billion by 2030.

Which truck weight segment holds the largest share?

Trucks above 26 tons captured 47.25% of 2024 revenue, reflecting demand for high-payload cross-border hauls.

How dominant are diesel engines in Mexico’s heavy-duty fleet?

Internal-combustion powertrains held 92.49% share in 2024, but electric variants are forecast for a 15.32% CAGR to 2030.

Which region is growing fastest for truck demand?

Western Mexico is expected to post the highest 8.11% CAGR through 2030 on the back of Pacific-port investments.

What is the key regulatory driver shaping new-truck demand?

NOM-044 emission rules that mirror U.S. EPA 2010 standards are accelerating fleet renewal with cleaner technologies.

Page last updated on: