North America OTR Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 6.11 Billion |

| Market Size (2030) | USD 7.69 Billion |

| Growth Rate (2025 - 2030) | 4.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America OTR Tire Market Analysis by Mordor Intelligence

The North America OTR Tire Market size is estimated at USD 6.11 billion in 2025, and is expected to reach USD 7.69 billion by 2030, at a CAGR of 4.71% during the forecast period (2025-2030). Sustained highway modernization under the Infrastructure Investment and Jobs Act, renewed mining investment aimed at green-metals production, and rapid port-automation rollouts at Long Beach and Los Angeles form the backbone of this expansion. Fleet managers are lengthening asset life cycles, which keeps aftermarket volumes high even as OEM demand rebounds alongside autonomous haulage system uptake. Technology-rich radial designs, tire-pressure monitoring, and predictive analytics now anchor competitive differentiation, while anti-dumping tariffs on Chinese imports at a higher rate are reshaping sourcing strategies.

Key Report Takeaways

- By tire type, radial products captured 55.67% of the North America OTR tire market share in 2024, growing at a 4.72% CAGR through 2030.

- By equipment type, earthmovers led with a 28.13% of the North America OTR tire market share in 2024; loaders and dozers posted the fastest trajectory, at a 4.81% CAGR to 2030.

- By rim size, 31–40 inches dominated with 43.37% of the North America OTR tire market share in 2024, while above 45 inches are expanding at a 4.77% CAGR through 2030.

- By industry, Construction accounted for 34.51% of the North America OTR tire market share in 2024; port operations represent the fastest-growing pocket, with a 4.78% CAGR to 2030.

- By material type, Natural rubber retained 68.82% of the North America OTR tire market share in 2024, whereas synthetic rubber compounds are advancing at a 4.73% CAGR through 2030.

- By distribution channel, the aftermarket controlled 57.88% of the North America OTR tire market share in 2024, and OEM sales are set to rise at a 4.83% CAGR through 2030.

- By country, the United States held an 83.41% of the North America OTR tire market share in 2024 and is projected to climb at a 4.75% CAGR to 2030.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on otr tire market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America OTR Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Infrastructure Investment | +1.2% | US core, spillover to Canada and Mexico | Medium term (2-4 years) |

| Mining Output Rebound And Green-Metals Demand | +0.9% | US mining regions, Canadian resource corridors | Long term (≥ 4 years) |

| Growing Farm Mechanization Rates | +0.7% | US Midwest, Canadian Prairies, Mexico agricultural zones | Long term (≥ 4 years) |

| Surge In Port-Automation Fleets | +0.6% | West Coast ports, Gulf Coast terminals | Short term (≤ 2 years) |

| TPMS-Enabled Premium Radial OTR Tire Adoption | +0.5% | North America fleet operations, mining corridors | Medium term (2-4 years) |

| Autonomous Haulage System Tire Demand Spike | +0.4% | US mining regions, Canadian resource extraction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infrastructure Investment In Road & Industrial Projects

Federal spending channeled through the Infrastructure Investment and Jobs Act translates into higher utilization of graders, compactors, and earthmovers, which in turn lifts replacement cycles for large-diameter OTR tires[1]“Fact Sheet: Infrastructure Investment and Jobs Act,” White House, whitehouse.gov. Even though elevated interest rates forced many contractors to defer new-equipment purchases in 2024, they kept machines working by prioritizing tire replacement schedules, sustaining the aftermarket share within the North American OTR tire market. State-level grant programs for industrial parks also deploy forklift fleets that specify radial tires with telematics-ready sensors to contain downtime. Suppliers that align inventory with federally funded project corridors enjoy shorter lead times and improved pricing power.

Mining Output Rebound And Green-Metals Demand

Copper and lithium operations in Nevada, Arizona, and British Columbia have ramped up load-haul cycles, boosting demand for 57-inch and 63-inch mining radials capable of supporting autonomous trucks[2]“Autonomous Haulage System Surpasses 10 Billion Tons Hauled,” Komatsu Ltd., komatsu.com. Komatsu’s autonomous fleet surpassed 10 billion tons hauled in 2025, validating the need for premium compounds that handle constant braking heat. The green-energy transition continues to favor miners extracting battery metals, and their capital budgets include multi-year tire-supply agreements that lock in volume commitments for Tier-1 brands. Predictive maintenance suites embedded in TPMS platforms are now standard on new trucks, providing tire makers with recurring software revenue streams alongside product sales.

Growing Farm Mechanization Rates

Despite a minimal fall in overall United States tractor sales in 2024, four-wheel-drive models with over 400 horsepower posted double-digit gains as growers traded for efficiency. Machines such as the Case IH Steiger 715 require wider flotation tires or dual IF/VF sets that distribute weight and reduce soil compaction, leading to larger unit values per wheel position. Canadian Prairie growers mirrored this shift, quickly increasing four-wheel-drive registrations even as total tractor volumes fell[3]“Canadian Tractor Sales 2024,” Agriculture and Agri-Food Canada, agr.gc.ca. Agronomic service providers now advise GPS-based inflation adjustment, which favors sensor-equipped radials. The North America OTR tire market, therefore, captures a structural upswing in premium farm fitments even when total acres planted remain flat.

Surge In Port-Automation Fleets (Straddle Carriers, RTGs)

Automated container yards are moving from pilot to commercial scale, exemplified by the Port of Long Beach’s zero-emission yard-tractor project. Straddle carriers and grid-tied RTG cranes consume specialized solid or radial tires designed for precise cornering and minimal rolling resistance under repetitive travel paths. Real-time load monitoring enables ports to schedule proactive tire swaps during lull windows, a capability that lifts demand for sensor-integrated products. As only 4% of global container handling capacity is automated today, early adopters in North America maintain steep learning curves that tire suppliers can monetize via on-site engineering support contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Natural-Rubber and Petrochemical Feedstock Prices | -0.8% | Global supply chains affecting North America | Short term (≤ 2 years) |

| Retread Market Cannibalization | -0.6% | US aftermarket, Canadian fleet operations | Medium term (2-4 years) |

| Anti-Dumping Tariffs On Imported OTR Tires | -0.4% | US import channels, cross-border trade | Short term (≤ 2 years) |

| Tightening Scrap-Tire Disposal and ESG Compliance Rules | -0.3% | North America regulatory jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Rubber & Petrochemical Feedstock Prices

Over four-fifths of the natural-rubber supply originates from Southeast Asia, where disease outbreaks and geopolitical risks produced sharp price swings in 2024. Synthetic rubber cost curves were just as erratic because benzene and butadiene input prices tracked crude oil volatility. North America-based tire makers responded by raising hedging ratios and shifting compound recipes, yet they still confronted margin compression when contracts locked in OEM pricing for up to 12 months. R&D teams are fast-tracking guayule and dandelion latex studies, but commercial volumes will not displace Asian sheet rubber before 2028.

Retread Market Cannibalization Of New-Tire Demand

Imported low-cost radials from Thailand and Vietnam reached price points within USD 200 of an equivalent retread in 2024, eroding casing demand for domestic retreaders. Even though mining sizes such as 33.00R51 maintain healthy pull-through, smaller contractors increasingly choose virgin imports because turnaround time trumps life-cycle economics. Retread shops face additional headwinds, including casing scarcity, skilled-labor shortages, and rising insurance premiums. Unless U.S. retreaders pivot to specialized niches or integrate sensor-ready compounds, the North America OTR tire market could see the retread share slip below the current one-tenth by 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tire Type: Radial Technology Drives Market Evolution

Radial designs commanded 55.67% of the North America OTR tire market share in 2024, as their steel-belted construction reduced rolling resistance and dissipated heat more effectively than bias ply alternatives. This edge translates into up to minimal fuel savings, offsets the higher acquisition price for large mining haulers and articulated dump trucks. Radial uptake scales further as OEMs integrate telematics sensors and fleet managers adopt predictive maintenance workflows. Bias tires remain relevant where sidewall flex and cut resistance eclipse ride quality, such as in abrasive quarry pits. Solid tire demand clusters around port equipment and indoor materials-handling vehicles, where puncture elimination drives the value proposition.

The above dynamics place radial tires on a 4.72% CAGR trajectory through 2030, while bias volumes inch forward. Premium brands package radial products with warranty extensions and on-site engineering audits, deepening customer stickiness. A handful of ports have started validating airless polyurethane cores for automated guided vehicles, though commercialization beyond pilot yards will likely occur after 2027.

By Equipment Type: Earthmovers Lead While Loaders Accelerate

Earthmovers topped equipment demand with 28.13% of the North America OTR tire market share in 2024, reflecting their foundational role in highway reconstruction and large-scale excavation. Their per-machine tire bill often exceeds USD 120,000, and life-cycle planning depends on rigorous TKPH (ton-kilometer per hour) calculations. Loaders and dozers exhibit the fastest growth at 4.81% CAGR through 2030, fueled by mining fleet modernization and civil-works subcontractors upgrading to higher breakout force platforms. Mine haul trucks consume ultra-class sizes but add only steady growth because pit expansions are gated by permitting schedules.

Across segments, autonomous retrofits place fresh stress on heat-cycle management since machines run longer shifts without operator breaks. This requirement favors premium compounds with advanced cooling ribs and enhances the revenue pool for remote inflation monitoring subscriptions.

By Rim Size: Large Diameter Growth Reflects Equipment Scaling

Rims in the 31–40 inch band captured 43.37% of the North America OTR tire market share in 2024, underscoring their versatility across 40-ton articulated trucks, wheel loaders, and midsize graders. The more than or equal to 45-inch band is set to clock the highest 4.77% CAGR because next-generation mining haulers deploy 57-inch or larger assemblies to move 400-plus-ton payloads. Uprated ply ratings and higher TKPH thresholds are central specs in bid tenders.

Smaller than 30-inch sizes still populate skid steers and compact backhoes that surged during residential buildouts before interest rates spiked. However, aftermarket churn remains brisk because these machines experience abrasive job-site wear. Mid-range 41–45 inch fitments serve mid-tier dump trucks popular at aggregates quarries, where operating payload trumps haul distance.

By Industry: Construction Leads While Ports Surge

Construction projects delivered 34.51% of the North America OTR tire market share in 2024, as state DOT contracts and private warehouse builds continued amid cost-inflation headwinds. OEM placements moderated because contractors deferred new iron, but replacement cycles progressed uninterrupted. Although smaller in absolute volumes, port operations register the swiftest 4.78% CAGR through 2030 thanks to battery-electric yard tractors and stacker cranes requiring high-stability tires.

Mining accounts for roughly one-quarter of the North American OTR tire market, and its long-duration supply contracts ensure volume predictability. Agriculture faces secular consolidation of farms, yet upgrades to larger horsepower keep dollar spending consistent. Industrial segments, including steel mills, waste management, and forestry, provide countercyclical ballast, smoothing demand during construction lulls.

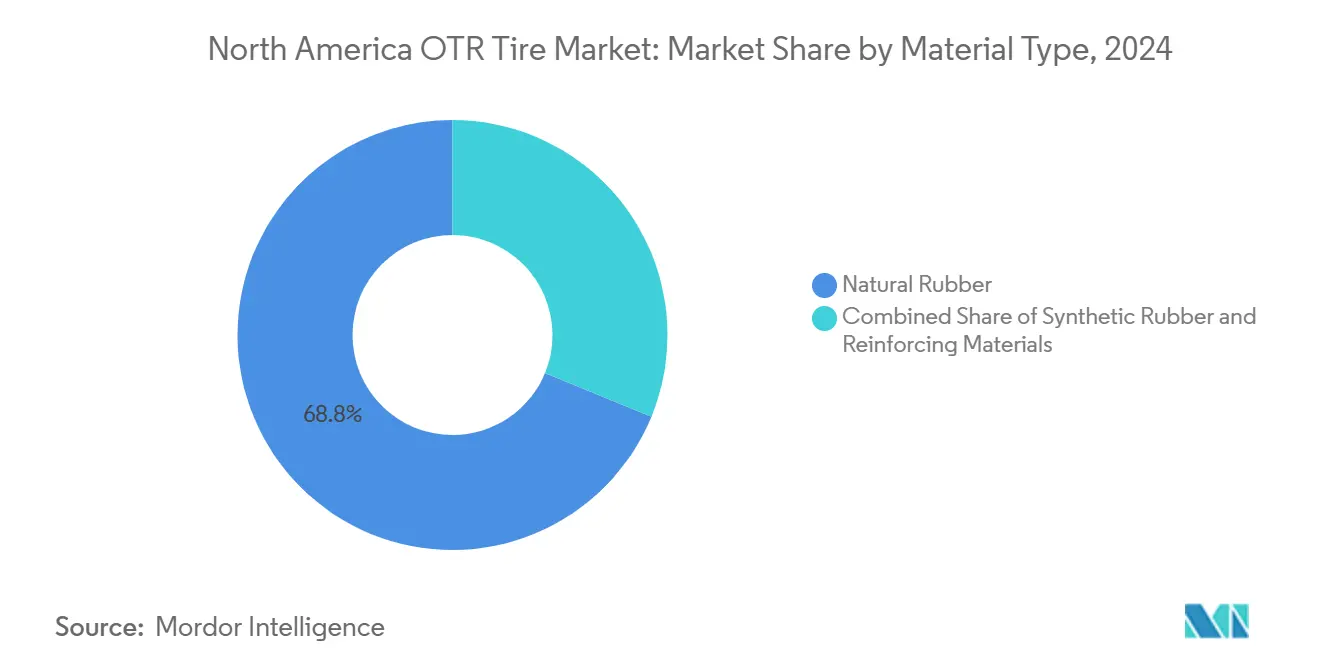

By Material Type: Natural Rubber Dominance Faces Synthetic Growth

Natural rubber delivered 68.82% of the North America OTR tire market in 2024, favored for heat resistance in 24-hour mining duty cycles. Synthetic rubber, led by SBR and polybutadiene blends, should log a 4.73% CAGR through 2030 because it hedges supply risk and enables compound tweaks for extreme cold or chemical exposure. Advanced aramid and steel reinforcements raise load indexes without excessive weight gain, which is key for autonomous haulage that targets tighter energy budgets.

Mixing plants run digital twin simulations to adjust real-time recipes against commodity price feeds. The North America OTR tire industry is further experimenting with recycled crumb rubber infusion to hit OEM sustainability KPIs, though adoption remains limited to non-critical bead zones.

By Distribution Channel: Aftermarket Dominance Reflects Fleet Optimization

Aftermarket avenues moved 57.88% of the North America OTR tire market in 2024 as fleets stretched equipment life cycles during high-interest conditions. National dealer consolidators leverage bulk buying to secure allocation from Tier-1 brands, while smaller independents maintain niche services like foam fill and on-site sectional repair. OEM shipments will outpace at a 4.83% CAGR because autonomous trucks and port cranes require factory-integrated sensor gateways.

Digital ordering portals reduce stock-keeping costs by predicting replacement windows via telematics feeds. Tire makers that couple product supply with cloud-based monitoring win bundled contracts that command 8 to 12% price premiums over spot transactions.

Geography Analysis

North America’s OTR tire market exhibits pronounced regional specialization. The United States alone accounts for 83.41% of the North American OTR tire market in 2024 and is projected to climb at a 4.75% CAGR to 2030 due to continuous highway reconstruction and a mining sector targeting battery-metal output. California’s Los Angeles and Long Beach ports anchor early-stage zero-emission yard-tractor deployments that demand solid or specialty radial tires with heat-resistant tread patterns.

Canada follows with a strong resource-sector orientation. Oil-sands producers operate ultra-class haulers with 63-inch rubber. At the same time, Prairie farmers upgrade to high-horsepower tractors with flotation tires to maximize short planting windows. Northern mine sites impose severe cold-crack constraints, pushing manufacturers to deploy aramid-reinforced sidewalls rated to –50 °C.

Mexico’s profile skews toward agriculture and export-manufacturing. Tomato and avocado growers adopt VF 710/70R38 tires that cut soil compaction, and new logistics parks along the Bajío corridor require forklift radials rated for high-cycle use. Local production capacity expansion shortens lead times and cushions currency fluctuations, attracting OEM assemblers seeking near-shore supply chains.

Competitive Landscape

Strategic consolidation is reshaping rivalry. Yokohama’s purchase of Goodyear’s OTR unit in February 2025 vaulted it to second place in North America. CEAT’s acquisition of Camso’s OTR range in December 2024 extends its reach into the construction and agriculture segments. Despite divesting Camso, Michelin retains a premium mining share via its XDR3 line and supplements it with digital services like MEMS Evo.

Bridgestone invested heavily in scaling its Mastercore technology and released the VRDU quarry tire in March 2025, touting better cut resistance. Continental secured Caterpillar’s factory approval for 49-inch haul-truck fitments, underscoring the value of OEM endorsements. Chinese entrants Triangle and Sailun pursue price-sensitive accounts yet face a heavy anti-dumping wall that limits direct imports. Instead, they eye Mexican production to skirt tariff barriers.

Competition increasingly revolves around data platforms. Kal Tire’s TireSight and Continental’s Bluetooth-enabled sidewalls deliver real-time TKPH analytics, giving fleets actionable insights to prevent heat separation events. Vendors that monetize algorithms alongside rubber are securing multi-year tenders covering both tires and monitoring subscriptions, a model that could lift total contract value per haul truck.

North America OTR Tire Industry Leaders

Bridgestone Corporation

Michelin

Continental AG

The Goodyear Tire & Rubber Company

Yokohama Rubber Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bridgestone launched the Mastercore VRDU tire tailored for the aggregate segment, enhancing durability for high-chip environments.

- December 2024: CEAT acquired Camso’s OTR business from Michelin for USD 225 million to deepen its off-highway presence.

- July 2024: Yokohama completed its USD 905 million acquisition of Goodyear’s OTR assets, expanding its specialty portfolio in North America.

North America OTR Tire Market Report Scope

| Radial OTR Tires |

| Bias OTR Tires |

| Solid OTR Tires |

| Earthmovers |

| Loaders & Dozers |

| Dump Trucks |

| Tractors |

| Forklifts |

| Graders |

| Others |

| Below 31 Inches |

| 31–40 Inches |

| 41–45 Inches |

| Above 45 Inches |

| Construction |

| Mining |

| Agriculture |

| Industrial |

| Port Operations |

| Others |

| Natural Rubber |

| Synthetic Rubber |

| Reinforcing Materials |

| OEM |

| Aftermarket |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Tire Type | Radial OTR Tires |

| Bias OTR Tires | |

| Solid OTR Tires | |

| By Equipment Type | Earthmovers |

| Loaders & Dozers | |

| Dump Trucks | |

| Tractors | |

| Forklifts | |

| Graders | |

| Others | |

| By Rim Size | Below 31 Inches |

| 31–40 Inches | |

| 41–45 Inches | |

| Above 45 Inches | |

| By Industry | Construction |

| Mining | |

| Agriculture | |

| Industrial | |

| Port Operations | |

| Others | |

| By Material Type | Natural Rubber |

| Synthetic Rubber | |

| Reinforcing Materials | |

| By Distribution Channel | OEM |

| Aftermarket | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North American OTR tire market in 2025?

The market stands at USD 6.11 billion and is projected to reach USD 7.69 billion by 2030.

Which tire type is growing fastest?

Radial OTR tires lead with a 4.72% CAGR through 2030, driven by fuel efficiency and TPMS compatibility.

What impact do anti-dumping duties have on supply?

High Tariffs rates on Chinese imports push sourcing toward North American and Mexican production sites.

Why is port automation necessary for tire demand?

Straddle carriers and electric RTG cranes require specialized, sensor-ready tires, giving port operations a 4.78% CAGR.

Which companies made major acquisitions recently?

Yokohama bought Goodyear’s OTR unit, and CEAT purchased Camso’s OTR range.

Page last updated on: