Meperidine Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 608.18 Million |

| Market Size (2031) | USD 736.58 Million |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

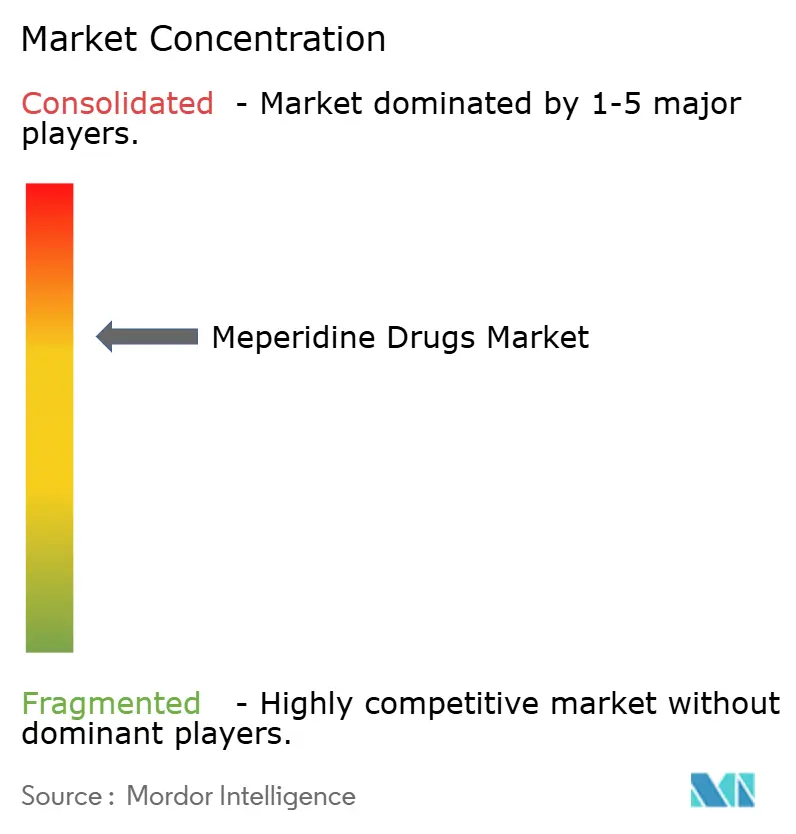

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meperidine Drugs Market Analysis by Mordor Intelligence

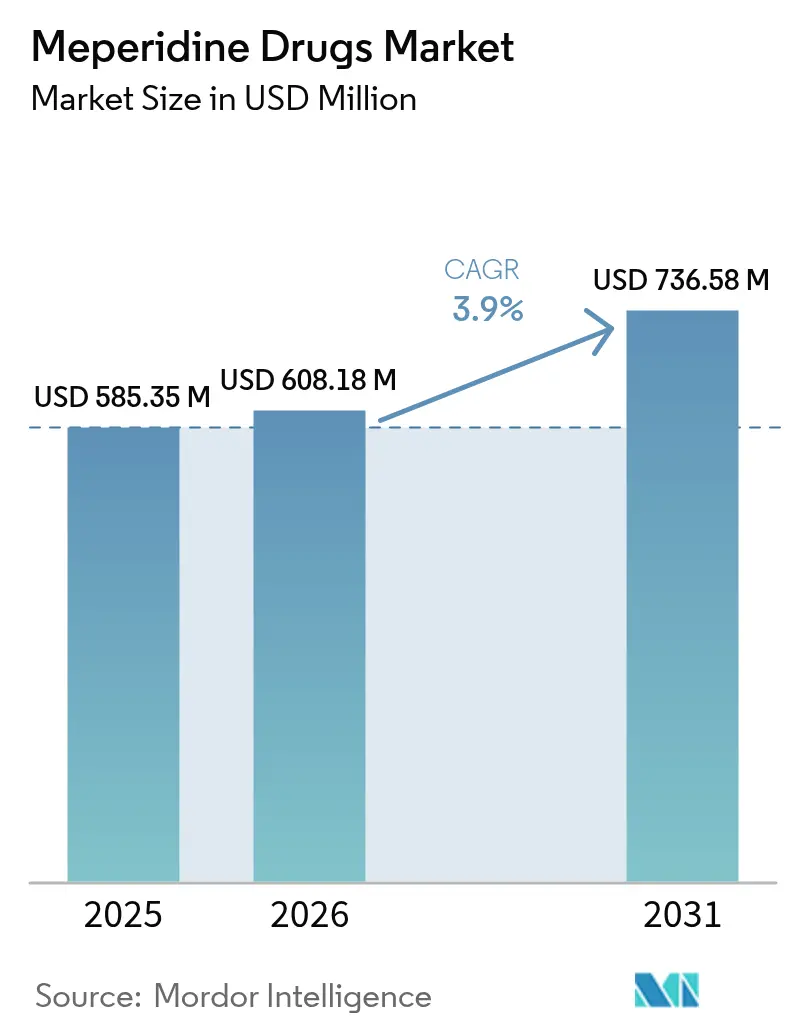

The Meperidine Drugs Market size is expected to grow from USD 585.35 million in 2025 to USD 608.18 million in 2026 and is forecast to reach USD 736.58 million by 2031 at 3.90% CAGR over 2026-2031.

Demand persists because meperidine occupies narrow but defensible hospital niches where its rapid onset, short duration, and anti-shivering effects outclass substitutes. Hospitals rely on injectable forms for peri-operative pain control and shivering prevention, ensuring steady bulk purchasing even as broader opioid use contracts. Growth momentum is further supported by palliative-care programs treating complex cancer pain and by emerging-market surgical expansion that mirrors Western peri-operative protocols. Manufacturing quotas set by the U.S. Drug Enforcement Administration, alongside comparable controls in Europe and Asia, create a tightly regulated supply channel that benefits compliant producers with proven quality systems. While safer novel analgesics and stricter formularies temper headline expansion, supply chain resilience and specialized clinical evidence keep the meperidine drugs market on a predictable upward curve.

Key Report Takeaways

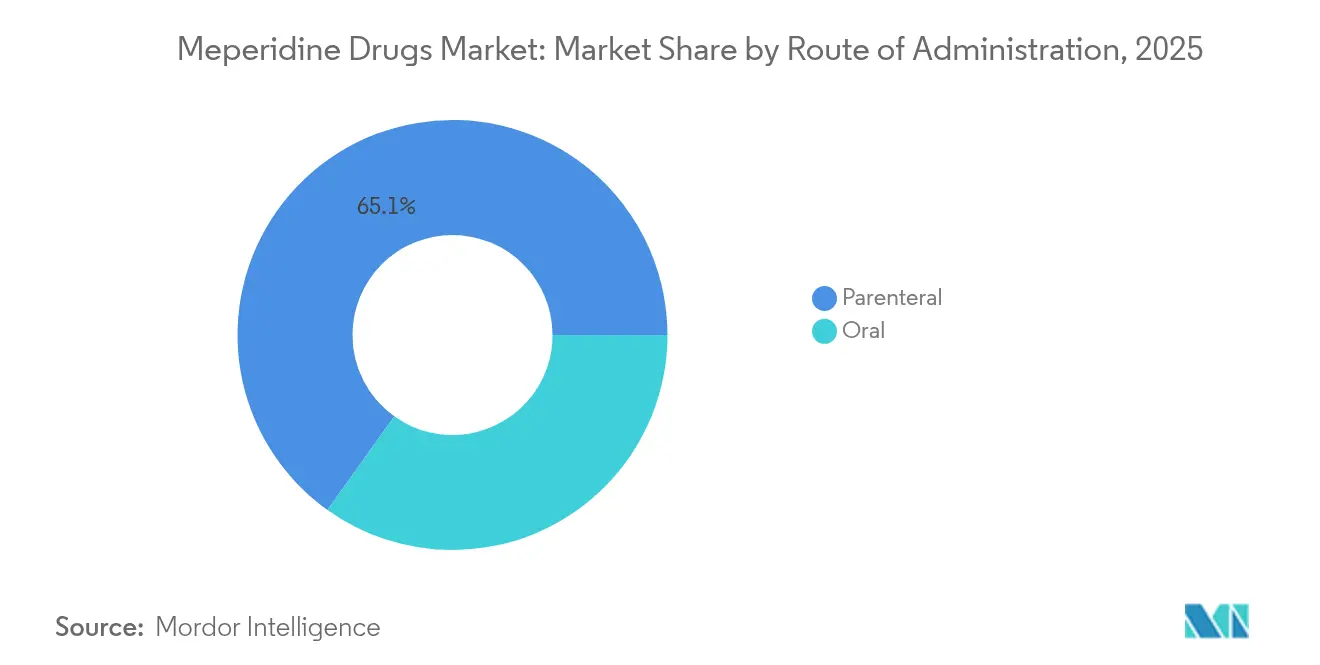

- By route of administration, parenteral formulations led with 65.12% of the meperidine drugs market share in 2025; while parenteral maintains a 6.56% CAGR.

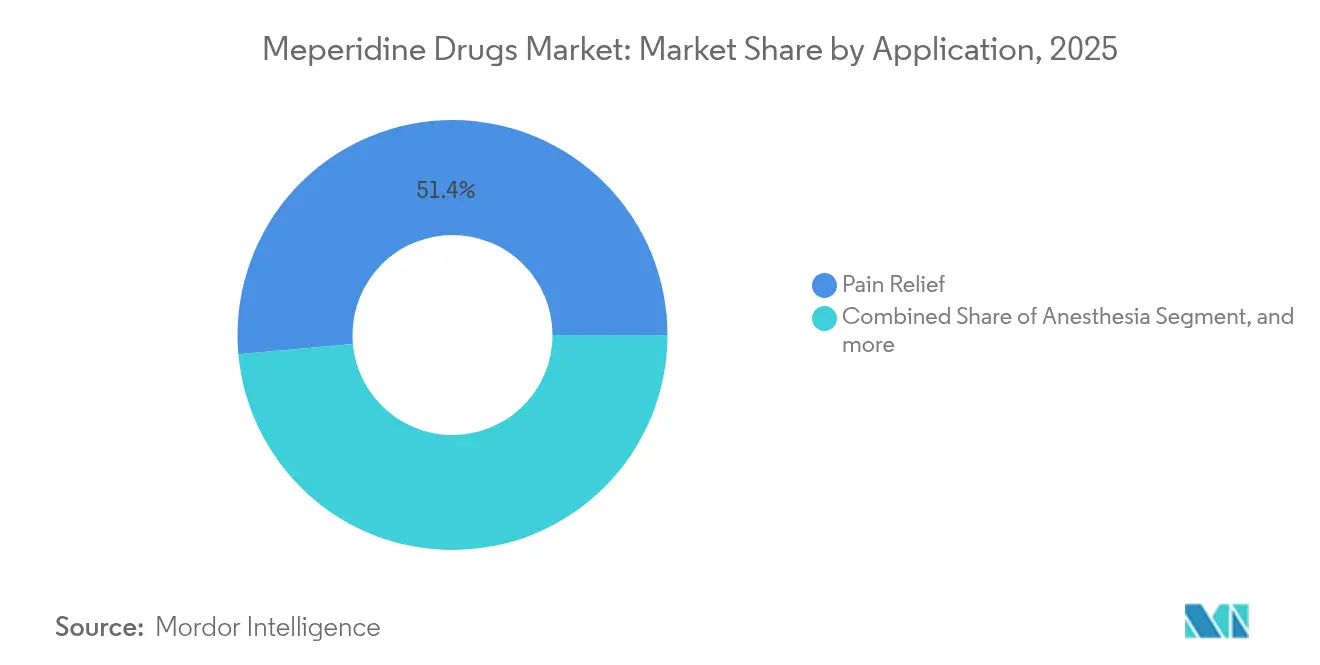

- By application, pain relief dominated with 51.42% revenue share in 2025, yet post-operative shivering is forecast to expand at 4.88% CAGR to 2031, the fastest among all indications.

- By geography, North America accounted for 43.12% of the meperidine drugs market size in 2025, while Asia-Pacific is advancing at a 6.92% CAGR through 2031 to become the principal growth arena.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meperidine Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Palliative and End-of-Life Opioid Utilization | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Surging Need for Rapid-Onset, Short-Duration Peri-Operative Analgesia | +0.8% | Global, particularly Asia-Pacific surgical centers | Medium term (2-4 years) |

| Lower Cost Profile Compared to Newer Synthetic Opioids | +0.6% | APAC core, spill-over to Latin America | Short term (≤ 2 years) |

| Niche Clinical Applications Such as Anti-Shivering Management | +0.9% | Global, with early adoption in tertiary care centers | Medium term (2-4 years) |

| Renewed Adoption as a Combined Opioid and Local Anesthetic Agent | +0.4% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Limited Global Regulatory Bans | +0.3% | Global, excluding select jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Palliative and End-of-Life Opioid Utilization

Cancer incidence continues to climb, and multidisciplinary palliative-care teams increasingly select meperidine when mixed nociceptive–neuropathic pain resists first-line morphine or fentanyl. Intrathecal regimens show meaningful reductions in breakthrough pain episodes, improving quality-of-life metrics that national oncology societies now track closely.[1]Philip Larkin, “Opioid Use in Palliative Care,” BMC Palliative Care, bmcpalliativecare.biomedcentral.com Long-term demand is therefore partly insulated from routine surgical fluctuations, reinforcing baseline purchasing volumes at large oncology centers.

Surging Need for Rapid-Onset, Short-Duration Peri-Operative Analgesia

Outpatient surgeries in Asia-Pacific and Latin America are rising briskly, and anesthesiologists prefer an agent that wears off quickly enough to permit same-day discharge without respiratory-depression risk overnight. Meperidine’s 3-5 hour activity window outperforms longer-acting opioids in enhanced-recovery protocols, helping hospitals shorten recovery-room stays and optimize operating-room throughput.[2]European Society of Anaesthesiology, “Short-Acting Opioids in Day Surgery,” journals.lww.com

Lower Cost Profile Compared with Newer Synthetic Opioids

Off-patent status allows generic suppliers across India and China to offer sterile vials at a fraction of branded novel opioids. Formularies under value-based purchasing models lean toward meperidine when clinical equivalence is documented, making cost discipline a decisive driver in public hospitals and managed-care systems.

Niche Clinical Applications Such as Anti-Shivering Management

Systematic reviews confirm a number-needed-to-treat of 2.7 for shivering prevention, a metric unmatched by tramadol or dexmedetomidine in randomized studies. Because patient-comfort scores influence hospital quality ratings, anesthesiology departments keep meperidine protocols despite restrictive opioid stewardship programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing formulary exclusions and prescribing restrictions | -0.7% | North America & Europe, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Rising clinical substitution by safer opioids | -0.5% | Global, led by developed markets | Medium term (2-4 years) |

| Persistent global shortages of active pharmaceutical ingredient | -0.4% | Global, concentrated in regulated markets | Short term (≤ 2 years) |

| Toxicity concerns with repeated dosing | -0.3% | Global, particularly geriatric populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Formulary Exclusions and Prescribing Restrictions

The American Geriatrics Society Beers Criteria highlights neurotoxicity risks tied to normeperidine metabolites. Electronic medical-record alerts now flag meperidine orders, triggering peer review or prior authorization that slows dispensing workflows.[3]Pennsylvania Patient Safety Authority, “High-Risk Medication Alerts,” patientsafety.pa.gov These administrative hurdles compress daily volumes even in hospitals that otherwise value the drug.

Rising Clinical Substitution by Safer Opioids

FDA clearance of suzetrigine in January 2025 created a non-opioid alternative for moderate to severe acute pain. Early adopters report similar analgesia without respiratory-depression monitoring, prompting guideline committees to downgrade meperidine except for anti-shivering use. As younger clinicians are trained on suzetrigine, substitution pressure is expected to intensify through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Parenteral Dominance Reflects Hospital-Centric Usage

Parenteral formulations captured 65.12% of the meperidine drugs market in 2025 and are projected to advance at 6.56% through 2031, a pace that outstrips overall industry growth. This sustained edge stems from meperidine’s first-line role in operating theaters, emergency departments, and critical-care units where rapid onset is non-negotiable. Sterile-injectable production remains technically demanding, providing incumbents with regulatory and capital barriers that discourage new entrants and support stable price realization. The meperidine drugs market size for parenteral products is therefore expected to widen its revenue gap over oral presentations as day-surgery volumes and ER admissions continue rising.

Hospital formularies persistently favor parenteral meperidine for shivering control, and recent supply disruptions have underscored the formulation’s indispensability. Pfizer’s 2024–2025 manufacturing delays tightened availability, but they also validated procurement strategies that diversify sources among Mallinckrodt, Hikma, and regional sterile-injectable specialists. Because injectable products must comply with Schedule II controlled-substance logistics, wholesalers and group-purchasing organizations give preferential contracts to partners with proven cold-chain integrity and real-time serialization, reinforcing the competitive moat around parenteral offerings.

By Application: Pain Relief Leadership Challenged by Specialized Indications

Pain-relief accounts for 51.42% of 2025 revenue, yet its incremental growth lags at 2.03% as post-operative shivering surges ahead. Hospitals increasingly codify shivering-prevention bundles in enhanced-recovery pathways, lifting demand for meperidine despite broad opioid de-emphasis. The meperidine drugs market size associated with shivering prevention is forecast to grow 4.88% annually, quickly converting a formerly small indication into a material revenue stream within peri-operative budgets.

Oncology-based palliative care also supports the pain-relief line item by supplying a steady flow of complex cases that benefit from meperidine’s receptor binding profile. However, cough and diarrhea suppression applications are plateauing, and detox programs prefer buprenorphine, limiting upside. Clinical guideline updates through 2031 will likely ratify meperidine’s niche roles while directing routine analgesia toward competing molecules, keeping market segmentation fluid but predictable.

Geography Analysis

North America led the meperidine drugs market with 43.12% revenue in 2025. Hospital stewardship dashboards now track meperidine days-of-therapy separately from other opioids, preserving access for anti-shivering and select palliative applications yet constraining routine post-surgical use. Because national distributors allocate inventory against strict Schedule II ledger controls, any manufacturer outage can ripple quickly, and provider contracts increasingly hinge on supply-assurance clauses.

Asia-Pacific stands out with a 6.92% CAGR driven by elective-surgery expansion, medical tourism, and domestic pharmaceutical capacity growth. Regulatory harmonization initiatives in China and India streamline dossier reviews and encourage local API production, strengthening the regional supply chain. Indian firms earning USFDA and EU-GMP approvals are exporting finished doses to Southeast Asia, shortening lead times and compressing landed costs. Rising adoption of U.S.-style enhanced-recovery protocols pushes tertiary hospitals in Thailand, Malaysia, and Vietnam to stock meperidine for shivering control, accelerating market penetration.

Europe presents mid-single-digit growth as guidelines tilt toward newer agents. EMA centralization expedites assessment, but member-state formularies often restrict meperidine to anesthesia departments with clear written protocols. Middle East and Africa show latent demand tied to the gradual roll-out of cancer centers and trauma units. South American uptake is episodic; Brazil and Chile demonstrate steady volumes while Argentina and Venezuela struggle with economic headwinds. Collectively, emerging geographies provide volume growth that counterbalances plateauing demand in mature Western markets, cementing a stable global outlook for the meperidine drugs market.

Regulatory Landscape

Meperidine is regulated as a Schedule II controlled substance in the United States under the Controlled Substances Act. This places manufacturing, distribution, prescribing, and recordkeeping under DEA diversion-control requirements, in addition to FDA drug quality oversight. The DEA sets annual Aggregate Production Quotas (APQ) that cap supply, and for 2026 the established APQ for meperidine is 681,184 grams. This quota serves as a concrete constraint that affects both finished-dose output and upstream API planning.

U.S. market participation also depends on dual-track compliance for importation and manufacturing, including FDA establishment registration (21 CFR Part 207) plus DEA registration for controlled-substance importing and shipment-by-shipment import declarations. In December 2025, the FDA issued a formal determination that certain Demerol (meperidine hydrochloride) products were not withdrawn from sale for safety or effectiveness reasons, supporting continued ANDA activity for compliant generics. In May 2026, the DEA published a proposed rule (Docket No. DEA-1278) to revise how manufacturing and procurement quotas are managed for Schedule I and II substances. The proposal signals tighter supply-chain visibility and reporting expectations for quota holders.

Competitive Landscape

The competitive field shows moderate concentration. Pfizer, Teva, and Mallinckrodt historically command a higher share of global finished-dose sales, placing the market in an oligopolistic middle ground. Sterile-injectable expertise remains the principal differentiator because regulatory complexity around Schedule II manufacturing screens out many generic firms. The March 2025 merger between Mallinckrodt and Endo joins complementary production plants and controlled-substance licenses, creating a more formidable rival to Pfizer’s Demerol franchise.

Supply reliability is turning into the critical purchasing criterion. Pfizer’s 2024–2025 line shutdowns forced hospital buyers to diversify suppliers, allowing Hikma to raise U.S. institutional share with contingency allocations. In parallel, API producers in India such as Rusan Pharma gained visibility by meeting stringent U.S. DEA site inspections, giving downstream partners an alternative to traditional European synthesis routes. Qualified contract manufacturing organizations are investing in isolator-based filling lines that meet Annex 1 revisions, promising both volume flexibility and compliance headroom.

Pricing remains rational because the pool of DEA-registered importers is limited and production slots for controlled substances often compete with higher-margin injectables. Manufacturers therefore focus on cost containment through continuous-manufacturing upgrades and digital batch-record systems rather than price wars. Pipeline activity is light; most innovation effort surrounds tamper-resistant ampoule caps and barcode serialization rather than new formulations, reflecting the generic status of meperidine. Strategic alliances center on supply continuity rather than novel therapeutics, reinforcing the importance of operational excellence in sustaining or enlarging positions within the meperidine drugs market.

Meperidine Drugs Industry Leaders

Mallinckrodt Pharmaceuticals

Pfizer Inc.

Sandoz (Novartis AG)

Epic Pharma LLC

Sanofi S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most actionable opportunities sit in hospital-controlled niches where meperidine use remains protocol-driven, especially sterile injectable use for peri-operative care and post-operative shivering management. Parenteral formulations already account for the majority of demand (65.12% share in 2025 per the report context), and procurement behavior increasingly rewards suppliers that can keep Schedule II-compliant inventory moving without interruptions. The DEA-established 2026 APQ for meperidine at 681,184 grams also anchors near-term supply planning. Its May 2026 proposed quota-management updates add additional pressure for more transparent, auditable quota and inventory controls, which favors manufacturers and CMOs that invest in controlled-substance compliant serialization, batch records, and resilient sourcing.

Opportunity also comes from regulatory clarity and shortage-management mechanisms that help keep the generic pathway open even as clinical guidelines restrict routine use. The FDA determination dated December 12, 2025 that certain Demerol products were not withdrawn for safety or effectiveness reasons removes a regulatory barrier for ANDA approvals and maintenance, supporting additional qualified sources where supply risk persists. At the same time, stewardship tools, including geriatric-risk cautions tied to normeperidine and formulary restrictions, narrow use into defined indications. That focus increases the value of targeted medical education, hospital-protocol alignment, and dependable unit-dose and Carpuject-style institutional presentations, rather than broad outpatient expansion.

Recent Industry Developments

- August 2026: Pfizer updated institutional customers with an estimated 3Q 2026 recovery timing for Demerol 50 mg/mL Carpuject availability in its hospital channel. The communication shows how supply restoration milestones at a major branded supplier can shape hospital allocation strategies and accelerate secondary sourcing shifts among DEA-compliant alternatives during constrained periods.

- December 2025: The US FDA published a formal determination that certain Demerol (meperidine hydrochloride) products were not withdrawn from sale for reasons of safety or effectiveness. This action preserves a pathway for ANDA submissions and approvals for meperidine generics that meet current quality standards, helping diversify supply in a quota-controlled category.

- August 2024: Pfizer received FDA approval for an emergency extension of use dates for Demerol (meperidine hydrochloride injection, USP C-II) 50 mg/mL and 75 mg/mL presentations to mitigate shortage conditions. Extending use dating can improve effective on-hand inventory for hospitals and distributors, reducing near-term disruption in peri-operative and anti-shivering protocols that depend on injectable availability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the annual value of meperidine based medicines sold for clinical use in managing moderate to severe pain, where the drug is dispensed through healthcare settings and pharmacies and used as per approved medical practice.

Scope exclusions: It excludes illicit opioids, non-meperidine pain medicines, and non-drug pain management devices or procedures.

Segmentation Overview

- By Route of Administration

- Oral

- Parenteral

- Intravenous

- Intramuscular

- By Application

- Pain Relief

- Anesthesia

- Cough Suppression

- Diarrhea Suppression

- De-addiction / Detox Support

- Post-operative Shivering

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the guardrails that shape prescribing for this opioid, so the model reflects real world use rather than broad pain prevalence. We refer to public health statistics and surveillance resources such as CDC opioid guidance and safety communications, NIH and NLM literature, and peer reviewed clinical journals that discuss meperidine use patterns and risks.

To ground geography and access side assumptions, we also use sources such as FDA drug labeling and safety notices, WHO and OECD health indicators, and government procurement and reimbursement notes where available. Company filings, investor presentations, and reputable press are reviewed to understand portfolio changes, manufacturing updates, and supply constraints. In parallel, we use paid subscriptions for company financials and intelligence, and for patent databases, to cross check product activity and lifecycle signals. These desk sources are illustrative only, and many other references were used for data collection, cross checks, and clarification during the work.

Primary Interviews and Surveys

Primary work is used to pressure test the demand indicators and pricing logic, especially where published prescribing narratives are not directly convertible into revenue. We speak with a mix of manufacturers, distributors, hospital pharmacy stakeholders, pain management and anesthesiology facing clinicians, and procurement or formulary aligned roles across APAC, EMEA, and the Americas, then refine assumptions where responses converge.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 42% |

| Mid tier: 41% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 21% | Managers: 50% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool assessment where treatment settings and route of administration are used to reconstruct the likely annual consumption and value, then validated with selective bottom-up approximations. On the demand side, we rely on inputs such as procedure volumes that typically require acute analgesia (including post operative and labor settings), hospital admission and surgery trends, opioid prescribing and stewardship signals, route mix between oral and parenteral use, and observed price bands by dosage strength and pack presentation.

Once the base year is set, revenue is modeled as volume proxies multiplied by an adjusted average selling price, and gaps are handled by conservative proxy ratios agreed in interviews, especially where channel split data is not consistently visible. For forecasting, we use scenario analysis supported by a light multivariate regression check, where the forward path is tied to changes in acute care activity, opioid safety policies, substitution toward alternative analgesics, and expected pricing behavior in regulated markets. The result is then compared back to supplier and channel checks, so any over or under statement can be corrected before finalizing.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, so the final totals do not rely on a single dataset or a single opinion. We run variance checks across regions, route mix, and implied pricing, and any outliers are reviewed and reworked until the drivers are explainable with real world logic.

Before sign off, the model and written conclusions pass through multi step analyst reviews, with targeted re contact of experts when a key assumption shifts, or when new safety or supply news changes the short term view. Reports are refreshed annually, and interim updates are made when material events occur. Immediately before delivery, a fresh review pass is done so the updated numbers and narrative reflect the latest inputs.

Mordor Intelligence's Meperidine Drugs Market Size Measured Against Other Published Estimates

Published market values for meperidine based drugs can look far apart even when they appear to cover the same category, because the underlying scope and year anchors are not always aligned. Differences also come from how analysts treat route mix, the use of older base years, and whether values reflect strict prescription use or broader opioid spending.

In practice, the largest gaps usually come from what gets counted as meperidine revenue, how average price is trended over time, and how quickly assumptions are refreshed after policy and safety shifts. Some estimates fold in a wider set of branded references or adjacent opioid analgesics, or they apply a single global price progression without checking hospital versus retail dynamics, which can push totals up or down.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 608.18 M (2026) | |

| Global Research Publisher A | USD 970.00 M (2024) | Uses an earlier base year and a broader segmentation set that can capture wider opioid pain revenue, and the conversion to value is less transparent on route level pricing and channel mix. |

| Industry Analyst Group B | USD 993.87 M (2025) | Reported as a 2025 base with a wider formulation framing and fewer visible checks on acute care demand proxies, which can lead to higher implied volumes when hospital use is generalized. |

The table shows that year choice and what gets included around route, channel, and adjacent products can move the total meaningfully. By tying value to route specific usage and acute care demand signals and then rechecking price and volume assumptions with interviews, the estimate stays closer to the definable meperidine demand pool, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current Meperidine Drugs Market size?

The Meperidine Drugs Market is projected to register a CAGR of 3.90% during the forecast period (2026-2031)

Who are the key players in Meperidine Drugs Market?

Sanofi Aventis, Mallinckrodt Pharmaceuticals, Pfizer Inc, Novartis (Sandoz Canada Inc.) and Epic Pharma are the major companies operating in the Meperidine Drugs Market.

Which is the fastest growing region in Meperidine Drugs Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Meperidine Drugs Market?

In 2025, the North America accounts for the largest market share in Meperidine Drugs Market.

What years does this Meperidine Drugs Market cover?

The report covers the Meperidine Drugs Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Meperidine Drugs Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: