Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.5 Billion |

| Market Size (2031) | USD 24.98 Billion |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outdoor Furniture Market Analysis by Mordor Intelligence

The outdoor furniture market size was valued at USD 19.70 billion in 2025 and estimated to grow from USD 20.5 billion in 2026 to reach USD 24.98 billion by 2031, at a CAGR of 4.04% during the forecast period (2026-2031). Despite volatile raw-material costs and seasonal demand swings, the sector is set to maintain steady growth as manufacturers pivot to eco-friendly materials, modular designs, and omnichannel distribution. Strong investment in resort construction, rooftop amenities, and outdoor-living renovations keeps commercial demand high while the residential segment accelerates on the back of work-from-home lifestyle shifts. Premium collections outpace the overall market as buyers weigh total cost of ownership and curb-appeal value more heavily than the upfront price. Material innovation, especially recycled composites and hybrid designs, remains a crucial differentiator, while smart features such as built-in charging ports help brands stand out in a crowded field.

Key Report Takeaways

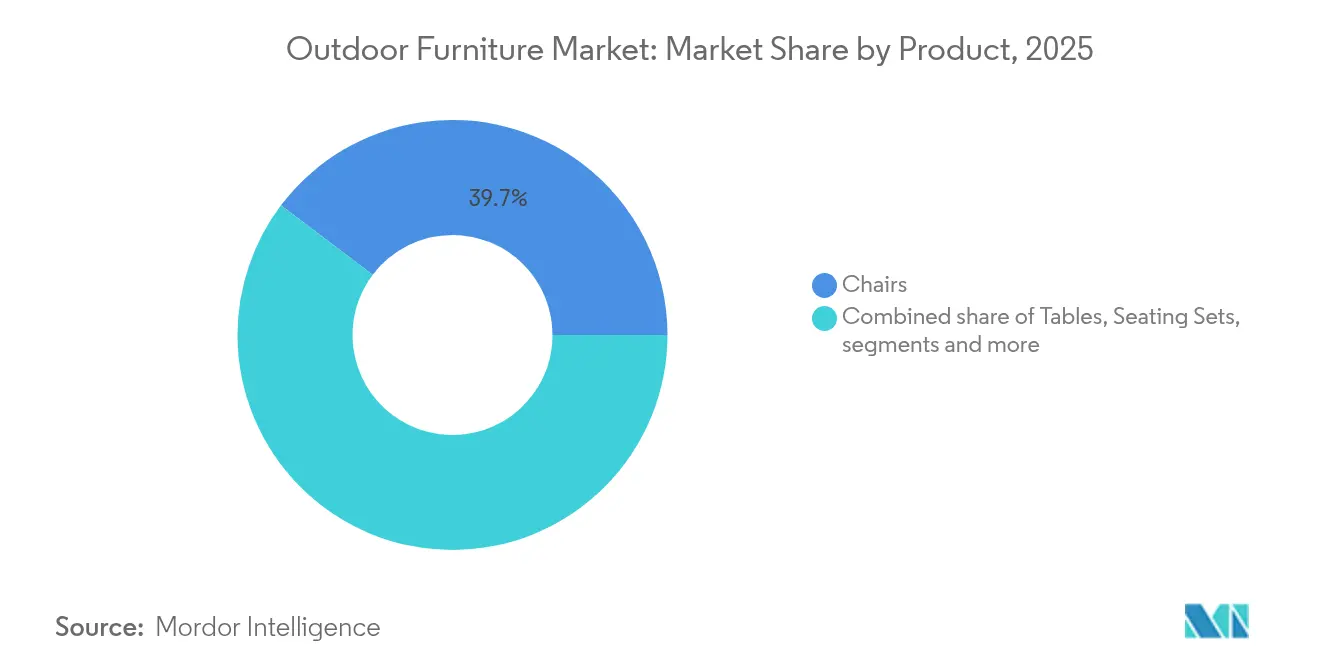

- By product, chairs led with 39.70% outdoor furniture market share in 2025, while loungers and daybeds are projected to grow at a 5.68% CAGR through 2031.

- By end user, the commercial segment captured 59.20% of the outdoor furniture market in 2025; the residential segment is forecast to expand at a 5.19% CAGR to 2031.

- By material, wood held 39.60% outdoor furniture market share in 2025; plastics and polymers are advancing at a 5.0% CAGR.

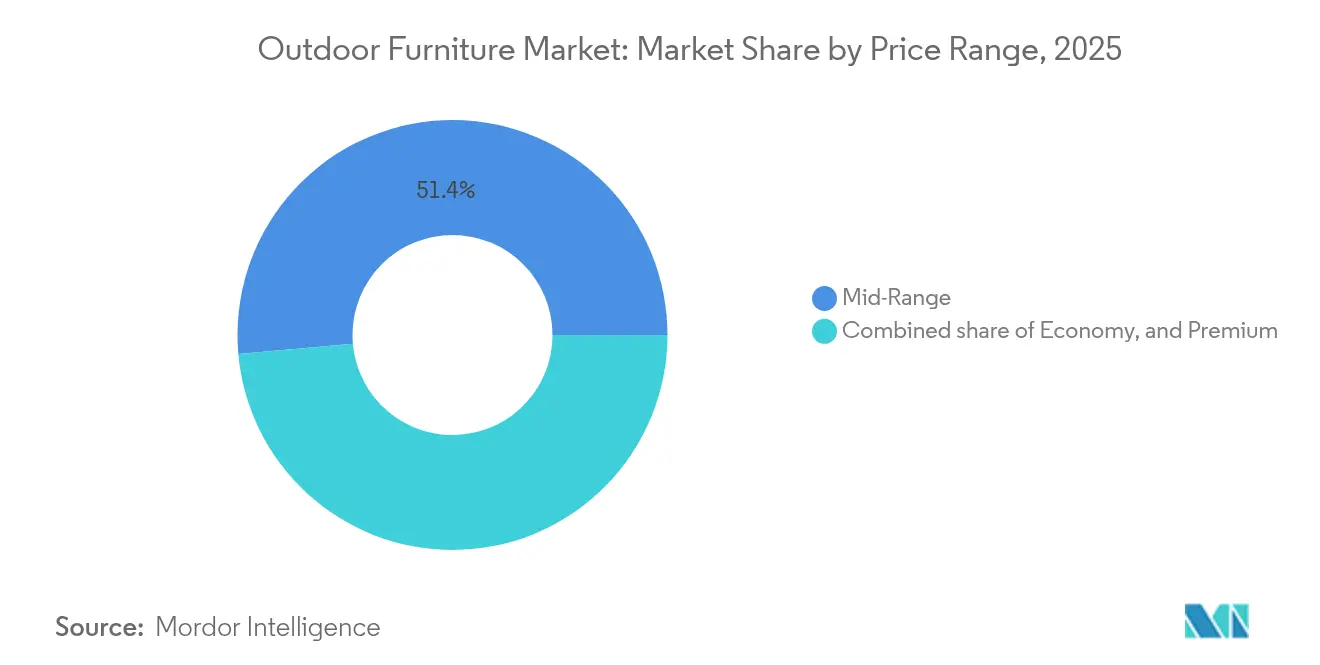

- By price range, the mid-range tier accounted for 51.40% of the outdoor furniture market in 2025; the premium tier is set to rise at a 5.88% CAGR.

- By distribution channel, the B2B/contractor route represented 58.60% of the outdoor furniture market in 2025; the online channel within B2C/retail is advancing at a 6.86% CAGR.

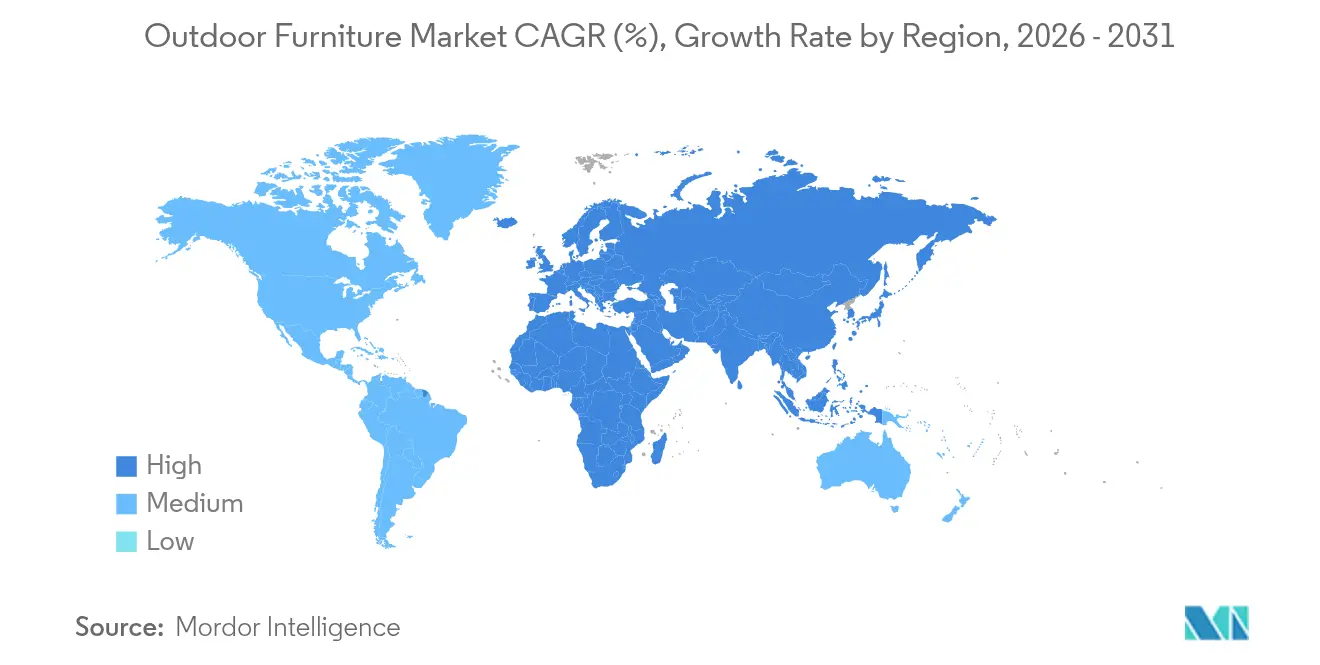

- By geography, Asia-Pacific commanded 45.70% outdoor furniture market share in 2025 and is pacing a 6.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outdoor Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resort and boutique-hotel construction raising demand for premium poolside sets | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Outdoor-living room renovation trend among millennials and Gen-X homeowners | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Direct-to-consumer e-commerce platforms are easing bulk purchases | +0.7% | Global | Short term (≤ 2 years) |

| Urban rooftop and co-working terrace projects adopting modular sets | +0.5% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Environmental regulations and green procurement | +0.3% | Europe, North America, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Resort and Boutique-Hotel Construction Boosting Premium Poolside Furniture Demand

Developers in 2025 allocated Furniture, Fixtures, and Equipment (FF&E) budgets to outdoor zones, turning pool decks and beach clubs into headline amenities that drive guest bookings and social-media exposure. Marriott’s network expansion to 8,800 properties across 139 countries and its 2025 leisure-travel revenue surge testify to the scale of future demand.[1]Marriott Investor Relations, “Annual Report 2024,” Marriott International, marriott.gcs-web.com Properties increasingly specify modular seating that can be reconfigured for events, pushing suppliers to design re-stackable frames and quick-swap cushions. Contract buyers also demand performance fabrics that resist sunscreen stains, salt spray, and UV fading across multiyear duty cycles. As hospitality pipelines diversify into glamping, bungalow, and wellness-retreat formats, product lines that blend resort durability with boutique aesthetics enjoy an enlarged addressable market.

Outdoor-Living Room Renovation Trend among Millennials and Gen-X Homeowners

Homeowners now treat patios, balconies, and yards as true extensions of the floor plan, with deep-seating sectionals, plush daybeds, and coordinated décor mirroring indoor comfort. Millennials already account for a rising share of category spending and frequently dedicate up to one-quarter of home-improvement budgets to open-air spaces. Manufacturers respond with mix-and-match modules that let buyers add pieces over successive seasons, mitigating budget constraints while driving brand loyalty. Built-in USB ports, solar-powered lighting, and weather-responsive textiles boost functional value and create cross-sell opportunities for smart-home suppliers. Architectural Digest reports that 82% of U.S. homeowners became more inclined to upgrade outdoor areas post-pandemic, a signal that the behavior has structural rather than temporary roots.

Direct-to-Consumer E-commerce Platforms Lowering Barriers for Bulk Outdoor Furniture Purchases Globally

Specialized DTC platforms give retailers, developers, and residential buyers instant visibility into pricing tiers and lead times once available only through offline dealer networks. Augmented-reality tools improve conversion by letting users visualize true-to-scale items in situ, while back-end integrations provide real-time inventory updates. Fermob’s B2B portal, which now contributes one-quarter of turnover, illustrates the efficiency benefits of a digital-first model. Manufacturers are leveraging these channels to trial limited-edition collections, gather usage analytics, and run just-in-time production cycles that cut stock obsolescence.

Environmental Regulations and Green Procurement

Europe leads with strict limits on chemical preservatives and deforestation, forcing global suppliers to verify the chain of custody and adopt water-based finishes. Public-sector tenders and corporate sustainability pledges now require environmental product declarations or comparable proofs of recycled content. Companies such as Kedel have commercialized 100% recycled plastic benches that outperform timber in marine and park settings while ticking ESG boxes for institutional buyers. As compliance costs rise, vertically integrated firms with traceable material flows gain margin resilience and regulatory headroom.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices are squeezing manufacturer margins | -0.8% | Global, high in Asia-Pacific | Medium term (2-4 years) |

| Seasonality and weather variability raise inventory risk | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Stringent anti-deforestation and chemical-preservative rules limiting wood supply | -0.4% | Europe, North America, and the Global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices Pressuring Manufacturer Margins

Aluminum, teak, and petroleum-based inputs have swung sharply since 2024, leaving mid-market producers vulnerable. Material efficiency in wood processing can range from 70–85%; any spike in timber prices flows straight to cost of goods sold and erodes profitability. Larger groups combat volatility through multi-source contracts and scrap-recycling programs, yet smaller firms must either hedge, absorb the hit, or pass costs to distributors. Capital-intensive vertical-integration moves promise future savings but worsen near-term cash-flow strain.

Seasonality and Weather Variability Increasing Inventory Risk for Retailers

Erratic spring or autumn onset distorts sell-through timelines, resulting in premature markdowns and costly overstocks. Because outdoor sets occupy significant floor and warehouse space, missed sales windows can impair a retailer’s entire year. Merchants now experiment with seasonless assortments and drop-ship partnerships that shift stock risk back onto factories equipped for flexible manufacturing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Loungers Lead Relaxation Revolution

Loungers and daybeds are the fastest-growing category, advancing at a 5.68% CAGR as buyers invest in premium relaxation pieces suitable for pool decks and shaded reading nooks. The chairs segment, while mature, retained 39.70% of 2025 revenue and continues to anchor bundled patio sets in both hospitality and residential channels. Advancements in quick-dry foams, UV-stable dyes, and ergonomic forms elevate perceived value and extend upgrade cycles. Integrated side tables, shade articulations, and electronic charging modules further differentiate high-end loungers amid rising competition.

Manufacturers target multifunctional formats that adapt from sun-bathing to social-gathering layouts, an approach favored in urban settings where balconies double as dining and lounging zones. The outdoor furniture market size for loungers is expected to outstrip overall growth as wellness-focused consumers allocate discretionary income toward yoga daybeds and zero-gravity recliners. Meanwhile, dining tables and benches gain traction in commercial patios where year-round outdoor service extends guest capacity. Designers cite texture layering—rope, woven accents, and teak inserts—as a key tactic to lift aesthetic appeal without hiking frame weight.

By Material: Sustainability Drives Innovation

Wood preserved its 39.60% share in 2025 on the strength of teak’s weather resistance and warm appeal, yet supply constraints and price sensitivity push experimentation with eucalyptus, bamboo, and thermally modified pine. Plastics and polymers hold the highest growth runway at 5.0% CAGR as suppliers commercialize recycled composites such as ScanCom’s DuraPlast, which meets circular-economy goals while outperforming virgin HDPE under UV exposure. Hybrid builds combine aluminum skeletons with synthetic-rope or TechTeak slats, creating lighter yet robust profiles that speed container loading and reduce freight emissions.

Commercial buyers increasingly request environmental declarations alongside warranty documents, embedding sustainability into the procurement scorecard. The outdoor furniture market size for recycled plastic collections is set to climb steadily, supported by park agencies and hospitality chains seeking maintenance-free solutions. Metal frames remain the mainstay in high-traffic venues where resistance to impact and vandalism supersedes weight considerations. Powder-coat advancements and marine-grade stainless steel bolsters corrosion defenses in coastal installations.

By End User: Commercial Dominance Persists

Commercial projects captured 59.20% of 2025 revenue, underpinned by hotel, resort, restaurant, and corporate campus spending. Hospitality designers specify furniture that marries luxury aesthetics with contract durability, including concealed fasteners and replaceable upholstery panels for cost-efficient refurbishment. Restaurants have converted sidewalks, rooftops, and car parks into semi-permanent al-fresco zones, keeping demand elevated even in cooler climates through the addition of heaters and windbreaks.

The residential segment is posting a 5.19% CAGR as homeowners continue pandemic-era investments in outdoor sanctuaries configured for remote work, family gatherings, and wellness activities. The outdoor furniture market size for premium residential sets is forecast to rise faster than mid-market offers, reflecting homeowners’ willingness to pay more for weather-proof fabrics and extended warranties. Commercial aesthetics increasingly influence residential tastes, while homeowners’ desire for commercial-grade robustness encourages crossover designs with thicker wall sections and contract-grade fabrics.

By Price Range: Premium Segment Accelerates

Mid-range collections held 51.40% of revenue in 2025, but premium lines are tracking a 5.88% CAGR on the back of affluent consumer demand for bespoke finishes, muted jewel tones, and artisan craftsmanship. Buyers justify the uplift through lower lifetime maintenance and stronger resale value if properties change hands. Premium producers now offer bundle design consultation, 3D space planning, and white-glove delivery, making service a key value driver alongside product.

Economy tiers still serve first-time buyers and price-sensitive rental markets, yet rising awareness of durability gaps constrains their share gains. Manufacturers leverage feature migration, such as quick-dry foam and Sunbrella-level fabrics, to refresh mid-range lines and defend volume. The outdoor furniture industry uses premium innovation as a halo effect that elevates perceived quality across an entire brand portfolio in both residential and commercial eyes.

By Distribution Channel: B2B Efficiency Drives Growth

The B2B pathway concentrates 58.60% of sales due to developers and hospitality groups sourcing in bulk to lock consistent aesthetics across multi-site portfolios. Dedicated sales teams, project-management software, and just-in-sequence shipping schedules create stickiness with these clients. Contract furniture makers integrate BIM libraries and configurable SKUs to streamline specifications with architects and procurement teams.

Within the retail/B2C segment, which represents 41% of global revenue, online channels show the fastest expansion, registering a 6.86% CAGR forecast for 2026-2031. Growth is propelled by sharper 3-D visualization tools, broader SKU depth, and frictionless checkout options that make high-ticket outdoor items easier to buy sight-unseen. Retailers and home centers retain relevance in residential starter sets by offering immediate pickup and adjacent categories such as grills and décor. However, DTC platforms now bridge showroom inspiration and online convenience, providing AR visualization, chat-based design advice, and no-interest financing. The outdoor furniture market sees rising hybrid models: brands operate flagship experiences for tactile engagement, then route transactions to web portals that carry the full catalog, reducing inventory overhead.

Geography Analysis

Asia-Pacific leads with a 45.70% share and should maintain a 6.27% CAGR to 2031 as rising urban middle-class households adopt Western-style outdoor-living concepts. China dominates production and internal demand, while India’s fast-growing residential construction and hotel pipelines underpin long-run volume gains. Japan and South Korea focus on compact, modular lines that suit high-density living, whereas Australia spends heavily on all-season alfresco culture. Singapore and Malaysia benefit from tourism and luxury condos that demand high-end communal decks furnished with contract-grade sets.

North America ranks second in revenue. The United States remains the bellwether; its deep-seated patio culture drives replacement cycles every four to six years. Covered porches and three-season rooms mitigate strict winter off-season periods, smoothing sales curves. Canada mirrors the U.S. in design tastes but emphasizes harsher climate resistance. Mexican demand rises as resort development and a growing middle class converge. Reshoring is also gaining traction as U.S. case-goods manufacturers convert tariff headwinds into competitive advantage by relocating portions of production to domestic facilities. These moves shorten lead times, buffer supply-chain shocks, and let brands highlight “Made in USA” provenance in premium positioning. This intensifies competition for skilled labor and raises interest in automation technologies to offset higher labor cost.

Europe exhibits sophisticated taste and strict sustainability. Germany spearheads eco-compliance, forcing suppliers to refine coatings and secure FSC timber certificates. France and Italy leverage heritage manufacturing and design cachet in the premium tier, while the Nordics favor weather-adaptive textiles that cope with short summers and long winters. Mediterranean nations sustain a robust café culture that privileges dining sets, umbrellas, and stackable seating. Eastern Europe expands its manufacturing footprint, luring OEM contracts and accelerating domestic availability of mid-range collections.

Competitive Landscape

The outdoor furniture market hosts global manufacturers, regional specialists, and agile DTC entrants, creating a moderately concentrated competitive landscape. Leading groups leverage vertical integration—from sawmill to upholstery—and multi-brand portfolios that cover economy through luxury. Mid-tier brands often pursue niche differentiation in materials, such as HDPE lumber or artisan wicker, to avoid direct price wars.

Lean manufacturing fused with sustainability yields measurable performance gains.[3]Marek Wieruszewski et al., “Economic Efficiency of Pine Wood Processing in Furniture Production,” Forests Journal, doi.org Leaders also deploy digital twins to simulate weather exposure and structural loads, shortening design-to-launch cycles. Polywood remains a benchmark for recycled-plastic lumber adoption, locking in hospitality contracts where maintenance-free durability offsets higher acquisition costs.

Strategic moves center on capacity expansion, material innovation, and omnichannel integration. Marriott-aligned suppliers invest in regional warehouses to fulfill rollouts across multiple hotel flags. Competitive tension is elevated by lifestyle retailers and grill makers broadening into furniture bundles, diluting traditional segmentation lines, and intensifying the race for consumer attention.

Outdoor Furniture Industry Leaders

IKEA

Ashley Furniture Industries Inc.

Brown Jordan Inc.

Agio International Company Ltd.

Keter Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Berlin Gardens unveiled the recycled-material Murphy Collection and minimalist Vida line, strengthening its sustainability play.

- March 2025: DecoScape, a new luxury outdoor-furniture manufacturer, launched its Bosca collection featuring Mid-Century Modern styling and GreenCircle Certified sustainability credentials; the molded-lumber line uses 93% recycled content.

- February 2024: Crate & Barrel announced plans to open three additional U.S. stores to showcase full-home solutions that now feature extended outdoor vignettes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the outdoor furniture market as the annual value of movable seating, dining, lounging, and accessory pieces purpose-built for exterior use in residential yards, balconies, gardens, public parks, hospitality terraces, and similar spaces, regardless of sales channel. Products are counted at the manufacturer-level invoice price and must be manufactured from weather-resistant wood, metal, plastics, or mixed composites. According to Mordor Intelligence, built-in fixtures, grills, patio heaters, and site-built structures such as pergolas fall outside this scope.

Scope exclusion: grills, patio heaters, and fixed architectural elements are not included.

Segmentation Overview

- By Product

- Chairs

- Tables

- Seating Sets

- Loungers and Daybeds

- Dining Sets

- Other Products

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By End User

- Residential

- Commercial

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Retail/B2C Channels

- Home Centers

- Specialty Stores

- Online

- Other Distribution Channels

- B2B Channel/Contractors

- Retail/B2C Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed purchasing managers at hotel chains, category buyers at big-box retailers, contract furniture distributors, and materials specialists across North America, Europe, and Asia-Pacific. These conversations validated demand drivers such as hospitality refurbishment cycles, clarified average replacement intervals for timber seating, and vetted working assumptions on freight-adjusted landed costs.

Desk Research

We gathered baseline figures and trend signals from publicly available tier-one sources such as the UN Comtrade trade database, the International Casual Furnishings Association's shipment survey, the U.S. Census Bureau's Monthly Retail Trade series, Eurostat dwelling permit data, and World Bank disposable-income indicators. Company 10-Ks, investor decks, and trade-show presentations supplemented product-level average selling prices and material splits.

To enrich country splits and brand shares, our analysts tapped paid repositories, D&B Hoovers for financials, Dow Jones Factiva for news flow, and Asia Metal for teak and aluminum cost curves, linking those data points to publicly reported unit volumes. The sources named are illustrative; many additional datasets were consulted for cross-checks and context clarity.

Market-Sizing & Forecasting

A top-down model converts domestic output plus net imports into apparent consumption, with trade codes 9403.61-69 and 9403.89 reconstructed for key economies. Results are stress-tested through selective bottom-up checks, sampling leading supplier revenues and channel sell-through ratios to spot material under- or overstatement. Core inputs include new housing completions, outdoor dining seat counts, teak lumber import prices, home-improvement spending indices, patio e-commerce penetration, and average furniture life-cycle length. Multivariate regression on these variables generates the 2025-2030 trajectory, while scenario analysis captures swings in raw-material inflation or construction slowdowns. Data gaps in smaller economies are bridged by region-specific import reliance factors vetted during interviews.

Data Validation & Update Cycle

Every model run passes anomaly flags, peer review, and a supervisor sign-off before release. Reports refresh once a year; extraordinary events such as tariff shifts trigger interim updates, and we re-query experts prior to any client delivery so users receive the most current view.

Why Mordor's Outdoor Furniture Baseline Commands Reliability

Published estimates differ widely because firms mix scopes, price points, and refresh cadences. By focusing strictly on movable weather-resistant pieces and anchoring values at manufacturer price, we avoid double counting and inflated retail margins.

Key gap drivers versus other publishers include inclusion of grills and patio heaters, use of retail sell-through instead of factory shipments, and broader material pools that sweep in outdoor kitchens and modular decks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.70 B (2025) | Mordor Intelligence | - |

| USD 53.27 B (2024) | Global Consultancy A | Bundles grills, heaters, accessories; mixes factory and retail values |

| USD 50.89 B (2024) | Trade Journal B | Counts semi-fixed kitchens and deck structures; applies retail ASP uplift |

These contrasts show that Mordor's disciplined scope selection, trade-verified inputs, and annual refresh cycle give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the size of the outdoor furniture market in 2026?

The outdoor furniture market stands at USD 20.5 billion in 2026 and is projected to hit USD 24.98 billion by 2031 at a 4.04% CAGR.

Which region holds the largest share of the outdoor furniture market?

Asia-Pacific leads with 45.70% market share in 2025 and is pacing the highest regional CAGR at 6.27% through 2031.

Which outdoor furniture product category is growing fastest?

Loungers and daybeds are the quickest-expanding segments with a 5.68% CAGR forecast for 2031.

What material type is gaining momentum in the outdoor furniture market?

Plastics and polymer composites are advancing at a 5.0% CAGR as recycled and weather-resistant formulations gain favor.

Which distribution channel generates the most outdoor furniture sales?

The B2B or contractor channel accounts for 58.60% of global revenue due to bulk hospitality and real-estate orders.

Page last updated on: