Plastic Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.56 Billion |

| Market Size (2031) | USD 21.88 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

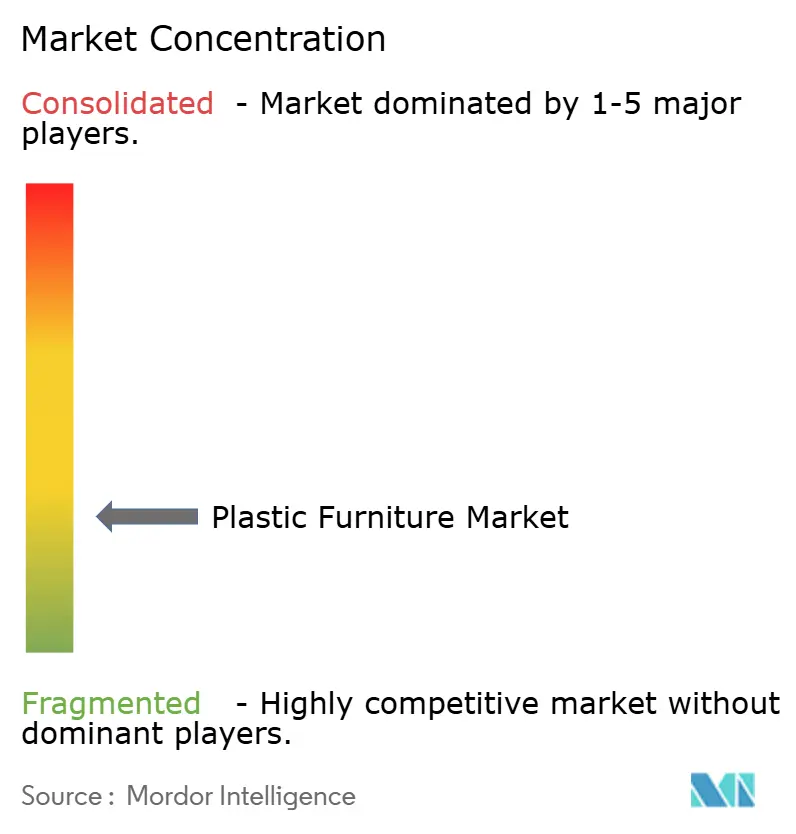

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Furniture Market Analysis by Mordor Intelligence

The Plastic Furniture market size is expected to grow from USD 16.80 billion in 2025 to USD 17.56 billion in 2026 and is forecast to reach USD 21.88 billion by 2031 at 4.5% CAGR over 2026-2031.

Solid demand stems from rapid urbanization, rising outdoor living investments, and the cost advantages of flat-pack designs that travel well through e-commerce channels. Manufacturers are widening their range with recycled and specialty polymers to stay ahead of tightening sustainability regulations. Product innovation now centers on modular, space-saving furniture that appeals to apartment dwellers, while UV-stabilized and glass-reinforced composites extend use into harsher climates and premium indoor settings. Competitive intensity is growing as direct-to-consumer (DTC) entrants absorb retail margins and incumbents fund circular-economy initiatives to secure post-consumer plastic feedstock.

Key Report Takeaways

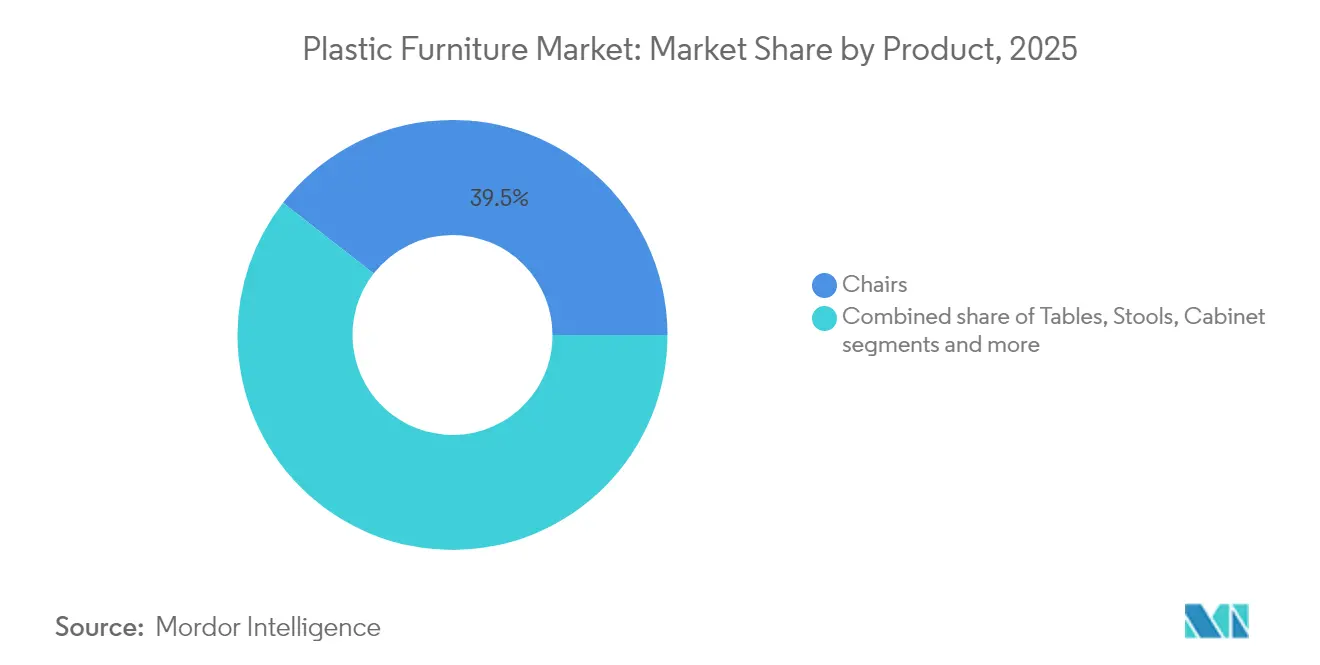

- By product, chairs led with 39.45% revenue share in 2025; cabinets are projected to expand at a 5.12% CAGR through 2031.

- By end user, the residential segment held 59.30% of the plastic furniture market share in 2025, while the commercial segment records the highest projected CAGR at 5.39% through 2031.

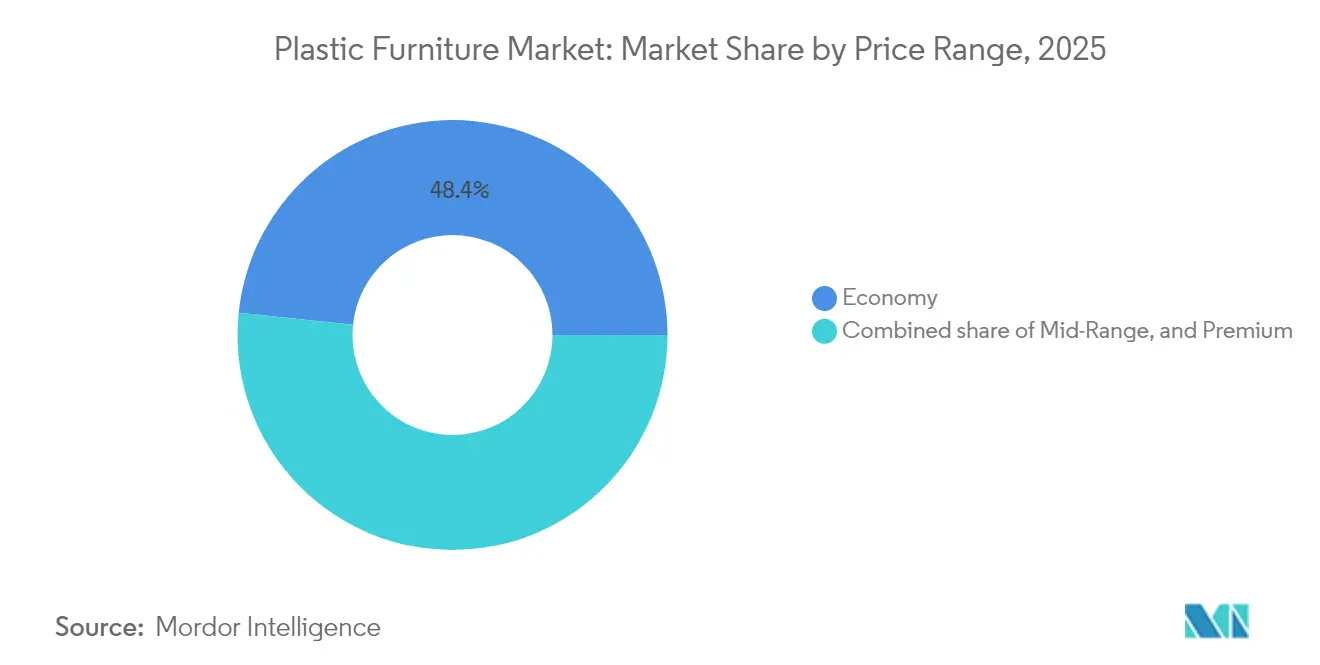

- By price range, economy products commanded 48.35% of the plastic furniture market size in 2025; the premium tier is set to grow at a 5.67% CAGR during 2026-2031.

- By distribution channel, B2C/retail dominated at 61.10% in 2025; online retail within this channel is forecast to grow at a 6.08% CAGR from 2026-2031.

- By region, North America accounted for 34.70% revenue share in 2025; Asia-Pacific is the fastest-growing geography with a 5.88% CAGR projected for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization is driving modular space-saving designs | +1.0% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2–4 years) |

| Outdoor & garden furniture demand | +0.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Eco-friendly and recycled materials | +0.6% | Global (early uptake in Europe, North America) | Long term (≥ 4 years) |

| Low manufacturing costs are widening access | +0.9% | Global (highest in emerging markets) | Medium term (2–4 years) |

| E-commerce-led DTC models | +0.7% | Global (peak in North America, Europe) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization Drives Space-Saving Solutions

Rapid urbanization is shrinking living space in many cities, especially across the Asia-Pacific region. Currently, India's urban population stands at approximately 410 million, accounting for 32% of the nation's total. Projections indicate this figure will surge to 814 million, constituting 50% of the population, by 2050 [1]World Economic Forum, “Reforms to Accelerate the Development of India’s Smart Cities,” weforum.org. As apartments become smaller, residents gravitate toward furniture that serves more than one purpose—pieces that fold, stack, or hide storage inside. Designers are responding with modular plastic units that help households reclaim every inch of floor area. By 2030, when 60% of the world’s population is expected to live in urban settings, adaptable furniture will likely be a standard feature in compact homes.

Outdoor Living Spaces Expand Applications

More households and businesses now treat patios, rooftops, and hotel decks as everyday living areas. Plastic furniture suits these settings because it shrugs off rain, sun, and salt while asking little of owners beyond an occasional wipe-down. Designers highlight recycled plastics in their 2025 collections, pairing modular layouts that can move or grow with changing needs. Many new pieces even hide smart touches such as built-in speakers or USB ports, turning an ordinary lounge chair into a mini-entertainment hub. Warm climates keep outdoor areas in use all year, so factories can plan steadier production instead of racing to meet a single summer spike.

Eco-Friendly Materials Transform Product Development

Environmental awareness is rewriting the recipe for plastic furniture. Vitra’s choice to make the Eames Plastic Chair from post-consumer polypropylene shows that style icons can cut carbon emissions in half without losing their look. Polywood goes further by grinding up roughly 400,000 used milk jugs every day and molding them into deck chairs that carry a premium price because buyers trust the closed-loop story. Brands that lock in steady streams of recycled resin shield themselves from volatile virgin-plastic costs and earn loyalty from shoppers who are happy to pay more for clear proof of responsibility.

Direct-to-Consumer Models Reshape Distribution Economics

Online stores now connect factories straight to living rooms, bypassing wholesalers and showroom rents. Plastic furniture travels well in flat-pack cartons, so shipping fees stay low and damage rates fall. Virtual showrooms let shoppers spin a sofa in 3D or drop a chair into a phone camera view of their balcony, cutting return headaches. Because every molded piece looks the same as its photo, buyers feel safer ordering sight-unseen. Direct-to-consumer sales, therefore, grow faster than any store channel and reward brands that invest in digital service rather than shelf space.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Microplastic emission regulations | -0.7% | Europe, North America, global rollout pending | Medium term (2–4 years) |

| Low heat-resistance of conventional plastics | -0.5% | Global (most acute in luxury markets) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Microplastic Regulations Create Compliance Challenges

Scientists now trace tiny plastic particles in rivers back to the slow breakdown of outdoor chairs and tables. A 2024 report from the International Joint Commission singled out furniture as an overlooked contributor International Joint Commission. Policymakers in Brussels and Washington respond with proposals that would force manufacturers to test, label, and sometimes redesign products. Meeting these rules means extra lab work and new coatings, costs that weigh heaviest on small producers [2]International Joint Commission, “Microplastic Pathways in Consumer Goods,” ijc.org.

Material Performance Limitations Constrain Expansion

Plastic still struggles where heat is part of daily use. Standard polypropylene starts to soften around 100 °C, so high-end dining tables often stay wood or metal despite higher emissions profiles. Reinforced composites raise heat tolerance but add triple-digit cost premiums that only niche buyers accept today. Until prices fall, this barrier tempers the plastic furniture market’s share gains in upscale indoor segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Chairs Lead While Cabinets Gain Momentum

Chairs retained 39.45% of the plastic furniture market share in 2025 by serving residential, hospitality, and institutional needs with ergonomic updates that satisfy office-health guidelines. The segment’s stable costs and broad style palette support steady volume growth. Meanwhile, cabinets headline the fastest expansion at a 5.12% CAGR to 2031, as city dwellers seek modular storage to counter shrinking closets.

Tables, stools, and sofas continue to round out portfolios, but momentum clearly tilts toward space-saving storage lines. Vitra’s switch to recycled polypropylene in its iconic shell chair cut product carbon intensity by more than 50%, inspiring rival brands to re-engineer legacy SKUs around reclaimed feedstock. Recent material breakthroughs help broaden product scope. Glass-fiber infusions lift load capacity, enabling three-seat plastic couches that meet residential durability norms. Gas-assisted molding yields sculptural coffee tables with seamless cores, blurring functional and aesthetic boundaries. These shifts re-position plastic from strictly utilitarian to design-forward, moving the plastic furniture market toward higher price-point opportunities.

By End User: Residential Dominance Amid Commercial Growth

Residential buyers controlled 59.30% of 2025 sales thanks to cost, color variety, and low upkeep. Outdoor decks, balconies, and small dining corners remain prime destinations for synthetic materials that shrug off rain and sun. The commercial segment is forecast to post a 5.39% CAGR through 2031, driven by hotels and quick-service restaurants that value stackability and antibacterial coatings.

Offices, hotels, and schools are rethinking how they use space, so they now want furniture that moves and adapts as quickly as their floor plans. Lightweight plastic panels and clip-together seating let a conference room flip into a training hall before lunch. Buyers also look for greener inputs, ergonomic shapes, and built-in tech such as cable ports. Hotels have turned to plastic sets for pool decks and budget guest rooms because they wash clean with a hose and resist salt or sun fade. Schools follow the same logic: stackable chairs survive daily knocks and wipe down in minutes, keeping maintenance costs low.

By Price Range: Economy Segment Leads While Premium Grows Fastest

Economy lines captured 48.35% of 2025 sales, whereas the premium band, including reinforced composites and designer collaborations, is rising at a 5.67% CAGR through 2031. Consumers increasingly pay 15-25% above mid-market tags for recycled or biodegradable content, lifting gross margins and funding R&D.

Mid-range offerings blur the cost-value gap by adopting gas-assist finishes and advanced pigments that mimic natural textures while staying price-competitive. Brand portfolios now span economy to premium within common mold platforms, simplifying tooling yet diversifying retail positioning. The resulting laddered assortment aligns with widening household income tiers across emerging Asia-Pacific and Latin America, sustaining momentum for the plastic furniture market.

By Distribution Channel: Online Retail Disrupts Traditional Models

B2C/retail channels still account for 61.10% of global turnover, but within that slice, online retail grows at a 6.08% CAGR as virtual showrooms border on mainstream. Home centers benefit from immediate take-home convenience, although market share erodes as mobile-first shoppers secure free shipping and easy returns. Specialty stores remain relevant in the premium tier, where tactile assessment underpins buying confidence.

The B2B/project lane caters to large-volume rollouts in education and hospitality. Yet here too, digitalization gains ground, with configurators enabling architects to download BIM objects and order factory-pre-assembled sets in one click. Rural Handmade reports AR visualization tools cutting return rates by nearly one-third, tipping both consumers and specifiers toward e-commerce checkouts. Lightweight plastics, consistent color bans, and minimal part counts enhance the online fit, reinforcing the channel shift within the plastic furniture market.

Geography Analysis

North America anchored 34.70% of global revenue in 2025, sustained by robust consumer spending, a mature DIY culture, and growing interest in recycled resin products. United States homeowners drive spring-season spikes as landscaping projects fold patio upgrades into mortgage refinancing budgets. Canada follows a seasonal rhythm, while Mexico emerges as a growth pocket on the back of rising homeownership and mall expansions that stock affordable plastic SKUs. Environmental regulation is tightening, with several U.S. states debating minimum recycled content mandates, pushing producers toward closed-loop resin contracts.

Asia-Pacific represents the fastest trajectory, advancing at a 5.88% CAGR from 2026-2031. China champions supply depth and rising domestic demand for cost-efficient décor. India trails closely, buoyed by a growing middle class that favors versatile furniture for compact flats. Southeast Asia’s dual-speed picture shows Singapore and Malaysia leaning premium, whereas Indonesia and Vietnam pack volume in the economy tier. Tropical climates enable year-round patio usage, smoothing seasonal swings and offering continuous shelf velocity for outdoor sets, thereby enlarging the plastic furniture market.

Europe balances premium design with stringent eco rules. The United Kingdom and Germany spearhead recycled-plastic certification, while Spain and Italy emphasize alfresco dining sets to suit Mediterranean lifestyles. Eastern Europe supplies incremental upside as incomes swell and e-commerce infrastructure matures. Rethink Plastic Alliance notes that 64% of European furniture buyers now request transparent lifecycle disclosures, making environmental footprints a central brand metric. Digital channels grow twice as fast as brick-and-mortar for plastic furniture, capitalizing on efficient parcel networks and consumer confidence in return policies.

Competitive Landscape

The plastic furniture market remains moderately fragmented: global names such as IKEA, Keter Group, and Rubbermaid coexist with regional specialists that tailor catalogs to local tastes and climate. Sustainability is the new battleground. IKEA targets a 70% cut in transport emissions and an 80% absolute logistics reduction by 2040, influencing upstream freight choices and prompting suppliers to adopt rail or biofuel shipping options. Several players integrate backward by contracting plastic recyclers, ensuring long-term feedstock and price stability.

Design innovation offers differentiation for mid-sized firms. ScanCom International’s DuraPlast pairs virgin and reclaimed polymers in weather-resistant lounge sets, extending warranty periods and opening new hospitality accounts. Technology further reshapes rivalry: brands embed NFC chips in chair frames to authenticate recycled content claims, while logistics platforms optimize last-mile routes to curb costs and emissions.

Market entrants leverage DTC channels; low tool-up costs and cloud-based storefronts let them challenge incumbents without vast capital. However, meeting upcoming microplastic limits will steepen compliance hurdles, likely prompting consolidation as smaller outfits license patented resins from larger peers. Overall, pricing power rests with firms that mix design pedigree, recycling capacity, and agile distribution within the plastic furniture market.

Plastic Furniture Industry Leaders

Keter Group

Nilkamal Limited

Supreme Industries Limited

Tramontina

Cosmoplast Industrial Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IKEA ranked third in sustainable supply chains, highlighting a plan to cut transport emissions by 70% and overall logistics emissions by 80% by 2040.

- May 2025: Penn State Behrend announced the Innovation & Emerging Plastics Technologies Conference for June 2025, drawing 200 industry engineers.

- January 2024: Vitra had transitioned to producing the Eames Plastic Chair using post-consumer recycled polypropylene, a change that had advanced the company’s climate objectives and had enabled the chair to be recyclable at the end of its lifecycle.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the plastic furniture market as the value of new, finished indoor and outdoor household or commercial fixtures molded mainly from polymer resins, typically polypropylene, polyethylene, polycarbonate, or recycled blends, sold through retail and contract channels during 2019-2030.

Scope exclusion: Fixtures whose primary structure is metal, wood, or rattan with only plastic trims are outside our scope.

Segmentation Overview

- By Product

- Chairs

- Tables

- Stools

- Cabinets

- Sofas

- Shelves

- Other Products

- By End User

- Residential

- Commercial

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B /Project

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with resin suppliers, contract furniture buyers, online retail merchandisers, and facility managers across North America, Europe, and Asia-Pacific. The conversations validated unit price brackets, clarified recycled-content adoption rates, and aligned scenario assumptions on urban outdoor living trends that secondary sources only hinted at.

Desk Research

We first map the demand pool using freely accessible statistics, such as United Nations Comtrade trade codes for HS 940370, the US Census Bureau's Housing Starts, Eurostat furniture production indices, and environmental data from PlasticsEurope. Company filings, trade-show catalogs, and press releases then reveal typical average selling prices and new product launches. Paid datasets like D&B Hoovers and Dow Jones Factiva help our analysts sanity-check firm-level revenues. These references illustrate, not exhaust, the secondary sources consulted during data collection, validation, and clarification.

A second pass benchmarks regional shipment flows with customs dashboards and association portals (e.g., American Home Furnishings Alliance, British Plastics Federation) to confirm import-export balances and spot substitution toward recycled resin lines.

Market-Sizing & Forecasting

We anchor the 2024 base year by combining a top-down reconstruction of global production and trade volumes, adjusted for regional consumption ratios, with selective bottom-up checks from supplier roll-ups and sampled ASP × unit calculations. Key variables in the model include virgin and recycled resin prices, per-capita residential floor-space additions, outdoor leisure spending, e-commerce penetration in furniture sales, and regulatory shifts on single-use plastics that spur recycled lines. Multivariate regression links these drivers to historical market values; an ARIMA overlay smooths cyclical swings before forecasts are stress-tested through expert scenarios. Data gaps in smaller countries are bridged by regional proxy coefficients derived from primary interviews.

Data Validation & Update Cycle

Outputs pass a two-step analyst review, anomaly flags trigger rechecks against alternative data signals, and results are signed off only after variance falls within the accepted tolerance band. Reports refresh every twelve months, with interim updates after material supply-chain or policy events.

Why Mordor's Plastic Furniture Baseline Commands Reliability

Estimates across publishers often diverge because each defines product mix, price tiers, and refresh cadence differently. Our disciplined scope selection and annual revision rhythm minimize such drift.

Key gap drivers include: some firms fold in wood-plastic composites, others extrapolate sales from limited online panels, and a few convert currencies using static rates that inflate dollar totals during strong local-currency years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.80 B (2025) | Mordor Intelligence | - |

| USD 25.93 B (2024) | Global Consultancy A | Includes hybrid wood-plastic lines and uses optimistic e-commerce mark-ups |

| USD 13.33 B (2023) | Trade Journal B | Excludes commercial contract sales and applies constant 2020 resin prices |

The comparison shows that when scope breadth, price normalization, and update cadence are harmonized, Mordor's balanced baseline offers decision-makers a transparent figure tethered to reproducible variables and steps.

Key Questions Answered in the Report

What is the current value of the plastic furniture market?

The market is worth USD 17.56 billion in 2026 and is projected to reach USD 21.88 billion by 2031.

Which region grows fastest in plastic furniture sales?

Asia-Pacific leads with a 5.88% CAGR forecast for 2026-2031, propelled by rapid urbanization and a rising middle class.

Why are cabinets the quickest-growing product category?

Urban space constraints drive demand for modular storage, giving cabinets a 5.12% CAGR outlook through 2031.

How does e-commerce influence the plastic furniture market?

Online retail in B2C channels is advancing at a 6.08% CAGR as AR tools cut return rates and flat-pack plastics reduce shipping costs.

What sustainability trends shape product development?

Manufacturers increasingly use recycled polymers and closed-loop systems, enabling price premiums of 15-25% and better regulatory compliance.

Which price segment expands fastest?

The premium tier grows at 5.67% CAGR through 2031, thanks to design upgrades and consumer preference for eco-friendly materials.

Page last updated on: