Atomizing Metal Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

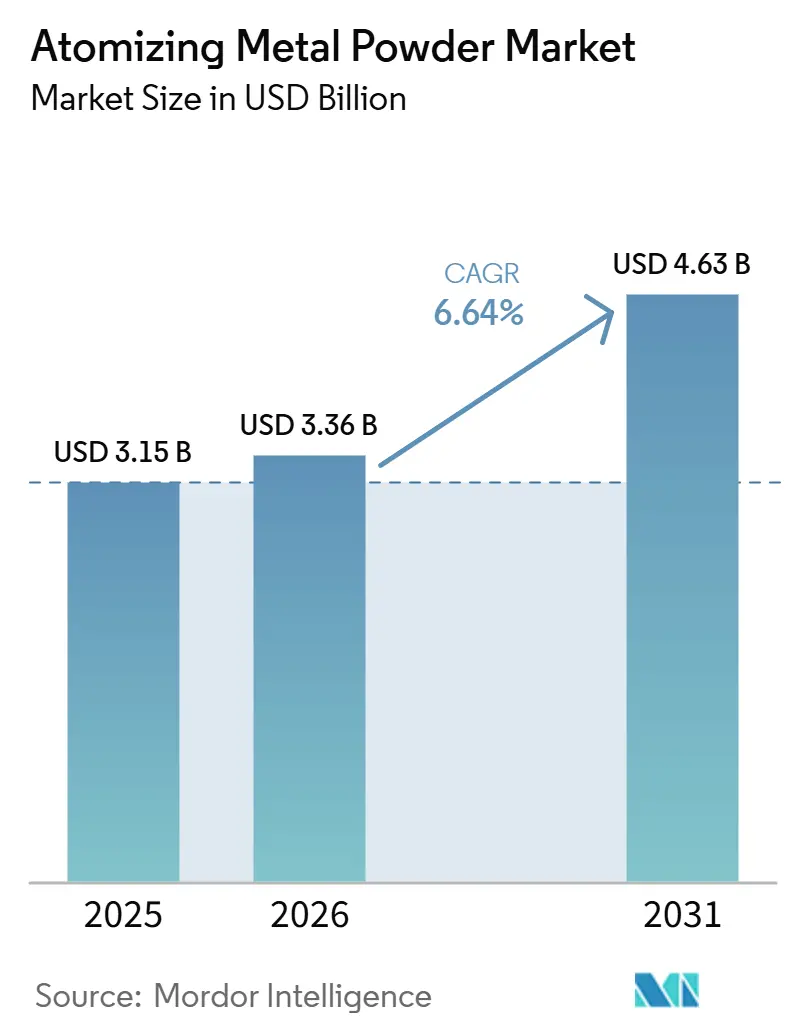

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atomizing Metal Powder Market Analysis by Mordor Intelligence

The Atomizing Metal Powder Market size is projected to expand from USD 3.15 billion in 2025 and USD 3.36 billion in 2026 to USD 4.63 billion by 2031, registering a CAGR of 6.64% between 2026 and 2031. Consistent demand for ultra-low-oxygen titanium and nickel-superalloy powders in hydrogen-ready gas turbines, the pivot to battery-grade spherical copper and aluminum powders, and the shift from conventional powder-metallurgy to precision additive-manufacturing feedstocks are the main forces lifting the Atomizing metal powder market. Plasma atomization is gaining traction as aerospace and medical-device firms tighten oxygen specifications, while micro-scale, containerized atomizers shorten lead times and enable closed-loop recycling at the point of use. North American reshoring programs backed by Defense Production Act grants are expanding domestic capacity, yet Asia-Pacific still leads by volume as Chinese, South Korean, and Japanese powders dominate battery supply chains. Supplier margins remain sensitive to helium price volatility and to rigorous ISO 52907 powder-quality audits that add up to USD 1,500 per ton in inspection costs.

Key Report Takeaways

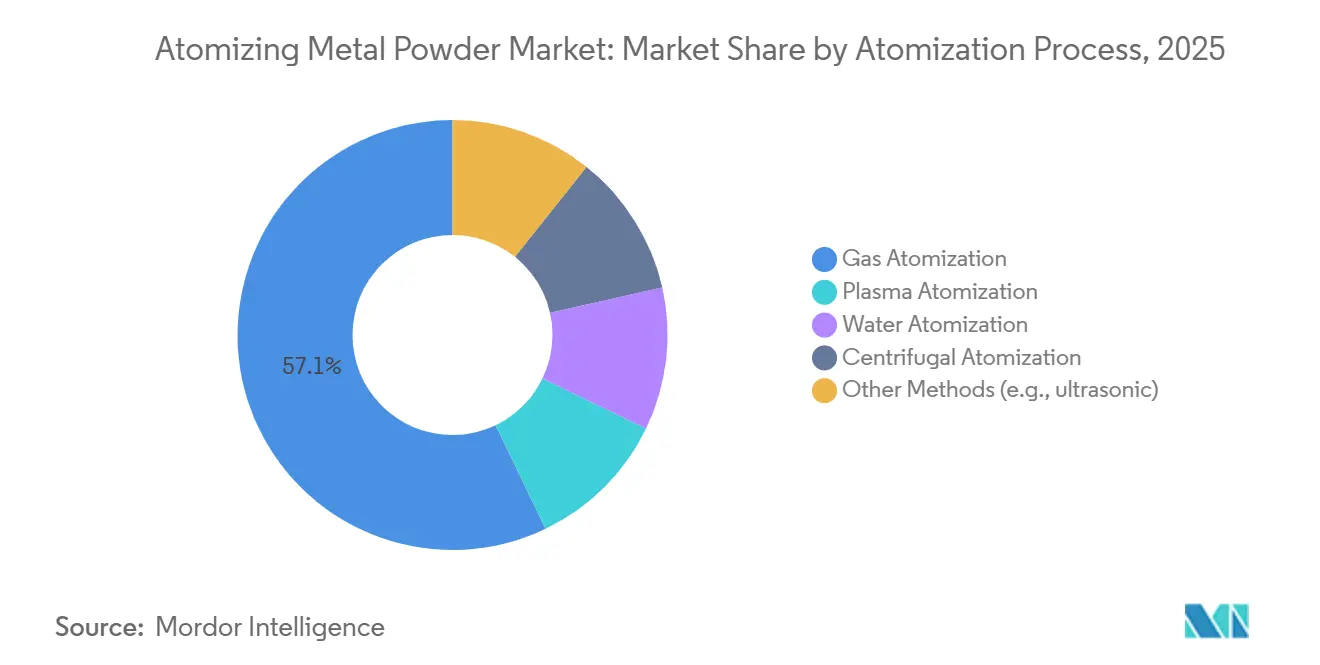

- By the atomization process, gas atomization commanded 57.12% of the Atomizing Metal Powder market share in 2025, while plasma atomization is projected to grow at a 6.88% CAGR during the forecast period (2026-2031).

- By metal type, stainless steel powders held 30.11% of the Atomizing Metal Powder market size in 2025, whereas titanium and superalloy powders are forecast to accelerate at a 7.03% CAGR to 2031.

- By application, additive manufacturing (AM/3DP) led with 40.44% revenue share in 2025, and is expected to post the highest 6.43% CAGR during 2026-2031.

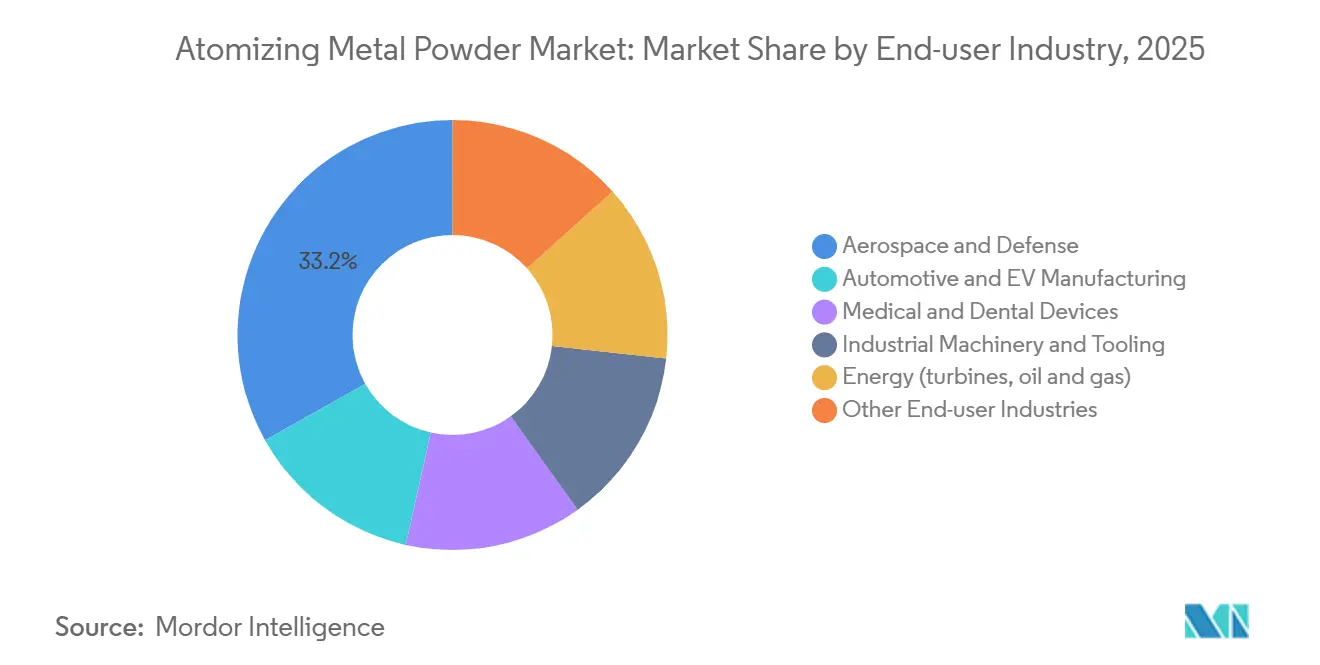

- By end-user industry, aerospace and defense accounted for a 33.15% share of the Atomizing Metal Powder market size in 2025, and automotive and EV manufacturing are expected to grow at a CAGR of 6.94% during the forecast period (2026-2031).

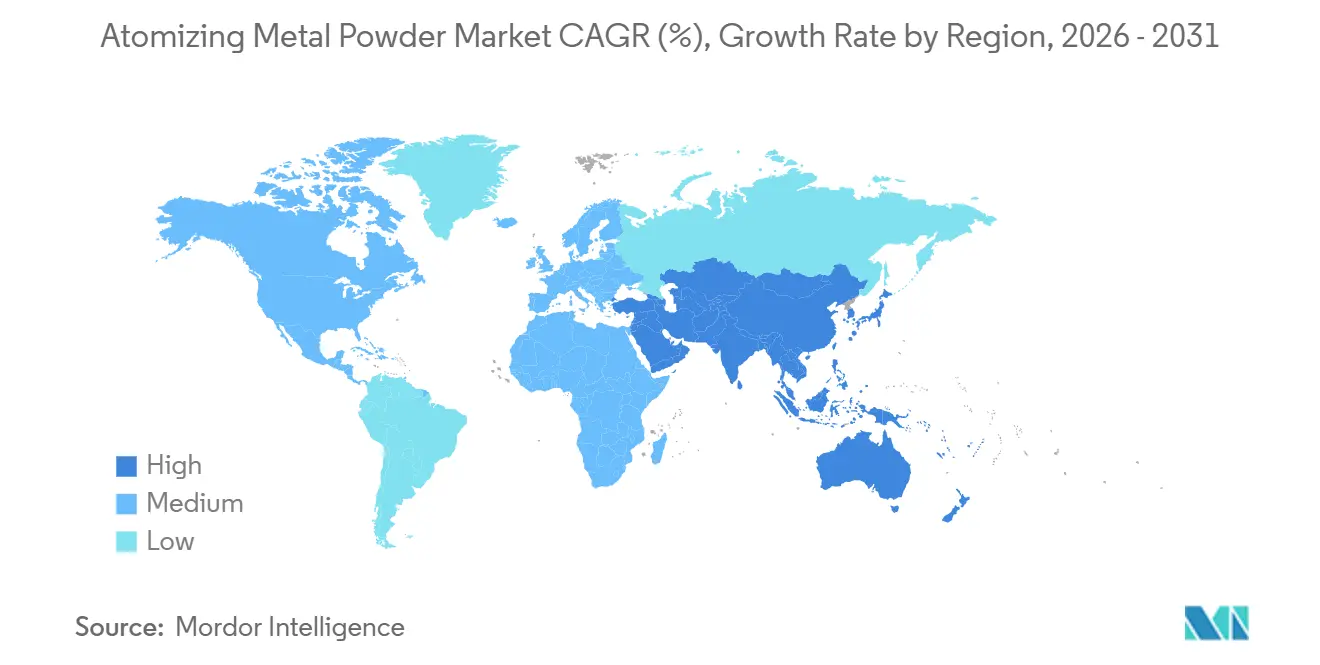

- By geography, Asia-Pacific captured 39.56% of the Atomizing Metal Powder market share in 2025 and is forecast to expand at a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Atomizing Metal Powder Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding demand for high-performance PM parts in aerospace and EVs | +1.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| Surging need for advanced titanium, nickel, and HEA powders | +1.5% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Decentralized micro-atomization for on-demand supply | +0.9% | North America and Europe | Short term (≤2 years) |

| Ultra-low-oxygen powders for hydrogen turbines and energy systems | +1.2% | Europe and North America | Medium term (2-4 years) |

| Battery-grade spherical Cu and Al powders for next-gen cells | +1.3% | Asia-Pacific core, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Demand for High-Performance PM Parts in Aerospace and EVs

Commercial airframe builders deploy more than 300 additive-manufactured components in the GE9X turbofan, cutting engine weight and lowering fuel burn by 10%[1]General Electric, “GE9X Commercial Engine,” ge.com. United States gas-turbine makers validate hydrogen blends up to 75%, raising consumption of nickel-based superalloy powders qualified to sub-300 ppm oxygen limits. Electric-vehicle platforms replace cast brackets with sintered steel and aluminum parts to trim mass per kilowatt-hour, a change mirrored in the 22.6% jump in North American aluminum powder shipments during 2024. Medical suppliers received five titanium spinal and maxillofacial implant clearances in Q1 2026 alone, reinforcing additive-manufacturing traction. These combined pulls add almost two percentage-points to the Atomizing metal powder market growth outlook.

Surging Need for Advanced Titanium, Nickel, and HEA Powders

FAA (Federal Aviation Administration) clearance of rapid-plasma-deposited titanium structures and Airbus-GE supply deals for 1,000 tons of titanium feedstock confirm industrial acceptance of premium alloys. Commercial volumes of high-entropy alloy powders entered the catalogs of three specialty suppliers in 2025, widening alloy menus for hypersonic vehicles and cryogenic pumps. Sandvik expanded capacity in the United Kingdom and Sweden, under AS9100D certification, to deliver oxygen-controlled nickel and titanium grades. Plasma-atomized titanium production exceeded 1,000 tons cumulative at TEKNA by late 2025, underscoring maturity. Demand for these alloys lifts the Atomizing metal powder market trajectory by 1.5 percentage-points.

Decentralized Micro-Atomization for On-Demand Supply

Container-size units such as AMAZEMET’s Powder2Powder systems recycle coarse fractions on-site, trimming scrap and freight costs by 30%. PyroGenesis commercialized turnkey plasma atomizers that deliver non-standard 45-106 µm titanium cuts favored by large aerospace primes. A Ukrainian-backed investment brought a USD 60 million micro-atomization plant to the United States, adding 230 skilled jobs and diversifying supply risk. 6K Additive’s UniMelt reactors switch chemistries in hours, supporting one-off heat-resistant alloys for turbine trials. Micro-atomization lifts short-run responsiveness and injects 0.9 percentage-points into forecast growth.

Ultra-Low-Oxygen Powders for Hydrogen Turbines and Energy Systems

A 2025 magnesium-assisted TiH₂ route achieved less than 800 ppm oxygen in titanium powder, meeting hydrogen turbine requirements. Oak Ridge researchers demonstrated sub-500 ppm iron powder via hydrogen reduction, promising cleaner sintered components. Siemens Energy entered a long-term pact with 6K Additive for microwave-plasma nickel powders, cutting energy use 91% and carbon 91.5% versus gas atomization[2]Siemens Energy, “Hydrogen Capable Gas Turbines,” siemens-energy.com. Mitsubishi Heavy Industries printed hydrogen combustor nozzles from ultra-clean powder in 2025 field tests. These advances improve turbine durability and add 1.2 percentage-points to the Atomizing Metal Powder market expansion.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent QC on particle-size distribution, morphology, and flowability | -0.7% | Global, acute in North America and Europe | Short term (≤2 years) |

| Helium price volatility for plasma and gas atomization | -0.5% | Global, highest in North America | Medium term (2-4 years) |

| Limited closed-loop recycling for reactive and critical powders | -0.6% | Global, severe in Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent QC on Particle-Size Distribution, Morphology, and Flowability

ISO 52907 and new ASTM powder-analysis standards require every batch to pass laser diffraction, Hall flow, and CT imaging, raising quality-control overhead by up to USD 1,500 per tonne. Satellite particles reduce flowability by up to 30%, forcing extra sieving that cuts yield from 85% to 65% and drives strategic throttling of capacity, as seen when Höganäs produced 412,000 tons against 500,000 tons nameplate in 2024. North American feedstock shipments fell 10% the same year because OEMs (original equipment manufacturers) delayed orders until suppliers proved tighter reproducibility. These requirements shave 0.7 percentage-points off forecast CAGR.

Helium Price Volatility for Plasma and Gas Atomization

United States reserve divestitures and Qatari delays lifted helium spot prices above USD 300 per Mcf in 2025, tripling 2020 levels and slicing 8-12% from plasma-atomization margins. Plasma systems need up to 15 m³ of helium per kilogram of titanium powder, adding USD 5 per kilogram in gas cost, yet aerospace primes still absorb the premium for sub-300 ppm oxygen powders. Smaller service bureaus pivot to argon or water atomization, but higher oxygen pickup restricts end-use scope.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Atomization Process: Plasma Gains on Oxygen Purity

Gas atomization retained 57.12% of 2025 volume owing to cost advantages, while water atomization served price-sensitive iron and tool-steel powders. Plasma atomization is projected to rise at a 6.88% CAGR, outstripping the Atomizing Metal Powder market average because aerospace and medical buyers demand oxygen below 300 ppm.

Plasma's non-standard cut flexibility was proven when PyroGenesis won Boeing qualification for 45-106 µm Ti-6Al-4V feedstock. Gas atomization remains critical for stainless steel and aluminum grades, but its dominance in the Atomizing metal powder market will gradually erode as quality specifications tighten and helium pricing stabilizes.

By Metal Type: Titanium and Superalloys Outpace Stainless Steel

Stainless steel powders commanded 30.11% of 2025 sales, yet titanium and nickel superalloys will capture incremental share at a 7.03% CAGR through 2031. The titanium category alone is set to climb substantially in the Atomizing Metal Powder market size as GE Additive supplies 1,000 tons of titanium powder to Airbus under a multi-year deal.

Nickel-based powders benefit from the 6K-Siemens alliance, delivering 91% carbon cuts and will likely reach double-digit share before 2031. Stainless steel keeps a foothold in automotive sintered parts where 316L and 17-4PH grades meet cost and corrosion targets, but its Atomizing metal powder market share may dip below over the forecast horizon. High-entropy alloys remain niche but command premium pricing that bolsters revenue even at low tonnage.

By Application: Additive Manufacturing Extends Leadership Over Conventional Powder Metallurgy

Additive manufacturing captured 40.44% of the Atomizing Metal Powder market share in 2025 and is projected to grow at a 6.43% CAGR through 2031 as airframe builders, orthopedic-implant makers, and tool-and-die shops certify ever larger series components. Medical approvals in Q1 2026 for titanium devices, like the Ventana A ALIF cage and SpineLinc cervical implant, are boosting Ti-6Al-4V feedstock orders. Aerospace leads additive use, with GE9X turbines using 304 printed parts, including TiAl blades that cut fuel use by 10%. This drives nickel-superalloy powder adoption for hydrogen blends up to 75%.

In 2024, North America saw a drop in conventional powder-metallurgy shipments, like valve seats and oil-pump gears, due to inventory adjustments and flowability issues. Nickel-base and cobalt-chrome powders gained traction in coatings for turbine blade repairs and petrochemical wear sleeves, though their share stayed below 10% due to overspray reuse. Tungsten-carbide powder shipments in 2024, driven by defense machining contracts, will offset tariff-related import shortfalls from China.

By End-User Industry: Automotive and EV Outpace Aerospace on Battery-Grade Powder Demand

Aerospace and defense absorbed 33.15% of global volume in 2025 as engine makers chased ultra-low-oxygen titanium and nickel powders for hydrogen-ready turbines, but automotive and EV producers are now advancing at a 6.94% CAGR to 2031, the fastest among all sectors. Light-weighting mandates also spur the switch from cast iron to pressed-and-sintered gears and stators, raising the baseline demand floor for medium-cost iron, steel, and aluminum powders.

Medical and dental OEMs, although representing less tonnage, continue to lift revenue because of the premium pricing commanded by plasma-atomized titanium and cobalt-chrome grades cleared for patient-specific implants. Energy-sector buyers, led by Siemens Energy’s hydrogen-capable turbine line, secure long-term nickel-superalloy supply agreements that insulate them from helium volatility yet keep a decent overall share because unit volumes remain modest versus automotive batteries. Collectively, these shifts mean automotive and EV applications will narrow the volume gap with aerospace by the decade’s end, further diversifying the Atomizing metal powder market size and cushioning suppliers against cyclical swings in any single industry.

Geography Analysis

Asia-Pacific dominated 39.56% of the Atomizing Metal Powder market in 2025 and is racing ahead at a 7.12% CAGR to 2031 as CNPC Powder, Avimetal, and Epson Atmix together add more than 10,000 tons of new capacity by end-2026. Local export controls on critical minerals push the region to build in-house recycling plants, yet helium sourcing and hydrogen-ready quality standards remain open challenges.

In North America, aluminum powder volumes surged 22.6% on electric-vehicle demand, and tungsten carbide climbed on defense machining requirements. Velta's USD 60 million investment in a United States titanium manufacturing facility, backed by Ukrainian foreign direct investment, reflects strategic reshoring to reduce geopolitical supply risk. 6K Additive's USD 23.4 million Defense Production Act Title III grant to scale from 200 metric tons per year to 1,000 metric tonnes per year underscores federal prioritization of domestic nickel-alloy and titanium powder capacity.

Europe's market share in 2025 is anchored by Höganäs' 500,000 tons per year capacity across 15 production sites, with biochar infrastructure investment to replace 20% of fossil coal by 2026 and China relocation completion in 2026. Sandvik's commissioning of two additional gas-atomization towers at Neath, United Kingdom, and a new plant in Sandviken, Sweden, for titanium and nickel alloys under AS9100D certification positions Europe to serve aerospace and medical-device OEMs.

South America and the Middle East-Africa together account for a relatively small market share yet display above-average automotive and petrochemical demand, suggesting a potential fast-follower pattern once regional recycling supply chains mature.

Competitive Landscape

The Atomizing Metal Powder market is moderately fragmented. Mergers and acquistion activity is likely as incumbents seek plasma know-how and disruptors search for distribution muscle. The competitive emphasis shifts from sheer tonnage to certification speed, localized inventory, and carbon intensity metrics demanded by OEM (original equipment manufacturer) scorecards.

Atomizing Metal Powder Industry Leaders

Höganäs AB

Sandvik AB

GKN Powder Metallurgy

General Electric Company

Oerlikon AM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Inland Atomize Metal Powder LLP (IAMP), based in Gujarat, India, began production of metal powders at its new manufacturing facility. Once fully operational, IAMP expects to produce up to 700 metric tons of metal powder annually. The company uses Vacuum Induction Gas Atomization (VIGA) and a hydrometallurgy process to produce a wide range of metal powders.

- August 2025: MITSUBISHI STEEL MFG. CO., LTD. is pioneering a gas-atomizing system to produce metal powders for additive manufacturing, commonly known as metal 3D printing. This gas atomization technique involves ejecting molten metal, specifically liquid steel, from a nozzle in a fine stream.

Global Atomizing Metal Powder Market Report Scope

Atomizing metal powder is the process of breaking molten metal into tiny droplets that solidify into powder, primarily for additive manufacturing, metal injection molding (MIM), and powder metallurgy.

The Atomizing Metal Powder market is segmented by atomization process, metal type, application, end-user industry, and geography. By the atomization process, the market is segmented into gas atomization, plasma atomization, water atomization, centrifugal atomization, and other methods (e.g., ultrasonic). By metal type, stainless steel powders, titanium and superalloy powders, aluminum powders, copper and copper-alloy powders, nickel-based alloys, and other metals and alloys. By application, the market is segmented into additive manufacturing (AM/3DP), powder-metallurgy components/parts, cutting tools and wear parts, coatings and thermal-spray materials, and other industrial applications. By end-user industry, the market is segmented into aerospace and defense, automotive and EV manufacturing, medical and dental devices, industrial machinery and tooling, energy (turbines, oil and gas), and other end-user industries. The report also covers the market size and forecasts for atomizing metal powder in 18 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Gas Atomization |

| Plasma Atomization |

| Water Atomization |

| Centrifugal Atomization |

| Other Methods (e.g., ultrasonic) |

| Stainless Steel Powders |

| Titanium and Superalloy Powders |

| Aluminum Powders |

| Copper and Copper-Alloy Powders |

| Nickel-based Alloys |

| Other Metals and Alloys |

| Additive Manufacturing (AM/3DP) |

| Powder-Metallurgy Components/Parts |

| Cutting Tools and Wear Parts |

| Coatings and Thermal-Spray Materials |

| Other Industrial Applications |

| Aerospace and Defense |

| Automotive and EV Manufacturing |

| Medical and Dental Devices |

| Industrial Machinery and Tooling |

| Energy (turbines, oil and gas) |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Atomization Process | Gas Atomization | |

| Plasma Atomization | ||

| Water Atomization | ||

| Centrifugal Atomization | ||

| Other Methods (e.g., ultrasonic) | ||

| By Metal Type | Stainless Steel Powders | |

| Titanium and Superalloy Powders | ||

| Aluminum Powders | ||

| Copper and Copper-Alloy Powders | ||

| Nickel-based Alloys | ||

| Other Metals and Alloys | ||

| By Application | Additive Manufacturing (AM/3DP) | |

| Powder-Metallurgy Components/Parts | ||

| Cutting Tools and Wear Parts | ||

| Coatings and Thermal-Spray Materials | ||

| Other Industrial Applications | ||

| By End-user Industry | Aerospace and Defense | |

| Automotive and EV Manufacturing | ||

| Medical and Dental Devices | ||

| Industrial Machinery and Tooling | ||

| Energy (turbines, oil and gas) | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Atomizing metal powder market in 2031?

The Atomizing Metal Powder market is forecast to reach USD 4.63 billion by 2031 from USD 3.36 billion in 2026, growing at a CAGR of 6.64%.

Which atomization process is growing fastest toward 2031?

Plasma atomization is advancing at an estimated 6.88% CAGR due to sub-300 ppm oxygen requirements in aerospace and medical parts.

Why are titanium and nickel superalloy powders drawing heightened demand?

Hydrogen-ready turbines and lightweight airframe components need ultra-clean titanium and nickel alloys that resist high-temperature fatigue and corrosion.

How is helium price volatility affecting powder producers?

Spot prices above USD 300 per Mcf have inflated plasma-atomization gas costs by up to USD 5 per kg, compressing margins and nudging some users toward argon.

Page last updated on: