Precious Metal Catalysts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

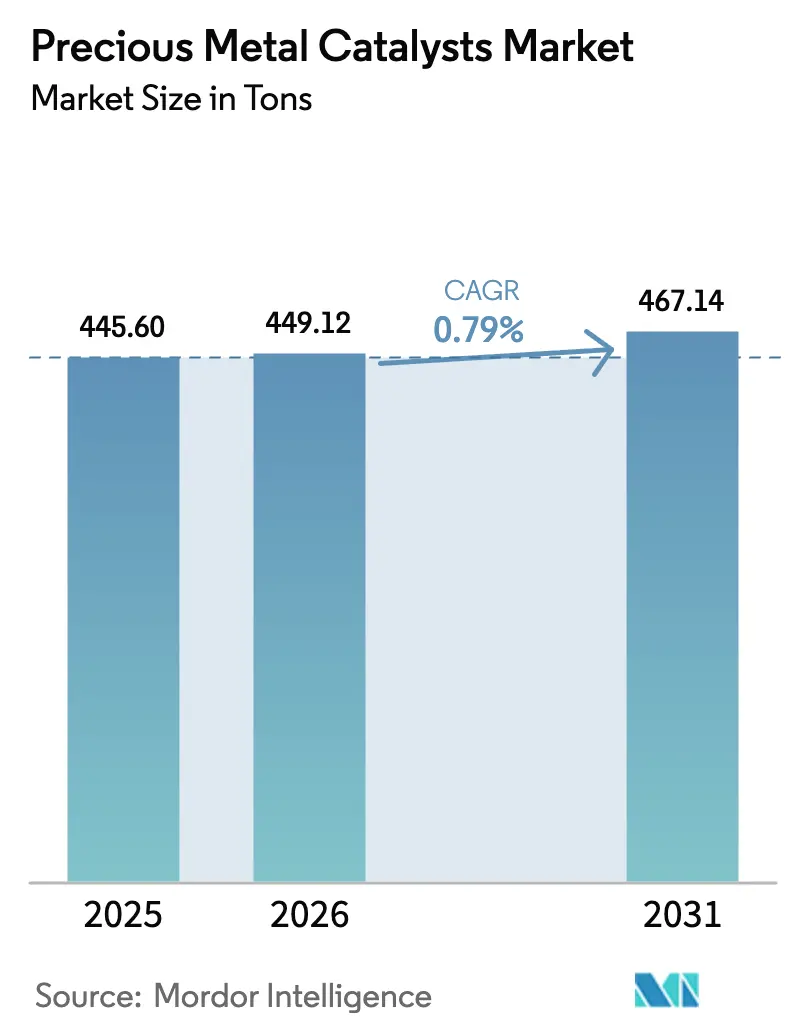

| Market Volume (2026) | 449.12 tons |

| Market Volume (2031) | 467.14 tons |

| Growth Rate (2026 - 2031) | 0.79% CAGR |

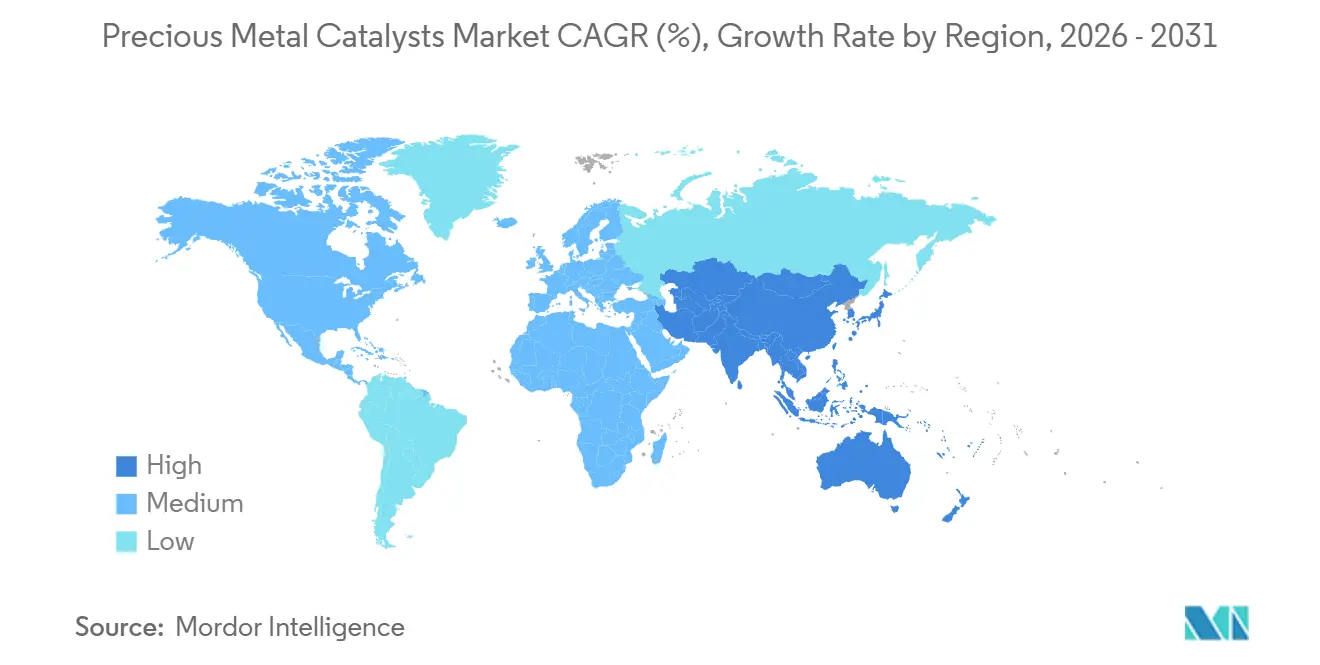

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precious Metal Catalysts Market Analysis by Mordor Intelligence

The Precious Metal Catalysts Market size was valued at 445.60 tons in 2025 and is estimated to grow from 449.12 tons in 2026 to reach 467.14 tons by 2031, at a CAGR of 0.79% during the forecast period (2026-2031). Modest headline growth co-exists with pronounced shifts in demand mix, most notably the gradual erosion of autocatalyst volumes, the rapid scale-up of green-hydrogen electrolyzers, and rising precision requirements in pharmaceutical synthesis. Intensifying Euro 7, China VI-b, and Bharat Stage VII regulations are lifting per-vehicle platinum-group-metal (PGM) loadings even as battery-electric vehicles (BEVs) temper unit shipments. Simultaneously, PEM electrolyzer build-outs are pulling iridium and platinum into double-digit expansion corridors, encouraging suppliers to widen recycling loops and deploy AI-assisted formulation platforms. Strategic hedges—platinum substitution for palladium, angstrom-level atomic-layer deposition (ALD), and digital-twin process optimization—are defending margins against volatile PGM spot prices. Portfolio rebalancing toward fuel-cell, refinery, and pharmaceutical catalysts is becoming a central competitive lever as incumbents confront a bifurcated growth landscape.

Key Report Takeaways

- By metal type, platinum commanded 40.92% of the precious metal catalysts market share in 2025, while iridium is advancing at a 3.01% CAGR through 2031.

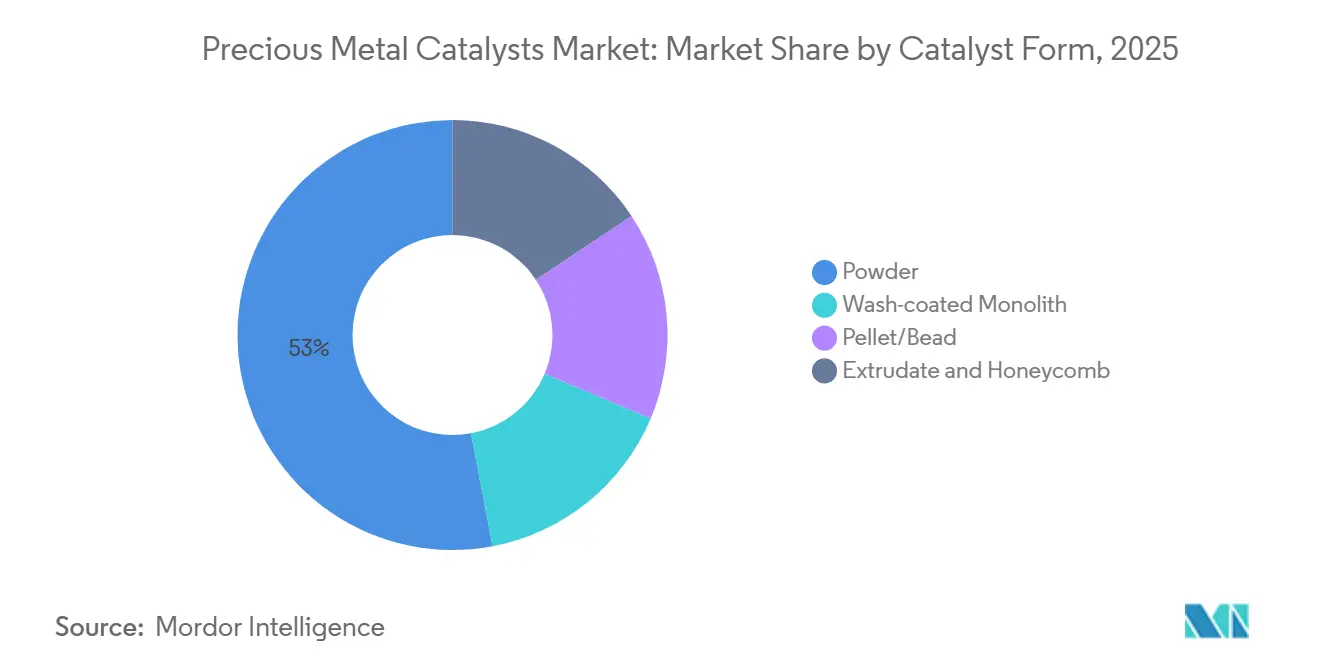

- By catalyst form, powder variants accounted for 52.98% of the precious metal catalysts market in 2025, while wash-coated monoliths are anticipated to grow with a 1.66% CAGR through 2031.

- By manufacturing process, incipient-wetness impregnation held 47.18% share of the precious metal catalysts market size in 2025; chemical vapour/atomic layer deposition is recording the highest projected CAGR at a 2.93% CAGR through 2031.

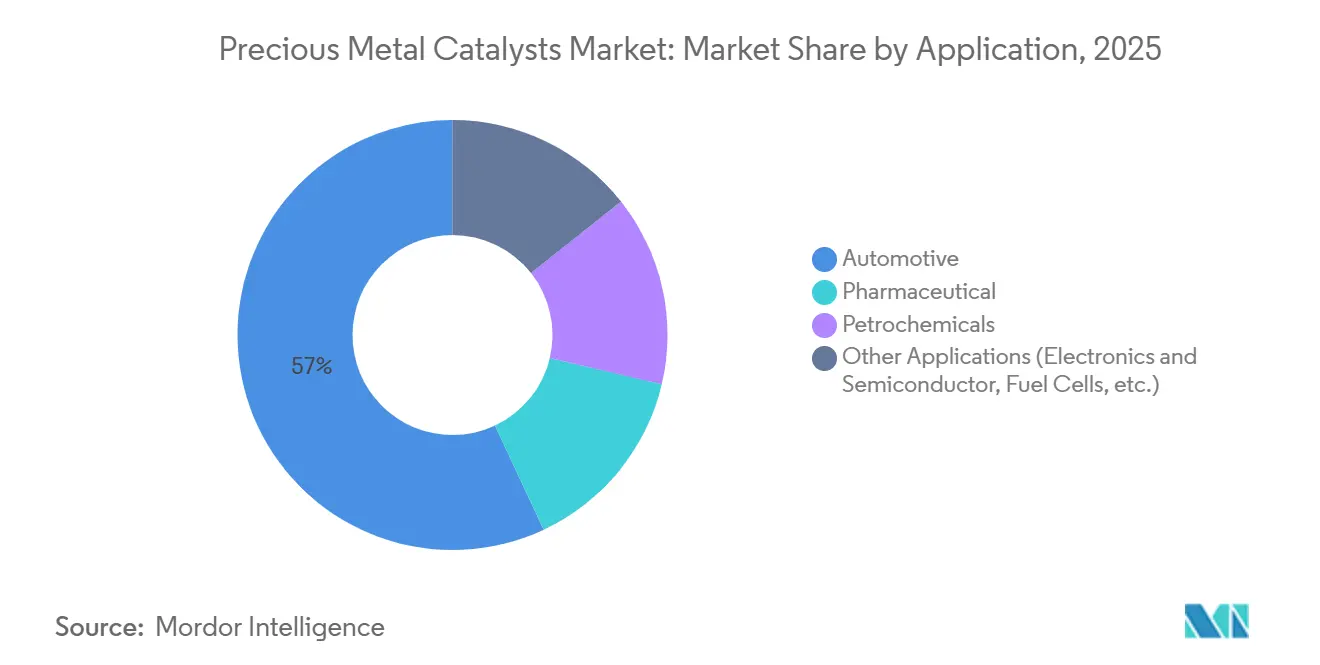

- By application, automotive maintained a 56.98% revenue share in 2025; the other applications segment, including fuel cells, electronics, and green hydrogen, is forecast to expand at a 2.78% CAGR to 2031.

- By geography, Asia-Pacific accounted for 39.82% of the precious metal catalysts market size in 2025 and is projected to grow at a 1.22% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Precious Metal Catalysts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter tail-pipe and stationary-emission standards | +0.3% | Global, with peak enforcement in EU, China, and India | Medium term (2-4 years) |

| Petro-refinery shift to higher-octane clean fuels | +0.2% | North America, Middle East, APAC refining hubs | Long term (≥ 4 years) |

| Platinum substitution for palladium in tri-metal autocatalysts | +0.1% | Europe, North America | Short term (≤ 2 years) |

| Green-hydrogen build-out spurring Ir/Pt catalyst demand | +0.4% | Europe, Japan, South Korea, early APAC adopters | Long term (≥ 4 years) |

| AI-designed reaction pathways trimming PGM loadings | +0.3% | Global, with peak enforcement in EU, North America and the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Tail-Pipe and Stationary-Emission Standards

The European Commission finalized Euro 7 in late 2025 for 2027 implementation, forcing OEMs to raise rhodium and palladium loadings by 15-20% per vehicle. China’s National VI-b, effective July 2024, triggered a 12% increase in PGM catalyst demand among domestic automakers in 2025. India’s Bharat Stage VII (April 2028) will extend real-driving-emission caps to two-wheelers, creating a fresh addressable segment. U.S. EPA Tier 4 Final standards are simultaneously boosting platinum-based oxidation catalysts for non-road diesel engines. The net result is a value-accretive mix enrichment that partially offsets stagnant ICE volumes.

Petro-Refinery Shift to Higher-Octane Clean Fuels

International Maritime Organization sulfur caps and regional low-sulfur gasoline mandates are driving refinery upgrades that favor platinum-on-alumina catalysts for hydroprocessing[1]American Petroleum Institute, “Low-Sulfur Fuel Standards Update,” api.org. Saudi Aramco’s Jazan refinery, commissioned in 2024, deployed more than 200 tons of precious-metal catalysts across its hydrocracking trains. Reliance Industries earmarked USD 1.2 billion in 2025 for BS-VII compliance at Jamnagar, anchoring incremental demand for platinum-rhenium catalysts. These investments underpin a parallel growth avenue that balances BEV-driven autocatalyst attrition.

Platinum Substitution for Palladium in Tri-Metal Autocatalysts

With palladium averaging USD 2,100/oz versus platinum at USD 950/oz in 2025, OEMs reformulated three-way catalysts, lifting platinum content from roughly 15% to near 30% of PGM mass. Stellantis raised platinum share to 28% of its Euro 6d catalyst systems, trimming palladium usage by 600 kg annually across European plants. Advances in washcoat chemistry mitigate platinum’s historical light-off limitations, stabilizing aggregate PGM demand even as palladium volumes soften.

Green-Hydrogen Build-Out Spurring Ir/Pt Catalyst Demand

Germany’s H2Global allocated EUR 4.5 billion in 2025, catalyzing orders for 2 GW of PEM electrolyzers that will require 18-22 tons of iridium by 2027. Japan’s 2026 hydrogen roadmap funnels JPY 300 billion into electrolyzer manufacturing, prioritizing iridium recycling to ease supply bottlenecks. PEM cathodes also absorb platinum, while ruthenium-platinum alloys are gaining share for enhanced corrosion resistance.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent PGM price volatility and supply shocks | -0.2% | Global, acute in APAC and Europe reliant on South African/Russian supply | Short term (≤ 2 years) |

| EV penetration shrinking ICE autocatalyst demand | -0.3% | China, Europe, North America | Medium term (2-4 years) |

| Rising recycling rates denting primary demand | -0.1% | Global, concentrated in regions with mature collection infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent PGM Price Volatility and Supply Shocks

Rhodium vacillated between USD 9,200 and USD 14,000/oz in 2025 after South African mine outages cut supply by 18%[2]Anglo American Platinum, “2025 Interim Production Report,” angloamericanplatinum.com. Russian palladium exports fell 40 tons under sanctions, forcing European formulators to buy higher-priced recycled metal. Iridium jumped 35% on electrolyzer orders, deferring several PEM projects. Tier 2 suppliers without integrated recycling absorbed a 400-600 bp margin compression under fixed-price contracts.

EV Penetration Shrinking ICE Autocatalyst Demand

China’s BEV share hit 38% of 2025 passenger-car sales, removing roughly 12,000 autocatalyst replacement cycles in Beijing and Shanghai ride-hailing fleets. Europe reached 22% BEV penetration in 2025 as targeted subsidies continued. The U.S. IRA tax credit doubled BEV share to 11%, prompting catalyst firms to accelerate diversification into fuel-cell and pharmaceutical segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal Type: Iridium Scales Fastest Despite Platinum Dominance

Platinum retained a 40.92% share in 2025, anchored by its versatility across autocatalyst, refinery, and pharmaceutical platforms. Iridium, though small in absolute terms, is expanding at a 3.01% CAGR on the back of PEM electrolyzer deployment. Ruthenium is carving a niche in chlor-alkali and ammonia catalysts for process-economic gains. AI-optimized nanoparticles are halving iridium intensity in 1-MW electrolyzers, reinforcing a value-over-volume trajectory.

Atomic-layer deposition is crucial here: Johnson Matthey demonstrated 50% higher oxygen-evolution rates with iridium dots on titanium oxide, cutting metal intensity per MW in half. For platinum, narrowing discounts to palladium are opening price headroom that sustains formulation experimentation.

By Catalyst Form: Powder Leads, Monoliths Gain on Integration Efficiencies

Powder catalysts accounted for 52.98% of 2025 demand, dominating pharmaceutical batch reactors and refinery fixed beds thanks to easy regeneration. Wash-coated monoliths are growing at a 1.66% CAGR, as automotive and stationary emission systems prize low pressure drop. Umicore’s 2025 rhodium-free monolith meets Euro VI limits with 30% less total PGM. Pellet forms target hydrogenation reactors where mechanical strength offsets costs. Integration efficiencies place monoliths at the forefront of emission-control research and development, while powders retain primacy where batch flexibility prevails.

By Manufacturing Process: ALD Scales as Precision Demands Rise

Incipient-wetness impregnation held a 47.18% share in 2025 owing to its low cost and scalability for automotive catalysts. Chemical vapour or atomic layer deposition (ALD) is advancing at a 2.93% CAGR as fuel-cell and fine-chemical producers demand sub-nanometer precision. Heraeus’ new ALD line delivers platinum mass activity 40% above impregnation benchmarks. Impregnation remains optimal for refinery catalysts where 0.3-0.5 wt% platinum loadings suffice. Electrochemical deposition is making headway in electrolyzers, producing iridium coats with superior adhesion.

By Application: Automotive Holds Majority, Fuel Cells Emerge

Automotive catalysts still held a 56.98% share in 2025, yet BEV substitution trims absolute volume even as per-vehicle PGM intensity rises. Pharmaceutical catalysts enable over 60% of global generic hydrogenations. Petrochemical catalysts underpin gasoline and aromatics production, especially in Middle Eastern and Asian refineries. Fuel cells and electrolyzers sit in the “other applications” bucket and are growing with the fastest CAGR of 2.78%. Iridium and platinum tonnage are on a steep up-curve as regional hydrogen roadmaps solidify. Toyota’s plan to triple Mirai output implies an extra 1.2 tons of platinum cathode demand by 2027.

Geography Analysis

Asia-Pacific controlled 39.82% of the 2025 volume and is set to grow at a 1.22% CAGR despite China’s NEV policy headwinds. China’s National VI-b raised PGM loadings per ICE by 14% in 2025, cushioning catalyst volume decline. Japan’s JPY 300 billion electrolyzer subsidy is pivoting the supply chain toward iridium recycling, with TANAKA tripling PEM catalyst capacity. India’s Bharat Stage VII will boost two-wheeler catalyst penetration from below 40% today, adding significant upside. South Korea’s 12,000 NEXO deliveries in 2025 kept platinum cathode volumes buoyant.

North America remains value-dense: U.S. refiners installed 8 tons of platinum catalysts to meet Tier 3 sulfur requirements in 2025. Europe’s EUR 3 billion electrolyzer funding is funneling iridium demand into Germany, Spain, and the Netherlands. South America leans on Brazil’s ethanol blend mandate, driving platinum-rhenium reforming catalyst purchases. The Middle East benefits from new hydrocracking trains at Jazan, while South Africa leverages domestic PGM mining for competitive recycling logistics.

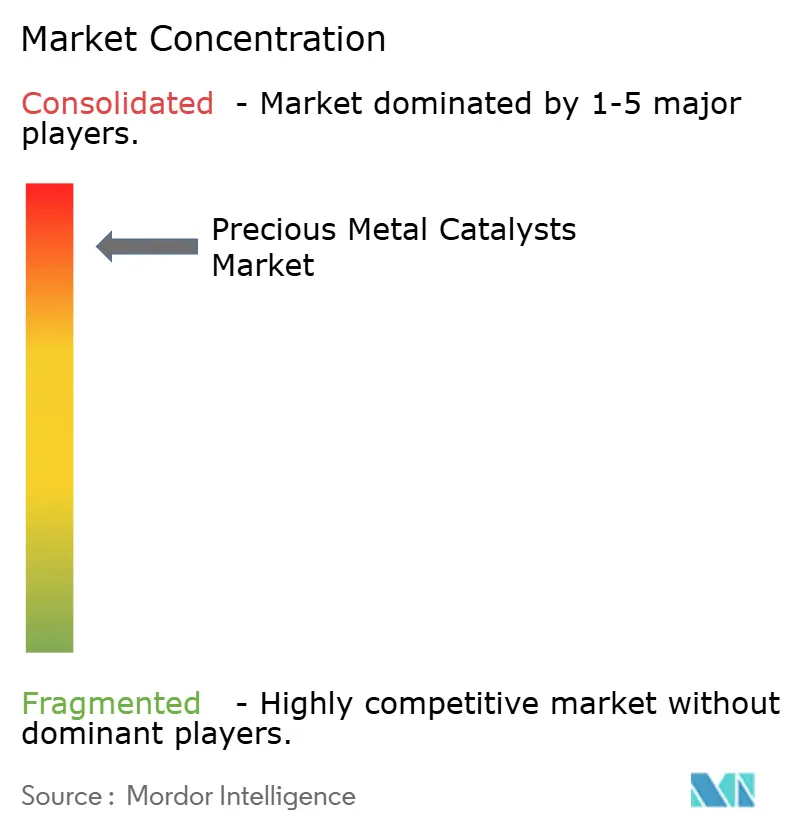

Competitive Landscape

The precious metal catalysts market demonstrates moderate consolidation. Closed-loop recycling has become a critical differentiator. For example, Umicore sources 52% of its feedstock from secondary PGM recovery, achieving an 18% reduction in Scope 3 emissions. Patent filings for AI-designed catalysts have increased by 40% year-on-year, with leading players such as BASF and Clariant leveraging machine learning to optimize bimetallic synergies. Chinese competitors Kaili Catalyst and Shaanxi Kaida have achieved 22% growth by capitalizing on their proximity to OEMs under the China VI-b regulations. Tier 1 companies are allocating USD 50-100 million annually to ALD and AI technologies to maintain profitability in high-value segments like fuel cells and pharmaceuticals. Meanwhile, Tier 2 companies are concentrating on incremental improvements in impregnation efficiency. Additionally, white-space opportunities are emerging in iridium recycling for PEM membranes and ruthenium catalysts for chlor-alkali cells.

Precious Metal Catalysts Industry Leaders

BASF

Honeywell International, Inc.

Umicore

Heraeus Precious Metals

Clariant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Umicore approved a EUR 120 million expansion at Hanau to triple iridium-catalyst capacity and install a 95% recovery loop targeting REPowerEU electrolyzer demand.

- November 2025: BASF and Siemens Energy formed a joint venture to commercialize fuel-cell catalysts with 40% lower platinum loadings; pilot output is slated for mid-2027.

- September 2025: Heraeus commissioned a USD 75 million ALD facility in Hanau for sub-nanometer platinum and iridium coatings, adding 12 tons of annual PEM catalyst capacity.

Global Precious Metal Catalysts Market Report Scope

Precious metal catalysts, also known as noble metal catalysts, are widely used in the chemical industry because they can speed up the chemical process. Precious metals possess an incompletely filled d-orbital to lend or withdraw electrons from the reagent, depending on the nature of the reaction. They show high activity and selectivity in catalysis.

The precious metal catalysts market is segmented by type, application, and geography. The market is segmented by type into platinum, palladium, rhodium, iridium, ruthenium, and other types. The market is segmented by application into automotive, pharmaceutical, petrochemicals, and other applications. The report also covers the market size and forecasts for the precious metal catalysts market in 15 countries across major regions. Each segment's market sizing and forecasts are based on volume (tons).

| Platinum |

| Palladium |

| Rhodium |

| Iridium |

| Ruthenium |

| Other Metal Types (Osmium, Gold, Silver) |

| Powder |

| Pellet / Bead |

| Extrudate and Honeycomb |

| Wash-coated Monolith |

| Incipient Wetness Impregnation |

| Electroless and Electrochemical Deposition |

| Chemical Vapour / Atomic Layer Deposition |

| Sol-Gel / Precipitation |

| Other Advanced Nano-structuring |

| Automotive |

| Pharmaceutical |

| Petrochemicals |

| Other Applications (Electronics and Semiconductor, Fuel Cells, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Metal Type | Platinum | |

| Palladium | ||

| Rhodium | ||

| Iridium | ||

| Ruthenium | ||

| Other Metal Types (Osmium, Gold, Silver) | ||

| By Catalyst Form | Powder | |

| Pellet / Bead | ||

| Extrudate and Honeycomb | ||

| Wash-coated Monolith | ||

| By Manufacturing Process | Incipient Wetness Impregnation | |

| Electroless and Electrochemical Deposition | ||

| Chemical Vapour / Atomic Layer Deposition | ||

| Sol-Gel / Precipitation | ||

| Other Advanced Nano-structuring | ||

| By Application | Automotive | |

| Pharmaceutical | ||

| Petrochemicals | ||

| Other Applications (Electronics and Semiconductor, Fuel Cells, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the precious metal catalysts market in 2026?

The market is estimated at 449.12 tons in 2026, with a 0.79% CAGR projected to 2031.

Which metal type holds the largest share in the precious metal catalysts space?

Platinum maintains leadership with 40.92% of 2025 volume.

How fast is iridium demand growing?

Iridium demand is advancing at a 3.01% CAGR, driven by PEM electrolyzer deployments.

Why are monolith catalysts gaining traction?

Wash-coated monoliths cut pressure drop and noble-metal inventory, growing at a 1.66% CAGR.

How significant is the Asia-Pacific region in global demand?

Asia-Pacific accounted for 39.82% of the 2025 volume and is the fastest-growing region at a 1.22% CAGR.

What strategic move are suppliers using to mitigate PGM price swings?

Expanded closed-loop recycling now supplies over half of Umicore’s feedstock, insulating margins.

Page last updated on: