Polycarboxylate Ether Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.74 Billion |

| Market Size (2031) | USD 9.03 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polycarboxylate Ether Market Analysis by Mordor Intelligence

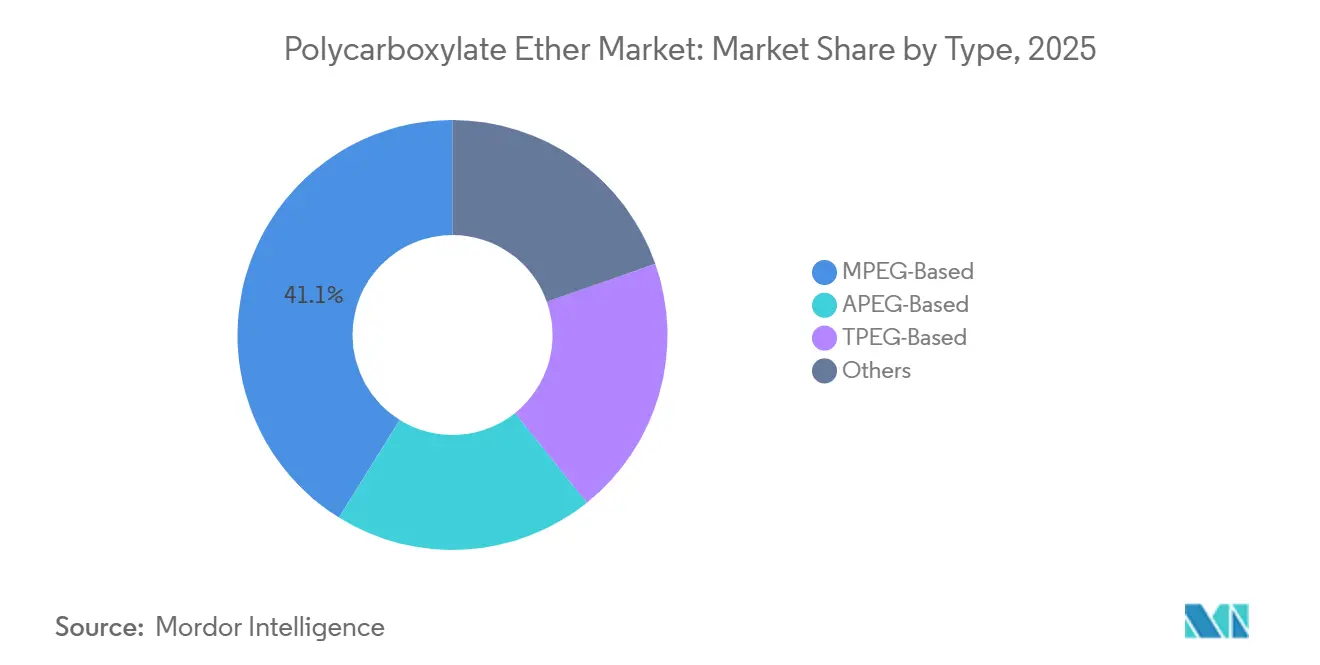

The Polycarboxylate Ether Market size is projected to expand from USD 7.51 billion in 2025 and USD 7.74 billion in 2026 to USD 9.03 billion by 2031, registering a CAGR of 3.12% between 2026 and 2031. Asia-Pacific retained 45.25% of the Polycarboxylate Ether market share in 2025, underpinned by India’s expanding ready-mix concrete networks and Southeast Asia’s infrastructure pipelines, but China’s 45% residential-construction contraction between 2023 and 2025 created a counterweight. Emerging binder chemistries such as limestone calcined clay cement (LC3) and geopolymer concrete can either raise dosage needs or divert demand toward alternative superplasticizers, prompting suppliers to pursue differentiated formulations that maintain workability at reduced water-cement ratios. Among product types, MPEG-based grades held 41.14% share in 2025 on cost advantages, yet TPEG-based variants are forecast to grow at 3.26% CAGR through 2031 because they preserve slump for more than 120 minutes in hot-weather, long-distance pumping conditions. Liquid products dominated with 74.56% share, but powder formulations are advancing at 3.78% CAGR thanks to 70% shipment-volume savings that appeal to Africa, the Middle East, and landlocked Asian nations.

Key Report Takeaways

- By type, MPEG captured 41.14% of the polycarboxylate ether market share in 2025, whereas TPEG is projected to record the fastest 3.26% CAGR through 2031.

- By form, liquid products led with 74.56% share in 2025; powder variants are poised to grow at a 3.78% CAGR to 2031.

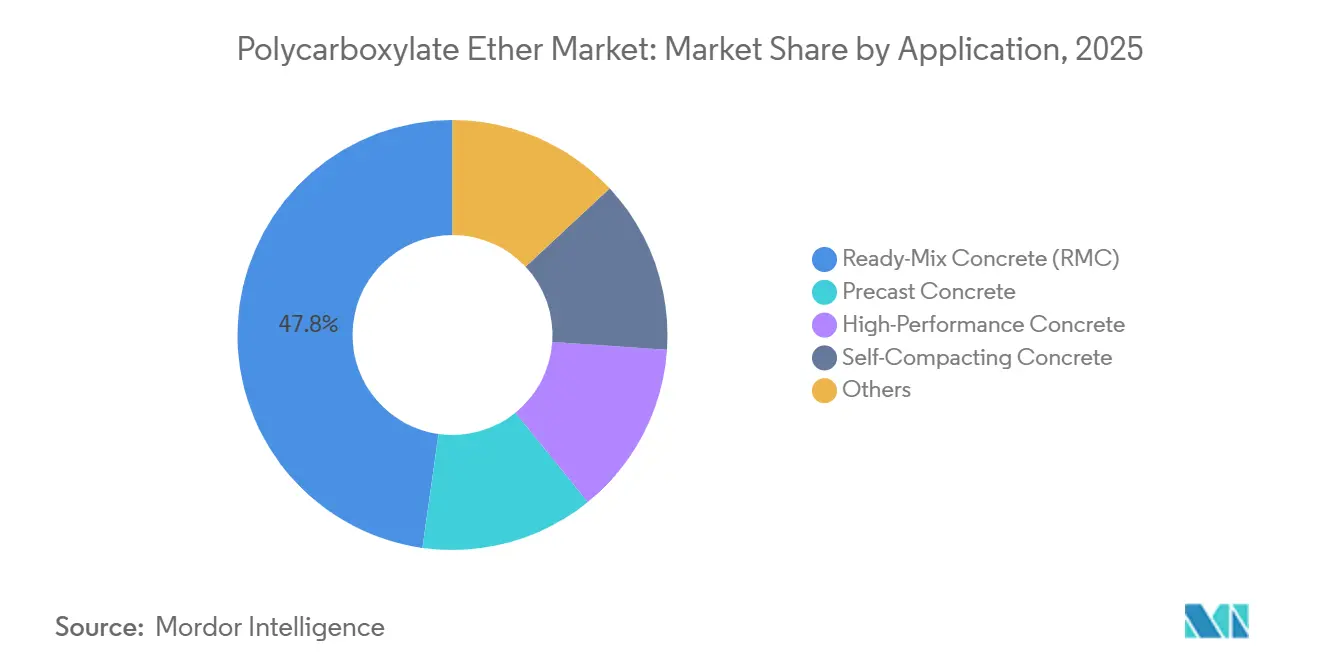

- By application, ready-mix concrete accounted for 47.78% of the 2025 polycarboxylate ether market size, while self-compacting concrete will advance at a 3.51% CAGR over 2026-2031.

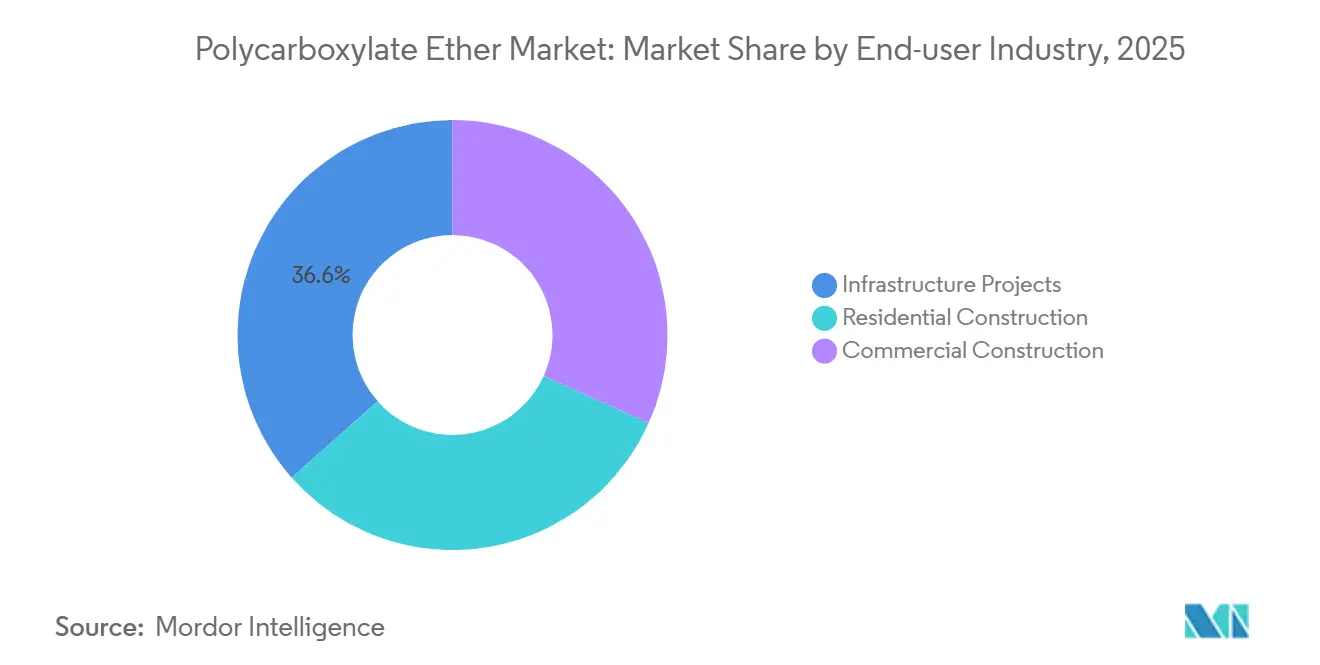

- By end-user industry, infrastructure projects held 36.55% revenue share in 2025; residential construction is forecast to accelerate at a 3.61% CAGR through 2031.

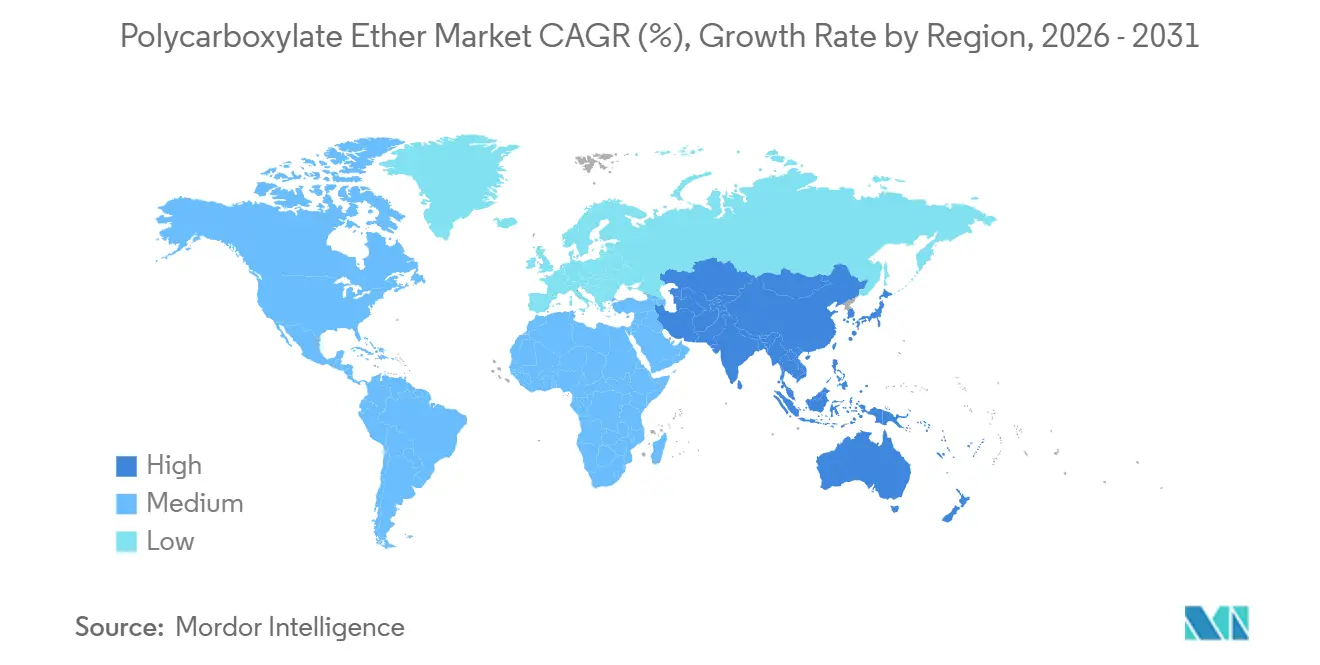

- By geography, Asia-Pacific dominated with 45.25% share in 2025 and is expected to remain the fastest-growing region, expanding at a 3.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polycarboxylate Ether Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid infrastructure investment across Asia-Pacific and Africa | +1.2% | Asia-Pacific (excluding China residential), Middle East & Africa | Medium term (2-4 years) |

| Tightening water-cement-ratio rules in green building codes | +0.6% | Global, with early adoption in EU, North America, and select Asia-Pacific metros | Long term (≥ 4 years) |

| Expansion of RMC batching plants in tier-2 cities | +0.8% | India, China tier-2/3, ASEAN, Latin America | Short term (≤ 2 years) |

| 3D-printed concrete needs rheology-tuned super-plasticizers | +0.3% | North America, EU, select Asia-Pacific hubs (Singapore, South Korea) | Long term (≥ 4 years) |

| Liquid-cooled data-center slabs demand ultra-low-shrinkage mixes | +0.4% | North America, EU, Asia-Pacific (Singapore, India, Australia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Infrastructure Investment Across Asia-Pacific and Africa

South Asia, Southeast Asia, and Africa together earmarked more than USD 250 billion for transport corridors, power grids, and water projects slated for 2026-2028; the Asian Development Bank alone allocated USD 98.6 billion for that window[1]Asian Development Bank, “Infrastructure Outlook 2026,” adb.org. Funds are channeling toward concrete used in bridges, highways, and metro systems, where long-haul pumping favors TPEG-based chemistries thanks to 120-minute slump retention. Africa’s annual infrastructure gap of roughly USD 170 billion is stimulating demand for powder-grade admixtures that cut freight volumes by 70%, a decisive cost advantage on landlocked routes. These capital programs collectively lift the Polycarboxylate Ether market by an estimated 1.2 percentage-point CAGR contribution through 2031.

Tightening Water-Cement-Ratio Rules in Green Building Codes

Municipal ordinances in Berkeley, California, cap water-cement ratios below 0.40 for projects above 5,000 ft², effectively mandating high-range water reducers such as Polycarboxylate Ether products to maintain workability. The EU’s Environmental Product Declaration scheme grants life-cycle-carbon credits for mixes that substitute 15-20% cement with supplementary materials, a target difficult to reach without advanced superplasticizers[2]European Federation of Concrete Admixtures, “EPD and Carbon Credits 2026,” efca.eu. LEED v5 and BREEAM 2024 now award extra points to slabs achieving the same sub-0.40 ratio, reinforcing a structural pull through 2031.

Expansion of RMC Batching Plants in Tier-2 Cities

India commissioned almost 300 new batching facilities across secondary cities from 2020-2025, with Shree Cement scaling to 45 RMC (ready-mix concrete) plants by end-2026. Polycarboxylate Ether market penetration in India’s tier-1 metros already tops 85%; the next adoption wave lies in the 60-70% uptake band of tier-2 locations. Similar patterns emerge in China’s smaller urban clusters, where MUHU and Sobute compete on price while international incumbents target premium mixes that conform to slump-loss specifications over one-hour transport cycles.

3D-Printed Concrete Needs Rheology-Tuned Super-Plasticizers

U.S. Marine Corps barracks built with robotic extrusion illustrate the labor and schedule savings of 3D-printed concrete, but yield-stress requirements oscillate by 30% with 10°C ambient swings, demanding adaptive dosing. Polymer side-chain architecture is being re-engineered to deliver low viscosity (less than 100 Pa) at the nozzle, yet stiffen to more than 1,000 Pa within one minute after deposition. Suppliers that scale such formulations early could carve a premium niche before standards coalesce.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental scrutiny of non-biodegradable polymer residues | -0.4% | EU, North America, select Asia-Pacific markets (Japan, South Korea) | Medium term (2-4 years) |

| Patent thickets around comb-polymer architectures | -0.3% | Global, with highest friction in North America and EU | Long term (≥ 4 years) |

| Rise of LC3 and geopolymer concrete reducing PCE dosage | -0.5% | India, Africa, Southeast Asia, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental Scrutiny of Non-Biodegradable Polymer Residues

The European Union (EU) microplastics restriction 2023/2055 forces admixture producers to document degradation paths for polyethylene-oxide side chains; a 2028 review could rescind current construction exemptions. The U.S. EPA’s updated Toxic Substances Control Act inventory likewise obliges manufacturers to disclose molecular-weight distributions, adding USD 50,000-100,000 compliance cost per formulation. These pressures accelerate research into lignin-based alternatives that deliver 28-32 % water reduction yet command 20-25 % higher cost.

Patent Thickets Around Comb-Polymer Architectures

BASF’s US11851384B2 covers grafting densities from 0.15-0.35 mol/100 g, Sika’s US11952310B2 secures terminal-hydroxyl combs enhancing adsorption at 35°C, and Dow’s US11945763B2 locks in TPEG designs above 35°C, collectively squeezing new entrants. Royalty rates of 3-5% of net sales leave a limited margin for low-scale producers, especially in markets where price competition is intense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: TPEG Gains on Performance, MPEG Holds Cost Edge

MPEG held 41.14% Polycarboxylate Ether market share in 2025 because its cost sits 20-25% below TPEG. TPEG, however, is forecast for a 3.26% CAGR during the forecast period (2026-2031) owing to 120-minute slump retention in 35-45°C pours, essential for remote infrastructure segments. The Polycarboxylate Ether market size for TPEG-based grades could rise by 2031 if current specifications persist, while APEG remains niche for precast. BASF’s May 2025 boost in Pluriol A2400I capacity confirms accelerating TPEG demand.

Regional preferences diverge: Middle East megaprojects overwhelmingly specify TPEG, China’s tier-2 builders substitute MPEG to win bids, and Europe is slowly pivoting toward TPEG as infrastructure specs lengthen transport windows. Emerging lignin-based and phosphonate-modified types are expected to have a minimal share by 2031, owing to feedstock and process bottlenecks, but may command premium pricing where bio-based or clay-tolerant credentials are mandated.

By Form: Powder Variants Gain in Logistics-Constrained Markets

Liquid products dominated 74.56% of the Polycarboxylate Ether market size in 2025 due to plug-and-play batching. Powder forms, though, are anticipated to grow at 3.78% CAGR during the forecast period (2026-2031), taking share in Africa, the Middle East, and Central Asia, where freight savings exceed 40% on long ocean-plus-road voyages. A shift of even five percentage points toward powder could lift its revenue contribution substantially by 2031.

Dissolution times have shrunk below three minutes through spray-drying advances, removing the chief operational barrier for high-throughput plants. In Europe and North America, powder-grade uptake in dry-mix mortars and self-leveling compounds supports just-in-time prefabrication strategies, solidifying a premium sub-segment that sells at 10-15% price lifts over liquid equivalents.

By Application: Self-Compacting Concrete Rises as Labor Costs Climb

Ready-mix concrete retained 47.78% share of the Polycarboxylate Ether market size in 2025, yet self-compacting concrete is set for a faster 3.51% CAGR during the forecast period (2026-2031), fueled by 8-12% annual wage inflation in India, Vietnam, and Indonesia. Eliminating vibration cuts placement time 30-40% and reduces noise by 15-20 dB, benefits that justify 25-30% higher admixture doses. High-performance bridge and tunnel mixes using 0.25-0.35% Polycarboxylate Ether plus 30-40% supplementary cementitious materials target 60 MPa compressive strength and less than 1,000 coulomb chloride permeability, consolidating a durable growth pocket tied to aging infrastructure upgrades.

By End-user Industry: Residential Gains as Housing Mandates Multiply

Infrastructure captured 36.55% of the 2025 Polycarboxylate Ether market share; still, residential construction is the fastest-growing at 3.61% CAGR through 2031, aided by India’s plan for 20 million urban units under Pradhan Mantri Awas Yojana (Urban). Affordable-housing codes now call for 25 MPa concrete, a specification seldom met without modern superplasticizers.

Data-center slabs within the commercial bucket form a high-value micro-segment demanding shrinkage below 400 µstrain, a parameter necessitating 20-25% higher Polycarboxylate Ether dosage. The interplay between these two end-users will gradually narrow the historical dominance of infrastructure projects, but is unlikely to displace them before the next decade.

Geography Analysis

Asia-Pacific commanded 45.25% of the Polycarboxylate Ether market share in 2025 and should sustain a 3.79% CAGR to 2031. India’s Polycarboxylate Ether market is buoyed by a ready-mix expansion, with new batching plants in Nagpur, Ranchi, Raipur, and Gandhinagar driving uptake. Conversely, China’s 45% residential downturn curtailed polymer demand in top-tier metros, though a CNY 1 trillion infrastructure stimulus preserved concrete production at 2.4 billion m³ in 2024. Southeast Asian nations executing the ASEAN Connectivity master-plan corridors increased Polycarboxylate Ether market penetration in ready-mix to roughly 60% by 2026.

North America's share in 2025 was strengthened by the USD 550 billion Infrastructure Investment and Jobs Act, which is channeling funds to bridges and broadband foundations requiring high-performance concrete. The region’s hyperscale data-center boom is another accelerant: more than 40 sites broke ground in 2025 alone, each specifying ultra-low-shrinkage mixes. Sika’s December 2025 automated plant in Florida demonstrates local capacity buildup to meet Southeastern U.S. demand.

Europe’s market share reflects recovery from the 2023-2024 slump; Germany and France resumed stalled urban-mobility projects, while Eastern Europe leverages EU Cohesion Funds for transport upgrades. BASF’s Pluriol A2400I expansion provides regional feedstock security for TPEG-based grades amid stricter EPD rules. The Middle East & Africa and South America exhibit above-average growth. Saudi Arabia and the UAE specify TPEG polymers for mega-projects facing 45°C site temperatures, whereas South Africa’s ZAR 1 trillion (USD 59.4 billion) infrastructure pipeline uses powder grades to sidestep long-haul liquid shipping costs. Brazil’s market is rebounding as Sika extends admixture output to serve mining and ready-mix clients.

Competitive Landscape

The Polycarboxylate Ether market is moderately concentrated. Competitive intensity peaks in China’s tier-2 markets; MUHU and Sobute undercut prices, compressing gross margins to 20-25% and limiting research and development investment for next-generation phosphonate-modified polymers. Multinational incumbents instead differentiate through service bundles, such as Sika’s Verifi on-truck monitoring suite, which delivers real-time dosage adjustment that can trim cement consumption 5-7% per load, anchoring high-stickiness customer relationships.

Polycarboxylate Ether Industry Leaders

BASF

MAPEI S.p.A.

Sika AG

Arkema

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sika AG opened a new production facility in Ust-Kamenogorsk with production lines for mortar and concrete admixtures (such as polycarboxylate ether), as well as a modern laboratory. The plant is Sika’s fourth factory in Kazakhstan and is located in a key industrial region in the country.

- May 2025: BASF Industrial Formulators expanded its portfolio of reactive polyethylene glycol with the introduction of Pluriol A 2400 I. This new product is tailored for polycarboxylate ethers (PCE) used in Europe's construction sector.

Global Polycarboxylate Ether Market Report Scope

Polycarboxylate Ether (PCE) is a high-performance, third-generation superplasticizer used in the construction industry to significantly reduce water usage while enhancing the workability, flow, and strength of concrete.

The Polycarboxylate Ether market is segmented by type, form, application, end-user industry, and geography. By type, the market is segmented into MPEG-based, APEG-based, TPEG-based, and others. By form, the market is segmented into liquid and powder. By application, the market is segmented into ready-mix concrete (RMC), precast concrete, high-performance concrete, self-compacting concrete, and others. By end-user industry, the market is segmented into residential construction, commercial construction, and infrastructure projects. The report also covers the market size and forecasts for polycarboxylate ether in 16 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| MPEG-Based |

| APEG-Based |

| TPEG-Based |

| Others |

| Liquid |

| Powder |

| Ready-Mix Concrete (RMC) |

| Precast Concrete |

| High-Performance Concrete |

| Self-Compacting Concrete |

| Others |

| Residential Construction |

| Commercial Construction |

| Infrastructure Projects |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | MPEG-Based | |

| APEG-Based | ||

| TPEG-Based | ||

| Others | ||

| By Form | Liquid | |

| Powder | ||

| By Application | Ready-Mix Concrete (RMC) | |

| Precast Concrete | ||

| High-Performance Concrete | ||

| Self-Compacting Concrete | ||

| Others | ||

| By End-user Industry | Residential Construction | |

| Commercial Construction | ||

| Infrastructure Projects | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is expected demand for global Polycarboxylate Ether in 2026 and 2031?

The Polycarboxylate Ether Market size is projected to expand from USD 7.51 billion in 2025 and USD 7.74 billion in 2026 to USD 9.03 billion by 2031, registering a CAGR of 3.12% between 2026 and 2031.

Which product type is growing fastest within today's Polycarboxylate Ether space?

TPEG-based superplasticizers are forecast to expand at 3.26% CAGR during the forecast period (2026-2031) because they sustain slump above 120 minutes in hot climates.

Why are powder-grade Polycarboxylate Ethers gaining traction?

They reduce shipment volume by roughly 70% and avoid freeze-thaw risks, advantages valued in logistics-constrained regions.

How do green building codes influence Polycarboxylate Ether usage?

Codes mandating water-cement ratios below 0.40 or life-cycle carbon credits increasingly require high-range water reducers to maintain workability.

Page last updated on: