Medical Penlights Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

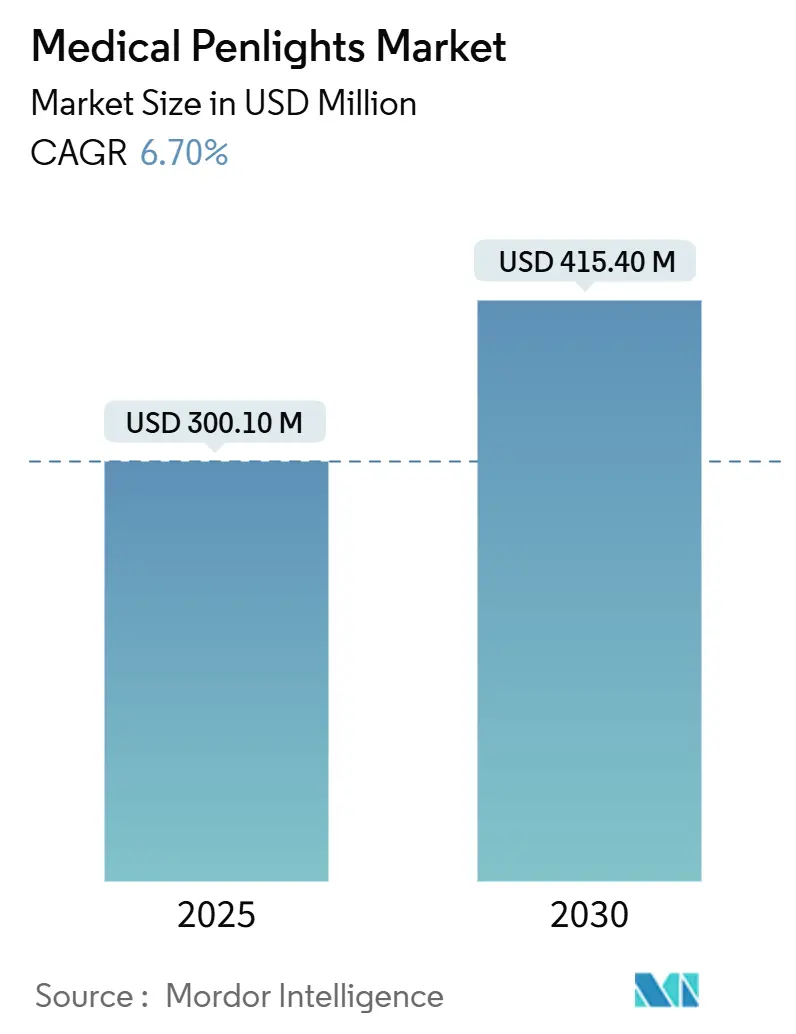

| Market Size (2025) | USD 300.10 Million |

| Market Size (2030) | USD 415.40 Million |

| Growth Rate (2025 - 2030) | 6.70% CAGR |

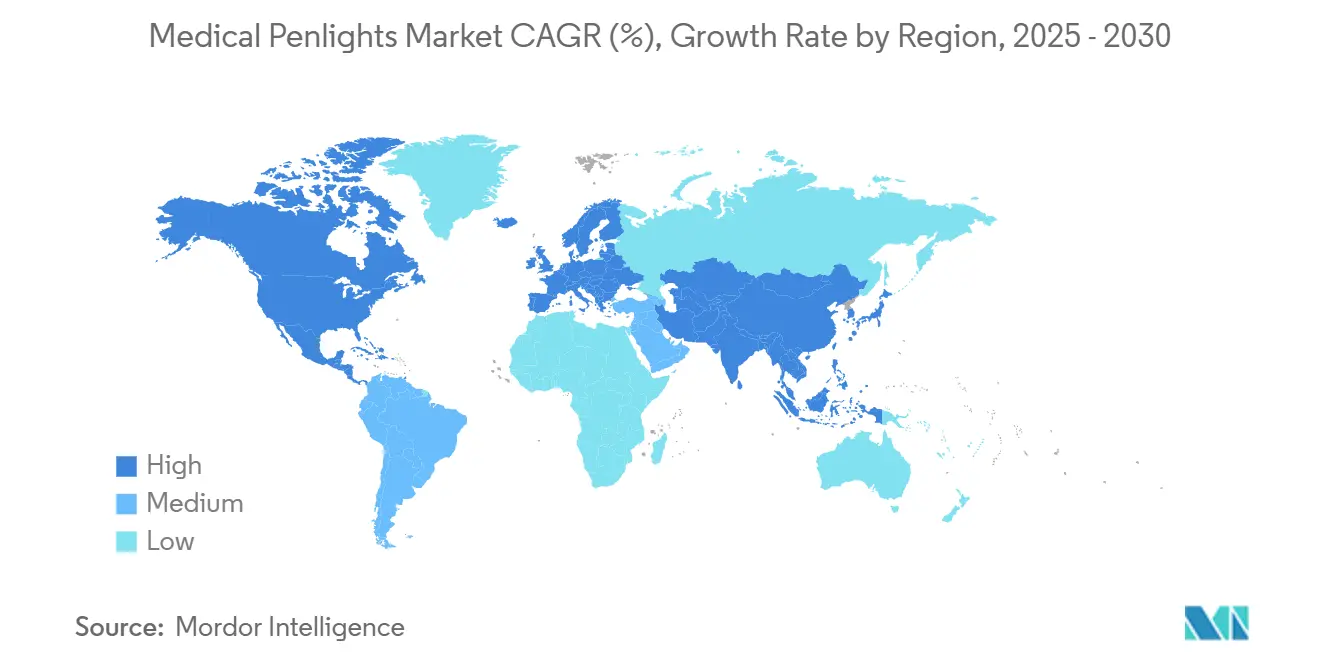

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Penlights Market Analysis by Mordor Intelligence

The medical penlights market size reached USD 300.1 million in 2025 and is forecast to climb to USD 415.4 million by 2030, advancing at a 6.7% CAGR. This growth reflects the rapid replacement of incandescent and halogen units with energy-efficient LEDs, the expanding use of disposable devices for infection control, and the broader role of portable diagnostics in digitally connected care settings. Continued hospital automation, the rise of vending-based distribution, and increasing clinician reliance on point-of-care tools position the medical penlights market as a key beneficiary of telemedicine and remote monitoring adoption. High-CRI LED technology is gaining favor because accurate color rendering directly affects dermatological outcomes, while supply-chain concerns around rare-earth phosphors prompt work on alternative materials. Regulatory initiatives—most notably IEC 62471 photobiological safety rules and the European Union’s battery-waste directive—are reshaping product design priorities toward safer light spectra and user-removable power modules.

Key Report Takeaways

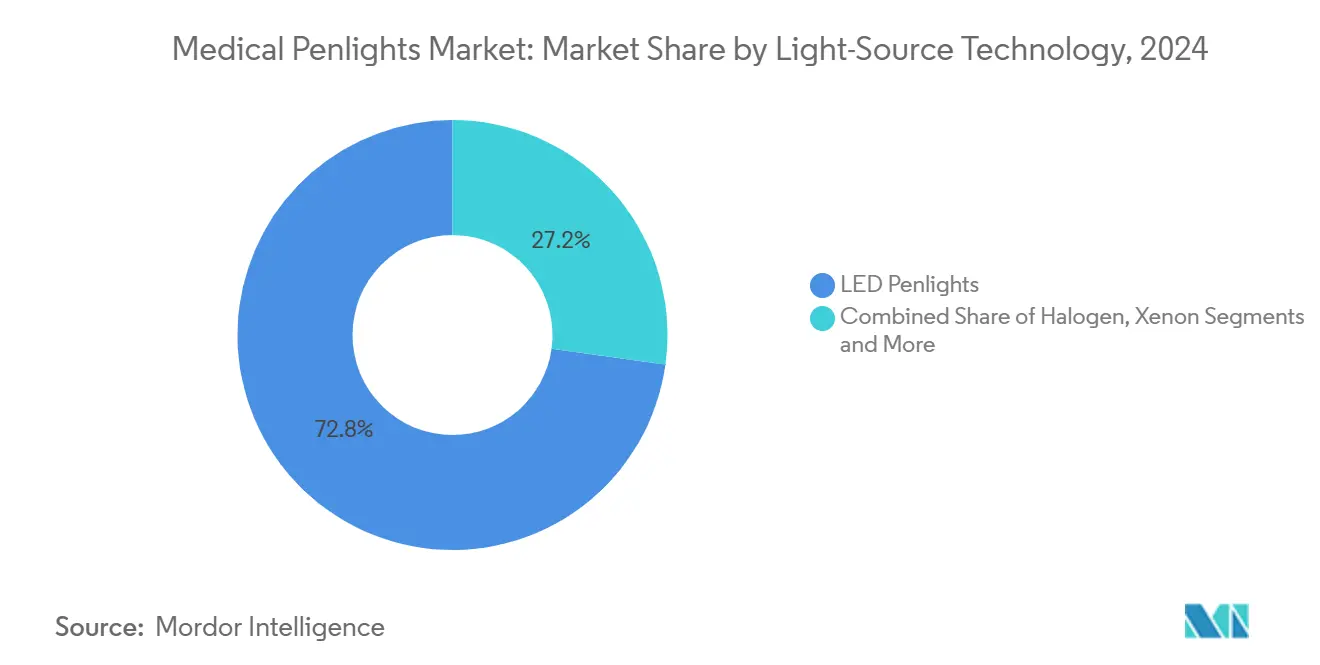

- By light-source technology, LED dominated with 72.8% revenue share in 2024; UV/Wood’s-Lamp is projected to expand at a 12.3% CAGR through 2030.

- By usage type, disposables captured 62.3% of the medical penlights market share in 2024, while reusable/rechargeables are projected to grow at 9.4% CAGR through 2030.

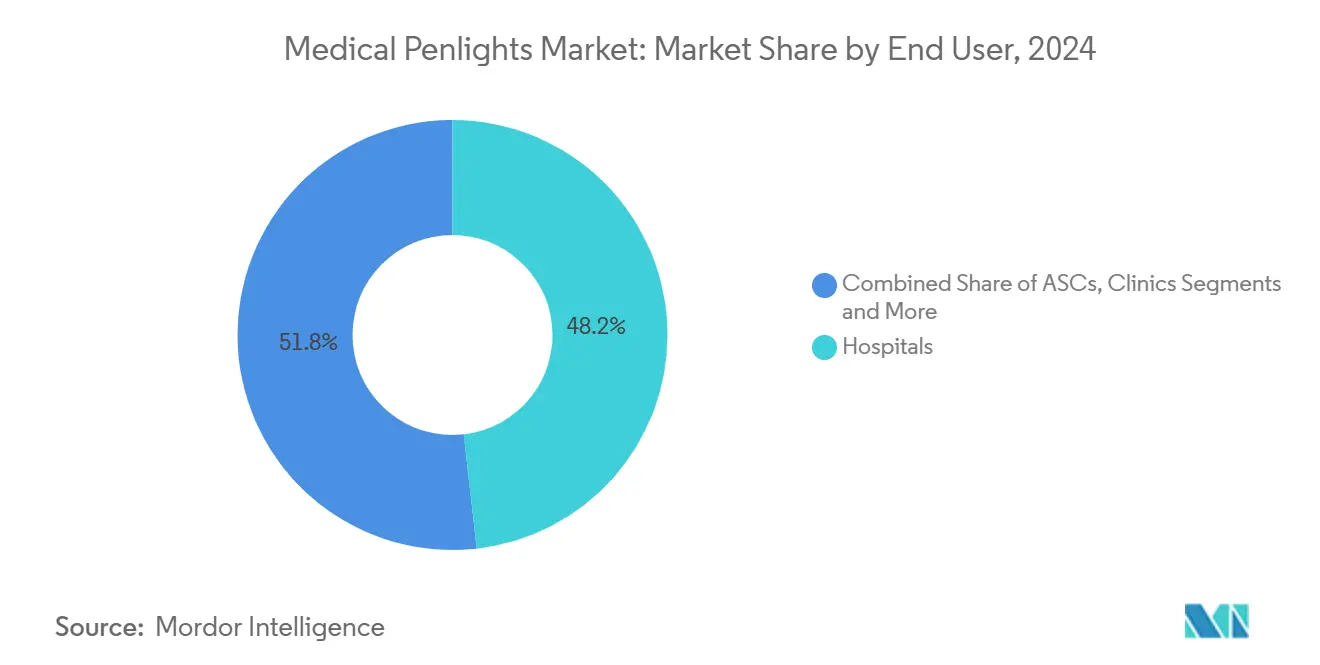

- By end-user, hospitals led with 48.2% revenue share in 2024; home healthcare and first responders are forecast to grow at a 10.8% CAGR to 2030.

- By geography, North America led with 36.2% revenue in 2024, but Asia Pacific is set to post the fastest 5.3% CAGR to 2030

Global Medical Penlights Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Numbers Of Medical Procedures Globally | +1.80% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| The Shift Toward Energy-Efficient, Longer-Lasting LED Lighting | +1.20% | Global, led by Europe & North America | Long term (≥ 4 years) |

| Expansion Of Nursing Services And Home Healthcare | +1.50% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Hospitals Are Adopting Disposable Penlights To Reduce Infection Risks | +0.90% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| High-CRI LEDs Enabling Tele-Dermatology | +0.70% | North America & Europe, selective APAC markets | Medium term (2-4 years) |

| On-Site Vending Contracts In Outpatient Clinics | +0.40% | North America, expanding to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Numbers of Medical Procedures Globally

Growing surgical and diagnostic volumes fuel sustained demand for portable illumination across hospitals, ambulatory centers, and home-care visits. Aging populations in developed countries, combined with healthcare infrastructure investments in emerging economies, elevate baseline usage of penlights for pupillary checks, throat exams, and dermatology triage. These devices also help mitigate nurse shortages by enabling rapid bedside assessments without bulky equipment. Disposable variants are favored where high patient throughput raises cross-contamination risks.[1]Centers for Disease Control and Prevention, “Best Practices for Single-Use (Disposable) Devices,” cdc.gov

The Shift Toward Energy-Efficient, Longer-Lasting LED Lighting

Hospitals pursuing carbon-footprint targets are phasing out incandescent and halogen units. LEDs consume 80% less power and last up to 25 times longer, reducing maintenance as well as hazardous waste. A U.S. federal medical center recorded USD 500,000 in ten-year energy savings after an LED retrofit.[2]Environmental Protection Agency, “Case Study: Energy Reduction through Lighting Improvement,” epa.gov Instant-on functionality and stable luminance throughout battery discharge give clinicians consistent light output in critical care.

Expansion of Nursing Services and Home Healthcare

Rising in-home treatment for chronic disease management increases reliance on compact diagnostics. Visiting nurses carry penlights for pupil and skin assessments in environments lacking controlled lighting. AARP notes that mobile medical services have expanded rapidly, supported by portable X-ray and specimen-collection tools.[3]AARP, “Advances in Mobile Medical Care Aid Older Adults, Caregivers,” aarp.org As advanced practice nurses gain prescribing authority, demand for high-quality handheld lighting grows in tandem.

Hospitals Are Adopting Disposable Penlights to Reduce Infection Risks

Single-use devices eliminate reprocessing steps and lower microbial bioburden compared with reusable tools. Studies confirm persistent contamination on portable equipment despite routine disinfection. Automated dispensing cabinets optimized for disposables have cut consumption 30%–40% while maintaining availability. Guidance from U.S. agencies encourages single-patient-use items to curb healthcare-associated infections.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheap Generic Flashlights | -0.80% | Global, particularly in price-sensitive markets | Short term (≤ 2 years) |

| Battery-Waste Regulations | -0.60% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| IEC 62471 Blue-Light Hazard Limits | -0.40% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) |

| Phosphor Supply Volatility For High-CRI LEDs | -0.50% | Global, concentrated impact on premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cheap Generic Flashlights

Low-cost consumer LEDs erode entry-level demand when hospitals or clinics buy on price alone. The performance gap narrows as mainstream LEDs improve, compelling medical brands to highlight infection-control certification, drop resistance, and verified color fidelity. Premium manufacturers counter by bundling training and compliance documentation that generic sellers cannot easily match.

Battery-Waste Regulations

The EU Batteries Regulation 2023/1542 requires user-removable cells and imposes collection targets that raise design complexity and compliance costs. U.S. universal waste rules also heighten disposal obligations. Disposable penlights with sealed batteries must be re-engineered, and some buyers may defer purchases until compliant options arrive, tempering short-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Light-Source Technology: LEDs Command the Upgrade Cycle

LED units held 72.8% revenue share in 2024, validating their status as the default choice for new purchases. UV/Wood’s-Lamp devices, though less common, are expanding at 12.3% CAGR on the back of rising dermatology caseloads and teledermoscopy adoption. The medical penlights market size for LED-based models is set to grow steadily as hospitals target 15% energy savings and specify high-CRI packages for color-critical applications. Xenon and halogen remain niche, serving clinicians who need a specific spectral signature or warmer tone, but represent a shrinking fraction of the medical penlights market. Manufacturers continue refining LED optics to deliver uniform beams without hot spots, a feature clinicians cite as essential during prolonged ear, nose, and throat exams. High-CRI improvements and rare-earth-free phosphors head the innovation agenda as suppliers pursue color fidelity without supply-chain risk.

Halogen’s decline nonetheless leaves replacement demand, especially where older otoscopes and laryngoscope handles use the same cell packs. LED retrofit bulbs sustain a small aftermarket segment. UV/Wood’s-Lamp models now integrate smartphone adapters so clinicians can capture images for teleconsultation, broadening utility beyond vitiligo screening to fungal and bacterial infection mapping.

By Usage Type: Disposable Dominance Reinforced by Infection Control

Disposable units accounted for 62.3% revenue share in 2024 as single-use culture shifts from surgical suites to general wards. Automated dispensing has accelerated adoption, with facilities reporting 30–40% supply reductions once individual-issue controls replaced open-bin stocking. Hospitals note that the medical penlights market share of disposables will widen as staff turnover makes reprocessing compliance harder to monitor. Environmental concerns drive interest in user-removable batteries and recyclable plastics to align disposables with new waste rules. Reusable/rechargeable designs endure where high annual purchase volumes raise sustainability alarms or where specialty departments require integrated brightness adjustments. Vendors position hybrid heads—reusable shells with disposable tips—as a middle path, but uptake depends on demonstrated cost-in-use advantages.

Disposable growth also dovetails with point-of-care expansion outside traditional wards, including ambulance kits and pop-up vaccination sites. Clinicians value guaranteed sterility and predictable brightness for up to 30 minutes of intermittent use. Battery-waste legislation, however, may temper growth unless suppliers offer compliant take-back programs or adopt zinc-air chemistries deemed less hazardous.

By End-User: Hospitals Lead, but Home Healthcare Sets the Pace

Hospitals retained 48.2% revenue share in 2024 through bulk procurement and protocol-driven standardization. Their purchasing committees favor penlights that meet IEC 62471 and include anti-microbial housings, driving premium features mainstream. Nonetheless, decentralized care models propel double-digit expansion among home-health providers and first responders, whose mobile kits demand compact, reliable illumination. The medical penlights market size generated by the home-care segment is projected to rise at 10.8% CAGR as aging populations elect for in-home recovery and monitoring. Ambulatory surgery centers increasingly install vending cabinets that link consumption data to electronic health records, further embedding penlights into supply loops. Veterinary practices, though outside human healthcare regulations, represent a parallel growth pocket, adopting LED units for small-animal exams where precision color rendering aids dermatologic diagnoses.

Geography Analysis

North America accounted for the largest regional share in 2024, underpinned by advanced hospital infrastructure, aggressive infection-control mandates, and early LED adoption. The U.S. Veterans Health Administration’s nationwide lighting retrofit programs exemplify institutional readiness to transition entire inventories to LEDs, while Canada’s provincial health authorities fund energy-efficiency upgrades that include hand-held diagnostic tools. Workforce shortages magnify reliance on portable gear, pushing the medical penlights market toward value-added features such as high-CRI beams and antimicrobial grips. Mexico’s medical tourism hubs also contribute, purchasing penlights tailored to dermatology packages.

Europe ranks second, propelled by sustainability policies that reward energy-efficient equipment. Upcoming battery-waste rules accelerate the shift to user-removable cells, opening a competitive window for suppliers that pre-certify designs. Germany, the United Kingdom, and the Nordics lead ordering volumes, while Southern European hospitals increasingly bundle LEDs within broader green-hospital overhauls. Telemedicine reimbursement expansions promote high-CRI lighting for remote dermatology consults, bolstering UV/Wood’s-Lamp uptake.

Asia Pacific is the fastest-growing territory. China and India channel healthcare stimulus into cost-effective diagnostics, favoring domestic LED makers who adapt consumer-grade production lines for medical compliance. Japan and South Korea anchor premium demand, specifying CRI ≥ 95 for dermatology applications and driving R&D partnerships aimed at rare-earth-free phosphors. The region’s aging demographics and rapid rollout of community clinics elevate penlight demand in both institutional and home-care settings. Southeast Asian governments promoting rural outreach programs purchase disposable penlights in bulk for vaccination drives, widening the customer base.

Competitive Landscape

The market remains moderately fragmented. Long-standing medical brands such as Welch Allyn, HEINE Optotechnik, and American Diagnostic Corporation leverage legacy distribution networks and regulatory dossiers to defend hospital contracts. LED specialists from the professional-flashlight sector—Nextorch Industries and Fenix Lighting—apply high-lumen, ruggedized designs to medical formats, intensifying feature competition. Differentiation now hinges on high-CRI output, antimicrobial surfaces, battery-waste compliance, and integration with automated dispensing software rather than simple brightness metrics.

High-CRI innovation creates entry barriers because rare-earth phosphors demand vertical integration or secure supply contracts. Companies exploring manganese-doped or perovskite phosphors seek to sidestep supply shocks while hitting CRI targets. Battery regulations spur R&D into tool-free cell replacement mechanisms and cradle-charge systems that log usage data. Automated dispensing interface modules and telemedicine-ready image capture rings represent new white-space opportunities.

Scale advantages encourage consolidation: mid-sized firms lacking global regulatory teams may partner or merge to share IEC 62471 testing costs. Meanwhile, hospital group purchasing organizations (GPOs) drive price negotiations that reward vendors combining LED expertise with infection-control credentials and waste-mitigation programs. Over the forecast horizon, M&A activity is expected among LED newcomers aiming to acquire medical sales channels and among incumbents seeking next-generation phosphor or battery technologies.

Medical Penlights Industry Leaders

Welch Allyn (Hillrom/Baxter)

American Diagnostic Corp (ADC)

HEINE Optotechnik

Rudolf Riester GmbH

MDF Instruments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Research published in Cutis highlighted the growing use of smartphone-based UV light applications. These tools offer an affordable alternative to traditional Wood's lamps, providing portable diagnostic capabilities similar to UV penlights.

- September 2024: Nextorch has launched two medical penlight models designed with healthcare professionals in mind. The Dr. K3S Medical Penlight, priced at USD 11.99 and covered by a lifetime warranty, features dual light modes (yellow and white) and a high CRI of 90 for accurate color representation. The premium Dr. K3 Pro model, available for USD 49.99, includes dual light sources (3000K yellow and 5500K white), an IPX7 waterproof rating, and a built-in 320 mAh lithium battery.

- August 2024: ADC has introduced new pricing for its medical penlight lineup. The Adlite Pro Penlight is now available for USD 20.62. Meanwhile, the Metalite Reusable Penlight is on clearance for USD 3.19, which could suggest efforts to manage inventory or refresh the product line.

Global Medical Penlights Market Report Scope

| LED Penlights |

| Halogen Penlights |

| Xenon Penlights |

| UV / Wood's-Lamp Penlights |

| Others (Fiber-optic, etc.) |

| Disposable |

| Reusable / Rechargeable |

| Hybrid (Replaceable Head) |

| Hospitals |

| Ambulatory Surgical Centres |

| Clinics & Physician Offices |

| Home Healthcare & First-Responders |

| Veterinary Practices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Light-Source Technology | LED Penlights | |

| Halogen Penlights | ||

| Xenon Penlights | ||

| UV / Wood's-Lamp Penlights | ||

| Others (Fiber-optic, etc.) | ||

| By Usage Type | Disposable | |

| Reusable / Rechargeable | ||

| Hybrid (Replaceable Head) | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Clinics & Physician Offices | ||

| Home Healthcare & First-Responders | ||

| Veterinary Practices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the global medical penlights market?

The medical penlights market size reached USD 300.1 million in 2025.

How fast is the market expected to grow over the next five years?

The market is forecast to increase at a 6.7% CAGR, reaching USD 415.4 million by 2030.

Which light-source segment holds the largest share?

LED penlights commanded 72.8% revenue share in 2024.

Why are disposable penlights gaining traction in hospitals?

Disposable units eliminate reprocessing, reduce cross-contamination risk, and align with infection-control protocols.

What regional market is expanding the quickest?

Asia Pacific is the fastest-growing region due to healthcare infrastructure investments and rising procedure volumes.

How will EU battery regulations influence product design?

Manufacturers must provide user-removable batteries and implement take-back programs, driving redesigns of disposable and rechargeable models.

Page last updated on: