Refractive Surgery Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

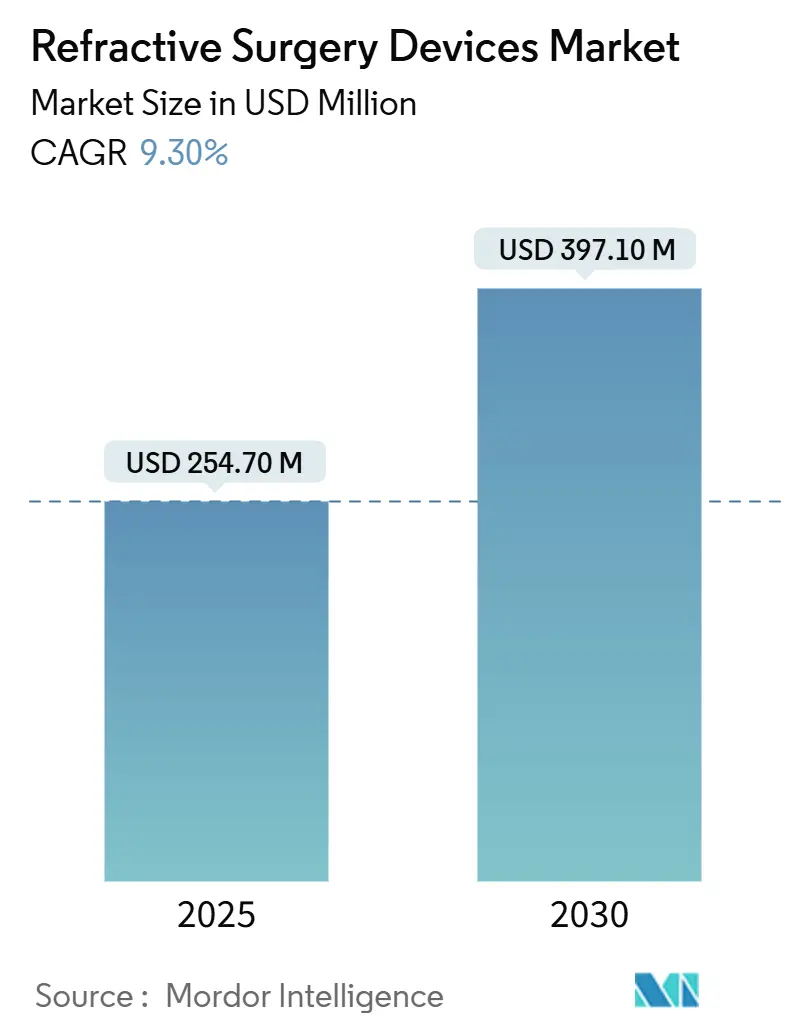

| Market Size (2025) | USD 254.70 Million |

| Market Size (2030) | USD 397.10 Million |

| Growth Rate (2025 - 2030) | 9.30% CAGR |

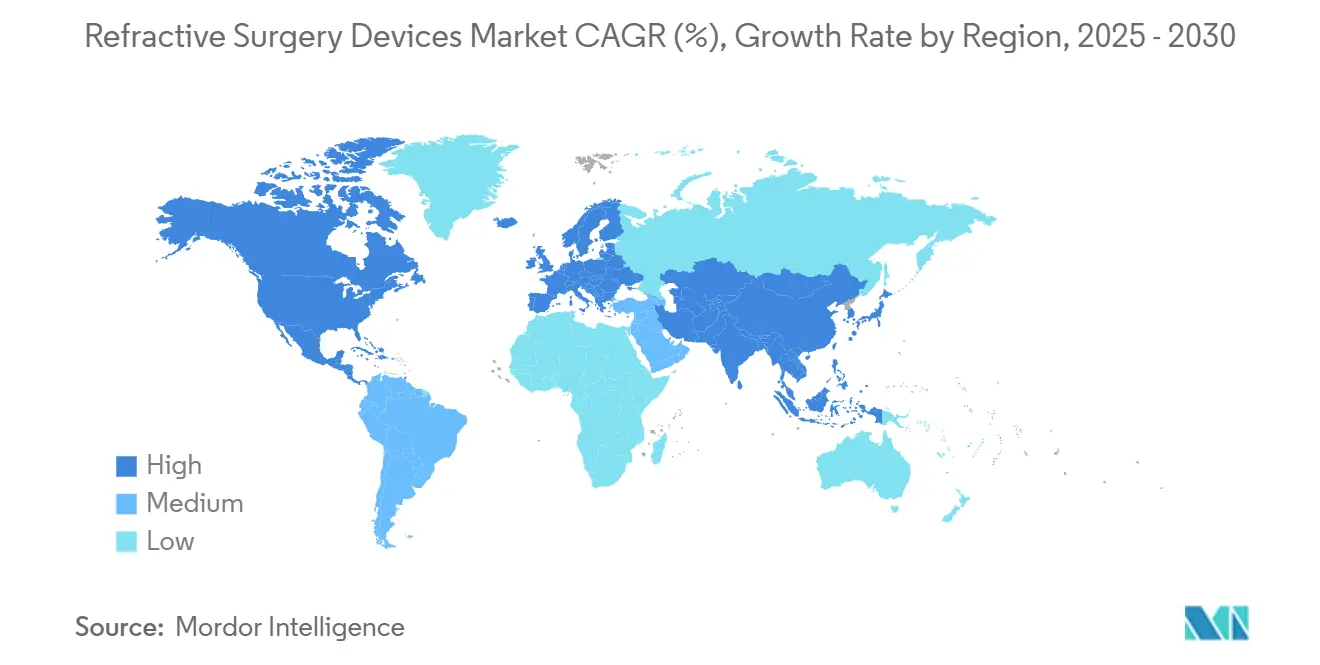

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refractive Surgery Devices Market Analysis by Mordor Intelligence

The refractive surgery devices market size stood at USD 254.7 million in 2025 and is forecast to reach USD 397.0 million by 2030, advancing at a 9.30% CAGR over the period. Growing demand for spectacle-free vision, rapid adoption of femtosecond platforms, and broader insurance coverage in Asia Pacific sustain double-digit procedure growth. Artificial intelligence now guides patient selection and surgical planning, lifting conversion rates in high-volume centers. Military and first-responder programs that mandate unaided visual acuity further expand the addressable base. Strategic acquisitions, most notably Alcon’s USD 1.5 billion purchase of STAAR Surgical, signal rising competitive intensity and a shift toward platform ecosystems that bundle hardware, software, and consumables. At the same time, sustainability scrutiny of energy-intensive lasers and persistent dry-eye concerns influence capital purchasing decisions and spur innovation in lower-fluence technologies and post-operative care protocols.

Key Report Takeaways

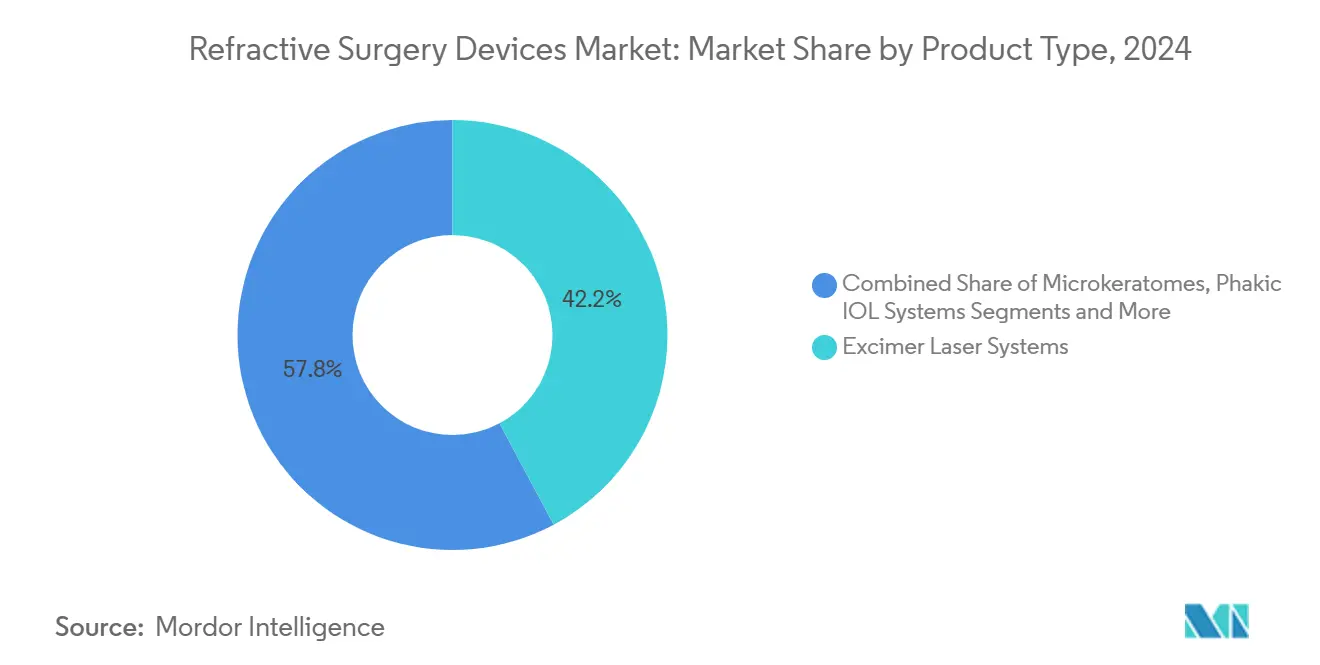

- By product type, excimer laser systems had a 42.2% market share in refractive surgery devices in 2024, while SMILE/RCLE platforms are projected to expand at an 11.8% CAGR through 2030.

- By refractive error, myopia correction commanded a 62.7% share of the refractive surgery devices market size in 2024; presbyopia treatments are advancing at a 9.5% CAGR to 2030.

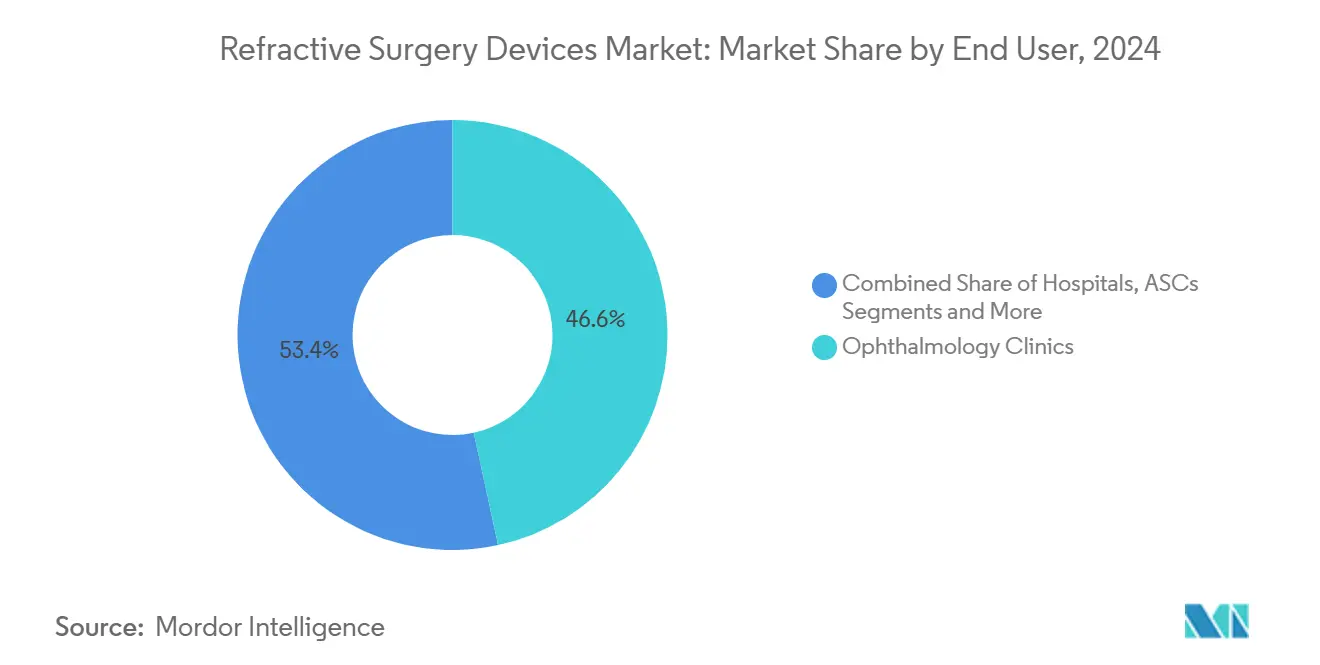

- By end user, ophthalmology clinics held 46.6% revenue share in 2024, whereas ambulatory surgery centers are growing at an 8.7% CAGR during the forecast horizon.

- By geography, North America led with 34.5% revenue in 2024, but Asia Pacific is set to post the fastest 7.9% CAGR to 2030.

Global Refractive Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Myopia & Presbyopia | +2.10% | Global, concentrated in Asia Pacific | Long term (≥ 4 years) |

| Shift Toward Minimally-Invasive Femtosecond Platforms | +1.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expanding Insurance Coverage For Elective Refractive Surgery (Asia) | +1.40% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| AI-Driven Pre-Operative Screening Boosting Conversion Rates | +1.20% | Global, early adoption in North America | Short term (≤ 2 years) |

| Military & First-Responder Adoption Of Spectacle-Free Standards | +1.00% | North America, expanding to allied nations | Medium term (2-4 years) |

| 3-D Printed, Patient-Specific Ablation Profiles | +0.80% | North America & EU, R&D phase globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Myopia & Presbyopia

World Health Organization projections show 4.76 billion people may be myopic by 2050, while presbyopia cases could reach 2.1 billion by 2030.[1]Jing Xie et al., “Global Trends in Refractive Disorders,” Frontiers in Public Health, frontiersin.orgEast Asia already records 51.6% myopia prevalence, intensifying demand for surgical correction. Younger professionals in China cite career requirements in 48.9% of LASIK decisions, underscoring socioeconomic drivers. The expanding middle class across Asia Pacific lifts procedure affordability, and insurers in Japan, South Korea, and Singapore now reimburse partial costs, stimulating volume growth. Together, these trends underpin sustained device utilization across age cohorts and geographies.

Shift Toward Minimally Invasive Femtosecond Platforms

SMILE delivers faster recovery and greater biomechanical stability than traditional LASIK, with 92% of patients achieving 6/9.5 uncorrected visual acuity.[2]European Society of Cataract and Refractive Surgeons, “Expanding the Limits of KLEx,” escrs.org FDA clearance of the ZEISS VisuMax 800 in 2024 cut lenticule creation time below 10 seconds and added advanced centration aids, enhancing throughput. The U.S. Air Force has adopted femtosecond LASIK as a preferred option, validating safety and performance in demanding environments. Eye-tracking at 1,740 Hz on the Bausch + Lomb TENEO platform maintains accuracy despite saccadic movements. Collectively, these features shift capital allocation toward femtosecond systems and accelerate the replacement of older excimer units.

Expanding Insurance Coverage for Elective Refractive Surgery

Public insurers in South Korea now reimburse up to 40% of laser procedures, and Chinese commercial plans cover disposables in tier-2 cities, lowering out-of-pocket costs. Insurers report 17% year-on-year growth in claims linked to vision-correction benefits, reflecting policy traction. Broader coverage eases price sensitivity, fosters procedural upselling to premium lenses, and supports the refractive surgery devices market in traditionally cash-pay economies. Manufacturers respond with flexible financing schemes for physicians to accelerate platform adoption.

AI-Driven Pre-Operative Screening Boosting Conversion Rates

Algorithms such as the Tomographic/Biomechanical Index raise sensitivity for ectasia detection, reducing unsuitable candidates by 28%. AEYE Health’s autonomous system delivers 92-93% sensitivity in diabetic retinopathy screening, setting a regulatory precedent for AI diagnostics. Deep-learning models now predict implantable collamer lens vault with 94% accuracy, optimizing sizing decisions. Clinics integrating AI show 12% higher booking-to-procedure ratios within 12 months. These gains improve profitability while reducing post-operative complications, reinforcing surgeon confidence in advanced platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Procedure Costs | -1.90% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Post-Operative Dry-Eye & Ectasia Concerns | -1.30% | Global, regulatory focus in North America & EU | Medium term (2-4 years) |

| Limited Surgeon Capacity In Fast-Growing Markets | -0.90% | APAC core, MEA, South America | Medium term (2-4 years) |

| Sustainability Scrutiny Of High-Energy Laser Platforms | -0.70% | EU leading, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Procedure Costs

Acquiring a dual-laser suite costs USD 400,000–500,000 and per-case fees of USD 300-400, pressing small clinics’ margins. The 2025 Medicare physician fee schedule proposes a 3% cut to cataract reimbursements, compounding financial stress.[3]American Society of Cataract and Refractive Surgery, “2025 Medicare Physician Fee Schedule Proposed Rule,” ascrs.org Charge-to-payment ratios in ophthalmology widened to 3.03 in 2020, exposing uninsured patients to high out-of-pocket charges. Practices pivot toward ambulatory surgery centers and premium packages to offset declining reimbursement, yet access remains constrained in low-income regions.

Post-Operative Dry-Eye & Ectasia Concerns

Systematic reviews link tear-film instability to flap creation, highlighting the need for gentler interfaces. Corneal Biomechanical Index algorithms improve ectasia risk prediction, but residual uncertainty deters some candidates. Mitomycin C at 0.02% lowers corneal haze incidence to 6.5% versus 15.2% in controls, yet long-term safety monitoring is ongoing. Device makers now bundle ocular-surface analytics to reassure surgeons and patients, although regulatory scrutiny persists, particularly in the EU.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: SMILE Platforms Accelerate Replacement Cycle

Excimer systems captured 42.2% of 2024 revenue, equating to USD 107.6 million of the refractive surgery devices market size, but their share is eroding as SMILE/RCLE units post an 11.8% CAGR to 2030. Surgeons favor single-incision techniques that preserve corneal biomechanics and shorten recovery. Femtosecond platforms command premium pricing yet deliver higher throughput, improving return on investment and driving upgrades among early LASIK adopters. Microkeratome sales continue to wane as blade-free flap creation becomes standard. Device vendors differentiate via faster eye tracking, smaller footprints, and integrated analytics to defend margins amid intensifying competition.

SMILE adoption influences consumable sales by reducing need for single-use blades, prompting manufacturers to emphasize software subscriptions and service contracts. The refractive surgery devices market benefits from the recurring revenue, yet clinics scrutinize total cost of ownership as reimbursements tighten. Phakic IOLs revive interest where corneal thickness limits laser eligibility, and Light Adjustable Lens technology extends customization into the post-operative period. These adjuncts broaden manufacturer portfolios, positioning them to capture share across diverse patient profiles.

By Refractive Error: Presbyopia Emerges as High-Growth Niche

Myopia procedures represented 62.7% of the 2024 refractive surgery devices market share, whereas presbyopia treatments are expanding at 9.5% per year as global populations age. Pharmacologic options such as pilocarpine drops serve as entry points, yet surgical correction retains appeal for durable outcomes. PRESBYOND and multifocal IOLs achieve 94% patient satisfaction among pilots and surgeons who require high-contrast vision. Hyperopia and astigmatism cases increasingly leverage topography-guided algorithms, widening indications for laser correction.

Emerging blended-vision protocols support the refractive surgery devices market. Clinics segment marketing campaigns by age bracket, focusing on convenience narratives for younger myopes and productivity themes for presbyopes. Vendors thus tailor educational content to distinct cohorts, emphasizing the evolving precision and safety profile of modern platforms.

By End User: Ambulatory Surgery Centers Narrow Gap with Clinics

Ophthalmology clinics accounted for 46.6% of 2024 revenue, but ambulatory surgery centers are gaining ground with an 8.7% CAGR. ASC reimbursement climbed 2% in 2025 to USD 1,329 for cataract cases, incentivizing migration of refractive volumes. Surgeons value ASC scheduling flexibility and lower overhead, while patients appreciate streamlined check-in and recovery. Private-equity-backed practice management groups accelerate ASC expansion, although higher interest rates slow deal flow.

Hospitals respond by converting under-utilized outpatient space into eye-care suites, yet regulatory reporting burdens limit agility. Academic centers retain a niche for complex cases and technology validation trials. The refractive surgery devices market continues adjusting as capital allocation shifts toward settings with favorable payer mixes and throughput efficiencies.

Geography Analysis

North America generated 34.5% of 2024 revenue on the back of early adoption, strong disposable incomes, and aggressive marketing by leading chains. Premium procedure penetration exceeds 70%, and military volume provides a stable baseline demand. Public debate over environmental impact has sparked interest in lower-fluence systems, pushing vendors to highlight energy-efficiency metrics during tenders.

Asia Pacific records the fastest 7.9% CAGR, fueled by middle-class expansion, surging digital-device usage, and increasing myopia prevalence. China’s NMPA nod for the VisuMax 800 unlocks pent-up demand, and Carl Zeiss Meditec reports double-digit consumable growth in the region. Government pilot programs in Singapore subsidize adolescent myopia-control measures, indirectly nudging families toward surgical solutions for adults.

Europe demonstrates steady replacement demand as clinics swap aging excimer platforms for femtosecond units. The EU Medical Device Regulation drives compliance investments that favor multinationals with robust quality systems. Emerging markets in MEA and South America lag in volume but represent strategic expansion arenas; manufacturers partner with NGOs for surgeon training and donate refurbished systems, seeding future commercial sales.

Competitive Landscape

The top five players capture an estimated 72% of global revenue, indicating moderate concentration. Alcon’s USD 1.5 billion buyout of STAAR Surgical and USD 356 million acquisition of LENSAR reposition the company with a cradle-to-cataract portfolio and strengthens its presence in femtosecond lasers. Carl Zeiss Meditec leverages SMILE intellectual property and an installed base of 2,600 VisuMax systems to defend share. Johnson & Johnson deepened its digital ecosystem through investment in TECLens, targeting non-incisional correction modalities.

Bausch + Lomb re-entered the capital-equipment race with the TENEO excimer platform, seeking to convert legacy Technolas users. Mid-tier entrants focus on niche innovations such as servo-controlled fluidics or UV-adjustable lenses. Hardware differentiation alone is no longer sufficient; vendors bundle AI modules, cloud analytics, and training to build switching costs. Sustainability credentials, including power consumption and recyclable packaging, now feature prominently in tender evaluations, especially in the EU.

Regional challengers emerge in India and China, offering cost-optimized femtosecond systems at 20-30% lower price points. Yet limited global service networks and sparse regulatory filings constrain export ambitions. Overall, the competitive narrative centers on platform breadth, software sophistication, and post-sale service quality rather than single-device supremacy.

Refractive Surgery Devices Industry Leaders

Alcon

Johnson & Johnson Vision

Carl Zeiss Meditec AG |

Bausch + Lomb

SCHWIND eye-tech-solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcon agreed to acquire LENSAR for USD 356 million, expanding its femtosecond laser cataract portfolio.

- February 2025: Alcon introduced Clareon PanOptix Pro trifocal IOL, offering 94% light utilization and reduced scatter.

- October 2024: FDA approved Bausch + Lomb enVista Envy IOLs featuring ActivSync optic.

Global Refractive Surgery Devices Market Report Scope

| Excimer Laser Systems |

| Femtosecond Laser Systems |

| SMILE/RCLE Platforms |

| Microkeratomes |

| Phakic IOL Systems |

| Myopia |

| Hyperopia |

| Astigmatism |

| Presbyopia |

| Hospitals |

| Ophthalmology Clinics |

| Ambulatory Surgery Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Excimer Laser Systems | |

| Femtosecond Laser Systems | ||

| SMILE/RCLE Platforms | ||

| Microkeratomes | ||

| Phakic IOL Systems | ||

| By Refractive Error | Myopia | |

| Hyperopia | ||

| Astigmatism | ||

| Presbyopia | ||

| By End User | Hospitals | |

| Ophthalmology Clinics | ||

| Ambulatory Surgery Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the refractive surgery devices market in 2025?

The refractive surgery devices market size reached USD 254.7 million in 2025.

What is the expected growth rate through 2030?

The market is projected to grow at a 9.30% CAGR, reaching USD 397.0 million by 2030.

Which product segment is expanding the fastest?

SMILE/RCLE femtosecond platforms are forecast to post an 11.8% CAGR through 2030.

Why is Asia Pacific considered the most attractive region?

Rising middle-class incomes, a high myopia burden, and broader insurance coverage drive a 7.9% CAGR in Asia Pacific.

How are ambulatory surgery centers affecting device demand?

ASCs grow at an 8.7% CAGR as surgeons shift cases to lower-cost, high-throughput settings, boosting capital equipment turnover.

What role does AI play in refractive surgery today?

AI-based pre-operative screening improves risk assessment and lifts booking-to-procedure conversion rates by about 12%.

Page last updated on: