Penile Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

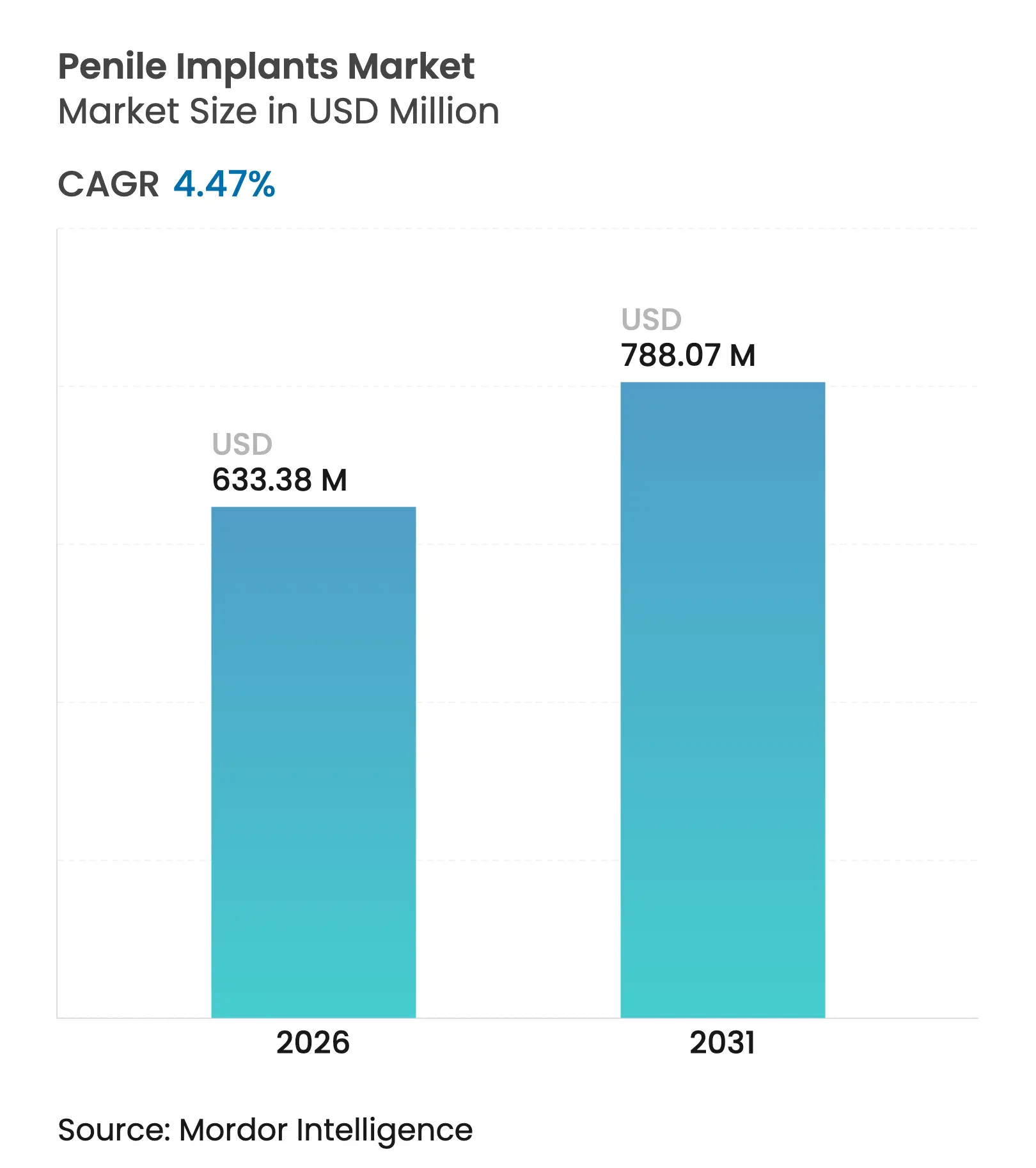

| Market Size (2026) | USD 633.38 Million |

| Market Size (2031) | USD 788.07 Million |

| Growth Rate (2026 - 2031) | 4.47 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Penile Implants Market Analysis by Mordor Intelligence

The Penile Implants Market size was valued at USD 606.29 million in 2025 and estimated to grow from USD 633.38 million in 2026 to reach USD 788.07 million by 2031, at a CAGR of 4.47% during the forecast period (2026-2031). Growing clinical acceptance of surgical solutions for erectile dysfunction, the shift to outpatient settings, and insurer support for value-based care are accelerating demand in the penile implant market. Innovation in antibiotic-coated cylinders, higher post-prostatectomy procedure volumes, and expanding specialist men’s-health clinics in Asia-Pacific further reinforce growth. At the same time, manufacturers benefit from quality-of-life metrics that favor device implantation over recurrent pharmacotherapy.

Key Report Takeaways

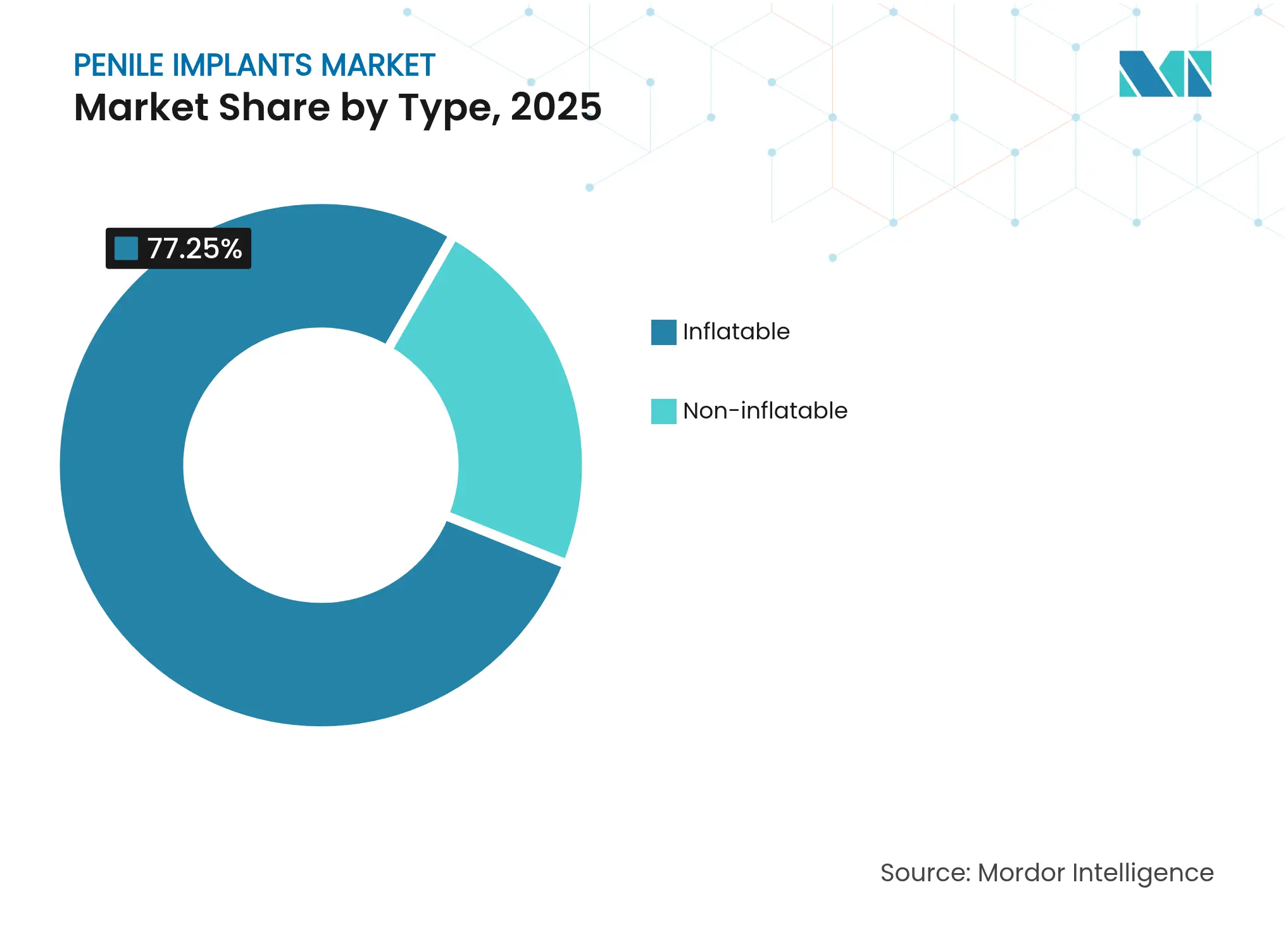

- By type, inflatable devices held 77.25% of penile implant market share in 2025, while antibiotic-coated inflatable systems are projected to expand at a 5.02% CAGR through 2031.

- By material, silicone components accounted for 62.35% of the penile implant market size in 2025; silicone-polymer hybrids are set to grow at 5.44% CAGR to 2031.

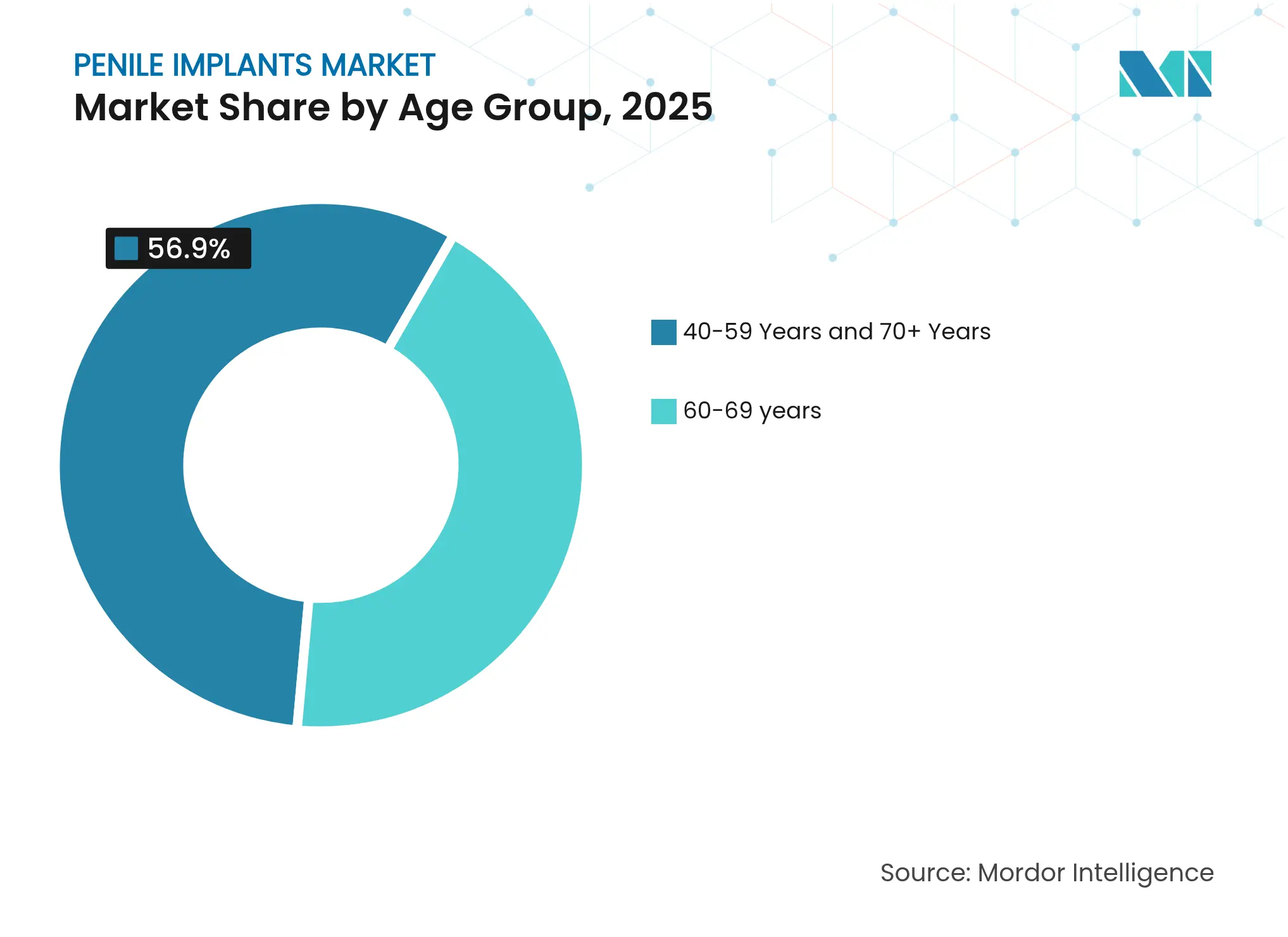

- By age group, patients aged 60-69 commanded 43.10% of penile implant market share in 2025, whereas the 40-59 segment records the fastest 5.93% CAGR.

- By patient indication, post-prostatectomy erectile dysfunction represented 37.20% of penile implant market size in 2025; transgender surgery leads growth at 6.48% CAGR.

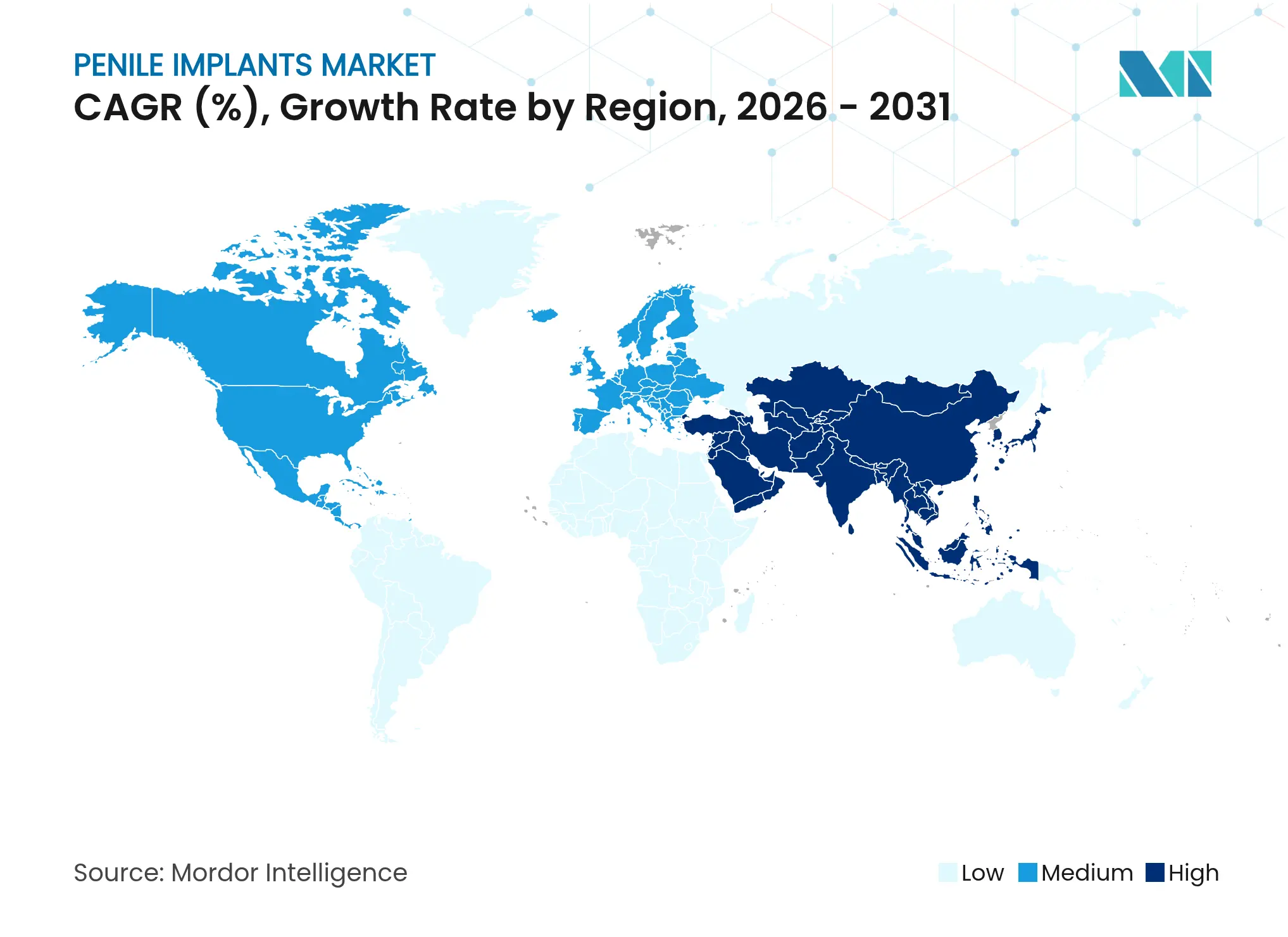

- By geography, North America contributed 37.40% of penile implant market revenue in 2025, while Asia-Pacific is rising at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Penile Implants Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in post-prostatectomy ED cases Surge in post-prostatectomy ED cases | +1.2% | Global, concentrated in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, concentrated in North America & EU | Impact Timeline:Medium term (2-4 years) |

Rising preference for outpatient implant surgery Rising preference for outpatient implant surgery | +0.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) | |||

Technological shift to antibiotic-coated cylinders Technological shift to antibiotic-coated cylinders | +0.6% | Global | Medium term (2-4 years) | |||

Growth of value-based urology reimbursement models Growth of value-based urology reimbursement models | +0.4% | North America & EU | Long term (≥ 4 years) | |||

Rapid expansion of specialized men's-health clinics in Asia-Pacific Rapid expansion of specialized men's-health clinics in Asia-Pacific | +0.7% | APAC core, spill-over to MEA | Medium term (2-4 years) | |||

Emerging demand from transgender masculinisation surgery Emerging demand from transgender masculinisation surgery | +0.3% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Post-Prostatectomy Erectile Dysfunction Cases

Radical prostatectomy volumes continue to rise, creating a steady stream of candidates for implantation. Current clinical registries show annual U.S. implant procedure counts of 20,000-25,000, reflecting strong physician confidence and patient satisfaction levels that exceed 85% across varying pre-operative erectile function statuses. High post-surgical success rates give manufacturers room to position premium inflatable systems. Device configurations tailored to altered pelvic anatomy are gaining uptake, and hospitals promoting survivorship programs increasingly add implants to standard post-cancer care pathways

Rising Preference for Outpatient Implant Surgery

Urology-focused ambulatory surgical centers now perform 90% of penile prosthesis placements that previously required inpatient stays. Same-day discharge reduces facility costs and speeds recovery[1]AORN Citation: Source: Joe Paone, "A Look Inside Urology ASCs," Outpatient Surgery Magazine, aorn.org . Three-year implant survival of 94% and five-year survival of 92.5% support ongoing migration to outpatient care. Multimodal analgesia protocols enable early ambulation, while streamlined infrapubic techniques shorten operating time. Outpatient-friendly device kits packaged for ASC workflows give suppliers a competitive edge within the penile implant market.

Technological Shift to Antibiotic-Coated Cylinders

Antibiotic coatings have cut infection incidence for initial implantations to 1-3%, down from historic 3-5% levels. Hydrophilic surfaces that bind and rebind antibiotics maintain antimicrobial activity during revision surgery, minimizing reoperation risk. Diabetic and immunocompromised patients benefit disproportionately, widening the candidate pool and boosting the penile implant market. Manufacturers continue to refine coating formulations and automated application processes as differentiators.

Growth of Value-Based Reimbursement Models

The 2025 CMS Physician Fee Schedule imposes a 2.83% conversion-factor cut, pushing providers toward high-outcome, low-revision solutions. Medicare beneficiaries spend roughly USD 1,600 out of pocket on inflatable prostheses per year, a cost advantage over recurrent injectable therapies. Device makers supplying robust outcome data see faster inclusion on hospital value-analysis committees. Bundled-payment pilots in large urology groups signal further payer interest in linking reimbursement to sustained device performance

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High revision cost & limited insurance coverage High revision cost & limited insurance coverage | -0.9% | Global, acute in developing markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Global, acute in developing markets | Impact Timeline:Medium term (2-4 years) |

Persistent mechanical failure rates of inflatable systems Persistent mechanical failure rates of inflatable systems | -0.7% | Global | Short term (≤ 2 years) | |||

Urologist supply shortage in North America Urologist supply shortage in North America | -0.6% | North America, emerging in EU | Medium term (2-4 years) | |||

Cultural stigma limiting procedure uptake in MEA Cultural stigma limiting procedure uptake in MEA | -0.4% | Middle East & Africa | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Revision Cost & Limited Insurance Coverage

Revision is required in roughly 12.1% of inflatable implant recipients, most often due to infection. In the United States, a primary procedure runs USD 15,000-40,000, and revisions attract additional charges that are not always reimbursed in full. Developing markets face steeper affordability barriers when public insurance is minimal. Budget-minded purchasers favor malleable systems despite lower satisfaction, challenging suppliers to produce cost-effective inflatable alternatives.

Urologist Supply Shortage in North America

More than 60% of U.S. counties lack a practicing urologist, and residency bottlenecks leave 23% of qualified applicants unmatched[2]LUGPA Citation: Source: LUGPA Policy Team, "Addressing the Physician and Urology Workforce Shortage," LUGPA Policy Brief, lugpa.org. Rural patients travel long distances for care, delaying consultations and reducing elective surgery throughput. Physician-extender models and telemedicine screening aim to mitigate access gaps, yet procedure capacity constraints temper the otherwise positive outlook for the penile implant market.

Segment Analysis

By Type: Inflatable Devices Drive Innovation

Inflatable implants commanded 77.25% of penile implant market revenue in 2025, underscoring their role as the procedural standard. Premium three-piece models deliver natural flaccidity and superior concealability, yielding 95% post-operative satisfaction for sexual activity. The antibiotic-coated subsegment is set to outpace overall segment growth at a 5.02% CAGR, strengthening the penile implant market size for advanced systems. Developments such as Boston Scientific’s TENACIO pump, cleared in 2023 and broadly launched in 2024, improve inflation control for patients with limited dexterity, supporting wider adoption.

Non-inflatable malleable devices retain a niche among cost-sensitive health systems and users prioritizing procedural simplicity. Boston Scientific’s Tactra, cleared in April 2025, combines a nitinol core with dual-layer silicone for easier modeling and improved comfort. Rigicon’s Infla10 platform pioneers Dynamic Inflatable Penile Prosthesis technology with enhanced pump ergonomics. Competitive differentiation now centers on simplified surgical steps, cylinder durability, and automated pressure regulation, keeping innovation brisk within the penile implant market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Silicone Dominance with Hybrid Innovation

Silicone captured 62.35% of penile implant market share in 2025, reflecting decades of biocompatibility evidence and stable manufacturing know-how. New hydrophilic silicone coatings bind antibiotics effectively, sustaining antimicrobial action during revision and supporting the penile implant market size for coated cylinders. Silicone-polymer hybrids post a 5.44% CAGR through 2031 as formulators blend properties to balance flexibility and structural strength.

Metallic elements such as nitinol enhance malleable shaft memory and inflatable pump performance integrity. Dual-layer silicone-nitinol designs like Tactra showcase material convergence that addresses physician handling and patient esthetics. R&D pipelines are evaluating ceramic-polymer barrier layers carrying antibiotic loads, a sign of relentless material-science focus within the penile implant market.

By Age Group: Younger Demographics Accelerate Adoption

Patients aged 60-69 held 43.10% of penile implant market revenue in 2025, consistent with erectile dysfunction’s traditional epidemiology. Yet the 40-59 group is advancing at 5.93% CAGR on improving societal openness and earlier treatment decisions. Physicians report frequent regret among patients who postpone surgery, a narrative now influencing younger men toward proactive implantation. The penile implant market size for middle-aged cohorts thus rises in tandem with wellness messaging and evolving masculinity norms.

The 70+ bracket continues to drive stable demand owing to safer anesthesia and minimally invasive methods that accommodate comorbidities. Cardiometabolic risk screening has become routine, enabling geriatric candidates to undergo implantation with confidence. Device makers are tailoring pump mechanisms for reduced hand strength, ensuring inclusivity across age profiles and reinforcing broad appeal in the penile implant market.

Note: Segment shares of all individual segments available upon report purchase

By Patient Indication: Post-Prostatectomy Leads, Transgender Segment Emerges**

Post-prostatectomy erectile dysfunction accounted for 37.20% of penile implant market size in 2025 as cancer survivorship climbs. Devices engineered for altered pelvic anatomy and enhanced rigidity profiles meet specific needs of this group. Neurogenic and diabetes-related dysfunction form sizeable secondary pools, with diabetic patient infection mitigation driving coated-cylinder uptake.

Gender-affirming surgery represents the fastest-growing indication at 6.48% CAGR. Specialized prostheses for neophallus implantation face higher complication rates but deliver meaningful quality-of-life gains, stimulating R&D. Manufacturers offering customizable cylinder lengths and anchoring solutions are carving share in this nascent pocket of the penile implant market

Geography Analysis

North America remains the largest regional contributor, capturing 37.40% of 2025 revenue. The outpatient shift across urology ambulatory surgical centers reduced costs and shortened recovery, supporting consistent procedure growth. Workforce shortages temper expansion, yet telehealth pre-assessment and traveling surgeon programs partially offset capacity gaps. Insurer scrutiny of revision rates incentivizes provider–manufacturer cooperation on quality metrics, sustaining positive momentum for the penile implant market.

Europe records healthy procedure counts as publicly funded health systems emphasize evidence-based interventions. Unified treatment guidelines from the European Association of Urology streamline patient pathways, while bundled payments nudge hospitals toward coated-cylinder adoption. Cross-border centers of excellence in Germany attract medical tourists, bolstering the penile implant market even in mature economies.

Asia-Pacific outpaces all regions at 7.08% CAGR, buoyed by rising disposable incomes and dedicated men’s clinics. National urology societies promote standardized surgical curricula, raising confidence among younger patient cohorts. Japanese and Australian insurers have begun pilot reimbursement for select inflatable systems, adding financial clarity. Cultural stigma persists in parts of South Asia and the Gulf, but outreach by device makers and local advocacy groups is gradually reshaping perceptions and enlarging the penile implant market.

Competitive Landscape

Market Concentration

Boston Scientific and Coloplast hold a commanding yet not monopolistic position, leveraging broad portfolios, surgeon education, and continuous product refresh. Boston Scientific deepened its urology footprint with a USD 3.7 billion Axonics acquisition in November 2024, widening cross-selling opportunities. Recent launches such as the TENACIO pump and Tactra malleable device showcase relentless upgrade cycles that reinforce brand loyalty within the penile implant market.

Rigicon and International Medical Devices pursue share gains through niche innovation. Rigicon’s Infla10 emphasizes pump ergonomics and girth customization, targeting underserved patient feedback themes. International Medical Devices positions its Himplant subcutaneous solution for post-prostatectomy cosmetics, appealing to appearance-focused segments. FDA Quality System Regulation harmonization effective February 2026 may impose compliance costs that favor well-capitalized incumbents, yet smaller players leverage agility to address unmet needs.

Strategic moves include value-based contracting with large urology group practices, co-development of telemonitoring apps that track pump cycles and pressure, and geographic expansion into high-growth Asia-Pacific markets via distributor alliances. Overall, sustained R&D and service differentiation define competition, keeping the penile implant market dynamic and moderately consolidated.

Penile Implants Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Boston Scientific closed its USD 3.7 billion Axonics acquisition, adding sacral neuromodulation to its urology lineup

- November 2024: Boston Scientific commenced full market launch of the TENACIO pump for the AMS 700 system.

- October 2024: FDA’s MAUDE database logged a deflation failure in an AMS 700 LGX MS pump, prompting surgical replacement

Table of Contents for Penile Implants Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surge in post-prostatectomy ED cases

- 4.2.2Rising preference for outpatient implant surgery

- 4.2.3Technological shift to antibiotic-coated cylinders

- 4.2.4Growth of value-based urology reimbursement models (US & EU)

- 4.2.5Rapid expansion of specialised men’s-health clinics in Asia-Pacific

- 4.2.6Emerging demand from transgender masculinisation surgery

- 4.3Market Restraints

- 4.3.1High revision cost & limited insurance coverage

- 4.3.2Persistent mechanical failure rates of inflatable systems

- 4.3.3Urologist supply shortage in North America

- 4.3.4Cultural stigma limiting procedure uptake in MEA

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Type

- 5.1.1Inflatable Penile Implant

- 5.1.2Non-inflatable

- 5.2By Material

- 5.2.1Silicone-based Components

- 5.2.2Polyurethane & Other Polymers

- 5.2.3Metallic Components

- 5.3By Age Group

- 5.3.140–59 Years

- 5.3.260–69 Years

- 5.3.370+ Years

- 5.4By Patient Indication

- 5.4.1Post-Prostatectomy Erectile Dysfunction

- 5.4.2Neurogenic Erectile Dysfunction

- 5.4.3Diabetes-Related Erectile Dysfunction

- 5.4.4Peyronie’s Disease

- 5.4.5Other Etiologies

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1United Kingdom

- 5.5.2.2Germany

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4South America

- 5.5.4.1Brazil

- 5.5.4.2Argentina

- 5.5.4.3Rest of South America

- 5.5.5Middle East and Africa

- 5.5.5.1GCC

- 5.5.5.2South Africa

- 5.5.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Boston Scientific Corporation

- 6.3.2Coloplast A/S

- 6.3.3Zephyr Surgical Implants

- 6.3.4Promedon S.A.

- 6.3.5Rigicon Inc.

- 6.3.6Silimed

- 6.3.7Timm Medical (Endo Pharmaceuticals)

- 6.3.8G. Surgiwear Ltd

- 6.3.9Corza Medical

- 6.3.10Advin Health Care

- 6.3.11Osbon Medical

- 6.3.12Pos-T-Vac Inc.

- 6.3.13Reflexonic LLC

- 6.3.14Vacurect Pty Ltd

- 6.3.15Eska Medical GmbH

- 6.3.16Uro Mems

- 6.3.17Penuma Inc.

- 6.3.18Implantech

- 6.3.19ReShape Medical

- 6.3.20Andromeda Surgical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Penile Implants Market Report Scope

Penile Implants is a medical device that is used to treat male sexual conditions, like- erectile dysfunction, premature ejaculation, impotency, and several other problems are treated with the help of penile implants. It is inserted inside the penis through a surgical procedure.

The penile implants market is segmented by product, end user, and Geography. By Product, the market is segmented into inflatable penile implants, and non-inflatable penile implants. In terms of Materials, the market is segmented into silicon, bioflex and others. By end user the market is segmented into hospitals, specialty clinics, and others. By Geography the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.