Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.83 Billion |

| Market Size (2031) | USD 30.49 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

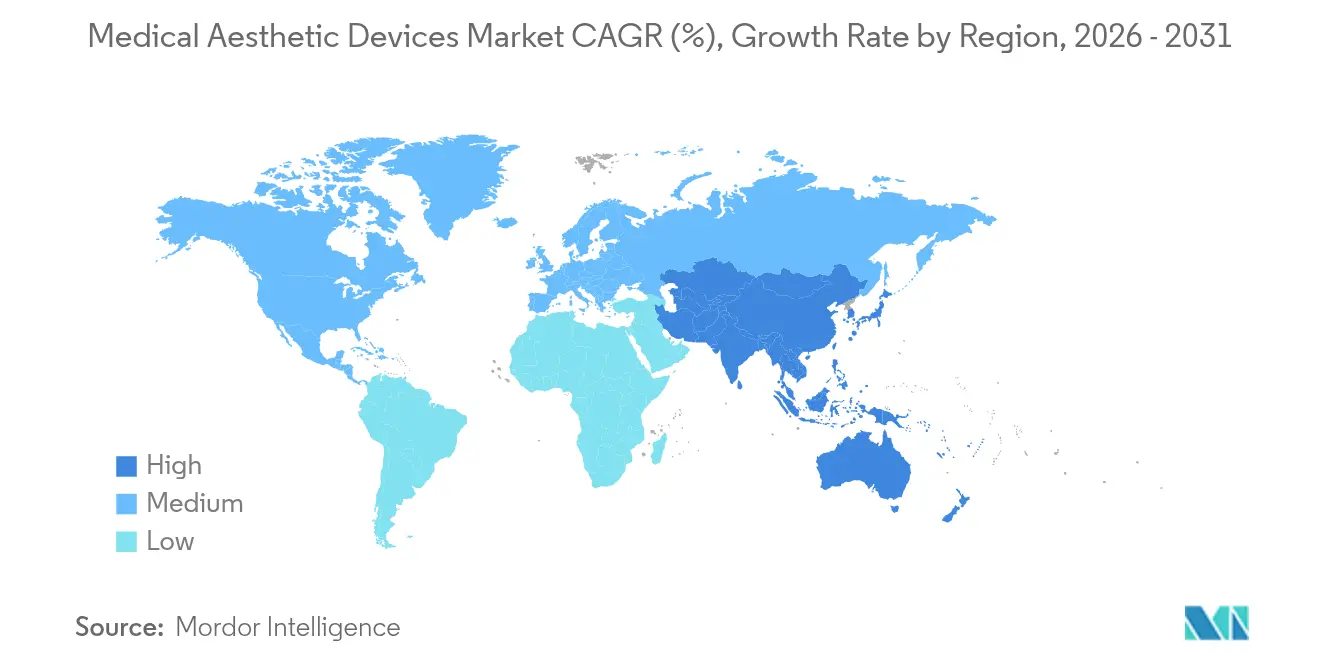

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

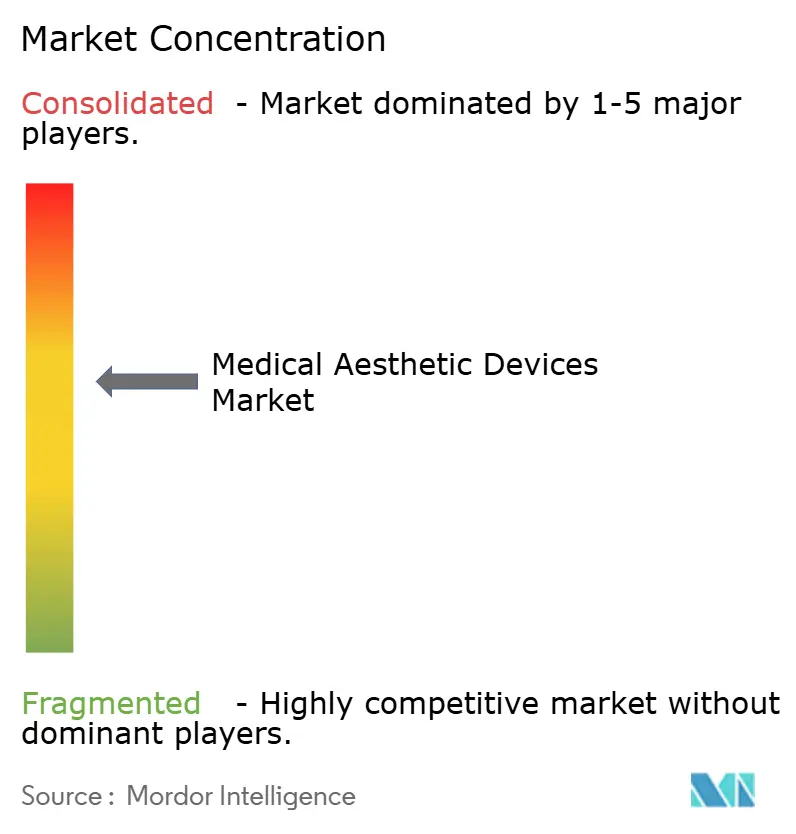

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Aesthetic Devices Market Analysis by Mordor Intelligence

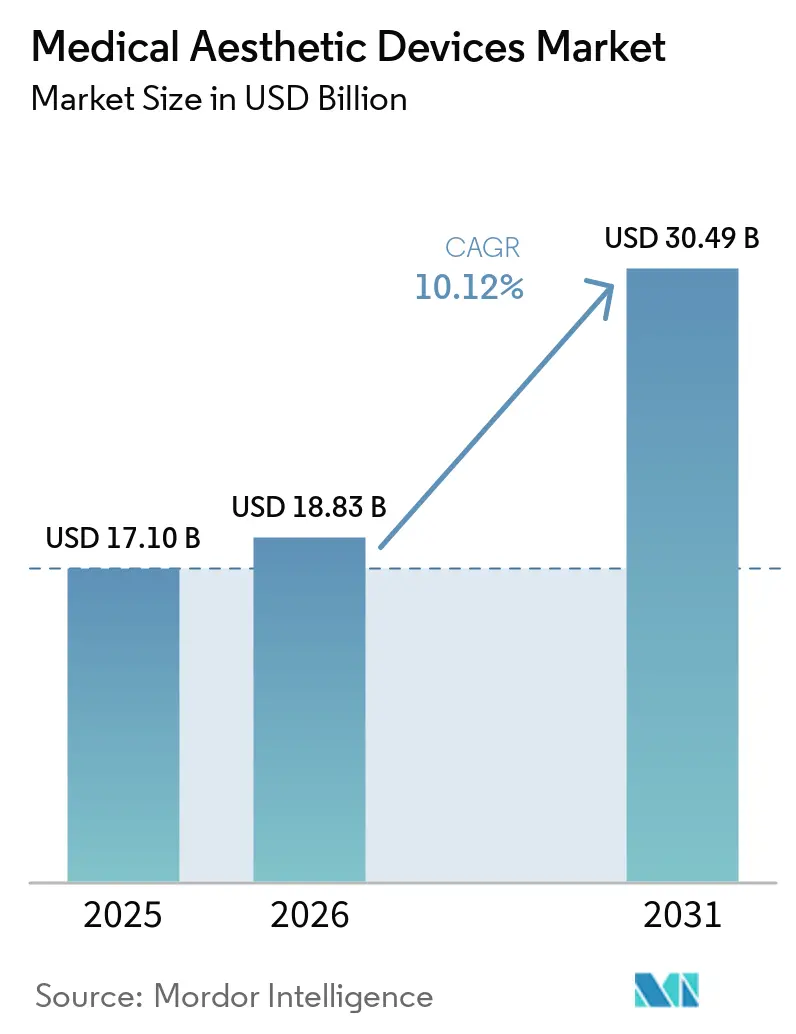

The medical aesthetic devices market size is expected to grow from USD 17.10 billion in 2025 to USD 18.83 billion in 2026 and is forecast to reach USD 30.49 billion by 2031 at 10.12% CAGR over 2026-2031. Continuous technology upgrades, rising disposable incomes, and wider consumer acceptance of minimally invasive cosmetic procedures underpin this momentum. Aging populations in developed economies and growing middle classes in emerging regions further amplify procedure volumes, while social-media visibility fuels awareness and demand. Device makers are quickening innovation cycles around energy delivery, AI-guided treatment protocols, and longer-lasting injectables, which together expand the addressable patient pool and shorten recovery times. Consolidation among leading manufacturers is accelerating, enabling broader product portfolios that blend laser, radiofrequency, ultrasound, and injectable solutions under single corporate umbrellas.

Key Report Takeaways

- By device type, energy-based platforms led with 52.12% revenue share in 2025, while non-energy devices are forecast to advance at a 12.31% CAGR through 2031.

- By procedure type, non-surgical treatments accounted for 55.32% of revenue in 2025, and surgical procedures are expected to grow at a 12.55% CAGR to 2031.

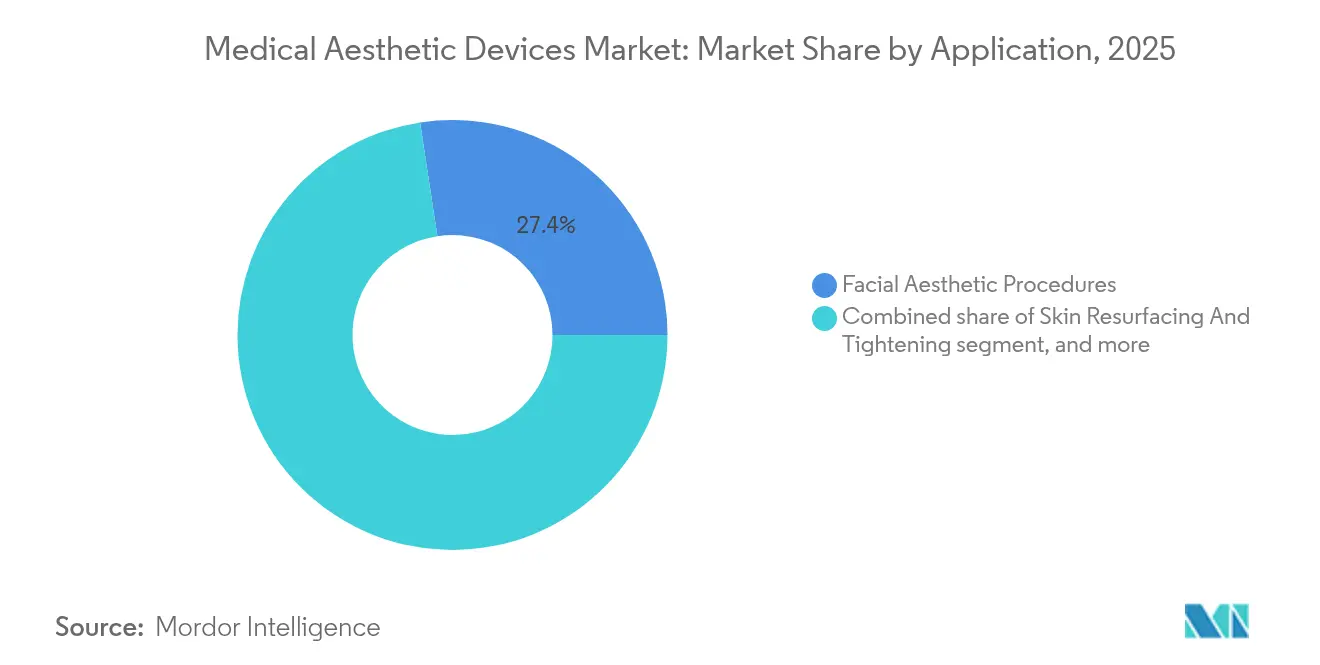

- By application, facial aesthetics captured 27.41% of spending in 2025, while body contouring is set to post a 13.29% CAGR through 2031.

- By end user, clinics and dermatology offices held 46.12% share in 2025, and medical spas are projected to expand at a 13.34% CAGR to 2031.

- By geography, North America commanded 42.02% of global revenue in 2025, whereas Asia-Pacific is expected to deliver an 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for minimally invasive procedures | +2.8% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Growing aging population and obesity rates | +2.1% | Developed markets worldwide | Long term (≥ 4 years) |

| Rising consumer awareness and acceptance of aesthetic treatments | +1.9% | Global, accelerating in Asia-Pacific | Short term (≤ 2 years) |

| Technological advancements in energy-based and injectable devices | +2.3% | Global, led by North American innovation hubs | Medium term (2-4 years) |

| Expansion of medical tourism hubs offering aesthetic services | +1.2% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Integration of digital marketing and social media influencers in patient acquisition | +0.9% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Minimally Invasive Procedures

Minimally invasive treatments continue to attract patients who value shorter recovery windows and lower risk profiles. U.S. data show that non-surgical options represented 54.9% of all aesthetic sessions in 2024, and 85% of surveyed consumers intend to maintain or boost spending even amid economic uncertainty. Younger adults now seek preventive neurotoxin injections, while male uptake of fillers and lasers keeps rising. Energy-based systems emulate surgical results by precisely targeting tissue layers without general anesthesia. Dermal fillers that retain volume for 12-18 months reinforce repeat-purchase behavior and strengthen provider loyalty. Collectively these factors raise treatment frequency and widen the customer base beyond traditional core segments.

Growing Aging Population and Obesity Rates

The 40-54 age bracket contributed 46.19% of U.S. aesthetic revenues in 2024 and is expanding at 13.9% CAGR as visible aging coincides with high earning power. Upticks in global obesity intensify demand for non-invasive body contouring tools that target stubborn adipose pockets. Injectable biostimulators restore facial fullness lost after weight-management therapeutics, as evidenced in recent Galderma trials that reported 89% patient satisfaction at three-month follow-up[1]Galderma Clinical Affairs, “SHAPE Up Interim Study Results,” galderma.com. Similar demographic shifts in East Asia, where populations age rapidly yet remain economically active, amplify regional procedure volume. These combined trends create a long-tail demand driver for both facial and body treatments.

Rising Consumer Awareness and Acceptance of Aesthetic Treatments

Social-media platforms normalize cosmetic interventions through real-time procedure videos and influencer testimonials. AI-enabled marketing suites adopted by medical spas personalize outreach and convert leads round-the-clock[2]American Med Spa Association, “2025 Medical Spa Industry Report,” amspa.org. Clinical studies show 92% post-treatment satisfaction when providers educate patients on expectations and safety measures. Transparent sharing of before-and-after imagery dispels myths, reduces treatment anxiety, and encourages multi-procedure journeys within single practices. This digital dialogue propels adoption across gender and age cohorts.

Technological Advancements in Energy-Based and Injectable Devices

D pipelines now blend AI, nanotechnology, and biomaterials to widen indications and deliver longer-lasting results. Face-conforming LED masks with high-density micro-LED arrays improve dermal elasticity compared with rigid predecessors. PEARL Technology extends neurotoxin longevity to six months, reducing patient visits and boosting practitioner productivity[3]Juvenology Clinic, “PEARL Technology Extends Botulinum Duration,” juvenologyclinic.com. Multi-modal radiofrequency platforms combine microneedling, heat, and ultrasound in single passes, cutting total treatment sessions in half while raising clinical outcomes. Injectable biostimulators that trigger endogenous collagen formation signal a pivot from temporary filling toward regenerative aesthetics.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure costs and limited insurance coverage | -1.8% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Stringent regulatory and safety compliance requirements | -1.2% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Workforce shortages of skilled aesthetic practitioners | -0.9% | Global, acute in rural and developing regions | Long term (≥ 4 years) |

| Environmental sustainability concerns around single-use consumables | -0.6% | Developed markets with strict environmental regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs and Limited Insurance Coverage

Aesthetic interventions are typically paid out-of-pocket, which limits uptake in low-income segments despite falling per-unit device costs. Financing schemes and installment plans are emerging, yet interest rates can deter price-sensitive prospects. Smaller clinics face steep capital requirements when acquiring new laser or body-sculpting platforms, which can cost over USD 150,000 each, concentrating market power among larger chains. Economic downturns heighten deferral of elective treatments, directly suppressing session volumes. Even in medical-tourism destinations, airfare and accommodation add to total spend, challenging affordability thresholds for many candidates.

Stringent Regulatory and Safety Compliance Requirements

The FDA will enforce ISO 13485:2016-aligned Quality System Regulation by February 2026, compelling manufacturers to overhaul documentation, risk management, and post-market surveillance. Similar tightening in the European Union under the Medical Device Regulation lengthens approval timelines and raises submission costs. Frequent safety advisories about counterfeit fillers or unlicensed practitioners raise public scrutiny, increasing compliance workloads for reputable clinics. These layers of oversight safeguard patients but can delay market entry for innovative startups with limited regulatory budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type Of Device: Diversification Beyond Energy Modalities

Energy-based platforms anchored the medical aesthetic devices market with 52.12% revenue share in 2025, underscoring the clinical trust built around lasers, radiofrequency, and ultrasound systems. The medical aesthetic devices market size for energy platforms is projected to remain dominant thanks to constant wavelength tuning and AI-guided protocols that personalize fluence levels for each tissue profile. Sales momentum also benefits from replacement-cycle dynamics as clinics upgrade to multi-modal consoles that combine skin resurfacing, tightening, and fat reduction in one footprint. In parallel, non-energy technologies such as fillers, neurotoxins, and thread lifts are growing faster at 12.31% CAGR, widening the total addressable base. These innovations rely on advanced biomaterials that trigger collagenesis, providing effects that can last 18 months and justify premium pricing. Longer duration means fewer clinic visits for patients and higher revenue per encounter for providers.

Combination therapies that marry fractional lasers with biostimulator injections further enhance outcomes, fostering cross-selling inside single appointments. Fragmentation persists among smaller device categories like microdermabrasion and light-emitting diode masks, yet even these niches attract consumer interest through lower price points and at-home variants. Competition now pivots toward integrated software that logs energy settings, tracks consumable usage, and supports remote diagnostics, helping clinics maximize device uptime. The medical aesthetic devices market will likely see increased collaboration between hardware makers and pharma firms to co-develop synergistic treatment protocols.

By Procedure Type: Surgical Techniques Regain Traction

Non-surgical approaches maintained 55.32% share of revenue in 2025 and remain attractive for their minimal downtime and reduced risk profiles. The medical aesthetic devices market share for these less invasive modalities is buoyed by broader candidacy across age groups and easier entry points for clinics lacking operating-room infrastructure. Yet surgical procedures are rebounding at 12.55% CAGR because micro-coring, endoscopic lifts, and laser-assisted lipolysis shorten convalescence and deliver longer-lasting results in a single session. Enhanced anesthesia methods reduce post-operative discomfort, while 3-D imaging improves pre-operative planning accuracy.

The line between surgical and non-surgical is blurring, with hybrid protocols that pair targeted fat removal with radiofrequency tightening during one visit. Patients who start with injectables often graduate to surgical lifts as aging progresses, creating lifecycle-long revenue opportunities for full-service practices. Clinics that offer both options retain patients and cross-refer internally, driving higher retention rates. Device makers develop accessories that make operating-room tools compatible with med-spa settings, widening the provider universe able to perform minimally invasive surgical work under local anesthesia.

By Application: Body Contouring Takes Center Stage

Facial aesthetics still contribute the largest slice of revenue at 27.41% in 2025, cementing their role as entry-level services that pull in new patients. Repeatable maintenance cycles for neurotoxins and fillers sustain cash flow and support upselling of adjunctive skin-rejuvenation packages. Nevertheless, body contouring now records the fastest 13.29% CAGR as obesity prevalence and social media favor sculpted silhouettes. The medical aesthetic devices market size for body contouring solutions is scaling quickly because cryolipolysis, monopolar radiofrequency, and high-intensity focused ultrasound promise visible inch loss without incisions.

Recent device generations integrate real-time temperature feedback and impedance monitoring, preventing overtreatment and lowering adverse event rates. Combined cellulite reduction and muscle-toning functionalities further elevate perceived value. While hair removal and skin resurfacing keep growing steadily, demand is gradually migrating toward multifunction consoles that can tackle pigment, texture, laxity, and vascular lesions in one setting. Emerging niches such as intimate wellness and scar management gain traction as patient openness expands and physicians seek portfolio diversification.

By End User: Experience-Driven Medical Spas Accelerate

Clinics and dermatology offices controlled 46.12% of global revenue in 2025 due to established medical reputations and access to prescription injectables. Their physician-led model reassures safety-conscious clients and accommodates complex cases. Meanwhile medical spas are rising at a 13.34% CAGR, powered by ambiance-rich facilities that fuse hospitality with clinical oversight. Loyalty programs, bundled packages, and AI-based scheduling enhance repeat visits and encourage multi-treatment adoption. The medical aesthetic devices market size within the spa channel is expanding as investors consolidate regional operators to form branded networks with shared procurement and marketing economies.

Hospitals continue to serve high-complexity reconstructive or surgical patients but increasingly carve out boutique aesthetic suites to tap elective revenue streams. Home-use devices approved by regulators for light hair removal or low-energy skin toning attract tech-savvy consumers yet often act as gateway products that push users toward in-clinic upgrades. Cross-channel synergies emerge as spas refer surgical candidates to partner surgeons, while clinics retail at-home maintenance tools to prolong in-office results.

Geography Analysis

North America retained 42.02% of revenue in 2025 as high discretionary incomes, a dense network of board-certified practitioners, and rapid product clearances converge. Domestic demand skews toward minimally invasive services, which account for 54.22% of sessions, reflecting patients’ preference for outcome-to-downtime efficiency. Federal reimbursement remains limited yet flexible financing models and loyalty plans cushion price sensitivity. Manufacturers tap U.S. innovation hubs to pilot AI-driven energy consoles and long-duration neuromodulators before global rollout, solidifying the region’s first-mover status.

Asia-Pacific is forecast to grow at 11.12% CAGR through 2031, moving the needle of the global medical aesthetic devices market. Regulatory reforms in China shorten device approval timelines, while rising middle-class purchasing power makes premium treatments attainable. South Korea’s K-beauty influence and Japan’s aging demographics boost filler and skin-tightening volumes. Regional medical tourism flows swell as Thailand and Malaysia offer bundled surgery plus recovery packages under internationally accredited clinics, though price competition remains intense.

Europe delivers steady expansion driven by Germany, France, and the United Kingdom, where public perception of aesthetics has shifted from vanity to self-care. Harmonized standards under the Medical Device Regulation support cross-border sales yet add compliance layers that raise entry costs. The Middle East builds luxury aesthetic centers to attract medical tourists, leveraging high disposable incomes and cultural acceptance of cosmetic enhancement. South America remains cost-competitive, with Brazil’s skilled surgeons and Colombia’s procedural value proposition drawing inbound patients. Emerging African economies are in early adoption phases but present long-term upside as urbanization and internet penetration spread awareness.

Competitive Landscape

The medical aesthetic devices market shows moderate consolidation, with top players leveraging acquisitions to secure technology breadth and distribution scale. Hahn & Company merged Cynosure and Lutronic to unite complementary laser portfolios and deepen Asian market reach. Crown Laboratories acquired Revance for USD 924 million, integrating DAXXIFY neuromodulator with microneedling and skincare lines to orchestrate full-patient-journey offerings. Galderma’s partnership with L’Oréal couples injectable expertise with skin-care science, accelerating anti-aging pipeline development.

Competitive advantages increasingly stem from proprietary software that guides treatment parameters based on real-time tissue feedback, reducing learning curves for new users. Firms incorporate cloud-based maintenance dashboards that predict consumable needs and schedule service visits, maximizing device uptime. Barriers to entry rise further as the FDA enforces ISO-aligned quality systems by 2026, favoring companies with mature compliance infrastructures. Startups gain traction by specializing in niche modalities such as regenerative aesthetics or eco-friendly consumables but often partner with incumbents for global distribution.

Price competition exists, yet providers focus more on outcome differentiation and patient experience than on equipment cost alone. Distributors expand value-added services like clinical education, marketing support, and financing solutions to lock in brand loyalty. Synergies between prescription dermatology, over-the-counter cosmeceuticals, and device treatments create omnichannel revenue streams, reducing reliance on any single product line.

Medical Aesthetic Devices Industry Leaders

Cynosure

Abbvie Inc.(Allergan plc)

Alma Lasers (Sisram Med)

Bausch Health Companies Inc. (Solta Medical Inc.)

Johnson & Johnson Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Acclaro Medical secured USD 23 million in Series B funding to advance next-generation skin lasers.

- April 2025: FDA cleared Evolysse Form and Evolysse Smooth hyaluronic acid fillers for nasolabial fold correction, marking Evolus’s debut in fillers.

- March 2025: Cytrellis Biosystems gained Canadian and Saudi approvals for the ellacor micro-coring system, expanding its global footprint.

- March 2025: Johnson & Johnson MedTech launched a U.K. recycling program for single-use medical products, supporting hospital sustainability targets.

- August 2024: Crown Laboratories and Revance finalized a USD 924 million merger to create a comprehensive aesthetics portfolio.

- June 2024: FDA approved Letybo for moderate-to-severe glabellar lines following positive phase III data.

Global Medical Aesthetic Devices Market Report Scope

As per the scope of the report, medical aesthetic devices refer to all medical devices that are used for various cosmetic procedures, which include plastic surgery, unwanted hair removal, excess fat removal, anti-aging, aesthetic implants, skin tightening, etc., that are used for beautification, correction, and improvement of the body.

The medical aesthetic devices market is segmented by type of device, application, end user, and geography. By type of device, the market is segmented into energy-based aesthetic devices and non-energy-based aesthetic devices. For energy-based aesthetic devices, the market is sub-segmented into laser-based aesthetic devices, radiofrequency (RF)-based, light-based, and ultrasound aesthetic devices. By non-energy-based aesthetic devices, the market is sub-segmented into botulinum toxin, dermal fillers and aesthetic threads, chemical peels, microdermabrasion, implants, and other aesthetic devices. By implants, the market is sub-segmented into facial implants, breast implants, and other implants. By application, the market is segmented into skin resurfacing and tightening, body contouring and cellulite reduction, hair removal, facial aesthetic procedures, breast augmentation, and other applications. By end user, the market is segmented into hospitals, clinics, and home settings. For each segment, the market size is provided in terms of value (USD).

By Type Of Device

| Energy-Based Aesthetic Devices | Laser-Based Aesthetic Devices |

| Radiofrequency-Based Aesthetic Devices | |

| Light-Based Aesthetic Devices | |

| Ultrasound-Based Aesthetic Devices | |

| Non-Energy-Based Aesthetic Devices | Botulinum Toxin |

| Dermal Fillers And Threads | |

| Microdermabrasion | |

| Implants | |

| Other Aesthetic Devices |

By Procedure Type

| Non-Surgical / Minimally Invasive |

| Surgical |

By Application

| Skin Resurfacing And Tightening |

| Body Contouring And Cellulite Reduction |

| Hair Removal |

| Facial Aesthetic Procedures |

| Breast Augmentation |

| Other Applications |

By End User

| Hospitals |

| Clinics And Dermatology Offices |

| Medical Spas |

| Home Settings |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type Of Device | Energy-Based Aesthetic Devices | Laser-Based Aesthetic Devices |

| Radiofrequency-Based Aesthetic Devices | ||

| Light-Based Aesthetic Devices | ||

| Ultrasound-Based Aesthetic Devices | ||

| Non-Energy-Based Aesthetic Devices | Botulinum Toxin | |

| Dermal Fillers And Threads | ||

| Microdermabrasion | ||

| Implants | ||

| Other Aesthetic Devices | ||

| By Procedure Type | Non-Surgical / Minimally Invasive | |

| Surgical | ||

| By Application | Skin Resurfacing And Tightening | |

| Body Contouring And Cellulite Reduction | ||

| Hair Removal | ||

| Facial Aesthetic Procedures | ||

| Breast Augmentation | ||

| Other Applications | ||

| By End User | Hospitals | |

| Clinics And Dermatology Offices | ||

| Medical Spas | ||

| Home Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the medical aesthetic devices market in 2026?

The medical aesthetic devices market size is USD 18.83 billion in 2026 and is forecast to reach USD 30.49 billion by 2031.

Which device category dominates global revenue?

Energy-based platforms, including lasers and radiofrequency systems, held 52.12% of 2025 revenue.

What is the fastest growing procedure type?

Surgical procedures, propelled by less invasive techniques like micro-coring, are projected to expand at 12.55% CAGR through 2031.

Which region offers the highest growth outlook?

Asia-Pacific leads with an expected 11.12% CAGR as regulatory reforms and rising incomes spur adoption.

Why are medical spas gaining popularity?

Medical spas blend hospitality with physician oversight and are forecast to grow 13.34% CAGR by integrating advanced devices and personalized digital marketing.

How will new FDA quality rules affect manufacturers?

The 2026 shift to ISO 13485-aligned regulations will increase compliance costs, favoring companies with robust quality infrastructures.

Page last updated on: