Medical Physics Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 5.92 Billion |

| Market Size (2031) | USD 8.06 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

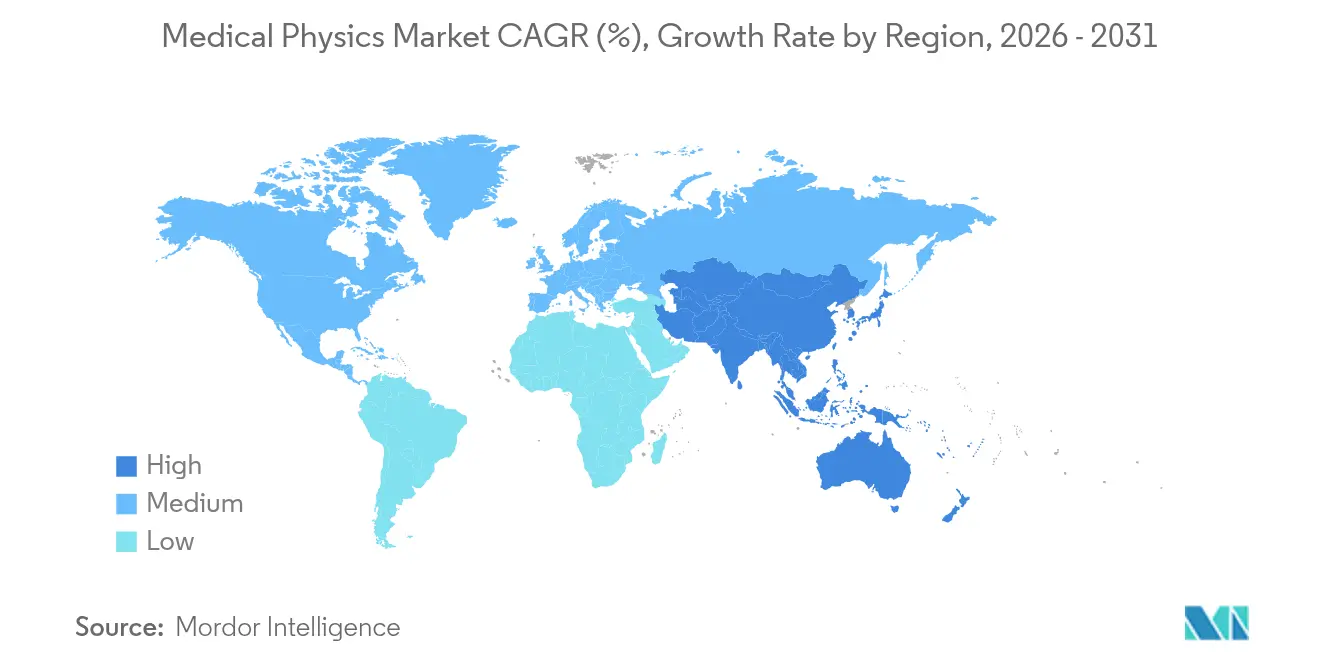

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Physics Market Analysis by Mordor Intelligence

The medical physics market size in 2026 is estimated at USD 5.92 billion, growing from 2025 value of USD 5.57 billion with 2031 projections showing USD 8.06 billion, growing at 6.36% CAGR over 2026-2031. Rising global cancer cases, rapid diffusion of high-precision proton therapy, and continuous upgrades in diagnostic imaging technologies underpin steady revenue expansion. Healthcare providers are accelerating capital spending on photon-counting CT, MR-guided linear accelerators, and AI-driven quality-assurance platforms, all of which increase demand for certified medical physicists. Vendors respond through vertical integration, software-hardware interoperability, and cloud analytics that enable remote equipment monitoring and predictive maintenance. Regional growth patterns remain uneven: while North America retains the largest share, Asia-Pacific delivers the quickest incremental gains as China and India add oncology capacity. Persistent workforce shortages, complex regulatory approvals, and high capital costs temper near-term momentum yet drive service consolidation and technology-enabled outsourcing models.

Key Report Takeaways

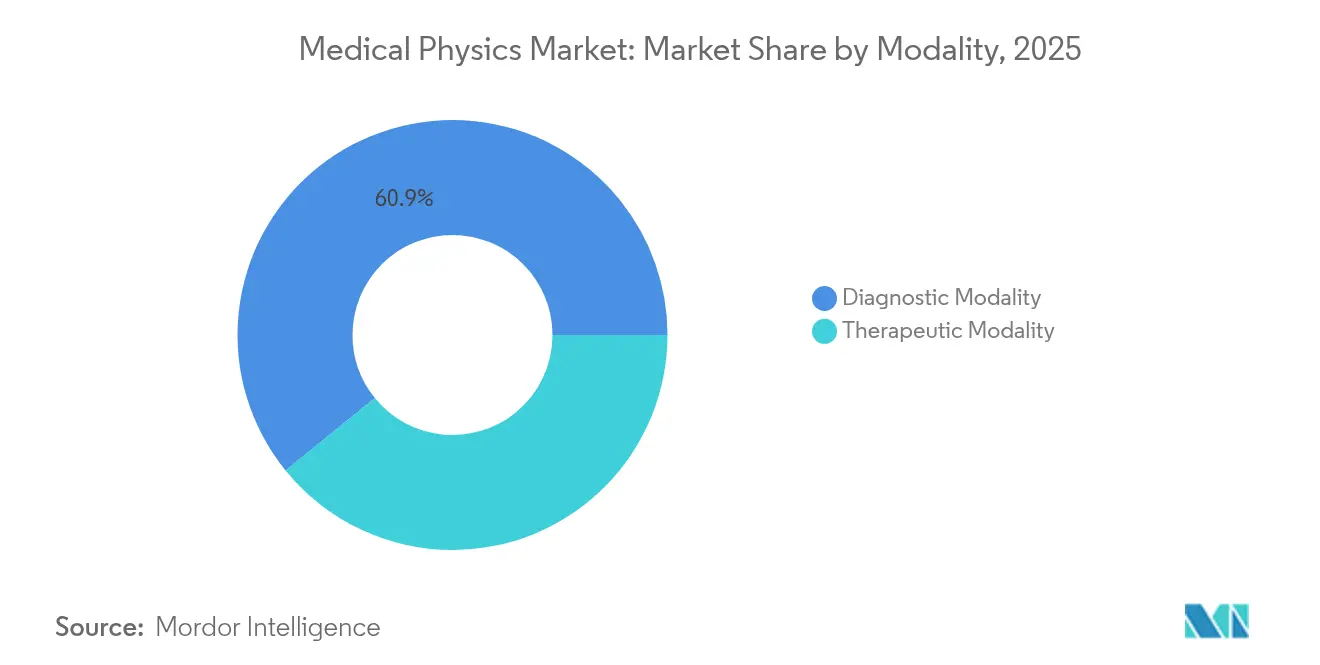

- By modality, diagnostic imaging held 60.85% of medical physics market share in 2025, while proton therapy is advancing at an 8.02% CAGR toward 2031.

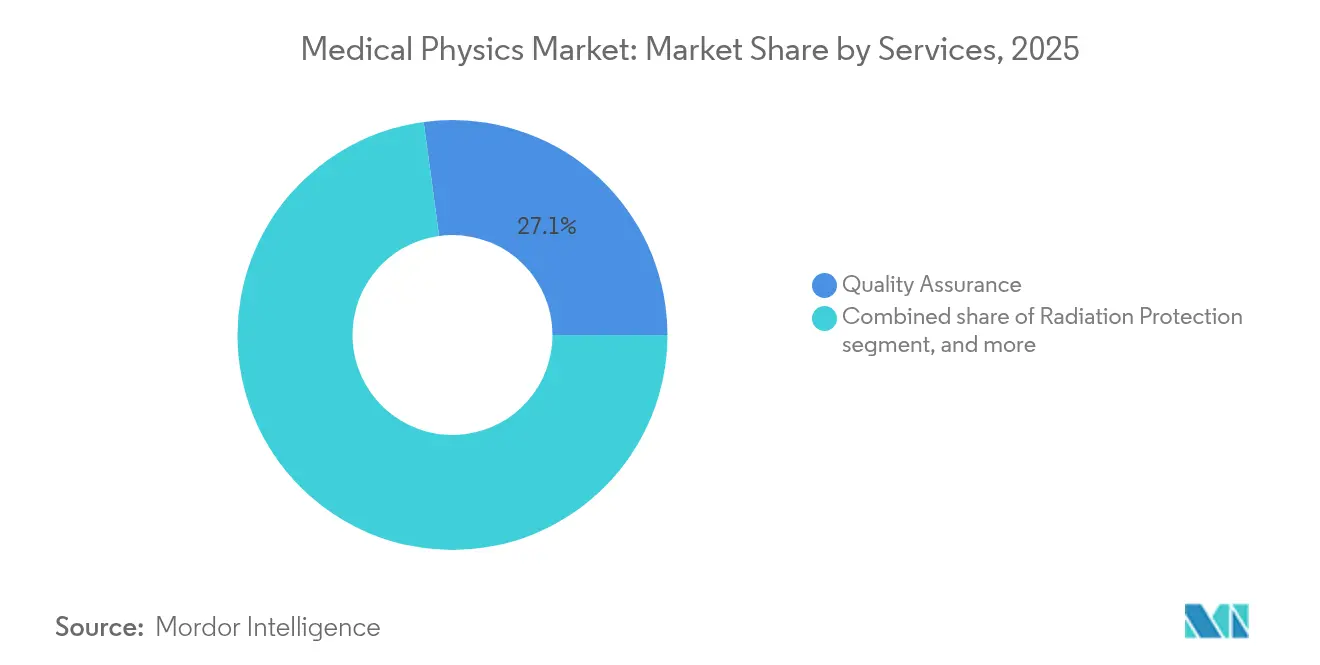

- By service, quality assurance accounted for 27.14% of the medical physics market size in 2025; nuclear medicine physics services post the fastest growth at an 8.35% CAGR through 2031.

- By end user, hospitals controlled 53.43% of medical physics market share in 2025, whereas specialized cancer centers are expanding at a 9.12% CAGR.

- By geography, North America led with 40.84% revenue share in 2025, yet Asia-Pacific is projected to grow at a 7.12% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Physics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cancer Incidence And Chronic Disease Burden | +1.8% | Global, highest in APAC & MEA | Long term (≥ 4 years) |

| Technological Advancements In Diagnostic And Therapeutic Modalities | +1.2% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Government Funding And Reimbursement Support For Radiation Therapy | +0.9% | North America & EU core, selective APAC markets | Medium term (2-4 years) |

| Integration Of Artificial Intelligence For Quality Assurance Automation | +0.7% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Expansion Of Outpatient Proton Therapy And Radiosurgery Centers | +0.5% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Growing Adoption Of Radiotheranostics In Precision Oncology | +0.4% | Global, with regulatory variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cancer Incidence and Chronic Disease Burden

Global oncology cases are expected to reach 24 million annually by 2030, creating sustained demand for radiation-based diagnostics and therapies and thereby lifting the medical physics market. Capacity gaps remain stark: Asia-Pacific reports a 43% shortage of qualified medical physicists relative to projected treatment needs, forcing providers to accelerate facility construction, expand training programs, and adopt telephysics services[1]Journal of Cancer Research and Therapeutics, “Medical Physics Workforce Projections 2025,” jcrtf.org. The shift toward precision oncology raises the complexity of dose optimization, driving adoption of adaptive planning and real-time verification tools. Beyond oncology, increased usage of cardiovascular and neurologic imaging widens the clinical footprint of ionizing-radiation modalities, reinforcing the need for rigorous quality and safety protocols.

Technological Advancements in Diagnostic and Therapeutic Modalities

AI-assisted planning platforms such as GPT-RadPlan now routinely outperform manual plans in target coverage, cutting optimization time from hours to minutes. Photon-counting CT lowers patient dose by up to 80% while preserving image quality, expanding its utility in routine diagnostics. Biology-guided radiotherapy, exemplified by the RefleXion X1, enables continuous tumor tracking during dose delivery, marking a shift from anatomy-centric to biology-centric targeting. Vendors couple these innovations with cloud analytics to facilitate remote performance monitoring and proactive maintenance, crucial for resource-constrained settings. Continuous professional-development requirements grow as physicists must stay current on complex hybrid systems and interoperability standards.

Government Funding and Reimbursement Support for Radiation Therapy

U.S. Medicare’s 2025 Physician Fee Schedule trimmed conversion factors by 2.83%, pressuring oncology margins but intensifying lobbying for the Radiation Oncology Case Rate Act, which could stabilize payments and link them to quality metrics[2]American Society for Radiation Oncology, “2025 Medicare Final Rule Analysis,” astro.org. Canada committed CAD 289 million (USD 213 million) to new proton facilities, illustrating direct government backing for capital-intensive technologies. In Europe, the SAMIRA Action Plan channels resources into radioisotope supply chains and harmonized QA frameworks to safeguard continuity of care. Such funding buffers capital constraints and secures long-term demand for medical physics expertise, although reimbursement volatility still dictates adoption speed for premium technologies such as MR-Linacs.

Integration of Artificial Intelligence for Quality-Assurance Automation

Automated QA platforms now analyze beam parameters in real time, highlighting deviations before patient exposure and reducing routine manual checks by up to 70%. Large-scale prescription-checking systems processed 24,000 treatment orders, with 31% of alerts preventing potential errors, underscoring tangible safety benefits[3]Practical Radiation Oncology, “Automated Prescription Checking,” practicalradonc.org. Privacy-preserving, on-premises large language models optimize treatment parameters without external data transfer, alleviating cybersecurity concerns and aligning with emerging FDA guidelines. While AI relieves workload pressures, validation across diverse clinical scenarios and maintaining algorithm transparency remain pivotal to regulatory acceptance.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Maintenance Costs Of Advanced Equipment | -1.1% | Global, higher impact in emerging markets | Long term (≥ 4 years) |

| Stringent Regulatory And Safety Compliance Requirements | -0.8% | Global, with varying regional intensity | Medium term (2-4 years) |

| Shortage Of Certified Medical Physicists In Emerging Markets | -0.6% | Emerging markets in APAC, MEA & LATAM | Long term (≥ 4 years) |

| Vulnerability Of Imaging IT Networks To Cybersecurity Threats | -0.4% | Global, especially in high-connectivity regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Advanced Equipment

Hospitals spend USD 93 billion annually on medical equipment but forgo 12-16% in potential savings due to poor lifecycle management. A single-room proton therapy suite costs USD 40–50 million, excluding annual service contracts, creating adoption barriers for mid-tier hospitals. AI-enabled MR-Linacs command premium pricing and require continuous software licensure, cybersecurity updates, and specialized staffing, swelling total cost of ownership. Leasing and vendor-managed-service models gain popularity as providers seek to spread capital outlays while securing technology refresh rights.

Stringent Regulatory and Safety Compliance Requirements

The FDA’s 2025 cybersecurity rule obliges manufacturers to embed risk-management and post-market surveillance features in connected devices, lengthening approval cycles and raising development costs. Europe’s updated Ionising Radiation Medical Exposure Regulations mandate enhanced diagnostic-reference-level tracking and audit documentation, adding administrative burden for providers. Divergent radiopharmaceutical standards across EU member states complicate cross-border service delivery, while AI-driven systems must undergo extensive software-validation trials to demonstrate consistent, bias-free performance. Cumulatively, these layers slow market entry for cutting-edge solutions and elevate compliance spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Diagnostic Dominance Drives Infrastructure Investment

Diagnostic imaging maintained 60.85% of medical physics market share in 2025 on the back of heightened demand for CT, MRI, and nuclear medicine scans. Advanced photon-counting detectors improve spatial resolution while trimming dose, thereby reinforcing computed tomography’s central role in fast-turnaround diagnostics. Parallel momentum in nuclear medicine stems from theranostic tracers that fuse imaging and therapy, spurring expansion of cyclotron capacity and specialized dosimetry services.

The therapeutic segment still draws the bulk of infrastructure budgets. External-beam radiation therapy contributes the largest revenue pool, yet proton therapy registers an 8.02% CAGR through 2031—the highest among all modalities—driven by favorable pediatric outcomes and growing adult indications such as head-and-neck and pancreatic cancers. MR-guided linear accelerators epitomize modality convergence: their embedded 1.5T magnets furnish on-table volumetric imaging, enabling real-time adaptive planning. Vendors therefore design integrated workflows that harmonize diagnostic acquisition with therapeutic execution, minimizing patient transfer and enhancing throughput.

By Services: Quality Assurance Leadership Amid Nuclear Medicine Expansion

Quality-assurance activities accounted for 27.14% of the services-segment medical physics market size in 2025, reflecting regulatory mandates for periodic equipment calibration and treatment-plan verification. AI-driven analytics now benchmark beam constancy and offer predictive alerts for component wear, reducing downtime and ensuring clinical accreditation compliance.

Nuclear-medicine physics services outpace all others at an 8.35% CAGR through 2031 as alpha-emitting radiotherapeutics migrate from trials into routine care. These therapies require individualized voxel-level dosimetry and elaborate radiation-safety protocols, pushing demand for highly specialized physicists. Meanwhile, imaging-physics consulting gains share as outpatient centers outsource complex acceptance testing and optimization tasks. The persistent talent gap triggers consolidation: large service organizations leverage cloud dashboards and remote QA to support satellite clinics, sustaining quality across geographically distributed networks.

By End User: Hospital Dominance Challenged by Specialized Center Growth

Hospitals captured 53.43% medical physics market share in 2025 because they house multidisciplinary teams and capital-intensive equipment. However, budget constraints and throughput pressures spur outsourcing of niche tasks like stereotactic QA to specialist firms. Academic medical centers continue to pilot novel technologies, acting as reference sites for vendors and influencing community adoption.

Dedicated oncology centers exhibit a 9.12% CAGR to 2031 as health systems deploy hub-and-spoke models that centralize high-complexity modalities while extending routine services through satellites. Such facilities integrate imaging, planning, and treatment within compact footprints, optimizing patient flow and leveraging tele-physics oversight. Independent imaging centers also gain traction through extended-hour operations and rapid-turnaround exams, though they remain reliant on mobile physicist pools for periodic compliance audits and accreditation renewal.

Geography Analysis

North America retained 40.84% medical physics market share in 2025, buoyed by early adoption of MR-Linacs, robust reimbursement codes, and a dense physicist workforce. Yet reimbursement cuts spur providers to streamline workflows and pursue operational partnerships that soften capital burdens.

Europe follows with strong governmental support and centralized procurement that accelerates technology rollout. Programs like the EUR-funded SAMIRA initiative secure radioisotope supply and harmonize QA guidelines, smoothing access to theranostic agents. Nevertheless, divergent reimbursement mechanisms across member states influence uptake of high-cost modalities and shape region-specific business models.

Asia-Pacific posts the fastest growth at a 7.12% CAGR through 2031, propelled by national cancer-control plans in China and India, plus Japan’s USD 112 billion precision-medicine agenda. China now hosts more than 1,200 nuclear-medicine hospitals delivering nearly 4 million procedures annually, creating a fertile market for dosimetry software and remote QA. Workforce shortages remain acute, prompting vendor-led training alliances and government scholarships that expand physicist pipelines. Southeast Asian countries prioritize smaller-footprint linacs and refurb-lease agreements to bridge budget gaps while adopting advanced planning software delivered via secure cloud.

Competitive Landscape

The medical physics market is moderately consolidated as imaging giants integrate vertically to capture service revenue. Siemens Healthineers’ USD 16 billion acquisition of Varian generates EUR 300 million in annual synergies by blending diagnostic imaging with radiation-therapy portfolios. GE HealthCare’s 2025 purchase of MIM Software widens its AI arsenal across oncology and neurology, strengthening end-to-end workflows from acquisition to follow-up. Elekta’s co-development pact with Sun Nuclear embeds QA into treatment-delivery ecosystems, underscoring the strategic value of software differentiation.

Service providers also scale rapidly: West Physics’ buy-out of Tricord enlarged its diagnostic-physics footprint, making it the largest U.S. player by covered sites. Emerging start-ups such as RefleXion and ViewRay challenge incumbents with biology-guided therapy and MR-Linac niches, nudging established vendors to accelerate R&D. The radiopharmaceutical field attracts venture inflows as alpha-emitter supply chains mature, expanding addressable service demand for isotope handling and patient-specific dosimetry.

White-space opportunities concentrate around AI-enabled QA, remote plan review, and cybersecurity consulting. Providers harness cloud dashboards to unify data from geographically dispersed linacs, enabling centralized oversight and reducing on-site staffing requirements—especially vital in APAC, where physicist availability lags demand by 43%.

Medical Physics Industry Leaders

Siemens Healthineers

Elekta AB

GE Healthcare

LANDAUER

Alyzen Medical Physics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBA introduced the myQA Blue Phantom³ water phantom with real-time contactless positioning at ESTRO 2025, improving beam-data acquisition speed.

- March 2025: Canon Medical Systems USA received FDA clearance for the Adora DRFi automated hybrid radiography-fluoroscopy suite, boosting workflow efficiency.

- February 2025: Varian secured FDA 510(k) for RapidArc Dynamic, offering 70% faster optimization and up to 50% dose reduction to organs at risk.

- February 2025: Varian allied with Sun Nuclear, integrating SunCHECK QA across 6,000 global cancer centers.

- January 2025: GE HealthCare finalized its acquisition of MIM Software, enhancing multimodality image-analysis capabilities.

- April 2024: Hologic acquired Endomag for USD 310 million, while West Physics purchased Tricord’s medical-physics unit to widen U.S. diagnostic-testing coverage.

Global Medical Physics Market Report Scope

As per the scope of the report, medical physics is the application of physics to healthcare using physics for patient imaging, measurement, and treatment. It comprises the science of human health and radiation exposure.

The medical physics market is segmented by modality, services, end user, and geography. By modality, the market is segmented into diagnostic modality and therapeutic modality. By diagnostic modality, the market is segmented into X-ray, computed tomography, magnetic resonance imaging, ultrasound, nuclear medicine, and mammography. By therapeutic modality, the market is divided into external beam radiation therapy, brachytherapy, proton therapy, stereotactic radiosurgery, and stereotactic body radiation therapy. By services, the market is segmented into radiation protection, quality assurance, regulatory compliance, medical imaging, nuclear medicine services, and radiation therapy services. By end user, the market is segmented into hospitals, diagnostic imaging centers, cancer treatment centers, and other end users. Other end users include clinics, outpatient facilities, and other medical services providers. The geography segment is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America.

For each segment, the market sizing and forecasts were made on the basis of value (in USD).

| Diagnostic Modality | X-ray |

| Computed Tomography | |

| Magnetic Resonance Imaging | |

| Ultrasound | |

| Nuclear Medicine | |

| Mammography | |

| Therapeutic Modality | External Beam Radiation Therapy |

| Brachytherapy | |

| Proton Therapy | |

| Stereotactic Radiosurgery | |

| Stereotactic Body Radiation Therapy |

| Radiation Protection |

| Quality Assurance |

| Regulatory Compliance |

| Medical Imaging Physics |

| Nuclear Medicine Physics |

| Radiation Therapy Physics |

| Hospitals |

| Diagnostic Imaging Centers |

| Cancer Treatment Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Diagnostic Modality | X-ray |

| Computed Tomography | ||

| Magnetic Resonance Imaging | ||

| Ultrasound | ||

| Nuclear Medicine | ||

| Mammography | ||

| Therapeutic Modality | External Beam Radiation Therapy | |

| Brachytherapy | ||

| Proton Therapy | ||

| Stereotactic Radiosurgery | ||

| Stereotactic Body Radiation Therapy | ||

| By Services | Radiation Protection | |

| Quality Assurance | ||

| Regulatory Compliance | ||

| Medical Imaging Physics | ||

| Nuclear Medicine Physics | ||

| Radiation Therapy Physics | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Cancer Treatment Centers | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected revenue for medical physics in 2031?

The market is forecast to reach USD 8.06 billion by 2031.

Which modality is growing the fastest?

Proton therapy shows the highest growth with an 8.02% CAGR through 2031.

How large is the current diagnostic-imaging share?

Diagnostic modalities hold 60.85% of 2025 revenue.

Which region is expanding most rapidly?

Asia-Pacific leads with a projected 7.12% CAGR to 2031.

Why is AI important in medical physics?

AI automates quality assurance, cuts treatment-planning time, and improves safety, mitigating workforce shortages.

What factors restrain technology adoption?

High capital costs and stringent regulatory compliance slow uptake of advanced equipment.

Page last updated on: